SMM, October 17:

This week, China's domestic tungsten market showed an overall stable performance. On the upstream side, most spot mine transactions were conducted around long-term contract prices, but trading volume was limited. After months of consecutive declines in the operating rate of the ammonium paratungstate (APT) industry, the market's hidden inventory remained low. Additionally, enterprises mainly delivered goods according to long-term contracts, which further intensified the tight circulation of spot orders. Manufacturers maintained firm quotations, and market transaction prices moved upward during the week.

The tungsten scrap market has also emerged from the pessimistic sentiment caused by previous market selling pressure. With recyclers holding low inventory, transaction prices were forced to rebound. After the holiday, prices in the overseas tungsten market rebounded rapidly, and the price gap with the domestic market narrowed quickly, reopening the export window for ferrotungsten and APT.

1. Mine Segment

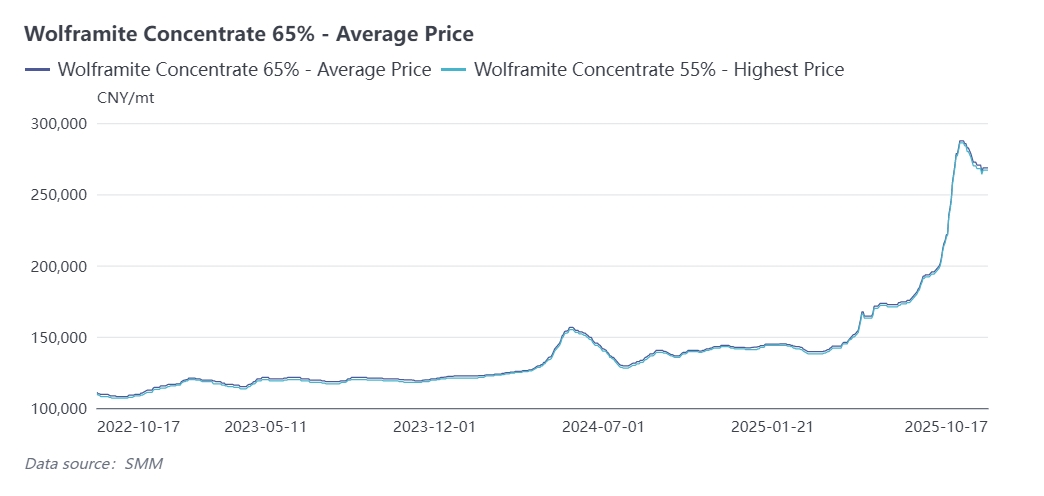

As of October 17, SMM quoted the price of 65% wolframite concentrate at 268,000 - 269,000 yuan per standard ton, up 3,000 yuan per standard ton compared with last Friday. During the week, mines in Guangxi, Guangdong and other regions sold goods through auctions, but downstream smelters showed low enthusiasm for participation, and market transactions remained sluggish.

In addition, it is reported that a large tungsten mine in Hunan has resumed production of scheelite concentrate, which is mainly for internal use within the group. Follow-up attention should still be paid to the output release of this enterprise.

Ammonium Paratungstate (APT)

