ข่าว

บทความวิเคราะห์พิเศษพร้อมข้อมูลตลาดล่าสุด และฟีดข่าวแบบเรียลไทม์

![สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]](https://imgqn.smm.cn/usercenter/VEROo20251217171737.jpg)

สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]

ในวันที่ 28 กรกฎาคม ตามเวลาท้องถิ่น คณะกรรมการกลางกำกับดูแลกิจการสื่อสารแห่งสหรัฐอเมริกา (FCC) ได้ปรับปรุงรายการครอบคลุม (Covered List) ให้รวมอุปกรณ์หุ่นยนต์ขั้นสูงที่ผลิตจากต่างประเทศและอินเวอร์เตอร์ไฟฟ้าแบบเชื่อมต่อ ภายใต้กฎใหม่นี้ รุ่นที่ยังไม่ผ่านการอนุมัติอุปกรณ์จาก FCC จะถูกห้ามจำหน่ายในตลาดสหรัฐฯ ส่วนรุ่นที่เคยได้รับอนุมัติก่อนหน้านี้จะยังไม่ได้รับผลกระทบทันที ในสถานการณ์เช่นนี้ ผลกระทบต่อผู้ประกอบการในตลาดปัจจุบันคืออะไร

29 Jul 2026 16:48

[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?

[บทวิเคราะห์ SMM: เกาหลีใต้เตรียมคุมเข้มการสำแดงส่งออกเศษทองแดง—กระแสการค้าเอเชียจะเปลี่ยนหรือไม่?] เกาหลีใต้มีแผนบังคับให้สำแดงการส่งออกสำหรับเศษเหล็กและเศษอโลหะตั้งแต่ปี 2027 โดยมาตรการนี้พุ่งเป้าไปที่การสำแดงข้อมูลไม่ตรงข้อเท็จจริงมากกว่าจำกัดการค้าที่ถูกกฎหมาย เนื่องจากจีน มาเลเซีย และไทยรับส่วนแบ่งการส่งออกสูงถึง 95.86% ในปี 2025 ผลกระทบจึงน่าจะจำกัดสำหรับสินค้าเกรดดีที่ปฏิบัติตามกฎระเบียบ แต่จะรุนแรงกว่าสำหรับเศษแบบผสมและเศษที่มีส่วนประกอบซับซ้อน

29 Jul 2026 16:31

[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้

ต้นทุนการปฏิบัติตามกฎระเบียบที่สูงขึ้น ปัญหาคอขวดด้านการตรวจสอบ และการคุมเข้มโควต้านำเข้าของสหภาพยุโรป ร่วมกันเปลี่ยนภูมิทัศน์การแข่งขันสำหรับซัพพลายเออร์สแตนเลสจากเอเชียในยุโรปนับตั้งแต่ปี 2026 มาตรการ CBAM ของอียูเริ่มใช้บังคับเต็มรูปแบบในวันที่ 1 มกราคม 2026 — เปลี่ยนจากการเป็นเพียงการรายงานข้อมูล ไปเป็นกลไกที่ส่งผลกระทบต่อต้นทุนทางการค้าอย่างแท้จริง

29 Jul 2026 13:53

ข่าวล่าสุด

ราคาทองแดงพุ่งแตะระดับสูงสุดในรอบสองเดือน ขณะที่เงินทุนไหลเข้าจากสหรัฐฯ เพิ่มขึ้นอย่างมากก่อนการตัดสินใจด้านภาษี

20 นาทีที่แล้ว

【SMM Flash】ประกาศราคาสัญญาซัลเฟอร์ตะวันออกกลางเดือนสิงหาคมแล้ว

7 ชั่วโมงที่แล้ว

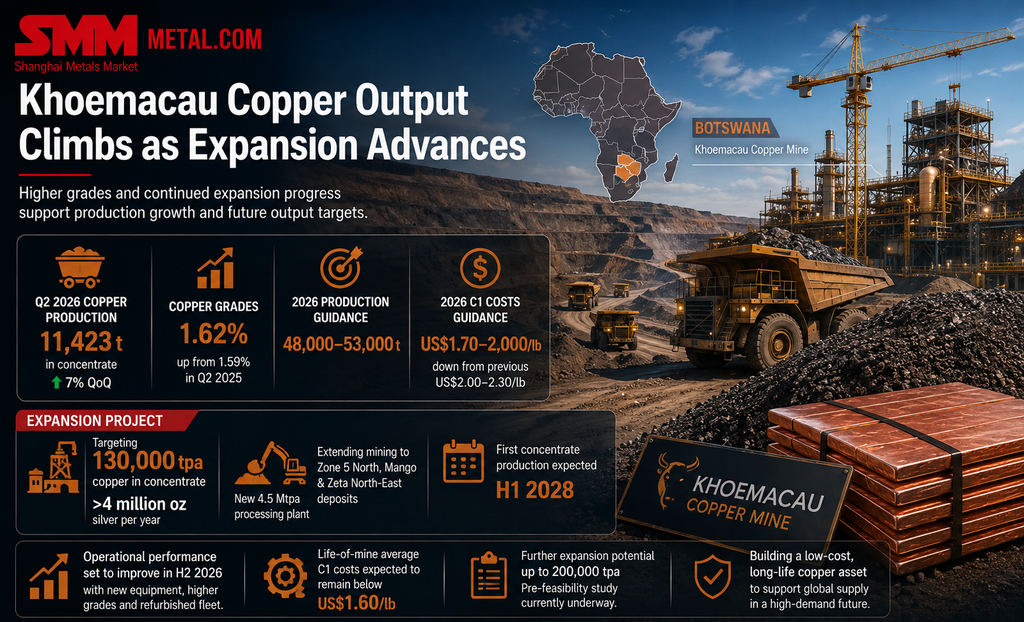

เหมืองทองแดงโคเอมาคาอูเพิ่มผลผลิตไตรมาส 2/2026 การขยายกำลังการผลิตตามแผน

8 ชั่วโมงที่แล้ว

ข้อมูล: ความเคลื่อนไหวตลาด SHFE, DCE (5 ส.ค.)

