Новости

Эксклюзивные аналитические статьи с последними обновлениями рынка и своевременными новостными лентами.

![[SMM анализ] Новый налог на потребление литиевых батарей в Китае: влияние на сектор переработанных ресурсов](https://imgqn.smm.cn/usercenter/zWZVI20251217171730.jpg)

[SMM анализ] Новый налог на потребление литиевых батарей в Китае: влияние на сектор переработанных ресурсов

Объявление № 20 от 2026 года официально вступило в силу, уточняя, что Китай возобновит взимание налога на потребление с литий-ионных аккумуляторов с 1 сентября 2026 года. Политика предусматривает ступенчатую шкалу налоговых ставок: период с сентября 2026 года по август 2027 года станет переходным, и ставка налога на потребление составит 2%; с 1 сентября 2027 года ставка будет официально повышена до 4%.

28 Jul 2026 14:26

[Анализ SMM] Почему Индия становится активным покупателем на мировом рынке медного лома?

[Анализ SMM: Почему Индия может сохранять высокие ставки на импортный медный лом?] Импорт медного лома в Индию растет, поскольку внутреннее предложение не удовлетворяет растущий спрос со стороны электросетей, кабельной промышленности и производства. Нулевая базовая таможенная пошлина, гибкая переработка, низкие затраты на переработку и преимущества по стоимости фрахта позволяют делать более высокие заявки. Однако ограниченное глобальное предложение и повышенные выплаты могут продолжить сжимать маржу.

27 Jul 2026 15:45

Индонезия, как сообщается, задержала груз глинозема из-за редкоземельных металлов. Вот что на самом деле говорят правила

Сообщается, что партия глинозёма, задержанная индонезийской таможней, привлекла внимание к возможным регуляторным последствиям обнаружения редкоземельных элементов в глинозёме. Это оставляет вопросы о том, как эти нормативные акты могут применяться в случаях, когда в глинозёме, в остальном соответствующем требованиям, выявляется измеримое содержание редкоземельных элементов.

27 Jul 2026 15:22

Последние новости

UBS прогнозирует избыток на рынке палладия и снижает прогноз цен до 1100 долларов США за унцию

31 Jul 2026 20:57

Платина держится выше $1600/унц., поскольку покупательский интерес компенсирует давление продаж.

31 Jul 2026 20:35

ARM продвигает проекты Бокони и Нкомати, несмотря на неоднозначные настроения инвесторов.

31 Jul 2026 20:20

[SMM Экспресс драгоценных металлов]

SMM сообщило 31 июля, что в июле 2026 года производство нитрата серебра SMM достигло 646 тонн, что на 11,0% м/м и на 28,93% г/г меньше, в основном из-за осторожного планирования выпуска на предприятиях солнечных элементов, слабых заказов на заводах серебряной пасты и ослабления передачи спроса со стороны потребителей нитрата серебра; в сочетании с продолжающимся внедрением технологий снижения использования серебра в фотоэлектрике спрос на серебро в отрасли снижался. Резкое сокращение в годовом выражении было обусловлено высокой базой спроса в аналогичном периоде прошлого года в сочетании с продолжающимся снижением использования серебра в фотоэлектрическом секторе.

31 Jul 2026 18:31

SMM: В июле 2026 года производство серебряных слитков сократилось, запасы выросли из-за ремонта на плавильных заводах.

[SMM Silver Express] СММ, 31 июля: производство серебра в слитках SMM 1# в июле 2026 года составило 1 556 тонн, что на 0,38% меньше, чем в предыдущем месяце, и на 3,59% меньше, чем в аналогичном периоде прошлого года; совокупный рост за первые семь месяцев составил 5,3%. Запасы производителей выросли на 22,2% по сравнению с предыдущим месяцем. Снижение в основном обусловлено плановыми ремонтами на медеплавильных, свинцовых и цинковых заводах, при этом часть запасов была зарезервирована для экспорта в рамках перерабатывающей торговли.

31 Jul 2026 18:08

Золото и серебро во время рецессии: как на самом деле ведут себя драгоценные металлы?

31 Jul 2026 17:27

Xingye Silver & Tin: Yinman Mining приостановила как свою добычную систему, так и систему обогащения хвостов.

31 Jul 2026 16:47

Цены на платину устойчивы, пополнение запасов у потребителей достаточное, на спотовом рынке слабые и спрос, и предложение [Ежедневный комментарий SMM]

31 Jul 2026 13:48

Ослабление доллара США и охлаждение PCE резонируют, серебро продолжает консолидироваться на минимумах [Ежедневный обзор SMM]

[Ежедневный обзор SMM: Ослабление доллара и снижение PCE резонируют, цены на серебро продолжают консолидацию на минимумах] Новости SMM от 31 июля: доллар упал ниже 100, PCE снизился, но условия для изменения тренда повышения ставок не сложились, и цены на серебро консолидировались. Спотовые поставки и спрос ослабли в конце месяца, сделки были вялыми. В центре внимания — ремонтные работы и восстановление спроса в следующем месяце.

