SMM News on June20:

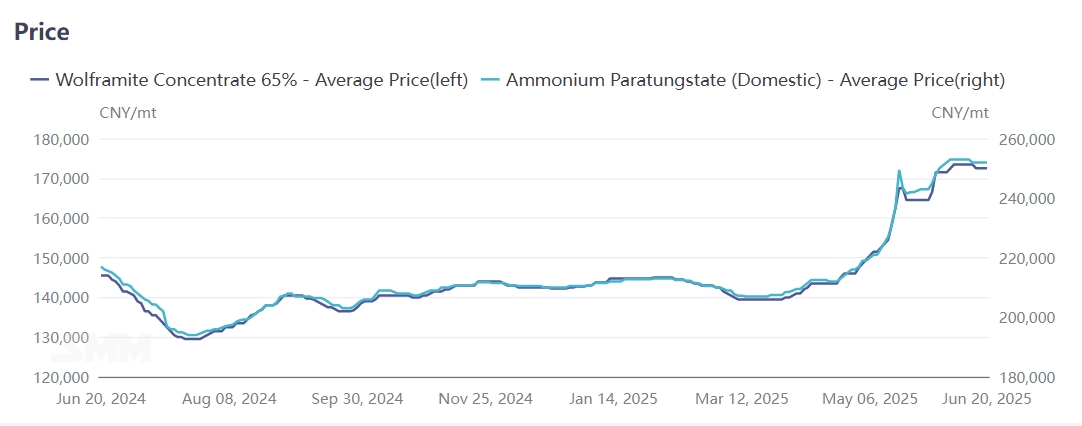

On June 20, major domestic tungsten enterprises successively finalized long-term supply prices for tungsten concentrate and APT products. Among them, the long-term contract price of national standard black tungsten concentrate was locked in the high range of 171,000-172,000 RMB/metric ton-degree, and the APT long-term price was anchored at 251,000 RMB/ton. The landing of high-level long-term orders from large manufacturers has consolidated the support for the "high-level operation" of the tungsten market in late June, with the market trend becoming clear and prices expected to maintain a high-level in the short term.

Looking back at the first half of 2025, driven by multiple factors such as policy regulation, explosive demand, and geopolitical games, global tungsten market prices fluctuated upward, with a sharp acceleration in the second quarter. Core products such as tungsten concentrate and ammonium paratungstate (APT) hit record highs successively. As of June 20, the domestic 65% black tungsten concentrate was quoted at 172,500 RMB/metric ton-degree, up 20.8% from the beginning of the year; APT closed at 252,000 RMB/ton, with a year-to-date increase of 19.7%. Other tungsten intermediates and downstream products generally followed the rise, with increases ranging from 19% to 21%.

The overseas market was more significantly impacted by China's export controls. Since February 2025, China's tungsten export controls have caused disruptions in overseas supply chains, leading to a rapid surge in European APT prices. As of June 18, the European APT price was quoted at 430 USD/ton-degree, up 30.3% from the beginning of the year; European tungsten ferroalloy closed at 51.85 USD/kg Mo, with a year-to-date increase of 17.8%.

China's Tightened Supply Dominates Global Tungsten Chain Pricing

According to USGS data, global tungsten reserves stood at 4.6 million metal tons as of 2024, with China holding 2.4 million tons (52% of the global total), giving it an absolute dominant position in the global tungsten market. Other major tungsten resource hubs include Australia (12%), Russia (9%), and Vietnam (3%). As a strategically advantageous mineral in China, tungsten resource development is subject to comprehensive policy regulation across four dimensions: industry access, total quantity control, export restrictions, and tax guidance.

Since 1991, tungsten has been designated by the State Council as a "specific mineral under protective mining," and since 2000, a combination of total output controls and the export quota system implemented in February 2025 has restricted new production capacity. The market supply now relies primarily on existing projects, stabilizing the industry landscape.

Secondly, Overseas New Tungsten Concentrate Capacity Release Is Slow & Downstream Smelting Chain Is Incomplete

In 2025, new overseas tungsten concentrate output will mainly come from new projects in South Korea and Kazakhstan. The South Korean Sandong tungsten mine plans to start production in the second half of 2025, with an annual output of 2,300 tons after the first-phase commissioning (calculated in terms of tungsten trioxide). The Boguty tungsten mine project in Kazakhstan was completed and put into operation at the end of 2024, and is expected to process 3.3 million tons of tungsten ore annually after full capacity, with an estimated output of 5,000 metric ton-degrees of tungsten concentrate in 2025. Other new mining projects show little change.

Moreover, the overseas tungsten smelting sector is incomplete—even if many countries and regions have tungsten concentrate, it is difficult to process it into other tungsten products. This leads to lower overseas ore-end prices than domestic ones, creating an import window for China. As both a major producer and importer of tungsten concentrate, China saw total tungsten concentrate imports reach 5,153 tons from January to May 2025, up 46.3% year on year.

Downstream Demand Stable & Overseas Geopolitical Instability Stimulates Strategic Tungsten Stockpiling

In the first half of 2025, domestic terminal demand for tungsten remained stable, with high-end manufacturing providing growth points. Demand for tungsten in humanoid robots, cutting machines, and other fields grew steadily, while traditional sectors like photovoltaic tungsten wires showed lackluster performance.

Moreover, since the implementation of domestic tungsten product export controls in February, exports of tungsten intermediates have significantly declined, but exports of terminal tungsten products have increased notably, driving up the export value-added of China's tungsten industry chain. Taking cemented carbide products and drills/drilling machines as examples, customs data shows that:

- Exports of cemented carbide products from January to May 2025 increased by about 31% year on year, with a marked acceleration in the second quarter.

- Exports of drills and drilling machines rose by approximately 22.3% year on year over the same period.

Additionally, tungsten demand in the military sector has significantly increased in 2025. Overseas geopolitical conflicts, coupled with global arms upgrades (such as the European "Celestial Law Program"), have made tungsten irreplaceable in military products like missile components and cutting tools. The continuous overseas military disturbances have to a certain extent driven the growth of tungsten metal material demand.

Comprehensive Analysis: Key Drivers and Outlook for Tungsten Market

The sustained high-level operation of the tungsten market is primarily driven by:

- Tightened supply-demand dynamics at the mine end, compounded by historically low global tungsten inventories;

- Global supply constraints triggered by China's export controls on tungsten products.

Entering the second half of June, the tungsten market has entered a phase of long-short gaming. While raw material prices (e.g., tungsten concentrate) remain high, the slow follow-up in prices of tungsten powder and chemical products has exposed acute contradictions of poor corporate profitability, curbing further price surges.

In the medium to long term:

- Reduced domestic tungsten concentrate output and declining ore grades may become the new normal;

- Sluggish growth in overseas supply will maintain tightness at the mine end.

Coupled with the current low-inventory landscape, the market will likely see replenishment demand driven by rising terminal consumption. This could reshape profit distribution along the tungsten industry chain, supporting a prolonged pattern of high-range volatility in overall prices.

![Transaction Pushed Magnesium Prices Up, Today's Magnesium Prices Hold Up Well [SMM Analysis]](https://imgqn.smm.cn/usercenter/CkvAg20251217171724.jpg)

![[SMM Magnesium Analysis] China Magnesium Trade Faces Challenges Amid Geopolitical Tensions and Export Controls](https://imgqn.smm.cn/usercenter/teIej20251217171724.jpeg)