ตารางต่อไปนี้แสดงความเคลื่อนไหวของโลหะเหล็กและโลหะนอกกลุ่มเหล็กในตลาด SHFE และ DCE เมื่อวันที่ 5 ส.ค. 2026

9 ชั่วโมงที่แล้ว

ราคาทองแดงแข็งค่าขึ้น ตลาดซื้อขายเศษทองแดงคึกคัก [SMM บทวิเคราะห์รายวันทองแดงทุติยภูมิ]

9 ชั่วโมงที่แล้ว

คนงานเหมืองในแซมเบียเรียกร้องนโยบายส่งเสริมการผลิตทองแดงและโครงสร้างพื้นฐานก่อนการเลือกตั้ง

ผู้ประกอบการเหมืองแร่ทั่วแซมเบียกำลังรวบรวมข้อเรียกร้องเชิงนโยบายก่อนการเลือกตั้งระดับชาติที่กำลังจะมาถึง โดยเรียกร้องให้รัฐบาลเพิ่มแรงจูงใจสำหรับการแปรรูปแร่ในประเทศ การสำรวจพื้นที่ใหม่ และการขยายกำลังการผลิตไฟฟ้า ผู้นำอุตสาหกรรมย้ำว่ามาตรการเหล่านี้มีความสำคัญต่อการบรรลุเป้าหมายระดับชาติในการเพิ่มผลผลิตทองแดงต่อปีเป็นสามเท่าสู่ระดับ 3 ล้านตัน

แรงผลักดันนี้เกิดขึ้นพร้อมกับตลาดทางกายภาพที่ตึงตัว ซึ่งความต้องการโลหะสำคัญที่พุ่งสูงขึ้นในยานยนต์ไฟฟ้า โครงข่ายไฟฟ้า และการก่อสร้าง ได้ผลักดันราคาล่วงหน้าทองแดงอ้างอิงให้สูงขึ้นกว่า 40% ในปีที่ผ่านมาอยู่ที่ 14,000 ดอลลาร์สหรัฐต่อตัน เสถียรภาพทางการคลังและการมีส่วนร่วมที่ใกล้ชิดยิ่งขึ้นกับบริษัทเหมืองได้ดึงดูดเงินลงทุนที่ยืนยันแล้วกว่า 1 หมื่นล้านดอลลาร์สหรัฐมายังแซมเบียนับตั้งแต่การเลือกตั้งปี 2564 อย่างไรก็ตาม การขยายผลผลิตในระยะยาวขึ้นอยู่กับการแก้ไขคอขวดด้านโครงสร้างพื้นฐานที่สำคัญ

ตามรายงานของหอการค้าเหมืองแร่แซมเบีย การรักษาแนวทางการสำรวจที่แข็งแกร่งผ่านการใช้จ่ายด้านการสำรวจพื้นที่ใหม่และการปฏิรูปใบอนุญาตเป็นสิ่งจำเป็นเพื่อให้เกิดการเติบโตของอุตสาหกรรมอย่างแท้จริง ในขณะเดียวกัน ผู้ผลิตที่ยังไม่ได้รวมธุรกิจยังคงสนับสนุนการยกเว้นภาษีส่งออกสำหรับหัวแร่ทองแดง ผู้บริหารในอุตสาหกรรมประเมินว่าแซมเบียต้องการกำลังการผลิตไฟฟ้าเพิ่มเติมอย่างน้อย 2,000 เมกะวัตต์ เพื่อป้องกันไม่ให้การขาดแคลนพลังงานอย่างรุนแรงเป็นข้อจำกัดการขยายเหมืองที่วางแผนไว้ เนื่องจากเหมืองแร่ยังคงเป็นกระดูกสันหลังทางเศรษฐกิจของประเทศ โดยมีส่วนสนับสนุน 9% ของ GDP 72% ของรายได้จากการส่งออก และเกือบครึ่งหนึ่งของรายได้รัฐบาล นักวิเคราะห์คาดการณ์ว่าจะมีความต่อเนื่องของนโยบายทั่วไปสำหรับการลงทุนโดยตรงจากต่างประเทศหลังการเลือกตั้ง

9 ชั่วโมงที่แล้ว

SMM เยี่ยมชมบริษัท หนิงปัว จินหลง คอปเปอร์ อินดัสทรี จำกัด เพื่อร่วมสำรวจโอกาสการพัฒนาในอุตสาหกรรมแปรรูปแท่งทองแดงและกระชับความร่วมมือห่วงโซ่อุตสาหกรรม

10 ชั่วโมงที่แล้ว

ความเสี่ยงแผ่นดินไหวระดับลึกปรากฏ; Codelco ระงับโครงการขยาย Andes Norte ที่เหมืองทองแดง El Teniente [บทวิเคราะห์ SMM]