31 Jul 2026 10:25

Implats приостанавливает работу платинового рудника Рюстенбург после того, как смертельные случаи вызвали проверку безопасности.

Impala Platinum Holdings (Implats) временно приостановила горные работы на своем флагманском комплексе Rustenburg в Южной Африке после шести смертельных случаев с работниками за последний год и роста числа серьезных инцидентов с безопасностью на подземных работах. Компания провела комплексную перезагрузку мер безопасности с 24 по 28 июля для усиления операционного контроля и предотвращения дальнейших происшествий.

Rustenburg — один из крупнейших в мире горнодобывающих комплексов по добыче металлов платиновой группы (МПГ) и крупнейшее предприятие Implats, на котором занято около 51 500 работников. На его долю приходится почти половина всего производства МПГ компании, и ожидается, что в 2026 финансовом году здесь будет произведено около 1,67–1,76 млн шестиэлементных унций МПГ.

Ожидается, что временная остановка повлияет на объем добычи примерно за восемь дней, при этом окончательное влияние на выпуск будет оценено после возобновления работ. Предполагается, что существующие складские запасы помогут смягчить любое краткосрочное воздействие на поставки.

Краткосрочное влияние на мировые поставки платины, как ожидается, останется ограниченным из-за непродолжительной остановки и доступных запасов. Однако возобновившиеся опасения по поводу безопасности на крупных южноафриканских предприятиях могут оказать дополнительную поддержку ценам на платину, подчеркивая потенциальные риски со стороны предложения, с которыми сталкивается ведущий регион мира по добыче МПГ.

30 Jul 2026 22:04

Ожидается, что рынок рутениево-иридиевых титановых анодов более чем удвоится к 2034 году

30 Jul 2026 19:21

Chifeng Gold: Ожидается, что проект SND на золотомедном руднике Сепон в Лаосе увеличит содержание металла в золотом эквиваленте до 260 метрических тонн

30 Jul 2026 18:13

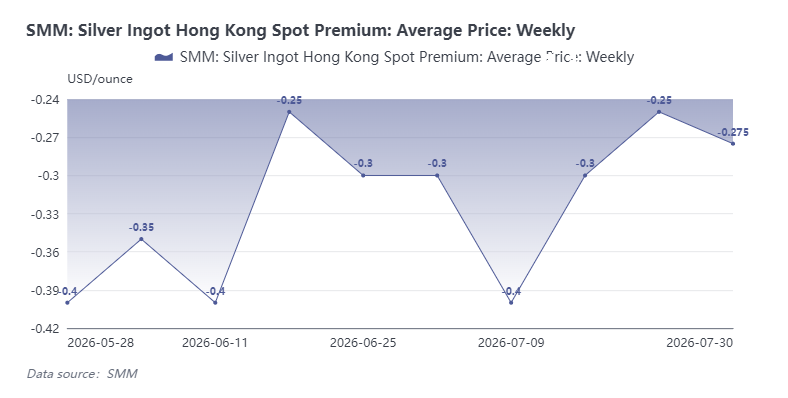

SMM Silver Express: Премия на спотовое серебро в Гонконге снижается на фоне сезонного спада спроса

30 Jul 2026 17:28

ФРС сохраняет ставки, но ястребы усиливаются, оказывая давление на драгметаллы на фоне высокой доходности и укрепления доллара

30 Jul 2026 17:27

Платина и палладий консолидировались в течение недели, завершив торги в целом снижением; ФРС США сохраняет неизменную ястребиную позицию по ставкам [SMM Еженедельный обзор платины и палладия]

На этой неделе платина и палладий сначала снизились, затем отскочили, а потом откатились, закрывшись в минусе после резких колебаний. В начале недели кратковременное прекращение огня между США и Ираном привело к снижению премий за риски безопасных активов, что наряду с растущими ожиданиями повышения ставок потянуло цены вниз. После достижения дна перепроданные покупки и спрос на защитные активы на фоне торговых трений вызвали восстановление. В конце недели ястребиное решение ФРС (голосование 9 к 3, при котором трое высказались за повышение ставки) вновь оказало давление на цены. На GFEX платина зафиксировалась на уровне 391,65 юаня за грамм, а палладий — 297,05 юаня за грамм. Спотовые премии в основном оставались стабильными при подавленном спросе. В ближайшей перспективе геополитическая волатильность и торговые трения могут оказывать эпизодическую поддержку, однако ястребиная позиция ФРС, усиливающая ожидания роста ставок, восстановление цен на нефть, подгоняющее инфляцию, и слабый конечный спрос продолжают ограничивать подъём. Следите за развитием ситуации с США и Ираном и траекторией политики на сентябрь.

