SMM December 4th News:

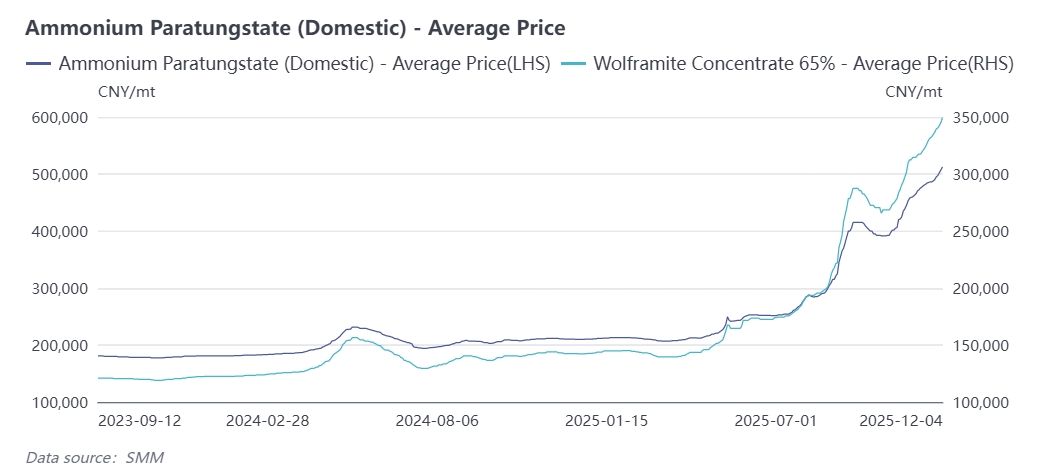

Since late October, the global tungsten market has once again embarked on a unilateral upward trend. As of December 4th, the price of 65% black tungsten concentrate has hit a record high of 350,000 yuan per standard ton, with a cumulative year-to-date increase of 145%. Ammonium Paratungstate (APT) prices have risen to 512,500 yuan per ton, up 143% year-on-year. Tungsten Carbide (WC) powder is quoted at 785 yuan per kilogram, a 152% increase since the start of the year, while tungsten powder stands at 820 yuan per kilogram, surging 160% year-to-date. Driven by the rally in upstream raw materials, the entire tungsten industrial chain has witnessed a synchronized upward movement. Given that the supply-demand imbalance in the tungsten market is unlikely to be resolved in December, the upward trend across the whole industrial chain is expected to continue. SMM analyzes the drivers behind this round of price increases based on the following factors:

① Domestic tungsten mining quotas issued gradually across provinces in November; full-year quota expected to be lower than 2024