[ความเสี่ยงแผ่นดินไหวเชิงลึกปรากฏขึ้น โคเดลโกระงับโครงการขยายแอนดีสเหนือที่เหมืองทองแดงเอลเตเนียนเต] โคเดลโกระงับกิจกรรมการพัฒนาและก่อสร้างที่โครงการแอนดีสเหนือของเหมืองทองแดงเอลเตเนียนเตเป็นการชั่วคราว เนื่องจากความเสี่ยงแผ่นดินไหวรูปแบบใหม่ที่อาจเกิดขึ้นในพื้นที่ลึก ขณะที่พื้นที่ผลิตอื่นของเหมืองยังคงเดินเครื่อง บริษัทจะเสริมการติดตามแผ่นดินไหวและการประเมินทางเทคนิคต่อไป และยังไม่ประกาศกำหนดกลับมาดำเนินการ แอนดีสเหนือเป็นโครงการสำคัญเพื่อสืบทอดทรัพยากรเชิงลึกของเอลเตเนียนเต การระงับครั้งนี้อาจเพิ่มความไม่แน่นอนต่อการฟื้นตัวของการผลิตระยะกลางและระยะยาวของเหมือง รวมถึงการเริ่มเดินเครื่องของโครงการเชิงลึก

10 ชั่วโมงที่แล้ว

การกลับตัวของ Parity นำเข้าและส่วนเพิ่มราคาตลาดอ่อนตัว; จับตาสถานการณ์ส่งออกของจีนต่อไป

[SMM ตลาดทองแดงนำเข้า] เมื่อเร็ว ๆ นี้ การพลิกกลับของพาริตีนำเข้าของจีนเห็นได้ชัด และโครงสร้าง backwardation ของสัญญา LME ระยะใกล้ได้ขยายกว้างขึ้น ผู้ขายในตลาดทองแดงนำเข้ามีการเสนอขายที่คึกคักมากขึ้น ประกอบกับอุปสงค์การบริโภคปลายน้ำที่ซบเซา ส่งผลให้ค่าพรีเมียมสปอตมีแนวโน้มปรับตัวลงจากระดับสูง อย่างไรก็ดี เนื่องจากผลการดูดซับอุปทานจากอเมริกาเหนือยังคงมีอยู่ การเติมเต็มอุปทานทองแดงนำเข้าในจีนจึงคาดว่าจะยังคงจำกัด ทำให้ค่าพรีเมียมสปอตมีแนวรับด้านล่าง นอกจากนี้ ผู้ถลุงบางรายมีแนวโน้มส่งออก ดังนั้นจึงจำเป็นต้องติดตามสถานการณ์การส่งออกของจีนในระยะต่อไปอย่างใกล้ชิด

11 ชั่วโมงที่แล้ว

ซัพพลายเออร์ลดราคาซ้ำๆ เพื่ออำนวยความสะดวกในการทำธุรกรรม ค่าพรีเมียมทองแดงสปอตเซี่ยงไฮ้โดยเฉลี่ยปรับตัวลดลง [SMM Shanghai spot copper]

[SMM ทองแดงสปอตเซี่ยงไฮ้] เมื่อมองไปถึงวันพรุ่งนี้ วันนี้ราคากลางทองแดง SHFE ปรับตัวสูงขึ้นไปเหนือระดับ 107,000 หยวนต่อเมตริกตัน ราคาทองแดงที่สูงขึ้นกดดันการซื้อของภาคปลายน้ำอย่างมาก โดยตลาดยังคงถูกครอบงำด้วยการซื้อตามความต้องการจำเป็น อย่างไรก็ตาม ผู้ขายมีความต้องการขายมากขึ้น และปรับลดราคาเสนอขายลงอย่างต่อเนื่องตลอดทั้งวันเพื่อกระตุ้นให้เกิดการซื้อขาย เมื่อราคาทองแดงคุณภาพมาตรฐานถอยลง ความต้องการซื้อของภาคปลายน้ำก็ดีขึ้น และมีการซื้อขายทองแดงราคาถูกบางส่วนอย่างค่อยเป็นค่อยไป ในขณะเดียวกัน สินค้าทองแดงคุณภาพสูงและทองแดง SX-EW จดทะเบียนที่มีอยู่ยังคงหายาก โดยราคาเสนอขายที่ค่อนข้างแข็งแกร่งช่วยหนุนค่าพรีเมียมสปอตอยู่บ้าง โดยรวมแล้ว ท่ามกลางสถานการณ์ที่ราคาทองแดงสูงกดดันความต้องการ และผู้ขายลดราคาอย่างแข็งขันเพื่อระบายสินค้า ราคาทองแดงสปอตเซี่ยงไฮ้เทียบกับสัญญา SHFE 2608 คาดว่าจะยังคงอยู่ในระดับพรีเมียมในวันพรุ่งนี้ ราคากลางโดยรวมอาจยังคงซบเซาต่อไป แต่การซื้อขายที่ดีขึ้นในราคาถูกอาจช่วยจำกัดการถอยลงของค่าพรีเมียม

11 ชั่วโมงที่แล้ว

มีรายงานว่า FCC กำลังร่างคำสั่งห้ามส่วนประกอบศูนย์ข้อมูลของจีน รวมถึงโมดูลออปติคัล