30 Jul 2026 17:23

Valterra Platinum сообщает о росте производства в первом полугодии на фоне высоких цен на МПГ, поддерживающих прибыль

[SMM PGM Express] Valterra Platinum сообщила об улучшении операционных и финансовых показателей в I полугодии 2026 года: совокупное производство металлов платиновой группы (МПГ) под управлением выросло на 4% год к году, до 1,519 млн унций, а собственная добыча увеличилась на 9%, до 1,012 млн унций. Выпуск рафинированных МПГ (без учёта толлинга) подскочил на 25%, до 1,742 млн унций, а объём продаж МПГ увеличился на 18%, до 1,737 млн унций.

Более сильным результатам способствовал значительный рост цен на МПГ. Реализованная цена корзины МПГ Valterra составила в среднем 2 801 долл./унция, что на 85% выше уровня предыдущего года, и обеспечила операционную EBITDA в размере 33,4 млрд рандов против 6,6 млрд рандов в I полугодии 2025 года.

Компания отметила, что средняя цена платины более чем удвоилась, достигнув 2 060 долл./унция, палладий подорожал на 60% до 1 560 долл./унция, родий вырос на 93% до 10 040 долл./унция, иридий прибавил 65% до 7 020 долл./унция, а рутений показал лучшую динамику, поднявшись на 165% до 1 530 долл./унция.

В перспективе Valterra ожидает сохранения структурного дефицита платины, постепенного движения палладия к рыночному балансу и устойчивой поддержки спроса на малые МПГ со стороны ужесточающихся норм выбросов автотранспорта, водородных технологий, электроники и новых промышленных применений, связанных с искусственным интеллектом.

30 Jul 2026 17:07

Серебро консолидировалось в форме буквы N и закрылось без изменений на этой неделе, поскольку геополитика и ожидания повышения ставок вели борьбу [SMM Silver Weekly Review]

[SMM Еженедельный обзор рынка серебра: Консолидация в форме N завершилась без изменений на фоне повторяющейся борьбы геополитики и ожиданий повышения ставок] На этой неделе цены на серебро демонстрировали N-образную динамику. В начале недели ожидания прекращения огня подтолкнули котировки вверх. Затем ястребиная ФРС США сохранила ставку без изменений, что в сочетании с периодическим обострением напряжённости на Ближнем Востоке привело к консолидации цен на уровне 14 286 юаней за кг. На спотовом рынке предложение и спрос были слабыми, сделки проходили по паритету. В части запасов общий объём социальных запасов вырос до 3 658 тонн, а открытый интерес по ETF незначительно снизился. В краткосрочной перспективе ожидается боковое движение с уклоном вниз.

30 Jul 2026 16:53

ФРС США сохраняет ставку без изменений на фоне продолжающейся борьбы бычьих и медвежьих сил на рынке драгоценных металлов [Макроанализ рынка драгоценных металлов SMM]

30 Jul 2026 15:09

Чэнтун Майнинг: чистая прибыль в первом полугодии выросла на 71,37% год к году, медно-кобальтовый сегмент в ДРК демонстрирует стабильную добычу

30 Jul 2026 13:46

[SMM Экспресс драгоценных металлов]

Последние официальные данные показывают, что экспорт полезных ископаемых Зимбабве вырос на 84%, при этом металлы платиновой группы (МПГ) остаются крупнейшей опорой. В первом полугодии 2026 года доходы Зимбабве от экспорта полезных ископаемых достигли рекордных 2,532 миллиарда долларов, что на 84% больше по сравнению с 1,376 миллиарда долларов за аналогичный период прошлого года, демонстрируя динамику быстро расширяющейся горнодобывающей и перерабатывающей промышленности. Из них на долю МПГ пришлось 33,93%, по-прежнему являясь крупнейшим источником экспортной выручки, а на концентраты МПГ — 13,73%. Примечательно, что Зимбабве больше не удовлетворяется простым экспортом сырой руды и постепенно переходит к переработке, добавлению стоимости и расширению производственных цепочек. Поскольку мировой спрос на МПГ и важнейшие минералы для возобновляемой энергетики продолжает расти, Зимбабве ускоряет

30 Jul 2026 13:39

Китай вносит организации ЕС в контрольный список экспортного контроля, нацеливаясь на цепочки поставок редкоземельных металлов【Анализ SMM】

24 июля 2026 года Министерство коммерции КНР опубликовало Объявление № 30 от 2026 года, включив 14 базирующихся в ЕС организаций, включая Lafert S.p.A., Rheinmetall AG, InPACT S.A. и Vigo Photonics S.A., в контрольный список экспортного контроля. Данное объявление, принятое в соответствии с Законом КНР об экспортном контроле и Положением об экспортном контроле товаров двойного назначения, предписывает

29 Jul 2026 19:06

![США ужесточают доступ для новых подключаемых инверторов: Каково влияние на текущий рынок? [SMM Analysis]](https://imgqn.smm.cn/usercenter/VEROo20251217171737.jpg)

США ужесточают доступ для новых подключаемых инверторов: Каково влияние на текущий рынок? [SMM Analysis]

29 Jul 2026 16:48

![[SMM Analysis] Южная Корея планирует ужесточить декларирование экспорта медного лома — изменятся ли азиатские торговые потоки?](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)

[SMM Analysis] Южная Корея планирует ужесточить декларирование экспорта медного лома — изменятся ли азиатские торговые потоки?