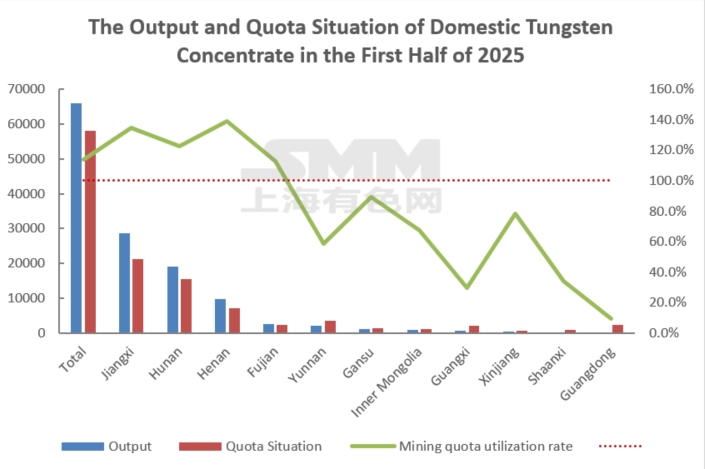

China accounts for 52% of global tungsten reserves and has long contributed over 80% of global output, serving as the core supply hub for the global tungsten market. Controlling domestic production through mining quotas not only prevents the excessive depletion of domestic resources but also secures China’s initiative in the global tungsten industrial chain. Coupled with subsequent export control policies, this forms a full-chain regulation of strategic resources to safeguard national industrial security. To ensure the sustainable utilization of resources, China officially implemented total mining volume control for tungsten in 2002. Policies have since been refined: in 2018, the Ministry of Natural Resources issued a notice specifying that new tungsten mining rights must comply with total volume control requirements. Starting from 2021, quotas have been issued in two batches to enhance regulatory precision. Meanwhile, in conjunction with environmental and safety supervision, no quotas are allocated to suspended mines, gradually phasing out non-compliant production capacity and making quotas a key tool to standardize industrial capacity and guide high-quality development. The delayed issuance of the second batch of domestic quotas in the second half of this year has left some mines without available quotas from September to November, resulting in slow production release. With the issuance of provincial quotas in November, some provinces launched tender-based shipments. However, mainstream mines report that the quotas allocated to their enterprises have not increased month-on-month or year-on-year, with some provinces even recording a year-on-year decline. Considering that the first batch of quotas decreased by 4,000 standard tons year-on-year, the total domestic tungsten concentrate mining quota for 2025 is expected to be lower than the 114,000 tons recorded in 2024.

② Low utilization rate of 25% of quotas restricts total industrial output

In previous years, the quota system was plagued by loopholes such as overproduction and inadequate supervision of associated tungsten mines. However, 2025 marks a crucial turning point in quota trends, with significantly strengthened regulatory oversight and almost zero possibility of industry overmining. According to the first batch of tungsten mining quotas, the three major domestic production regions—Jiangxi, Hunan, and Henan—accounted for 43,900 tons, or 75.7%, of the total domestic quota. Actual output in these three provinces in the first half of this year basically fully utilized the quotas, with some mines facing shortages. In contrast, regions such as Yunnan, Guangdong, and Guangxi have low quota utilization rates due to insufficient mine operation. Regional quota allocation issues may restrict the 2025 actual output from exceeding the total quota, exacerbating supply tightness.

③ Large mines slow down shipment pace at year-end, worsening supply constraints

As the year draws to a close, some mines have completed their full-year operational targets and slowed down shipment rhythms, further reducing market liquidity. In 2025, mining costs have increased due to higher environmental protection expenses and declining ore grades. Nevertheless, with the tungsten market fluctuating at high levels, tungsten resources have prominent strategic value, and the industry enjoys substantial profitability. After achieving phased goals, mines have slowed shipments.

④ High prices continue to transmit downstream; profit margins in intermediate smelting links recover