11 ชั่วโมงที่แล้ว

Baoming Tech พัฒนาฟอยล์ทองแดง HVLP4/5 สำหรับเซิร์ฟเวอร์ AI รอการตรวจสอบจากลูกค้า

11 ชั่วโมงที่แล้ว

![อัตราส่วนราคา SHFE/LME แย่ลงอีก, อุปสงค์ปลายน้ำอ่อนแอ, ศูนย์กลางพรีเมียมปรับลดลง [SMM ทองแดงสปอตหยางซาน]](https://imgqn.smm.cn/usercenter/uoTGi20251217171713.jpg)

อัตราส่วนราคา SHFE/LME แย่ลงอีก, อุปสงค์ปลายน้ำอ่อนแอ, ศูนย์กลางพรีเมียมปรับลดลง [SMM ทองแดงสปอตหยางซาน]

13 ชั่วโมงที่แล้ว

ผลงานตลาด NEV เดือนกรกฎาคมโดดเด่น

13 ชั่วโมงที่แล้ว

สินค้าคงคลังลดลง ซัพพลายเออร์คงราคา แต่ผู้ซื้อปลายน้ำซื้ออย่างระมัดระวัง [SMM ทองแดงสปอตจีนตอนใต้]

13 ชั่วโมงที่แล้ว

ราคาทองแดงสูงฉุดการซื้อ การซื้อขายซบเซาฉุดพรีเมียมสปอตจีนตอนเหนือ [SMM North China Copper Spot]

วันนี้ ราคาสปอตของทองแดงแคโทดเบอร์ 1 ในภาคเหนือของจีน เทียบกับสัญญาเดือนใกล้สุด เฉลี่ยอยู่ในช่วงส่วนลด 50 หยวน/ตัน ถึงพรีเมียม 40 หยวน/ตัน โดยส่วนลดเฉลี่ย 5 หยวน/ตัน ลดลง 50 หยวน/ตัน จากวันซื้อขายก่อนหน้า และราคาซื้อขายเฉลี่ยอยู่ที่ 107,090 หยวน/ตัน เพิ่มขึ้น 395 หยวน/ตัน

13 ชั่วโมงที่แล้ว

อุปสงค์นอกฤดูผนวกกับราคาทองแดงที่สูง สร้างแรงกดดันต่อการผลิตสายไฟและสายเคเบิลในเดือนกรกฎาคม [SMM Analysis]

[บทวิเคราะห์ SMM: อุปสงค์นอกฤดูกาลและราคาทองแดงที่สูงกดดันการผลิตสายทองแดงและสายเคเบิลในเดือนกรกฎาคม] ในเดือนกรกฎาคม อัตราการดำเนินงานของอุตสาหกรรมสายทองแดงและสายเคเบิลอยู่ที่ 69.82% ลดลง 2.4 จุดเปอร์เซ็นต์ MoM และลดลง 1.79 จุดเปอร์เซ็นต์ YoY ในจำนวนนี้ อัตราการดำเนินงานของกิจการขนาดใหญ่อยู่ที่ 75.13% ของกิจการขนาดกลางอยู่ที่ 47.75% และของกิจการขนาดเล็กอยู่ที่ 46.93%......

13 ชั่วโมงที่แล้ว

[SMM Flash] ประกาศราคาแนะนำกรดซัลฟิวริกของจีนประจำเดือนสิงหาคมแล้ว คำนวณโดยใช้ดัชนีแร่ทองแดงเข้มข้นของ SMM

เมื่อวันที่ 5 สิงหาคม 2026 หลังจากหารือกับผู้ประกอบการรายใหญ่และยื่นเรื่องต่อคณะกรรมการพัฒนาและปฏิรูปแห่งชาติ สมาคมกรดซัลฟิวริกและสมาคมปุ๋ยฟอสเฟตและปุ๋ยเชิงประกอบได้ร่วมกันตัดสินใจว่า: เพื่อให้ราคาเป็นธรรมและมีเสถียรภาพพอสมควร จึงปรับแก้ 'ค่าธรรมเนียมการแปรรูปหัวแร่ทองแดงล่าสุด' ในสูตรราคาแนะนำเดิมเป็น 'ค่าเฉลี่ยของค่าธรรมเนียมการแปรรูปหัวแร่ทองแดงในช่วงสามเดือนที่ผ่านมา' หลังจากการพิจารณาอย่างรอบคอบ ค่าธรรมเนียมการแปรรูปหัวแร่ทองแดงที่ใช้ในการคำนวณอ้างอิงตามดัชนีหัวแร่ทองแดงของ SMM

เมื่อคำนวณตามสูตรใหม่ ราคาแนะนำกรดซัลฟิวริกจากการถลุงเดือนสิงหาคมอยู่ที่ 1,555 หยวน/ตัน ราคาแนะนำในอดีต ได้แก่ เดือนพฤษภาคม (1,406 หยวน/ตัน) เดือนมิถุนายน (1,456 หยวน/ตัน) และเดือนกรกฎาคม (1,574 หยวน/ตัน)

14 ชั่วโมงที่แล้ว

Prysmian ใช้ทองแดงรีไซเคิล 100% 10,000 ตันในโครงการสายเคเบิลใต้ทะเลในสหราชอาณาจักร

