ข่าว

บทความวิเคราะห์พิเศษพร้อมข้อมูลตลาดล่าสุด และฟีดข่าวแบบเรียลไทม์

![สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]](https://imgqn.smm.cn/usercenter/VEROo20251217171737.jpg)

สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]

ในวันที่ 28 กรกฎาคม ตามเวลาท้องถิ่น คณะกรรมการกลางกำกับดูแลกิจการสื่อสารแห่งสหรัฐอเมริกา (FCC) ได้ปรับปรุงรายการครอบคลุม (Covered List) ให้รวมอุปกรณ์หุ่นยนต์ขั้นสูงที่ผลิตจากต่างประเทศและอินเวอร์เตอร์ไฟฟ้าแบบเชื่อมต่อ ภายใต้กฎใหม่นี้ รุ่นที่ยังไม่ผ่านการอนุมัติอุปกรณ์จาก FCC จะถูกห้ามจำหน่ายในตลาดสหรัฐฯ ส่วนรุ่นที่เคยได้รับอนุมัติก่อนหน้านี้จะยังไม่ได้รับผลกระทบทันที ในสถานการณ์เช่นนี้ ผลกระทบต่อผู้ประกอบการในตลาดปัจจุบันคืออะไร

29 Jul 2026 16:48

[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?

[บทวิเคราะห์ SMM: เกาหลีใต้เตรียมคุมเข้มการสำแดงส่งออกเศษทองแดง—กระแสการค้าเอเชียจะเปลี่ยนหรือไม่?] เกาหลีใต้มีแผนบังคับให้สำแดงการส่งออกสำหรับเศษเหล็กและเศษอโลหะตั้งแต่ปี 2027 โดยมาตรการนี้พุ่งเป้าไปที่การสำแดงข้อมูลไม่ตรงข้อเท็จจริงมากกว่าจำกัดการค้าที่ถูกกฎหมาย เนื่องจากจีน มาเลเซีย และไทยรับส่วนแบ่งการส่งออกสูงถึง 95.86% ในปี 2025 ผลกระทบจึงน่าจะจำกัดสำหรับสินค้าเกรดดีที่ปฏิบัติตามกฎระเบียบ แต่จะรุนแรงกว่าสำหรับเศษแบบผสมและเศษที่มีส่วนประกอบซับซ้อน

29 Jul 2026 16:31

[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้

ต้นทุนการปฏิบัติตามกฎระเบียบที่สูงขึ้น ปัญหาคอขวดด้านการตรวจสอบ และการคุมเข้มโควต้านำเข้าของสหภาพยุโรป ร่วมกันเปลี่ยนภูมิทัศน์การแข่งขันสำหรับซัพพลายเออร์สแตนเลสจากเอเชียในยุโรปนับตั้งแต่ปี 2026 มาตรการ CBAM ของอียูเริ่มใช้บังคับเต็มรูปแบบในวันที่ 1 มกราคม 2026 — เปลี่ยนจากการเป็นเพียงการรายงานข้อมูล ไปเป็นกลไกที่ส่งผลกระทบต่อต้นทุนทางการค้าอย่างแท้จริง

29 Jul 2026 13:53

ข่าวล่าสุด

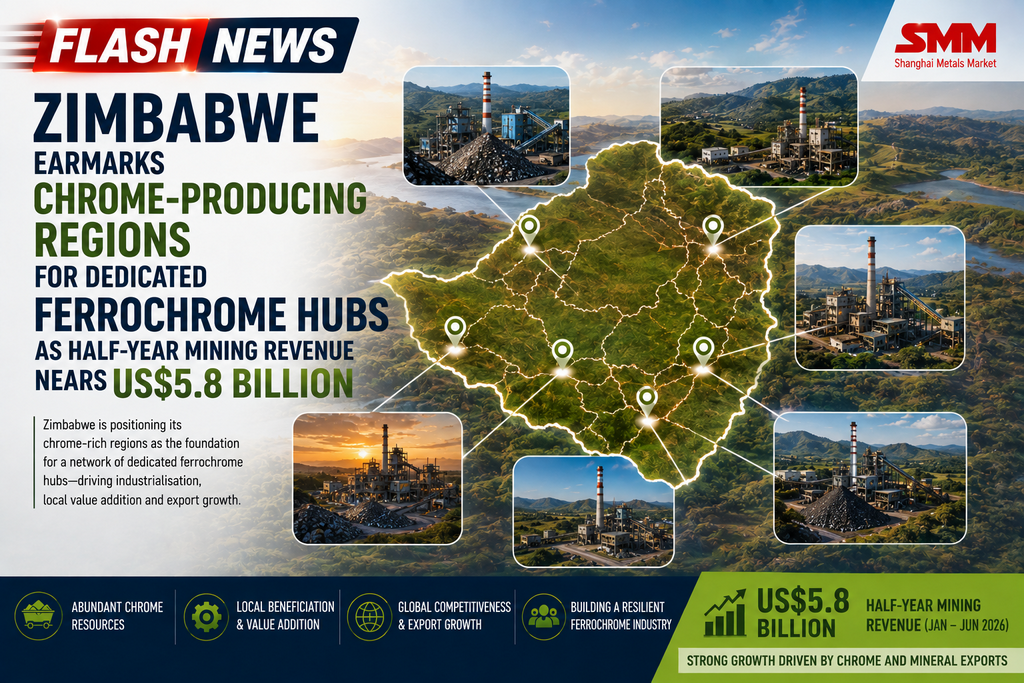

ซิมบับเวกำหนดให้พื้นที่ผลิตโครเมียมเป็นศูนย์กลางเฟอร์โรโครมโดยเฉพาะ ขณะที่รายได้ภาคเหมืองแร่ครึ่งปีแรกใกล้แตะ 5.8 พันล้านดอลลาร์สหรัฐ

2 ชั่วโมงที่แล้ว

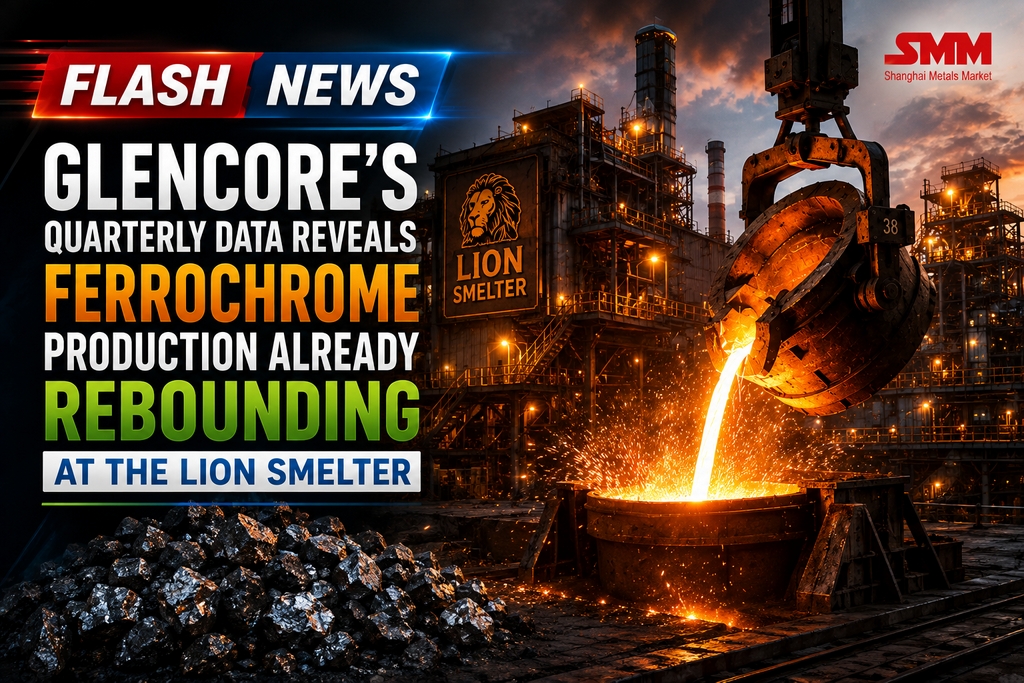

ข้อมูลรายไตรมาสของเกลนคอร์เผยการผลิตเฟอร์โรโครมที่โรงถลุงไลอ้อนฟื้นตัวแล้ว

4 ชั่วโมงที่แล้ว

![ตลาดแมกนีเซียมอินกอตลดลงเล็กน้อยท่ามกลางภาวะซบเซา อุปสงค์ทั้งในและต่างประเทศยังคงซบเซาไปพร้อมกัน [รายงานราคาแมกนีเซียมอินกอต SMM]](https://imgqn.smm.cn/usercenter/yunIW20251217171723.jpeg)