29 Jul 2026 16:31

![[Анализ SMM] Затраты CBAM вступают в силу, а возможности проверки отстают: что нужно знать экспортерам нержавеющей стали](https://imgqn.smm.cn/usercenter/yUOUz20251217171732.jpg)

[Анализ SMM] Затраты CBAM вступают в силу, а возможности проверки отстают: что нужно знать экспортерам нержавеющей стали

29 Jul 2026 13:53

[SMM анализ] Новый налог на потребление литиевых батарей в Китае: влияние на сектор переработанных ресурсов

28 Jul 2026 14:26

[Анализ SMM] Почему Индия становится активным покупателем на мировом рынке медного лома?

27 Jul 2026 15:45

Индонезия, как сообщается, задержала груз глинозема из-за редкоземельных металлов. Вот что на самом деле говорят правила

27 Jul 2026 15:22

Последние новости

UBS прогнозирует избыток на рынке палладия и снижает прогноз цен до 1100 долларов США за унцию

31 Jul 2026 20:57

Платина держится выше $1600/унц., поскольку покупательский интерес компенсирует давление продаж.

31 Jul 2026 20:35

ARM продвигает проекты Бокони и Нкомати, несмотря на неоднозначные настроения инвесторов.

31 Jul 2026 20:20

[SMM Экспресс драгоценных металлов]

31 Jul 2026 18:31

SMM: В июле 2026 года производство серебряных слитков сократилось, запасы выросли из-за ремонта на плавильных заводах.

31 Jul 2026 18:08

Золото и серебро во время рецессии: как на самом деле ведут себя драгоценные металлы?

31 Jul 2026 17:27

Xingye Silver & Tin: Yinman Mining приостановила как свою добычную систему, так и систему обогащения хвостов.

31 Jul 2026 16:47

Цены на платину устойчивы, пополнение запасов у потребителей достаточное, на спотовом рынке слабые и спрос, и предложение [Ежедневный комментарий SMM]

31 Jul 2026 13:48

Ослабление доллара США и охлаждение PCE резонируют, серебро продолжает консолидироваться на минимумах [Ежедневный обзор SMM]

31 Jul 2026 10:25

Implats приостанавливает работу платинового рудника Рюстенбург после того, как смертельные случаи вызвали проверку безопасности.

30 Jul 2026 22:04

Ожидается, что рынок рутениево-иридиевых титановых анодов более чем удвоится к 2034 году

30 Jul 2026 19:21

Chifeng Gold: Ожидается, что проект SND на золотомедном руднике Сепон в Лаосе увеличит содержание металла в золотом эквиваленте до 260 метрических тонн

30 Jul 2026 18:13

SMM Silver Express: Премия на спотовое серебро в Гонконге снижается на фоне сезонного спада спроса

30 Jul 2026 17:28

ФРС сохраняет ставки, но ястребы усиливаются, оказывая давление на драгметаллы на фоне высокой доходности и укрепления доллара

30 Jul 2026 17:27

Платина и палладий консолидировались в течение недели, завершив торги в целом снижением; ФРС США сохраняет неизменную ястребиную позицию по ставкам [SMM Еженедельный обзор платины и палладия]

30 Jul 2026 17:23

Valterra Platinum сообщает о росте производства в первом полугодии на фоне высоких цен на МПГ, поддерживающих прибыль

30 Jul 2026 17:07

Серебро консолидировалось в форме буквы N и закрылось без изменений на этой неделе, поскольку геополитика и ожидания повышения ставок вели борьбу [SMM Silver Weekly Review]

30 Jul 2026 16:53

ФРС США сохраняет ставку без изменений на фоне продолжающейся борьбы бычьих и медвежьих сил на рынке драгоценных металлов [Макроанализ рынка драгоценных металлов SMM]

30 Jul 2026 15:09

Чэнтун Майнинг: чистая прибыль в первом полугодии выросла на 71,37% год к году, медно-кобальтовый сегмент в ДРК демонстрирует стабильную добычу

30 Jul 2026 13:46

[SMM Экспресс драгоценных металлов]

30 Jul 2026 13:39