Prysmian จะใช้ทองแดงรีไซเคิลที่ตรวจสอบย้อนกลับได้ทั้งหมดประมาณ 10,000 ตัน ซึ่งจัดหาโดย La Farga สำหรับโครงการสายเคเบิลใต้ทะเล Eastern Green Link 2 ระยะทาง 505 กิโลเมตรของสหราชอาณาจักร การใช้ทองแดงรีไซเคิลคาดว่าจะช่วยหลีกเลี่ยงการปล่อยก๊าซคาร์บอนไดออกไซด์เทียบเท่าได้ประมาณ 56,675 ตัน เมื่อเทียบกับการใช้ทองแดงปฐมภูมิ

15 ชั่วโมงที่แล้ว

แคนาเดียน คอปเปอร์เข้าควบคุมแหล่งคาริบู ขณะที่การทบทวน EIA ของเมอร์เรย์ บรูกคืบหน้า

แคนาเดียน คอปเปอร์ ดำเนินการโอนกรรมสิทธิ์และเข้ารับบริหารจัดการโครงการคาริบูคอมเพล็กซ์ในรัฐนิวบรันสวิกเสร็จสิ้นแล้ว บริษัทได้แต่งตั้งบุคลากรรับผิดชอบงานดูแล บำรุงรักษา และการปฏิบัติตามข้อกำหนดด้านสิ่งแวดล้อม แม้ยังไม่มีการประกาศกลับมาเดินเครื่องผลิตแต่อย่างใด การประเมินผลกระทบสิ่งแวดล้อมของเมอร์เรย์ บรูก ก็ได้เข้าสู่การตรวจสอบอย่างเป็นทางการแล้วเช่นกัน

15 ชั่วโมงที่แล้ว

SMM เยือนสหพันธ์อุตสาหกรรมเหล็กและเหล็กกล้ามาเลเซีย (MISIF) เพื่อร่วมขับเคลื่อนการประสานความร่วมมือในอุตสาหกรรมโลหะกลุ่มเหล็กอาเซียน