ตลาดแมกนีเซียมอินกอตลดลงเล็กน้อยท่ามกลางภาวะซบเซา อุปสงค์ทั้งในและต่างประเทศยังคงซบเซาไปพร้อมกัน [รายงานราคาแมกนีเซียมอินกอต SMM]

8 ชั่วโมงที่แล้ว

สมาคมอุตสาหกรรมทังสเตนกานโจวปรับลดราคาคาดการณ์ตลาดทังสเตนของเดือนสิงหาคมทั้งหมด

[Tungsten Express] SMM, 5 สิงหาคม: ราคาคาดการณ์ตลาดทังสเตนของสมาคมอุตสาหกรรมทังสเตนก้านโจว ประจำเดือนสิงหาคม 2026: หัวแร่วุลแฟรม (เกรด 55%) 412,000 หยวน/เมตริกตันมาตรฐาน (อิงตาม 65% WO3) ลดลง 36,000 หยวน/เมตริกตันมาตรฐาน (อิงตาม 65% WO3) เมื่อเทียบกับเดือนก่อน; APT 606,000 หยวน/เมตริกตัน ลดลง 54,000 หยวน/เมตริกตัน เมื่อเทียบกับเดือนก่อน; ผงทังสเตนขนาดกลาง 1,000 หยวน/กก. ลดลง 100 หยวน/กก. เมื่อเทียบกับเดือนก่อน (ราคาทั้งหมดรวมภาษีมูลค่าเพิ่ม 13% และสำหรับอ้างอิงเท่านั้น ความเสี่ยงทางการค้าเป็นความรับผิดชอบของผู้ที่เกี่ยวข้อง)

9 ชั่วโมงที่แล้ว

องค์กรทังสเตนฉงอี้ปรับขึ้นราคาสัญญาระยะยาวเล็กน้อยสำหรับครึ่งแรกของเดือนสิงหาคม

[ข่าวทังสเตน] SMM, 5 สิงหาคม: บริษัททังสเตนในฉงอี้ประกาศสัญญาระยะยาวสำหรับครึ่งแรกของเดือนสิงหาคม โดยหัวแร่วูลแฟรไมต์ 55% ทำสัญญาที่ราคา 412,000 หยวน/ตันมาตรฐาน (อิงเกรด 65% WO3) หัวแร่ชีไลต์ 55% ที่ราคา 411,000 หยวน/ตันมาตรฐาน (อิงเกรด 65% WO3) และราคาสัญญาระยะยาวของแร่ปรับขึ้น 1,000 หยวน/ตันมาตรฐานเมื่อเทียบกับครึ่งหลังของเดือนกรกฎาคม สัญญาระยะยาว APT (เกรดศูนย์ มาตรฐานแห่งชาติ) ดำเนินการที่ราคา 606,000 หยวน/ตัน เพิ่มขึ้น 1,000 หยวน/ตันจากครึ่งหลังของเดือนกรกฎาคม

9 ชั่วโมงที่แล้ว

เซียะเหมิน ทังสเตน กลับมาเสนอราคาสัญญาระยะยาว โดย APT ราคาอยู่ที่ 606,000 หยวนต่อเมตริกตัน

[ทังสเตนแฟลช] ข่าว SMM, 5 สิงหาคม: กิจการทังสเตนแห่งหนึ่งในเซี่ยเหมินกลับมาเสนอราคาสัญญาระยะยาวอีกครั้ง โดยกำหนดราคาสัญญาระยะยาวสำหรับ APT ที่ซื้อจากภายนอกในช่วงครึ่งแรกของเดือนสิงหาคม 2026 ไว้ที่ 606,000 หยวน/ตัน

9 ชั่วโมงที่แล้ว

เหอเฟย ชีซิง ลงทุน 453 ล้านดอลลาร์ ในโครงการผลิตแท่งโลหะผสมแมกนีเซียม 50,000 ตัน ในมณฑลอานฮุย

[SMM Magnesium Express] เมื่อเร็วๆ นี้ บริษัท เหอเฟย ฉีซิง ไลท์ เมทัล เทคโนโลยี จำกัด ได้ลงทุนรวม 453 ล้านหยวนในโครงการผลิตแท่งโลหะผสมแมกนีเซียมน้ำหนักเบา 50,000 ตันต่อปี ซึ่งได้จัดตั้งขึ้นที่เมืองเฉาหู มณฑลอานฮุย โครงการนี้รวมถึงการก่อสร้างโรงงานทันสมัยและระบบหลอมอัจฉริยะ โดยมีเป้าหมายเพื่อเติมเต็มช่องว่างในท้องถิ่นด้านวัสดุโลหะผสมแมกนีเซียมระดับสูง และตอบสนองความต้องการอุปทานวัตถุดิบโลหะผสมแมกนีเซียมคุณภาพสูงที่มั่นคง ซึ่งจำเป็นสำหรับการใช้งานหล่อขึ้นรูปแบบรวมขนาดใหญ่ เช่น ถาดแบตเตอรี่และโครงมอเตอร์ไฟฟ้าในรถยนต์พลังงานใหม่ เมื่อโครงการเริ่มดำเนินการ คาดว่าขีดความสามารถในการสนับสนุนของห่วงโซ่อุตสาหกรรมโลหะผสมแมกนีเซียมในท้องถิ่นจะแข็งแกร่งยิ่งขึ้น

10 ชั่วโมงที่แล้ว

ผลผลิตแร่โครเมียมตามสัดส่วนของ Glencore ทรงตัวที่ระดับเกือบ 1.65 ล้านตันในช่วงครึ่งแรกของปี 2026 แม้จะเผชิญกับแรงกดดันจากธุรกิจเฟอร์โรอัลลอย

[SMM Express] รายงานการผลิตครึ่งปี 2026 ของเกลนคอร์แสดงปริมาณการผลิตแร่โครมตามสัดส่วน — ส่วนแบ่ง 79.5% ของกลุ่มในกิจการร่วมค้าโครมเกลนคอร์-เมราฟ — อยู่ที่ 1,647,000 ตัน สำหรับ H1 2026 ลดลงเพียง 4% (70,000 ตัน) จาก 1,717,000 ตัน ใน H1 2025 เกลนคอร์ให้เหตุผลการลดลงเล็กน้อยนี้ว่าเป็นผลจาก "สภาพการดำเนินงานในช่วงเวลาดังกล่าว" ซึ่งเป็นคำอธิบายที่เบากว่าภาษาเฉพาะที่ใช้กับโรงถลุงเฟอร์โรโครมอย่างเห็นได้ชัด ข้อมูลรายไตรมาสยืนยันว่านี่เป็นการชะลอตัวแบบค่อยเป็นค่อยไปมากกว่าการลดลงอย่างกะทันหัน: 910,000 ตันใน Q2/2025 เพิ่มเป็น 1,037,000 ตันใน Q3 ก่อนลดลงเหลือ 859,000 ตันใน Q4/2025, 830,000 ตันใน Q1/2026 และ 817,000 ตันใน Q2/2026 — ลดลง 10% เมื่อเทียบกับปีก่อนในระดับ Q2 ต่อ Q2