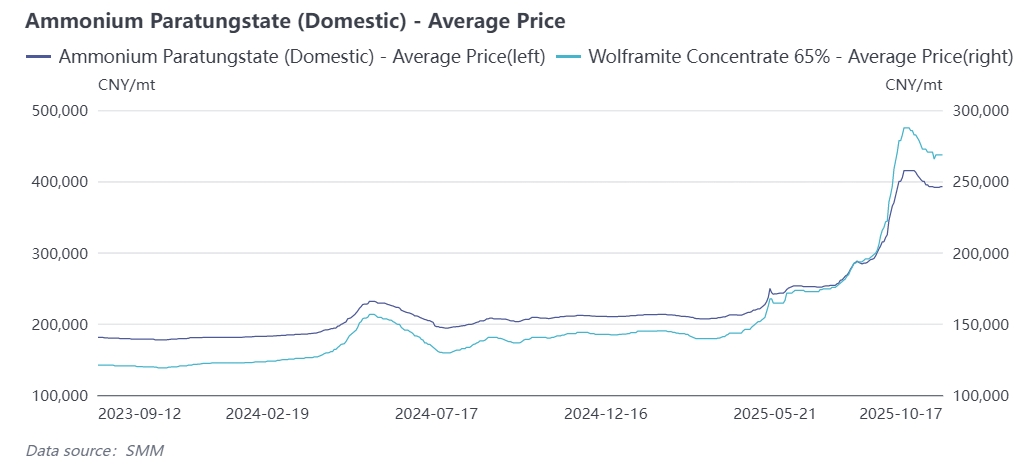

Today, SMM quoted the price of APT (≥88.5%) at 390,000 - 395,000 yuan per ton, up 1,000 yuan per ton from last Friday. China's APT industry faces significant cost pressure, and its operating rate has declined month by month. The industry operating rate dropped to below 60% in September. Some enterprises mainly focus on ensuring long-term contract supply, leading to a significant decrease in the circulation of spot orders and speculative transactions in the industry. The market's bargaining focus has moved upward, with some manufacturers quoting prices as high as around 400,000 yuan per ton.

The overseas tungsten market fluctuated strongly. As of today, European APT is quoted at 600 - 680 US dollars per ton-unit (converted to 378,000 - 422,000 yuan per ton), up 20 US dollars per ton-unit from before the holiday. The price gap between domestic and overseas markets has narrowed, and the export window is expected to open.

Tungsten Powder Market

This week, the tungsten powder market showed a divergent trend. Downstream cemented carbide enterprises had low enthusiasm for restocking after the holiday, and market transactions showed a slight decline. As of today, SMM quoted the price of tungsten carbide powder at 600 yuan per kilogram, down 8 yuan per kilogram from last Friday; tungsten powder was quoted at 615 yuan per kilogram, down 10 yuan per kilogram from last Friday.

Recently, raw materials such as cobalt powder have shown strong performance, putting significant cost pressure on downstream cemented carbide enterprises. The quotations for tungsten-cobalt alloy products have increased compared with the previous period.

Ferrotungsten

This week, ferrotungsten market transactions were average. However, due to rising costs, ferrotungsten enterprises intended to maintain firm prices for sales, but actual order follow-up was limited, and prices mainly fluctuated within a narrow range. Today, the mainstream quotation for 70% ferrotungsten is concentrated at 380,000 - 385,000 yuan per ton, down 5,000 yuan per ton from last Friday.

European ferrotungsten prices continued to rise; this week, European ferrotungsten closed at 86 - 89.5 US dollars per kilogram of tungsten.

Tungsten Scrap

The circulation of spot goods in the tungsten scrap market decreased. In addition, the industry cleared a large amount of inventory before the holiday, and downstream enterprises entered a period of concentrated restocking after the holiday. Holders maintained firm quotations, and the transaction focus moved upward. Today, SMM quoted the price of waste tungsten bars at 410 yuan per kilogram, up 33 yuan per kilogram from last Friday, basically recovering the previous decline.

Smelting-side operating rates shrink and profits are under pressure, reducing market liquidity