กัวลาลัมเปอร์ 3 ส.ค. – ในช่วงที่อุตสาหกรรมโลหะเหล็กทั่วโลกกำลังปรับโครงสร้างอย่างต่อเนื่อง อาเซียนได้ก้าวขึ้นเป็นศูนย์กลางการเติบโตสำคัญของอุตสาหกรรมเหล็ก โดยได้รับแรงหนุนจากอุปสงค์ปลายทางที่แข็งแกร่ง กำลังการผลิตที่ขยายตัวอย่างรวดเร็ว และพลวัตการค้าข้ามพรมแดนที่เปลี่ยนไป การยกระดับโครงสร้างพื้นฐานในภูมิภาค การปรับเปลี่ยนกำลังการผลิตภายในประเทศ และการปรับนโยบายการค้า กำลังขับเคลื่อนการเปลี่ยนแปลงในโครงสร้างอุปสงค์-อุปทาน ระบบราคา และห่วงโซ่อุปทานของตลาดเหล็กอาเซียนอย่างต่อเนื่อง อุตสาหกรรมนี้จึงต้องการแพลตฟอร์มการพูดคุยระหว่างประเทศที่เชี่ยวชาญเฉพาะทางอย่างเร่งด่วน เพื่อแก้ไขจุดที่เป็นอุปสรรคในการพัฒนาและเปิดประตูสู่โอกาสทางธุรกิจระดับโลก ท่ามกลางภูมิหลังทางอุตสาหกรรมนี้ คณะผู้แทนจากเซี่ยงไฮ้เมทัลส์มาร์เก็ต (SMM) ได้เข้าเยี่ยมคารวะ สหพันธ์อุตสาหกรรมเหล็กและเหล็กกล้ามาเลเซีย (MISIF) เมื่อวันที่ 31 กรกฎาคม และได้รับการต้อนรับอย่างอบอุ่นจาก Tan Ai Joo ซีอีโอของ MISIF และ Eveline Chu ผู้จัดการ ทั้งสองฝ่ายได้หารือกันอย่างลึกซึ้งในหัวข้อหลัก อาทิ การประสานทรัพยากรข้ามพรมแดน ความร่วมมือด้านการจัดนิทรรศการ การแบ่งปันข้อมูลอุตสาหกรรม และการร่วมกำหนดทิศทางตลาด โดยมุ่งเน้นไปที่การวางผังอุตสาหกรรมของ SMM ในภูมิภาคอาเซียนและการสร้างระบบนิเวศความร่วมมือข้ามพรมแดน ในด้านความร่วมมือระยะยาวในอนาคต ทั้งสองฝ่ายได้หารือกันอย่างลึกซึ้งถึงกลไกความร่วมมือแบบประจำที่อำนวยประโยชน์ร่วมกัน ชนะทั้งสองฝ่าย และยั่งยืน อันเป็นการวางรากฐานสำหรับการเสริมพลังร่วมกันให้แก่อุตสาหกรรมเหล็กในมาเลเซียและอาเซียนในอนาคต ความร่วมมือด้านข้อมูลอุตสาหกรรมและบริการข้อมูลการตลาดคือหนึ่งในแก่นของลำดับความสำคัญของการหารือครั้งนี้ MISIF ได้แบ่งปันสถานภาพการพัฒนาตลาดเหล็กของมาเลเซีย คุณลักษณะทางสถิติของอุตสาหกรรม และแผนการออกรายงาน SMM ได้นำเสนอรายละเอียดรูปแบบบริการสมัครสมาชิกที่สอดคล้องกับกฎระเบียบของแพลตฟอร์ม ซึ่งปกป้องข้อมูลการดำเนินงานที่เป็นความลับขององค์กรอย่างเข้มงวด และสามารถให้บริการข้อมูลเชิงลึกของอุตสาหกรรมที่ปรับแต่งได้ บริการวิเคราะห์ตลาด และการศึกษาวิจัยแนวโน้มให้ตรงตามคุณลักษณะของตลาดมาเลเซียและความต้องการเฉพาะของแต่ละองค์กร ยิ่งไปกว่านั้น ทั้งสองฝ่ายได้แลกเปลี่ยนมุมมองเกี่ยวกับความคลาดเคลื่อนของข้อมูลการค้าข้ามพรมแดนระดับโลก คุณลักษณะทางสถิติด้านศุลกากรของประเทศต่างๆ และตัวแปรของตลาดการค้าระหว่างประเทศ เป็นต้น ด้วยการใช้ประโยชน์จากระบบตรวจสอบข้อมูลท่าเรือที่ครอบคลุมของตน SMM สามารถให้บริการแบ่งปันข้อมูล อาทิ ปริมาณสินค้าคงคลังที่ท่าเรือจริงในจีนที่มีการอัปเดตแบบความถี่สูง ทั้งสองฝ่ายได้บรรลุฉันทามติเกี่ยวกับการจัดตั้งกลไกการสื่อสารอย่างสม่ำเสมอในอนาคต เพื่อดำเนินการแลกเปลี่ยนความร่วมมือในด้านข้อมูลอุตสาหกรรม ข้อมูลตลาด และแนวโน้มอุตสาหกรรมอย่างต่อเนื่อง SMM ได้ออกคำเชิญอย่างเป็นทางการไปยัง MISIF ให้นำองค์กรสมาชิกเข้าร่วมการประชุมสุดยอด SMM อาเซียน เฟอร์รัส เมทัลส์ 2026 (2026 SMM ASEAN Ferrous Metals Summit) ระหว่างวันที่ 26-27 พฤศจิกายน 2026 ณ กรุงกัวลาลัมเปอร์ ประเทศมาเลเซีย และแบ่งปันมุมมองของอุตสาหกรรม ร่วมกันสร้างแพลตฟอร์มการพูดคุยพหุภาคีสำหรับอุตสาหกรรมโลหะเหล็กที่เชื่อมโยงหลายชาติสมาชิกอาเซียน เกี่ยวกับ SMM รู้สึกตื่นเต้นที่จะประกาศว่าเราจะจัดงานการประชุมสุดยอด SMM อาเซียน เฟอร์รัส เมทัลส์ 2026 ขึ้นในวันที่ 26-27 พฤศจิกายน 2026 ณ กรุงกัวลาลัมเปอร์ ประเทศมาเลเซีย งานนี้คือแพลตฟอร์มระดับพรีเมียมในตลาดโลหะเหล็กอาเซียนที่จะรวบรวมผู้มีอำนาจตัดสินใจกว่า 