ความยืดหยุ่นนี้สอดคล้องกับสิ่งที่ SMM ได้ติดตามจาก Merafe Resources ซึ่งเป็นหุ้นส่วนสัดส่วน 20.5% ของเกลนคอร์ในกิจการร่วมค้าฯ เดียวกัน การเปิดเผยข้อมูล H1 2026 ของ Merafe เองแสดงปริมาณการผลิตแร่โครมที่ 425,000 ตัน ลดลง 4% จาก 443,000 ตัน — เป็นอัตราลดลงที่ใกล้เคียงกับตัวเลขของเกลนคอร์มาก เมื่อทั้งสองฝ่ายในกิจการร่วมค้าต่างรายงานการอ่อนตัวลงเล็กน้อยในฝั่งแร่อย่างอิสระต่อกัน แม้ว่าการผลิตเฟอร์โรโครมจะดิ่งลงในบัญชีของแต่ละฝ่าย รูปแบบนี้จึงถูกยืนยันในระดับกิจการร่วมค้าแทนที่จะเป็นเพียงสิ่งประดิษฐ์จากการรายงานของบริษัทใดบริษัทหนึ่ง: การทำเหมืองแร่โครมนั้นคงตัวได้ดีกว่าการถลุงขั้นปลายน้ำอย่างมากในช่วงครึ่งแรกของปี 2026

10 ชั่วโมงที่แล้ว

ตลาดแทนทาลัมและไนโอเบียมคาดว่าจะสูงถึง 8.74 พันล้านดอลลาร์สหรัฐภายในปี 2036

[SMM Express] ฟิวเจอร์ มาร์เก็ต อินไซต์ส (FMI) คาดการณ์ว่าตลาดวัสดุแทนทาลัมและไนโอเบียมโลกจะเติบโตจาก 4.36 พันล้านดอลลาร์สหรัฐในปี 2026 เป็น 8.74 พันล้านดอลลาร์สหรัฐภายในปี 2036 คิดเป็นอัตราการเติบโตต่อปีแบบทบต้น (CAGR) ที่ 7.2% แนวโน้มดังกล่าวได้รับแรงหนุนจากความต้องการตัวเก็บประจุแทนทาลัมที่เพิ่มขึ้นในอุปกรณ์อิเล็กทรอนิกส์ขั้นสูง และการใช้ไนโอเบียมที่ขยายตัวในเหล็กกล้าความแข็งแรงสูงผสมต่ำ ซูเปอร์อัลลอย และการประยุกต์ใช้ด้านการบินและอวกาศ

ตามรายงานของ FMI ภาคอิเล็กทรอนิกส์คาดว่าจะมีสัดส่วนความต้องการ 48.7% ในปี 2026 ส่วนแทนทาลัมจะยังคงเป็นวัสดุหลักด้วยส่วนแบ่งตลาด 62.4% ประเทศจีนคาดว่าจะมีอัตราเติบโตเร็วสุดที่ CAGR 9.7% ตามด้วยอินเดีย (9.0%) และเยอรมนี (8.3%) สะท้อนถึงการลงทุนที่เพิ่มขึ้นในภาคการผลิตขั้นสูง การผลิตเซมิคอนดักเตอร์ และโครงสร้างพื้นฐานยุคใหม่

การคาดการณ์นี้ตอกย้ำปัจจัยพื้นฐานระยะยาวที่แข็งแกร่งขึ้นของอุตสาหกรรมแทนทาลัมและไนโอเบียม โดยมีแรงหนุนจากอุปสงค์เชิงโครงสร้างจากอุตสาหกรรมอิเล็กทรอนิกส์ การบินและอวกาศ และเทคโนโลยีเปลี่ยนผ่านด้านพลังงาน การเติบโตอย่างต่อเนื่องคาดว่าจะสนับสนุนการลงทุนครอบคลุมทั้งเหมืองแร่ การถลุง และกระบวนการปลายน้ำ พร้อมทั้งเพิ่มความสำคัญเชิงกลยุทธ์ของห่วงโซ่อุปทานที่มีความหลากหลายและมั่นคง

10 ชั่วโมงที่แล้ว

NioBay Metals ประสบความสำเร็จในการผลิตไนโอเบียมและแทนทาลัมออกไซด์ความบริสุทธิ์สูงจากโครงการ Crevier ในรัฐควิเบก

[SMM เอ็กซ์เพรส] NioBay Metals Inc. ได้ประสบความสำเร็จในการผลิตไนโอเบียมและแทนทาลัมออกไซด์ความบริสุทธิ์สูงจากโครงการ Crevier ในรัฐควิเบก โดยได้ไนโอเบียมออกไซด์ (Nb₂O₅) ความบริสุทธิ์ประมาณ 99.6% และแทนทาลัมออกไซด์ (Ta₂O₅) ความบริสุทธิ์ 99.98% โครงการทำให้บริสุทธิ์ซึ่งเสร็จสมบูรณ์ด้วยงานกระบวนการและการวิเคราะห์ที่ดำเนินการโดย SGS Canada Inc. ได้ยืนยันประสิทธิภาพของผังกระบวนการโลหวิทยาและไฮโดรโลหวิทยาของบริษัท ซึ่งรวมถึงขั้นตอนการเผาที่อุณหภูมิสูงถึง 1,050°C

ตามข้อมูลของ NioBay ผลิตภัณฑ์ออกไซด์ดังกล่าวตรงตามข้อกำหนดเฉพาะของลูกค้าที่มีศักยภาพบางราย ซึ่งถือเป็นก้าวสำคัญทางเทคนิคสำหรับโครงการ Crevier บริษัทกำลังประเมินศักยภาพของโครงการในการผลิตไนโอเบียมออกไซด์สำหรับการใช้งานในแบตเตอรี่และซูเปอร์อัลลอย หลังจากการศึกษาก่อนหน้านี้บ่งชี้ถึงค่าพารามิเตอร์ทางเทคนิคและเศรษฐกิจที่น่าพอใจ

การผลิตไนโอเบียมและแทนทาลัมออกไซด์ความบริสุทธิ์สูงส่งสัญญาณถึงความก้าวหน้าอย่างต่อเนื่องในขีดความสามารถด้านการแปรรูปขั้นปลายนอกภูมิภาคซัพพลายดั้งเดิม ในขณะที่ความต้องการวัสดุที่มีข้อกำหนดเฉพาะสูงเพิ่มขึ้นในภาคการผลิตแบตเตอรี่ การบินและอวกาศ และการผลิตขั้นสูง การบรรลุก้าวสำคัญด้านการทำให้บริสุทธิ์อาจช่วยเสริมความแข็งแกร่งให้กับอุปทานในอนาคตและสนับสนุนการเพิ่มมูลค่าภายในห่วงโซ่อุปทานไนโอเบียมและแทนทาลัม

11 ชั่วโมงที่แล้ว

![ตลาดซบเซา,การลดกำลังผลิตเพิ่มขึ้น,การผลิตซิลิคอนเมทัลในเดือนสิงหาคมคาดว่าจะลดลง [บทวิเคราะห์จาก SMM]](https://imgqn.smm.cn/usercenter/ChqBy20251217171724.jpeg)

