Summary of basic Metal production in China in February 2019

Electrolytic copper

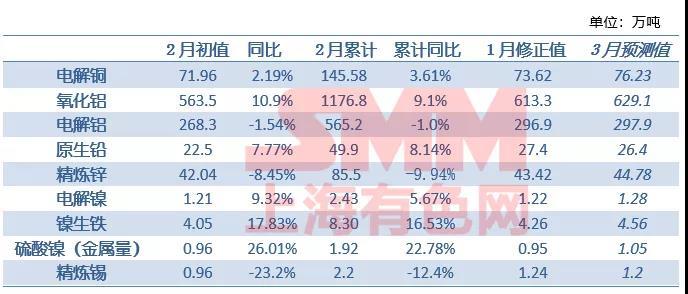

In February 2019, SMM's electrolytic copper production in China was 719600 tons, a decrease of 2.25% from the previous month, an increase of 2.19% over the same period last year. The reduction in production in February was mainly due to the reduction in the number of days of production.

In February, only Yuguang gold and lead was slightly affected by local environmental pressure, and the remaining refineries were not overhauled. In March, Jinchuan Fangcheng Port will begin maintenance, but the impact on the month's output will be limited, China's overall production will pick up 6% from the previous month. According to SMM research, the current sulfuric acid price is good, which makes up for the pressure brought by the decline of some copper concentrate TC, but most smelters say that the recovery rhythm of downstream after the festival is weaker than in previous years, and there is a backlog of electrolytic copper stocks in the plant. In addition, the recycled copper smelter did not increase the proportion of scrap copper because of the widening of the price difference of refined scrap after the festival, mainly considering the stability of the source of scrap copper and the risk of environmental protection.

According to the March production schedule, SMM expects China's electrolytic copper production to be 762300 tons in March, up 5.93 percent from the previous month and 6.85 percent from the same period last year. In the first three months, the cumulative output was 2.2181 million tons, an increase of 4.7 per cent over the same period last year.

Alumina

In February (28 days), China's alumina (metallurgical grade) output was 5.635 million tons, an increase of 10.93 percent over the same period last year, with an average daily output of 201000 tons, an increase of 3000 tons over the previous month, and an annualized operating capacity of 73.4563 million tons.

In February, the domestic alumina production capacity changes: 1) the maintenance of alumina plants in Guangxi ended in January; 2) the operation rate of alumina plants in Guizhou, which had been subject to ore supply problems, was gradually recovering. 3) during the Spring Festival, the opening rate of some alumina plants in Henan Province, which had been restricted before, increased; 4) the alumina plant in Shanxi area overproduced, and Zhaofeng stopped production during the Spring Festival due to ore supply problems, and then resumed, Xinghua suspended a 350000 ton production line due to ore supply problems.

It is estimated that in March (31 days), China's alumina production will be 6.291 million tons, an increase of 9.83 percent over the same period last year, with a daily average of 203000 tons, an increase of 2000 tons over the previous month. The increase in daily average output will mainly come from three aspects. First, Shanxi has completed the re-release of production capacity beyond the bottom emission limit; second, the Boxie Nanchuan Shuijiang project and Shandong Qixing (innovative trusteeship) have contributed to the resumption of production; third, the heating season ends on March 15, and environmental restrictions on production may be relaxed.

Electrolytic aluminum

In February (28 days), the national electrolytic aluminum output was 2.683 million tons, down 1.54 percent from the same period last year. By the end of February, the domestic electrolytic aluminum operation capacity was 35.9 million tons, about 130000 tons less than the same period last year. From January to February, including Shaanxi County Hengkang, Shandong Huayu, Shanxi Huasheng, Shanxi Huazawa, Jiaozuo Wanfang, Tongshun Aluminum and other electrolytic aluminum enterprises, as well as the comprehensive impact of the same period, Inner Mongolia Chuangyuan, Inner Mongolia Guyang and other new production capacity, The actual operating capacity scale remains low. After March, SMM research shows that the increment of electrolytic aluminum supply is still dominated by the unfinished production in 2018, including Inner Mongolia, Guangxi, Yunnan and other parts of the new and replacement capacity continues to be put in. As well as some of the production capacity in Shandong is about to return to production, the actual output is expected to be 2.979 million tons, down 1.6 per cent from the same period last year.

SMM expects domestic electrolytic aluminum production capacity to be 36.05 million tons by the end of March, about 350000 tons less than in the same period in March 2018.

Primary lead

In February 2019, China's primary lead production was 225000 tons, down 17.8 percent from the previous month and 7.9 percent higher than the same period last year.

According to SMM research, February coincides with the Chinese traditional Spring Festival, during which large primary lead smelting enterprises are on duty and maintain normal production, but because February is only 28 days, the output is also limited. Such as Hunan, Yunnan, Henan and other small and medium-sized smelting is generally closed for holiday. In addition, Hunan Yuteng, Yinxing, Henan Qinling, Yunnan Revitalization and so on entered the maintenance, so dragged down the month's primary lead production. In addition, the output increased in February 2019 compared with the same period last year, mainly due to blizzard weather in February 2018, power restrictions in Jiangxi, Hunan and other areas, local smelting enterprises stopped production for some reason, and this year the smelting enterprises are producing as usual.