400 รายจากเหมือง โรงงาน บริษัทค้า ผู้แปรรูป ผู้ให้บริการอุปกรณ์และเทคโนโลยี และผู้ประกอบการด้านโลจิสติกส์ มาอยู่ร่วมโต๊ะเดียวกัน ณ ห้วงเวลาที่ระเบียบระดับภูมิภาคกำลังถูกเขียนขึ้นใหม่ ไฮไลท์การประชุม 1. แนวโน้มตลาดเหล็กอาเซียน การวิเคราะห์เชิงลึกเกี่ยวกับอุปสงค์เหล็กในภูมิภาค โดยคาดว่าในปี 2026 การบริโภคจะพุ่งสูงถึง 87.9 ล้านเมตริกตัน ซึ่งขับเคลื่อนหลักจากเวียดนาม อินโดนีเซีย และฟิลิปปินส์ 2. การปรับโครงสร้างการค้าและห่วงโซ่อุปทานจีน-อาเซียน สำรวจกระแสการไหลเวียนที่เปลี่ยนไปของเหล็กแผ่นรีดร้อน (HRC) บิลเล็ต สแล็บ และผลิตภัณฑ์เหล็กอื่นๆ ท่ามกลางรูปแบบอุปทานที่เปลี่ยนแปลง มาตรการเยียวยาทางการค้า และพลวัตของตลาดในภูมิภาค 3. การขยายกำลังการผลิตและการเปลี่ยนผ่านด้านการผลิต ตรวจสอบภูมิทัศน์การผลิตเหล็กที่กำลังเปลี่ยนโฉมของอาเซียน รวมถึงการเติบโตของกำลังการผลิตแบบ BF-BOF การพัฒนาแบบ EAF การลงทุนจากต่างประเทศ และศูนย์กลางการผลิตแห่งใหม่ในภูมิภาค 4. นโยบายทางการค้าและการเข้าถึงตลาด ประเมินมาตรการต่อต้านการทุ่มตลาด ภาษีศุลกากร โอกาสที่เกี่ยวเนื่องกับ RCEP และการเปลี่ยนแปลงเชิงกฎระเบียบที่กำลังพลิกโฉมการค้าเหล็กทั่วอาเซียน 5. อุปสงค์ที่เติบโตสูงและโอกาสด้านผลิตภัณฑ์ ระบุโอกาสจากโครงสร้างพื้นฐาน การก่อสร้าง ยานยนต์ และการประยุกต์ใช้เหล็กขั้นสูง โดยมุ่งเน้นไปที่อินโดนีเซีย เวียดนาม และตลาดเกิดใหม่อื่นๆ 6. การสร้างเครือข่ายผู้บริหารและความร่วมมือระดับภูมิภาค เชื่อมโยงผู้ผลิตชั้นนำ ผู้ค้า ผู้ซื้อ นักลงทุน สมาคม ผู้กำหนดนโยบาย และผู้เชี่ยวชาญในอุตสาหกรรมจากทั่วอาเซียน จีน และตลาดโลก วิทยากรอาวุโส 2026 ภาพเหตุการณ์จากการประชุมครั้งที่ผ่านมา ระเบียบวาระการประชุม ติดต่อ: Horin Dong WhatsApp: +8618721310824 อีเมล: horindong@smm.cn สแกนคิวอาร์โค้ดสำหรับรายละเอียดการประชุมและข้อมูลส่วนลดเพิ่มเติม เกี่ยวกับ SMM SMM สั่งสมประสบการณ์อย่างลึกซึ้งในบริการอุตสาหกรรมสินค้าโภคภัณฑ์ระดับโลกมาอย่างยาวนาน พร้อมสานต่อความสัมพันธ์ความร่วมมือกับหน่วยงานภาครัฐ องค์กรวิสาหกิจ และสมาคมอุตสาหกรรมในประเทศต่างๆ ให้แน่นแฟ้นยิ่งขึ้น และขยายเครือข่ายบริการอุตสาหกรรมระดับโลกอย่างต่อเนื่อง ด้วยการใช้ประโยชน์จากรูปแบบความร่วมมือที่เติบโตเต็มที่กับภาครัฐ วิสาหกิจ และสมาคมต่างๆ ในอินโดนีเซีย SMM ได้สร้างระบบนิเวศแบบวงจรปิดที่ครอบคลุมสำหรับการแบ่งปันข้อมูลนิทรรศการและการประชุมในต่างประเทศ พร้อมทั้งยกระดับระบบข้อมูลขนาดใหญ่ของอุตสาหกรรมอย่างไม่หยุดยั้ง เพื่อให้บรรลุการแลกเปลี่ยนข้อมูลตลาดโลกอย่างมีประสิทธิภาพ การร่วมสร้างและแบ่งปันทรัพยากร SMM จัดงาน มากกว่า 50 งานระดับมืออาชีพในแต่ละปี ครอบคลุมการประชุมสุดยอดอุตสาหกรรม ฟอรั่มอุตสาหกรรม และการดูงานภาคสนาม ในจำนวนนี้ 40 งานมีรากฐานอย่างลึกซึ้งในตลาดจีน เกือบ 10 งานถูกจัดวางอย่างแม่นยำในตลาดหลักของเอเชียตะวันออกเฉียงใต้ และส่วนน้อยครอบคลุมยุโรปและแอฟริกา งานในต่างประเทศได้รับการยอมรับในระดับอุตสาหกรรมโลกจากรายชื่อแขกในแวดวงที่ทรงอำนาจ ข้อมูลสำรวจอุตสาหกรรมที่เป็นเนื้อแน่น และบริการจับคู่อุปสงค์-อุปทานที่แม่นยำ SMM ได้จัดการประชุมสุดยอดระดับสูงในอินโดนีเซียหลายครั้ง โดยร่วมมือกับหน่วยงานท้องถิ่น อาทิ กระทรวงการต่างประเทศ และสมาคมผู้ทำเหมืองนิกเกิลอินโดนีเซีย (APNI) ซึ่งรวบรวม กว่า 300 ผู้เชี่ยวชาญในอุตสาหกรรม และยังเสริมด้วยกิจกรรมดูงานภาคสนามตามห่วงโซ่อุตสาหกรรมในต่างประเทศอย่างมืออาชีพ เพื่อเสริมพลังให้กับการแลกเปลี่ยนทางอุตสาหกรรมและการจับคู่ทางการค้าของภูมิภาคอย่างรอบด้าน