ตลาดซบเซา,การลดกำลังผลิตเพิ่มขึ้น,การผลิตซิลิคอนเมทัลในเดือนสิงหาคมคาดว่าจะลดลง [บทวิเคราะห์จาก SMM]

12 ชั่วโมงที่แล้ว

ไป๋หยิน นอนเฟอรัส เปิดประกวดราคาแท่งเทลลูเรียม 5 ตัน เริ่มประมูลวันที่ 11 สิงหาคม

13 ชั่วโมงที่แล้ว

![บริษัท ไป๋หยิน นอนเฟอร์รัส กรุ๊ป จำกัด ได้จัดการประมูลสาธารณะสำหรับแท่งเทลลูเรียมปริมาณ 5 เมตริกตัน เมื่อวันที่ 5 [รายงาน SMM]](https://imgqn.smm.cn/usercenter/NPpAM20251217171723.jpeg)

บริษัท ไป๋หยิน นอนเฟอร์รัส กรุ๊ป จำกัด ได้จัดการประมูลสาธารณะสำหรับแท่งเทลลูเรียมปริมาณ 5 เมตริกตัน เมื่อวันที่ 5 [รายงาน SMM]

13 ชั่วโมงที่แล้ว

กฎความปลอดภัยเหมืองใหม่เข้มงวดขึ้น กระทบอุปทานในตลาดหัวแร่ทังสเตน

[ทังสเตน เอ็กซ์เพรส] ข่าว SMM วันที่ 5 สิงหาคม: วันนี้ ตลาดหัวแร่ทังสเตนยังคงทรงตัว เนื่องจากตลาดกำลังทบทวนผลกระทบของ “ความเห็นของสำนักงานความปลอดภัยเหมืองแร่แห่งชาติ ว่าด้วยการกำกับดูแลทีมงานก่อสร้างขุดเจาะ (เปิดเปลือกดิน) สำหรับเหมืองผลิตโลหะและอโลหะ” ต่ออุตสาหกรรมเหมืองที่ไม่ใช่ถ่านหิน เอกสารดังกล่าวกำหนดให้เหมืองใต้ดินภายในวันที่ 1 พฤษภาคม 2027 และเหมืองเปิดภายในวันที่ 1 พฤษภาคม 2028 เลือกหนึ่งในสองแนวทาง: ① จัดตั้งทีมขุดเจาะภายในองค์กร ② ว่าจ้างผู้รับเหมาเบ็ดเสร็จที่ปฏิบัติตามกฎหมาย ห้ามแบ่งงานย่อยและการรับช่วงแบบหลายชั้น ห้ามใช้แรงงานส่งจัดหาในงานใต้ดิน เหมืองที่ไม่สามารถปรับปรุงให้แล้วเสร็จตามกำหนดจะถูกสั่งระงับการผลิตเพื่อดำเนินการให้ถูกต้อง เหมืองทังสเตนของจีนส่วนใหญ่เป็นเหมืองใต้ดิน (เหมืองวุลแฟรไมต์ส่วนมากเป็นใต้ดิน ขณะที่เหมืองชีไลต์บางแห่งเป็นเหมืองเปิดหรือใต้ดิน) แหล่งผลิตหลักอย่างเจียงซีและหูหนานมีเหมืองทังสเตนขนาดกลางและเล็กจำนวนมากซึ่งพึ่งพาทีมรับเหมาช่วงขุดเจาะภายนอกมาอย่างยาวนาน ก่อให้เกิดข้อจำกัดอย่างมากทั้งด้านอุปทาน ต้นทุน และการอยู่รอดของเหมืองขนาดเล็ก ขณะที่ในช่วงสองวันที่ผ่านมา การซื้อขายในตลาดขายทันทีของหัวแร่ทังสเตนเริ่มกลับมาคึกคัก โดยผู้ค้าขนาดกลางเข้ามาดำเนินการอย่างต่อเนื่อง เมื่อวานนี้ เหมืองแห่งหนึ่งในกว่างตงได้ประมูลแร่เกรดต่ำ โดยขายได้ทั้งหมด 156 ตันมาตรฐาน ผู้ถลุงปลายน้ำยังคงระมัดระวัง รอทิศทางจากราคาสัญญาระยะยาวที่จะประกาศในวันนี้ โดยรวมแล้ว ตลาดได้รับแรงกระตุ้นจากนโยบายเหมืองแร่ที่ออกบ่อยครั้ง และการตรวจสอบความปลอดภัยที่มีความเข้มข้นในยูนนาน เจียงซี เหอหนาน และพื้นที่อื่นๆ ทำให้ความเชื่อมั่นในตลาดคลายลง ขณะที่ปัจจัยรบกวนด้านอุปทานทวีความรุนแรงขึ้น หากอุปสงค์กลับเข้าสู่ตลาดอย่างพอดี ตลาดทังสเตนจะพลิกฟื้น

15 ชั่วโมงที่แล้ว

การเพิ่มประสิทธิภาพการดำเนินงานกลายเป็นกลยุทธ์การเติบโตใหม่สำหรับผลผลิตโครเมียมของแอฟริกาใต้

[SMM Express] พัฒนาการล่าสุดในกลุ่มแร่บุชเวลด์ของแอฟริกาใต้บ่งชี้ว่า การเพิ่มประสิทธิภาพการดำเนินงาน แทนการพัฒนาเหมืองใหม่ กำลังกลายเป็นปัจจัยสำคัญในการผลักดันการเติบโตของผลผลิตโครเมียม ในขณะที่ผู้ผลิตพยายามสร้างมูลค่าสูงสุดจากแหล่งแร่ UG2 ที่มีอยู่ การลงทุนต่างมุ่งเน้นไปที่การปรับปรุงประสิทธิภาพการทำเหมือง ประสิทธิภาพการแปรรูป และการนำกลับคืนโครไมต์ เพื่อเพิ่มปริมาณโครเมียม พร้อมเสริมสร้างความแข็งแกร่งทางเศรษฐกิจโดยรวมของโครงการ

บริษัทนอร์แธม แพลทินัม เพิ่งทำสถิติผลิตหัวแร่โครเมียมได้ 1.69 ล้านเมตริกตันในปีงบประมาณ 2026 โดยได้รับการสนับสนุนจากปริมาณการผ่านแร่ UG2 ที่สูงขึ้น การขยายทีมงานเหมือง และการปรับปรุงกระบวนการแปรรูปที่เหมืองอีแลนด์ ในทำนองเดียวกัน ซิบันเย-สติลล์วอเตอร์ ได้วางแผนเพิ่มผลผลิตโครเมียมเป็นประมาณ 2.3 ล้านตันต่อปีภายในปี 2033 ผ่านการเพิ่มประสิทธิภาพการดำเนินงานที่มีอยู่ ขณะที่การศึกษาความเป็นไปได้ขั้นสุดท้ายของโครงการเบงเวนยามาโดยเซาเทิร์น แพลเลเดียม ได้เพิ่มปริมาณการผลิตหัวแร่โครเมียมที่คาดการณ์ไว้เป็นมากกว่า 1.05 ล้านตันต่อปี หลังจากปรับปรุงการนำกลับคืนโครไมต์จาก 30% เป็น 85.6% SMM เชื่อว่าพัฒนาการเหล่านี้ชี้ให้เห็นแนวโน้มอุตสาหกรรมที่กว้างขึ้น ซึ่งผู้ผลิตกำลังปลดล็อกอุปทานโครเมียมเพิ่มเติมผ่านการปรับปรุงการดำเนินงานและกระบวนการโลหะวิทยา ส่งผลให้โครเมียมกลายเป็นผู้มีส่วนสำคัญต่อรายได้และมูลค่าโครงการระยะยาวมากขึ้น ท่ามกลางแรงกดดันต่อเนื่องในตลาด PGM