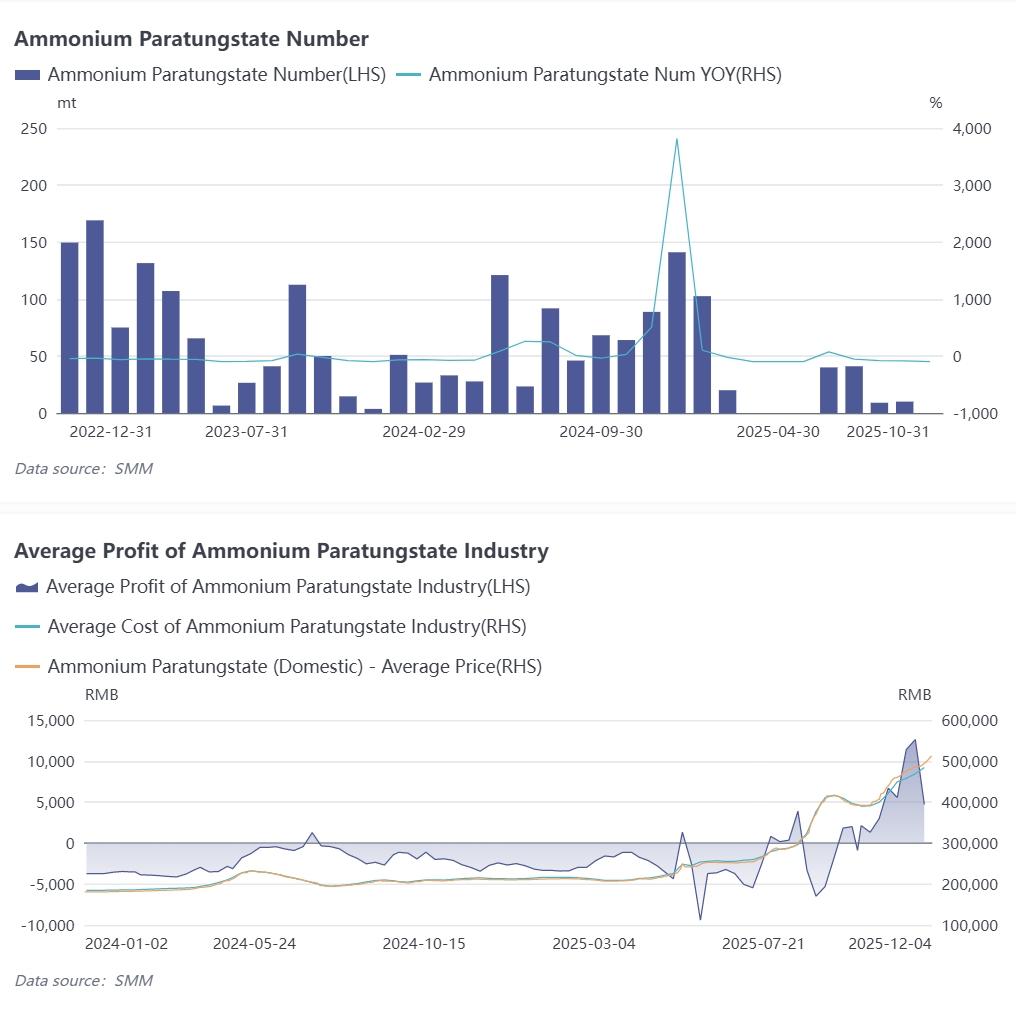

November witnessed a significant shift in the tungsten market: APT smelters turned from loss to profit, benefiting not only from the transformed supply-demand structure in the APT industry but also reflecting the smooth transmission of high prices. According to SMM data, domestic APT output in November 2025 increased by 1.5% month-on-month but fell by approximately 6% year-on-year. The operating rate of the APT industry in October was about 70.4%, a month-on-month increase of 0.3 percentage points. The average monthly price of 65% black tungsten concentrate in November 2025 was 321,300 yuan per standard ton, translating to an average APT production cost of around 465,000 yuan per ton. The industry thus shifted to profitability, with an average monthly profit of approximately 8,560 yuan per ton in November.

⑤ Downstream orders flow back to leading enterprises; lack of alternative materials in the market

Cost pressures from rising tungsten prices continue to transmit downstream. Downstream enterprises such as cemented carbide and cutting tool manufacturers have consecutively raised product prices from September to November, with on-hand order prices significantly higher than the average in the third quarter. Overseas, South Korean tungsten hexafluoride manufacturers have proposed a 70%-90% increase in next year’s contract prices due to doubling tungsten powder costs. Successive price hikes of terminal tungsten products are also testing the downstream application structure: some traditional civil industries have begun seeking alternative materials, but high-end application fields lack viable substitutes. Small and medium-sized enterprises (SMEs) face a dilemma of high capital pressure for raw material stockpiling and slow incoming terminal orders, forcing them to reduce production and cede market share to large enterprises.