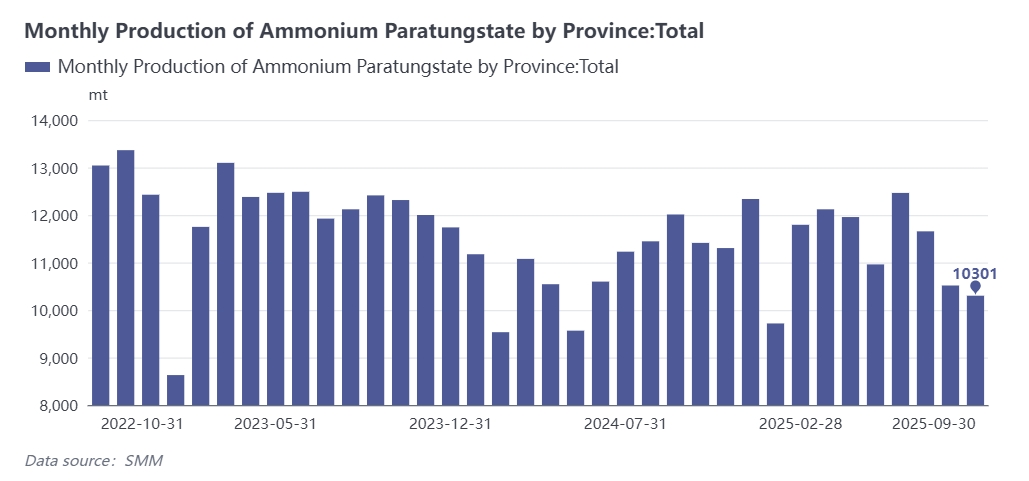

In September 2025, China's APT industry continued the trend of "shrinking operating rates + profit pressure", and the recovery of production was weaker than expected.

- Dual decline in output and operating rates: According to incomplete statistics from SMM, China's APT output in September decreased slightly month-on-month and dropped by 14% year-on-year. The industry operating rate fell by 1.4 percentage points month-on-month to 69.3%, and the continuous shrinking trend has not changed.

- Core reasons for restricted operation: On one hand, APT production is still dominated by "raw material constraints + high costs" - the cost of raw material procurement accounts for more than 85%, and the price of mines rises faster than the price of products, further squeezing the processing profits of enterprises and leaving them with no incentive to expand production. On the other hand, some APT enterprises that suspended production for maintenance due to cost pressure in August did not fully resume full-load production in September. The daily output of some resuming enterprises in Jiangxi was only 70% of that before maintenance. In addition, 2-3 small enterprises extended maintenance to October due to capital pressure or raw material shortages.

- Cost-profit inversion: The average cost of the APT industry in September was as high as 404,000 yuan/ton. Based on the spot price in the same month, the industry suffered an average loss of about 670 yuan/ton. The high cost further suppressed the enthusiasm for starting production.

Divergent operating conditions of end enterprises, with resilience in emerging sectors and exports

In September, the downstream end of the tungsten industry showed a pattern of "sluggish traditional demand, while emerging sectors and exports show resilience". Weak traditional demand was the core driver of the pre-holiday price pullback.

- Divergent operating conditions of cemented carbide enterprises: Affected by weak end demand, downstream cemented carbide enterprises mainly focused on destocking in September. They had a strong wait-and-see attitude towards procurement, and the bargaining focus continued to move downward, putting the smelting-side products such as APT under dual pressure of "cost + demand" and making it more difficult to secure new orders. Orders in emerging fields such as military industry were concentrated in medium and large enterprises, while small enterprises lost a large number of orders, and the industry concentration was higher than in previous years.

- Medium and long-term demand support: From the data perspective, China's metal machine tool output from January to August 2025 reached 564,000 units (up 14.6% year-on-year). The output of tungsten end products such as construction machinery remained stable and positive, driving the growth of tungsten consumption. The high-value-added segment performed prominently - in August, the export of cemented carbide cutting tools and inserts for metalworking machinery reached 286.8 tons (up 1.0% month-on-month and 4.1% year-on-year), with a cumulative year-on-year decrease of only 0.4% from January to August, benefiting from the global manufacturing demand for precision machining tools. The export of tungsten halogen lamps performed brilliantly, with 114 million units exported in August (a sharp 101.4% month-on-month surge and 46.2% year-on-year increase), and a cumulative year-on-year growth of 19.6% from January to August.

- Slowing growth of tungsten for photovoltaic applications: Affected by the high cost of the photovoltaic industry and industry competition, it is expected that the output of silicon wafers may decline in the fourth quarter (China's silicon wafer output from January to September was 488.17 GW, a year-on-year decrease of 5.58%). Although the penetration rate of the tungsten wire industry has driven an increase in tungsten used for photovoltaics compared with last year, the subsequent growth rate will continue to slow down.

![[SMM Analysis] What Drove Global Tungsten Markets in March? Offshore Prices Up 30%, China Enters Consolidation](https://imgqn.smm.cn/usercenter/eGQFu20251217171723.jpeg)

![[SMM Analysis] Chinese Tungsten Market Cools While Overseas Prices Sustain Gains – Long-Term Outlook Remains Bullish](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)