4 Aug 2026 23:11

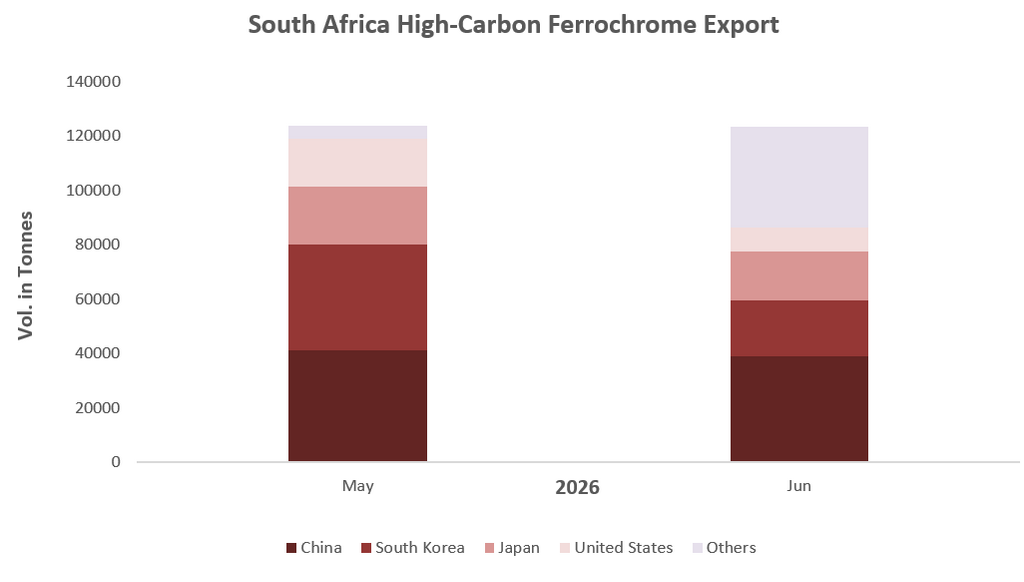

การส่งออกเฟอร์โรโครมคาร์บอนสูงของแอฟริกาใต้ลดลงเล็กน้อยในเดือนมิถุนายน จีนยังคงเป็นปลายทางหลัก

[SMM Express] ในเดือนมิถุนายน 2026 แอฟริกาใต้ส่งออกเฟอร์โรโครมคาร์บอนสูง 123,310.23 ตัน ลดลง 0.32% เมื่อเทียบกับเดือนก่อนหน้า (MoM) และ 44.57% เมื่อเทียบกับปีก่อนหน้า (YoY) ซึ่งบ่งชี้ว่าการส่งออกยังคงค่อนข้างคงที่จากเดือนพฤษภาคม แต่ยังคงตามหลังระดับของปีที่แล้ว ผลการดำเนินงานประจำปีที่ซบเซาสะท้อนถึงข้อจำกัดด้านการผลิตที่ดำเนินอยู่อย่างต่อเนื่องในอุตสาหกรรมเฟอร์โรโครมในประเทศ แม้ว่าอุปสงค์ระหว่างประเทศจะยังคงแข็งแกร่ง

จีนยังคงเป็นจุดหมายปลายทางการส่งออกใหญ่ที่สุดของแอฟริกาใต้ โดยคิดเป็นสัดส่วน 31.56% ของการจัดส่งทั้งหมดในเดือนมิถุนายน ซึ่งตอกย้ำตำแหน่งของจีนในฐานะตลาดเฟอร์โรโครมหลักของประเทศ เกาหลีใต้อยู่ในอันดับที่สองด้วยส่วนแบ่งการส่งออก 16.63% การกระจุกตัวของการจัดส่งไปยังตลาดเอเชียเน้นย้ำถึงความสำคัญอย่างต่อเนื่องของภูมิภาคนี้ในการสนับสนุนการค้าเฟอร์โรโครมของแอฟริกาใต้ แม้ว่าปริมาณการส่งออกโดยรวมจะยังคงอยู่ภายใต้แรงกดดัน

4 Aug 2026 22:54

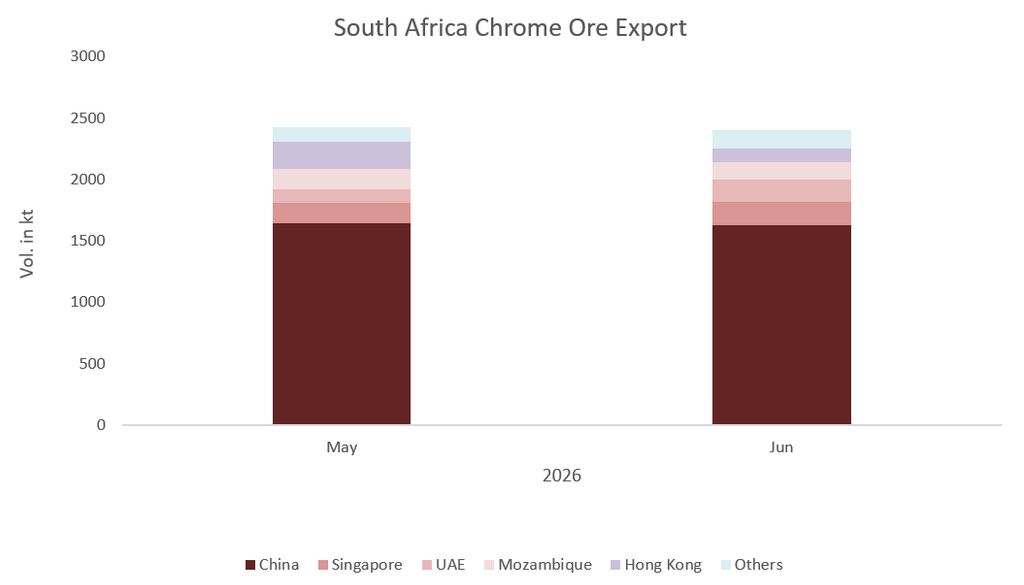

การส่งออกแร่โครเมียมของแอฟริกาใต้ลดลงเล็กน้อยเหลือ 2.4 ล้านตันในเดือนมิถุนายน แต่ยังคงเพิ่มขึ้นเกือบ 39% เมื่อเทียบกับช่วงเดียวกันของปีก่อน

[SMM Express] การส่งออกแร่โครเมียมทั้งหมดของแอฟริกาใต้ในเดือนมิถุนายน 2026 อยู่ที่ 2.40 ล้านตัน ลดลง 0.90% จากเดือนก่อน แต่ยังคงเพิ่มขึ้นอย่างรวดเร็ว 38.86% เมื่อเทียบกับปีก่อน การชะลอตัวลงเล็กน้อยรายเดือนบ่งชี้ว่าปริมาณการส่งออกเริ่มทรงตัวหลังจากช่วงขยายตัวแข็งแกร่ง แม้ว่าขนาดของการเพิ่มขึ้นรายปีจะยืนยันว่าอุปสงค์ภายนอกที่แท้จริงสำหรับแร่โครเมียมของแอฟริกาใต้ยังคงแข็งแกร่ง

จีนยังคงเป็นปลายทางหลัก โดยรองรับสัดส่วน 67.61% ของปริมาณการส่งออกทั้งหมดในเดือนมิถุนายน ตอกย้ำว่าการค้าแร่โครเมียมของแอฟริกาใต้ยังคงกระจุกตัวอย่างมากอยู่กับอุปสงค์เฟอร์โรโครมของจีน สิงคโปร์และสหรัฐอาหรับเอมิเรตส์ตามมาเป็นอันดับสองและสาม ที่ 7.85% และ 7.82% ตามลำดับ ซึ่งรวมกันคิดเป็นสัดส่วนเล็กน้อยแต่โดดเด่นนอกกระแสการค้าหลักที่เชื่อมโยงกับจีน

