SMM7 March 23:

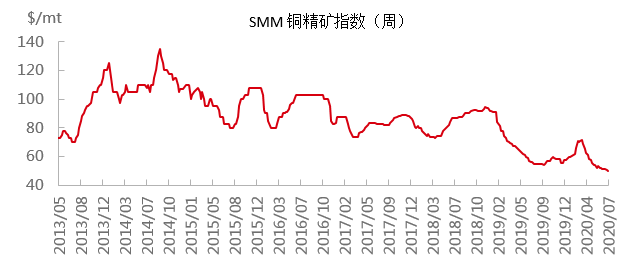

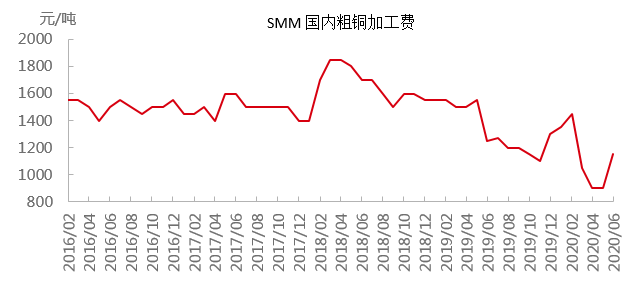

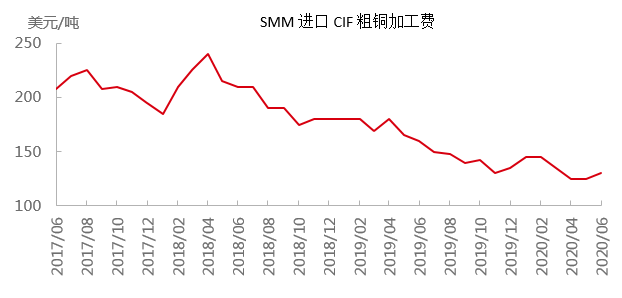

In June, the SMM copper concentrate index reached US $51.71 / ton, down US $1.76 / ton from the previous month, marking the third consecutive month of decline; while in June, the processing fee for domestic crude copper was 1100m2 yuan / ton, an increase of 150yuan / ton over the previous month; and the processing fee for imported CIF crude copper was US $125,135m / ton in June, up US $5 / ton from the previous month. Since March, due to the interference of overseas raw materials, TC and RC began to decline synchronously, but crude copper processing fees first rebounded in June, especially after entering July, the deviation between TC and RC intensified. On July 17, the SMM Copper concentrate Index (week) reached US $49.85 / ton, and the TC trading center has broken through the 50 hurdles, while the domestic crude copper processing fee to the factory price is currently about 1300 yuan / ton, and the import CIF crude copper processing fee has reached the level of 140USD / ton.

Crude copper as an intermediate product in the process of producing electrolytic copper from copper concentrate, mineral crude copper accounts for the vast majority of the source of crude copper, so there is a strong relationship between its supply and demand situation and copper supply and demand, and the trends of TC and RC are usually similar. But after June, with the mine supply still tight and overseas CCS and some domestic refineries overhauled, why did RC rise sharply independent of TC?

According to SMM analysis, although TC and RC have a strong correlation, they reflect the respective supply and demand of copper concentrate and crude copper market. As an important part of domestic negotiable crude copper, crude copper from scrap copper has an obvious impact on crude copper processing fees. Therefore, it is necessary to analyze the supply and demand of copper concentrate and crude copper market separately: although the operating rate of Peruvian mines continues to pick up, according to the government's plan to resume work by the end of June, the operating rate has increased to more than 80%. However, on the one hand, the number of newly diagnosed patients in Chile maintained a high level, and wage negotiations in some mines in the superimposed territory faced strikes, and the supply-side uncertainty persisted; on the other hand, more domestic copper concentrates went out of storage in the second quarter, and the raw material stocks of some refineries were close to the margin of safety, with a strong willingness to purchase and increase, and there was great pressure on both sides of supply and demand on TC. As for crude copper, due to the continuous rise in copper prices, starting from late May, the supply of scrap copper at home and abroad took the lead to recover, and the price advantage of scrap copper was obvious, squeezing out the demand for crude copper. On the other hand, overseas logistics began to resume in June, and crude copper shipments increased in July, while imported crude copper supplies were abundant. After the recovery of the long order supply of crude copper in the smelter itself, it has also reduced the purchasing demand in the zero order market. As a result, crude copper processing fees have risen. Due to the increase in domestic crude copper supply from the hazardous waste recycling industry, some refineries reduced procurement in the spot market, and sharply raised the quotation of domestic crude copper processing fees, leading to a more obvious increase in domestic prices.

So, can the rise in crude copper processing fees ease the current tight situation of domestic copper raw material supply?

SMM believes that there is a partial substitution relationship between copper concentrate and crude copper as raw materials for electric copper production, and the recent upside of crude copper processing fees can alleviate the tension of domestic copper raw materials to some extent, but the effect is relatively limited for the following reasons. The main results are as follows: 1. In the raw material structure of most crude refineries, the ratio of copper concentrate to crude copper is relatively fixed, and the raw material source mainly depends on copper concentrate, and the purchase proportion of crude copper will not increase obviously when the crude copper processing cost is dominant. 2. The upside of crude copper processing fees is mainly driven by the increase in the supply of crude copper produced by scrap copper, which is more due to the rise in copper prices and the release of inventory in the hands of domestic channel merchants, rather than an increase in domestic scrap copper supply, and overseas Europe and the United States and other countries have doubts about the future scrap copper recovery rate under the influence of the epidemic. It is expected that the scrap copper supply will not be sustainable after a short-term rapid outflow, crude copper as an intermediate regulator still has demand support, and the upstream space for processing fees is limited. 3. The logistics situation of crude copper producing areas such as Zambia and Congo improved in June, and the early backlog of inventory was issued, so crude copper was concentrated in Hong Kong in July, which is also an important factor in the rise of crude copper processing fees. However, with the end of this round of concentration in Hong Kong, the future supply of crude copper is expected to be less affected by the shortage of copper raw materials.

As for copper mines, due to the relatively high disruption in some large mines, especially in Peru, in the second quarter of this year, although the current operating rate has basically returned to normal, it is difficult to recover some of the losses. for example, if Chile can maintain normal copper production in the second half of the year, it is expected that the domestic copper raw materials will maintain a tight balance under lower inventories, but if the current copper supply risks in Chile do occur, Then the shortage of copper raw material supply may intensify.

![Buyer Warrant Demand Increased in Early Trading, Active Market Inquiries [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/KTLHT20251217171714.jpeg)

![BC Copper Closed Sharply Higher by 1.6%, Easing Geopolitical Tensions Boosted Copper Prices [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/EFLYr20251217171714.jpeg)