3 Aug 2026 10:16

SMM AICE เยือน VAFIE: เข้าใจตรรกะเบื้องหลังการขยายธุรกิจของบริษัทอะลูมิเนียมจีนในเวียดนาม

14 ชั่วโมงที่แล้ว

SMM เยือน VPG: สัญญาณสำคัญใดที่กลุ่มบริษัทเวียดนามนี้กำลังส่งถึงบริษัทอะลูมิเนียมจีน?

3 Aug 2026 16:42

จีนบรรจุหน่วยงานของสหภาพยุโรปลงในบัญชีเฝ้าระวังการควบคุมการส่งออก เล็งเป้าห่วงโซ่อุปทานแร่หายาก【SMM Analysis】

29 Jul 2026 19:06

สหรัฐฯ เข้มงวดการเข้าถึงอินเวอร์เตอร์เชื่อมต่อใหม่: ผลกระทบต่อตลาดปัจจุบันคืออะไร? [บทวิเคราะห์ SMM]

29 Jul 2026 16:48

![[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)

[SMM Analysis] เกาหลีใต้วางแผนเข้มงวดการสำแดงการส่งออกเศษทองแดง—กระแสการค้าในเอเชียจะเปลี่ยนไปหรือไม่?

29 Jul 2026 16:31

![[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้](https://imgqn.smm.cn/usercenter/yUOUz20251217171732.jpg)

[บทวิเคราะห์ SMM] ต้นทุน CBAM เริ่มมีผลบังคับใช้ กำลังการตรวจสอบล่าช้า: สิ่งที่ผู้ส่งออกเหล็กกล้าไร้สนิมต้องรู้

29 Jul 2026 13:53

ข่าวล่าสุด

ราคาทองแดงพุ่งแตะระดับสูงสุดในรอบสองเดือน ขณะที่เงินทุนไหลเข้าจากสหรัฐฯ เพิ่มขึ้นอย่างมากก่อนการตัดสินใจด้านภาษี

20 นาทีที่แล้ว

【SMM Flash】ประกาศราคาสัญญาซัลเฟอร์ตะวันออกกลางเดือนสิงหาคมแล้ว

7 ชั่วโมงที่แล้ว

เหมืองทองแดงโคเอมาคาอูเพิ่มผลผลิตไตรมาส 2/2026 การขยายกำลังการผลิตตามแผน

8 ชั่วโมงที่แล้ว

ข้อมูล: ความเคลื่อนไหวตลาด SHFE, DCE (5 ส.ค.)

9 ชั่วโมงที่แล้ว

ราคาทองแดงแข็งค่าขึ้น ตลาดซื้อขายเศษทองแดงคึกคัก [SMM บทวิเคราะห์รายวันทองแดงทุติยภูมิ]

9 ชั่วโมงที่แล้ว

คนงานเหมืองในแซมเบียเรียกร้องนโยบายส่งเสริมการผลิตทองแดงและโครงสร้างพื้นฐานก่อนการเลือกตั้ง

9 ชั่วโมงที่แล้ว

SMM เยี่ยมชมบริษัท หนิงปัว จินหลง คอปเปอร์ อินดัสทรี จำกัด เพื่อร่วมสำรวจโอกาสการพัฒนาในอุตสาหกรรมแปรรูปแท่งทองแดงและกระชับความร่วมมือห่วงโซ่อุตสาหกรรม

10 ชั่วโมงที่แล้ว

ความเสี่ยงแผ่นดินไหวระดับลึกปรากฏ; Codelco ระงับโครงการขยาย Andes Norte ที่เหมืองทองแดง El Teniente [บทวิเคราะห์ SMM]

10 ชั่วโมงที่แล้ว

การกลับตัวของ Parity นำเข้าและส่วนเพิ่มราคาตลาดอ่อนตัว; จับตาสถานการณ์ส่งออกของจีนต่อไป

11 ชั่วโมงที่แล้ว

ซัพพลายเออร์ลดราคาซ้ำๆ เพื่ออำนวยความสะดวกในการทำธุรกรรม ค่าพรีเมียมทองแดงสปอตเซี่ยงไฮ้โดยเฉลี่ยปรับตัวลดลง [SMM Shanghai spot copper]

11 ชั่วโมงที่แล้ว

มีรายงานว่า FCC กำลังร่างคำสั่งห้ามส่วนประกอบศูนย์ข้อมูลของจีน รวมถึงโมดูลออปติคัล

11 ชั่วโมงที่แล้ว

Baoming Tech พัฒนาฟอยล์ทองแดง HVLP4/5 สำหรับเซิร์ฟเวอร์ AI รอการตรวจสอบจากลูกค้า

11 ชั่วโมงที่แล้ว

อัตราส่วนราคา SHFE/LME แย่ลงอีก, อุปสงค์ปลายน้ำอ่อนแอ, ศูนย์กลางพรีเมียมปรับลดลง [SMM ทองแดงสปอตหยางซาน]

13 ชั่วโมงที่แล้ว

ผลงานตลาด NEV เดือนกรกฎาคมโดดเด่น

13 ชั่วโมงที่แล้ว

สินค้าคงคลังลดลง ซัพพลายเออร์คงราคา แต่ผู้ซื้อปลายน้ำซื้ออย่างระมัดระวัง [SMM ทองแดงสปอตจีนตอนใต้]

13 ชั่วโมงที่แล้ว

ราคาทองแดงสูงฉุดการซื้อ การซื้อขายซบเซาฉุดพรีเมียมสปอตจีนตอนเหนือ [SMM North China Copper Spot]

13 ชั่วโมงที่แล้ว

อุปสงค์นอกฤดูผนวกกับราคาทองแดงที่สูง สร้างแรงกดดันต่อการผลิตสายไฟและสายเคเบิลในเดือนกรกฎาคม [SMM Analysis]

13 ชั่วโมงที่แล้ว

[SMM Flash] ประกาศราคาแนะนำกรดซัลฟิวริกของจีนประจำเดือนสิงหาคมแล้ว คำนวณโดยใช้ดัชนีแร่ทองแดงเข้มข้นของ SMM

14 ชั่วโมงที่แล้ว

Prysmian ใช้ทองแดงรีไซเคิล 100% 10,000 ตันในโครงการสายเคเบิลใต้ทะเลในสหราชอาณาจักร

15 ชั่วโมงที่แล้ว

แคนาเดียน คอปเปอร์เข้าควบคุมแหล่งคาริบู ขณะที่การทบทวน EIA ของเมอร์เรย์ บรูกคืบหน้า

15 ชั่วโมงที่แล้ว