4 Aug 2026 21:30

สภาวะอุปทานล้นตลาดของแร่ไทเทเนียมเข้มข้นยังไม่เปลี่ยนแปลง ตลาดซบเซาต่อเนื่อง [SMM Titanium Spot Express]

[SMM ข่าวด่วนตลาดไทเทเนียม: ภาวะอุปทานล้นตลาดของสินแร่ไทเทเนียมไม่เปลี่ยนแปลง ตลาดซบเซายังคงดำเนินต่อไป] SMM 4 สิงหาคม: ราคาเสนอขายหลักของสินแร่ไทเทเนียม 46% อยู่ที่ 1,250 หยวน/ตันในวันนี้ แร่นำเข้าราคาถูกยังคงส่งผลกระทบต่อเนื่อง อุปทานจากแร่พลอยได้ในปานซีเพิ่มขึ้นแบบไม่ตั้งใจ ขณะที่อุปสงค์จากห่วงโซ่อสังหาริมทรัพย์ยังคงซบเซา และผู้ซื้อปลายน้ำยังคงรอดูสถานการณ์ เลื่อนการซื้อออกไป ราคาระยะสั้นยังคงถูกกดดัน

4 Aug 2026 18:48

ราคาประมูลหัวแร่ทังสเตนจากเหมืองในมณฑลกวางตุ้ง ประมาณ 337,000-349,000 หยวนต่อตันมาตรฐาน (อิงตามปริมาณ WO3 65%)

[ทังสเตน เอกซ์เพรส] วันที่ 4 สิงหาคม เหมืองแห่งหนึ่งในมณฑลกว่างตงได้ประมูลขายหัวแร่ทังสเตน โดยมีผลการซื้อขายดังนี้: 1. ปริมาณ: 67±5% ตันมาตรฐาน (อิงตาม 65%WO3) เกรด: 17.46% ราคาซื้อขายแปลงเป็น 337,400 หยวน/ตันมาตรฐาน (อิงตาม 65%WO3); 2. ปริมาณ: 89±5% ตันมาตรฐาน (อิงตาม 65%WO3) เกรด: 19.47% ราคาซื้อขายแปลงเป็น 349,000 หยวน/ตันมาตรฐาน (อิงตาม 65%WO3)

4 Aug 2026 18:44

[SMM Analysis] ราคาไทเทเนียมไดออกไซด์ปรับลดลงในเดือนกรกฎาคม ท่ามกลางสต็อกที่เพิ่มขึ้นและอุปสงค์ที่อ่อนแรง

ในเดือนกรกฎาคม 2569 ราคา TiO₂ ปรับตัวลดลง 1,900 หยวนต่อเมตริกตันจากระดับต้นเดือน โดยสต็อกเพิ่มขึ้น 23.26% เมื่อเทียบกับเดือนก่อนหน้า ถึงแม้ผลผลิตจะลดลงเล็กน้อย ราคาไทเทเนียมสปันจ์ลดลง 3,000 หยวนต่อเมตริกตัน เนื่องจากผลผลิตขยายตัว 5.45% เมื่อเทียบกับเดือนก่อนหน้า และอุปสงค์ยังคงอ่อนแอ โมเมนตัมการส่งออกชะลอตัวลงท่ามกลางช่วงขาลงของฤดูร้อนและการควบคุมที่เข้มงวดขึ้น คาดว่าตลาดทั้งสองจะยังคงอยู่ภายใต้แรงกดดันในระยะใกล้ โดยมีแนวโน้มขาลงในระยะสั้น

4 Aug 2026 18:26

SMM เยือนสหพันธ์อุตสาหกรรมเหล็กและเหล็กกล้ามาเลเซีย (MISIF) เพื่อร่วมขับเคลื่อนการประสานความร่วมมือในอุตสาหกรรมโลหะกลุ่มเหล็กอาเซียน