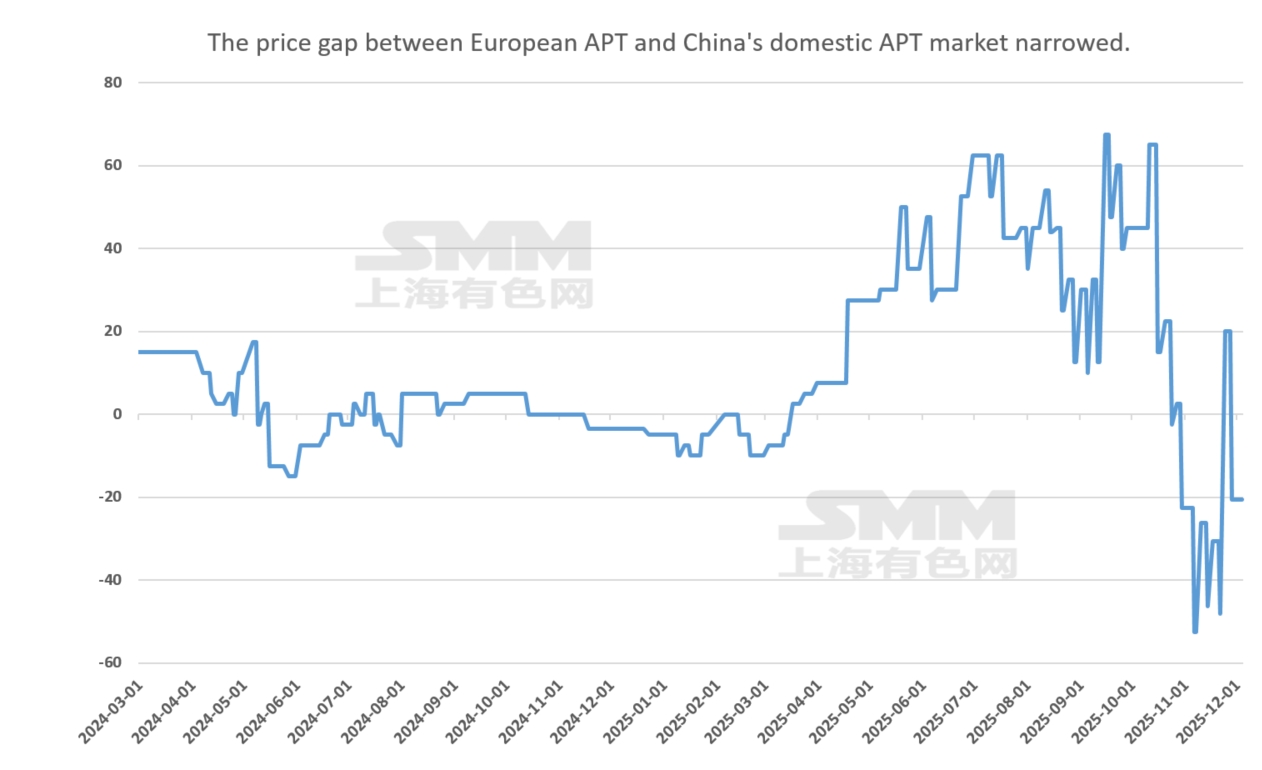

⑥ Weak global supply and demand; tungsten product premium partially recovered in November

As the world’s leading tungsten producer, China imposed export controls on APT, tungsten carbide, and tungsten powder in February this year, triggering a sharp rise in the overseas tungsten market and a significant premium for APT and other products. However, stimulated by domestic supply-demand imbalances in the second half of the year, domestic tungsten prices surged rapidly, while overseas markets followed suit sluggishly, leading to an internal-external price inversion in the third quarter and a decline in the tungsten premium. In November, driven by factors such as reduced production at Vietnam’s Masan Tungsten and the inclusion of tungsten in strategic metals by the EU and U.S. governments, the overseas tungsten market quickly followed the domestic rally. Nevertheless, terminal order follow-up remains slow, reflecting weak supply and demand, with some prices still lower than domestic levels, leaving room for further increases.

![Transaction Pushed Magnesium Prices Up, Today's Magnesium Prices Hold Up Well [SMM Analysis]](https://imgqn.smm.cn/usercenter/CkvAg20251217171724.jpg)

![[SMM Magnesium Analysis] China Magnesium Trade Faces Challenges Amid Geopolitical Tensions and Export Controls](https://imgqn.smm.cn/usercenter/teIej20251217171724.jpeg)