กัวลาลัมเปอร์ 3 ส.ค. – ในช่วงที่อุตสาหกรรมโลหะเหล็กทั่วโลกกำลังปรับโครงสร้างอย่างต่อเนื่อง อาเซียนได้ก้าวขึ้นเป็นศูนย์กลางการเติบโตสำคัญของอุตสาหกรรมเหล็ก โดยได้รับแรงหนุนจากอุปสงค์ปลายทางที่แข็งแกร่ง กำลังการผลิตที่ขยายตัวอย่างรวดเร็ว และพลวัตการค้าข้ามพรมแดนที่เปลี่ยนไป การยกระดับโครงสร้างพื้นฐานในภูมิภาค การปรับเปลี่ยนกำลังการผลิตภายในประเทศ และการปรับนโยบายการค้า กำลังขับเคลื่อนการเปลี่ยนแปลงในโครงสร้างอุปสงค์-อุปทาน ระบบราคา และห่วงโซ่อุปทานของตลาดเหล็กอาเซียนอย่างต่อเนื่อง อุตสาหกรรมนี้จึงต้องการแพลตฟอร์มการพูดคุยระหว่างประเทศที่เชี่ยวชาญเฉพาะทางอย่างเร่งด่วน เพื่อแก้ไขจุดที่เป็นอุปสรรคในการพัฒนาและเปิดประตูสู่โอกาสทางธุรกิจระดับโลก ท่ามกลางภูมิหลังทางอุตสาหกรรมนี้ คณะผู้แทนจากเซี่ยงไฮ้เมทัลส์มาร์เก็ต (SMM) ได้เข้าเยี่ยมคารวะ สหพันธ์อุตสาหกรรมเหล็กและเหล็กกล้ามาเลเซีย (MISIF) เมื่อวันที่ 31 กรกฎาคม และได้รับการต้อนรับอย่างอบอุ่นจาก Tan Ai Joo ซีอีโอของ MISIF และ Eveline Chu ผู้จัดการ ทั้งสองฝ่ายได้หารือกันอย่างลึกซึ้งในหัวข้อหลัก อาทิ การประสานทรัพยากรข้ามพรมแดน ความร่วมมือด้านการจัดนิทรรศการ การแบ่งปันข้อมูลอุตสาหกรรม และการร่วมกำหนดทิศทางตลาด โดยมุ่งเน้นไปที่การวางผังอุตสาหกรรมของ SMM ในภูมิภาคอาเซียนและการสร้างระบบนิเวศความร่วมมือข้ามพรมแดน ในด้านความร่วมมือระยะยาวในอนาคต ทั้งสองฝ่ายได้หารือกันอย่างลึกซึ้งถึงกลไกความร่วมมือแบบประจำที่อำนวยประโยชน์ร่วมกัน ชนะทั้งสองฝ่าย และยั่งยืน อันเป็นการวางรากฐานสำหรับการเสริมพลังร่วมกันให้แก่อุตสาหกรรมเหล็กในมาเลเซียและอาเซียนในอนาคต ความร่วมมือด้านข้อมูลอุตสาหกรรมและบริการข้อมูลการตลาดคือหนึ่งในแก่นของลำดับความสำคัญของการหารือครั้งนี้ MISIF ได้แบ่งปันสถานภาพการพัฒนาตลาดเหล็กของมาเลเซีย คุณลักษณะทางสถิติของอุตสาหกรรม และแผนการออกรายงาน SMM ได้นำเสนอรายละเอียดรูปแบบบริการสมัครสมาชิกที่สอดคล้องกับกฎระเบียบของแพลตฟอร์ม ซึ่งปกป้องข้อมูลการดำเนินงานที่เป็นความลับขององค์กรอย่างเข้มงวด และสามารถให้บริการข้อมูลเชิงลึกของอุตสาหกรรมที่ปรับแต่งได้ บริการวิเคราะห์ตลาด และการศึกษาวิจัยแนวโน้มให้ตรงตามคุณลักษณะของตลาดมาเลเซียและความต้องการเฉพาะของแต่ละองค์กร ยิ่งไปกว่านั้น ทั้งสองฝ่ายได้แลกเปลี่ยนมุมมองเกี่ยวกับความคลาดเคลื่อนของข้อมูลการค้าข้ามพรมแดนระดับโลก คุณลักษณะทางสถิติด้านศุลกากรของประเทศต่างๆ และตัวแปรของตลาดการค้าระหว่างประเทศ เป็นต้น ด้วยการใช้ประโยชน์จากระบบตรวจสอบข้อมูลท่าเรือที่ครอบคลุมของตน SMM สามารถให้บริการแบ่งปันข้อมูล อาทิ ปริมาณสินค้าคงคลังที่ท่าเรือจริงในจีนที่มีการอัปเดตแบบความถี่สูง ทั้งสองฝ่ายได้บรรลุฉันทามติเกี่ยวกับการจัดตั้งกลไกการสื่อสารอย่างสม่ำเสมอในอนาคต เพื่อดำเนินการแลกเปลี่ยนความร่วมมือในด้านข้อมูลอุตสาหกรรม ข้อมูลตลาด และแนวโน้มอุตสาหกรรมอย่างต่อเนื่อง SMM ได้ออกคำเชิญอย่างเป็นทางการไปยัง MISIF ให้นำองค์กรสมาชิกเข้าร่วมการประชุมสุดยอด SMM อาเซียน เฟอร์รัส เมทัลส์ 2026 (2026 SMM ASEAN Ferrous Metals Summit) ระหว่างวันที่ 26-27 พฤศจิกายน 2026 ณ กรุงกัวลาลัมเปอร์ ประเทศมาเลเซีย และแบ่งปันมุมมองของอุตสาหกรรม ร่วมกันสร้างแพลตฟอร์มการพูดคุยพหุภาคีสำหรับอุตสาหกรรมโลหะเหล็กที่เชื่อมโยงหลายชาติสมาชิกอาเซียน เกี่ยวกับ SMM รู้สึกตื่นเต้นที่จะประกาศว่าเราจะจัดงานการประชุมสุดยอด SMM อาเซียน เฟอร์รัส เมทัลส์ 2026 ขึ้นในวันที่ 26-27 พฤศจิกายน 2026 ณ กรุงกัวลาลัมเปอร์ ประเทศมาเลเซีย งานนี้คือแพลตฟอร์มระดับพรีเมียมในตลาดโลหะเหล็กอาเซียนที่จะรวบรวมผู้มีอำนาจตัดสินใจกว่า 400 รายจากเหมือง โรงงาน บริษัทค้า ผู้แปรรูป ผู้ให้บริการอุปกรณ์และเทคโนโลยี และผู้ประกอบการด้านโลจิสติกส์ มาอยู่ร่วมโต๊ะเดียวกัน ณ ห้วงเวลาที่ระเบียบระดับภูมิภาคกำลังถูกเขียนขึ้นใหม่ ไฮไลท์การประชุม 1. แนวโน้มตลาดเหล็กอาเซียน การวิเคราะห์เชิงลึกเกี่ยวกับอุปสงค์เหล็กในภูมิภาค โดยคาดว่าในปี 2026 การบริโภคจะพุ่งสูงถึง 87.9 ล้านเมตริกตัน ซึ่งขับเคลื่อนหลักจากเวียดนาม อินโดนีเซีย และฟิลิปปินส์ 2. การปรับโครงสร้างการค้าและห่วงโซ่อุปทานจีน-อาเซียน สำรวจกระแสการไหลเวียนที่เปลี่ยนไปของเหล็กแผ่นรีดร้อน (HRC) บิลเล็ต สแล็บ และผลิตภัณฑ์เหล็กอื่นๆ ท่ามกลางรูปแบบอุปทานที่เปลี่ยนแปลง มาตรการเยียวยาทางการค้า และพลวัตของตลาดในภูมิภาค 3. การขยายกำลังการผลิตและการเปลี่ยนผ่านด้านการผลิต ตรวจสอบภูมิทัศน์การผลิตเหล็กที่กำลังเปลี่ยนโฉมของอาเซียน รวมถึงการเติบโตของกำลังการผลิตแบบ BF-BOF การพัฒนาแบบ EAF การลงทุนจากต่างประเทศ และศูนย์กลางการผลิตแห่งใหม่ในภูมิภาค 4. นโยบายทางการค้าและการเข้าถึงตลาด ประเมินมาตรการต่อต้านการทุ่มตลาด ภาษีศุลกากร โอกาสที่เกี่ยวเนื่องกับ RCEP และการเปลี่ยนแปลงเชิงกฎระเบียบที่กำลังพลิกโฉมการค้าเหล็กทั่วอาเซียน 5. อุปสงค์ที่เติบโตสูงและโอกาสด้านผลิตภัณฑ์ ระบุโอกาสจากโครงสร้างพื้นฐาน การก่อสร้าง ยานยนต์ และการประยุกต์ใช้เหล็กขั้นสูง โดยมุ่งเน้นไปที่อินโดนีเซีย เวียดนาม และตลาดเกิดใหม่อื่นๆ 6. การสร้างเครือข่ายผู้บริหารและความร่วมมือระดับภูมิภาค เชื่อมโยงผู้ผลิตชั้นนำ ผู้ค้า ผู้ซื้อ นักลงทุน สมาคม ผู้กำหนดนโยบาย และผู้เชี่ยวชาญในอุตสาหกรรมจากทั่วอาเซียน จีน และตลาดโลก วิทยากรอาวุโส 2026 ภาพเหตุการณ์จากการประชุมครั้งที่ผ่านมา ระเบียบวาระการประชุม ติดต่อ: Horin Dong WhatsApp: +8618721310824 อีเมล: horindong@smm.cn สแกนคิวอาร์โค้ดสำหรับรายละเอียดการประชุมและข้อมูลส่วนลดเพิ่มเติม เกี่ยวกับ SMM SMM สั่งสมประสบการณ์อย่างลึกซึ้งในบริการอุตสาหกรรมสินค้าโภคภัณฑ์ระดับโลกมาอย่างยาวนาน พร้อมสานต่อความสัมพันธ์ความร่วมมือกับหน่วยงานภาครัฐ องค์กรวิสาหกิจ และสมาคมอุตสาหกรรมในประเทศต่างๆ ให้แน่นแฟ้นยิ่งขึ้น และขยายเครือข่ายบริการอุตสาหกรรมระดับโลกอย่างต่อเนื่อง ด้วยการใช้ประโยชน์จากรูปแบบความร่วมมือที่เติบโตเต็มที่กับภาครัฐ วิสาหกิจ และสมาคมต่างๆ ในอินโดนีเซีย SMM ได้สร้างระบบนิเวศแบบวงจรปิดที่ครอบคลุมสำหรับการแบ่งปันข้อมูลนิทรรศการและการประชุมในต่างประเทศ พร้อมทั้งยกระดับระบบข้อมูลขนาดใหญ่ของอุตสาหกรรมอย่างไม่หยุดยั้ง เพื่อให้บรรลุการแลกเปลี่ยนข้อมูลตลาดโลกอย่างมีประสิทธิภาพ การร่วมสร้างและแบ่งปันทรัพยากร SMM จัดงาน มากกว่า 50 งานระดับมืออาชีพในแต่ละปี ครอบคลุมการประชุมสุดยอดอุตสาหกรรม ฟอรั่มอุตสาหกรรม และการดูงานภาคสนาม ในจำนวนนี้ 40 งานมีรากฐานอย่างลึกซึ้งในตลาดจีน เกือบ 10 งานถูกจัดวางอย่างแม่นยำในตลาดหลักของเอเชียตะวันออกเฉียงใต้ และส่วนน้อยครอบคลุมยุโรปและแอฟริกา งานในต่างประเทศได้รับการยอมรับในระดับอุตสาหกรรมโลกจากรายชื่อแขกในแวดวงที่ทรงอำนาจ ข้อมูลสำรวจอุตสาหกรรมที่เป็นเนื้อแน่น และบริการจับคู่อุปสงค์-อุปทานที่แม่นยำ SMM ได้จัดการประชุมสุดยอดระดับสูงในอินโดนีเซียหลายครั้ง โดยร่วมมือกับหน่วยงานท้องถิ่น อาทิ กระทรวงการต่างประเทศ และสมาคมผู้ทำเหมืองนิกเกิลอินโดนีเซีย (APNI) ซึ่งรวบรวม กว่า 300 ผู้เชี่ยวชาญในอุตสาหกรรม และยังเสริมด้วยกิจกรรมดูงานภาคสนามตามห่วงโซ่อุตสาหกรรมในต่างประเทศอย่างมืออาชีพ เพื่อเสริมพลังให้กับการแลกเปลี่ยนทางอุตสาหกรรมและการจับคู่ทางการค้าของภูมิภาคอย่างรอบด้าน

3 Aug 2026 10:16

SMM AICE เยือน VAFIE: เข้าใจตรรกะเบื้องหลังการขยายธุรกิจของบริษัทอะลูมิเนียมจีนในเวียดนาม

15 ชั่วโมงที่แล้ว

SMM เยือน VPG: สัญญาณสำคัญใดที่กลุ่มบริษัทเวียดนามนี้กำลังส่งถึงบริษัทอะลูมิเนียมจีน?

3 Aug 2026 16:42

จีนบรรจุหน่วยงานของสหภาพยุโรปลงในบัญชีเฝ้าระวังการควบคุมการส่งออก เล็งเป้าห่วงโซ่อุปทานแร่หายาก【SMM Analysis】

29 Jul 2026 19:06

สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]

29 Jul 2026 16:48

![[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)

[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?

29 Jul 2026 16:31

![[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้](https://imgqn.smm.cn/usercenter/yUOUz20251217171732.jpg)

[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้

29 Jul 2026 13:53

ข่าวล่าสุด

ซิมบับเวกำหนดให้พื้นที่ผลิตโครเมียมเป็นศูนย์กลางเฟอร์โรโครมโดยเฉพาะ ขณะที่รายได้ภาคเหมืองแร่ครึ่งปีแรกใกล้แตะ 5.8 พันล้านดอลลาร์สหรัฐ

2 ชั่วโมงที่แล้ว

ข้อมูลรายไตรมาสของเกลนคอร์เผยการผลิตเฟอร์โรโครมที่โรงถลุงไลอ้อนฟื้นตัวแล้ว

4 ชั่วโมงที่แล้ว

ตลาดแมกนีเซียมอินกอตลดลงเล็กน้อยท่ามกลางภาวะซบเซา อุปสงค์ทั้งในและต่างประเทศยังคงซบเซาไปพร้อมกัน [รายงานราคาแมกนีเซียมอินกอต SMM]

8 ชั่วโมงที่แล้ว

สมาคมอุตสาหกรรมทังสเตนกานโจวปรับลดราคาคาดการณ์ตลาดทังสเตนของเดือนสิงหาคมทั้งหมด

9 ชั่วโมงที่แล้ว

องค์กรทังสเตนฉงอี้ปรับขึ้นราคาสัญญาระยะยาวเล็กน้อยสำหรับครึ่งแรกของเดือนสิงหาคม

9 ชั่วโมงที่แล้ว

เซียะเหมิน ทังสเตน กลับมาเสนอราคาสัญญาระยะยาว โดย APT ราคาอยู่ที่ 606,000 หยวนต่อเมตริกตัน

9 ชั่วโมงที่แล้ว

เหอเฟย ชีซิง ลงทุน 453 ล้านดอลลาร์ ในโครงการผลิตแท่งโลหะผสมแมกนีเซียม 50,000 ตัน ในมณฑลอานฮุย

10 ชั่วโมงที่แล้ว

ผลผลิตแร่โครเมียมตามสัดส่วนของ Glencore ทรงตัวที่ระดับเกือบ 1.65 ล้านตันในช่วงครึ่งแรกของปี 2026 แม้จะเผชิญกับแรงกดดันจากธุรกิจเฟอร์โรอัลลอย

10 ชั่วโมงที่แล้ว

ตลาดแทนทาลัมและไนโอเบียมคาดว่าจะสูงถึง 8.74 พันล้านดอลลาร์สหรัฐภายในปี 2036

10 ชั่วโมงที่แล้ว

NioBay Metals ประสบความสำเร็จในการผลิตไนโอเบียมและแทนทาลัมออกไซด์ความบริสุทธิ์สูงจากโครงการ Crevier ในรัฐควิเบก

11 ชั่วโมงที่แล้ว

ตลาดซบเซา,การลดกำลังผลิตเพิ่มขึ้น,การผลิตซิลิคอนเมทัลในเดือนสิงหาคมคาดว่าจะลดลง [บทวิเคราะห์จาก SMM]

12 ชั่วโมงที่แล้ว

ไป๋หยิน นอนเฟอรัส เปิดประกวดราคาแท่งเทลลูเรียม 5 ตัน เริ่มประมูลวันที่ 11 สิงหาคม

13 ชั่วโมงที่แล้ว

บริษัท ไป๋หยิน นอนเฟอร์รัส กรุ๊ป จำกัด ได้จัดการประมูลสาธารณะสำหรับแท่งเทลลูเรียมปริมาณ 5 เมตริกตัน เมื่อวันที่ 5 [รายงาน SMM]

13 ชั่วโมงที่แล้ว

กฎความปลอดภัยเหมืองใหม่เข้มงวดขึ้น กระทบอุปทานในตลาดหัวแร่ทังสเตน

15 ชั่วโมงที่แล้ว

การเพิ่มประสิทธิภาพการดำเนินงานกลายเป็นกลยุทธ์การเติบโตใหม่สำหรับผลผลิตโครเมียมของแอฟริกาใต้

4 Aug 2026 23:11

การส่งออกเฟอร์โรโครมคาร์บอนสูงของแอฟริกาใต้ลดลงเล็กน้อยในเดือนมิถุนายน จีนยังคงเป็นปลายทางหลัก

4 Aug 2026 22:54

การส่งออกแร่โครเมียมของแอฟริกาใต้ลดลงเล็กน้อยเหลือ 2.4 ล้านตันในเดือนมิถุนายน แต่ยังคงเพิ่มขึ้นเกือบ 39% เมื่อเทียบกับช่วงเดียวกันของปีก่อน

4 Aug 2026 21:30

สภาวะอุปทานล้นตลาดของแร่ไทเทเนียมเข้มข้นยังไม่เปลี่ยนแปลง ตลาดซบเซาต่อเนื่อง [SMM Titanium Spot Express]

4 Aug 2026 18:48

ราคาประมูลหัวแร่ทังสเตนจากเหมืองในมณฑลกวางตุ้ง ประมาณ 337,000-349,000 หยวนต่อตันมาตรฐาน (อิงตามปริมาณ WO3 65%)

4 Aug 2026 18:44

[SMM Analysis] ราคาไทเทเนียมไดออกไซด์ปรับลดลงในเดือนกรกฎาคม ท่ามกลางสต็อกที่เพิ่มขึ้นและอุปสงค์ที่อ่อนแรง

4 Aug 2026 18:26