Looking forward to March, the Spring Festival influencing factors will be lifted, the original lead small and medium-sized enterprises will resume work, coupled with the increase of normal working days in March, the output plan of primary lead smelting enterprises will generally increase. At the same time, such as Hunan Yuteng, Yinxing, Yunnan Revitalization and other smelting enterprises have been overhauled, so SMM expects the production of primary lead to increase to 264000 tons in March.

Refined zinc

In February 2019, SMM China produced 420400 tons of refined zinc, down 3.19 per cent from a month earlier and 8.45 per cent from a year earlier.

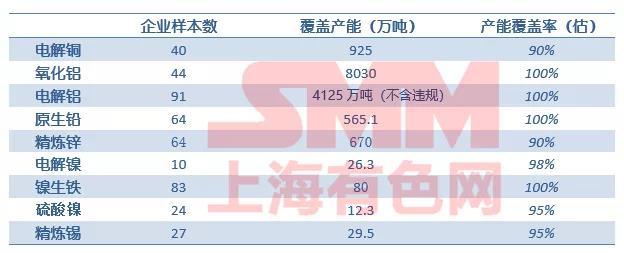

SMM adjusted the research sample production capacity to 6.085 million tons, the overall capacity reduced by 100000 tons, of which Zhuzhou smelting Group reduced 250000 tons of old plant dismantling and shutdown capacity, increased Wenshan zinc indium and four ring zinc germanium production capacity of 150000 tons to the sample.

In February, on the occasion of the domestic Spring Festival, although most of the major domestic smelters did not have a holiday, some small and medium-sized enterprises had a holiday to stop production, and some enterprises in western Hunan had a holiday for up to one month. At the same time, the number of production days decreased in February, and the actual output of many enterprises decreased due to the number of days. Although the production in the south of Hechi resumed, it still did not offset the reduction and shutdown brought about by the Spring Festival and maintenance.

In March, due to the abundant supply of domestic zinc concentrate, the short-term demand of refineries has not increased significantly, the processing fee has further risen to an all-time high, and the profits of refineries are considerable, stimulating the start of production. Although Sihuan zinc germanium and Liuzhou Huaxi maintenance reduced production, but Xiangxi area after the festival production began to resume, at the same time, the overall production days recovered, most refineries increased their own output, the output recorded a significant increase.

According to the March refinery production schedule, domestic refined zinc production is expected to increase by 27400 tons to 447800 tons in March from February, an increase of 0.42 per cent from a year earlier and 6.52 per cent from a month earlier.

Electrolytic nickel

In February 2019, the national natural monthly output of electrolytic nickel was 12100 tons, an increase of 9.32 per cent over the same period last year.

The national electrolytic nickel production in February was 0.82% lower than that in January, mainly due to the lack of natural days in February, which affected some of the output. Since February, Jilin Gene monthly production has stabilized at 500 tons, while Guangxi Silver billion in February has not been producing electrolytic nickel, the two increase or decrease offset.

According to a preliminary SMM survey, electrolytic nickel production increased by about 6 per cent in March from February to 12800 tons, mainly due to an increase in natural days.

Nickel pig iron

In February, the national nickel pig iron fell 4.89 per cent from a month earlier to 40500 nickel tons, an increase of 17.83 per cent over the same period last year. In terms of taste, the production of high nickel pig iron decreased by 4.89 per cent to 37200 nickel tons in February compared with January. The reduction in production days in February led to a month-on-month decline in high nickel pig iron production, but the gradual increase in production capacity at large nickel pig iron plants in Shandong made up for some of the reduction. Low-nickel pig iron production fell 1 per cent in February from a month earlier to 3300 nickel tons.

In March, the national production of nickel pig iron is expected to increase by 12.62% to 45600 nickel tons, and the output of high nickel pig iron is expected to increase by 10.78% to 41200 nickel tons. Due to the increase in the number of days of production in March, and the output released by the new production capacity of the Shandong plant continues to increase. The output of low nickel pig iron increased to 4400 nickel tons compared with February.

Nickel sulfate

In February, China produced 9647 tons of nickel sulfate and 43900 tons in kind. Production increased by 1.50% in February compared with the previous month. Although February was affected by production days and plant holidays, some nickel sulfate plants increased their nickel sulfate production capacity at the end of last year and after the year, including Jinchuan, Greenmei and capacity hundred lithium power and other enterprises. As a result, the national nickel sulfate production increased rather than decreased in February. The supply of nickel sulfate has increased, but the downstream ternary precursor plants have also increased production and actively purchased raw materials, resulting in a shortage of nickel sulfate in the market. The national nickel sulfate production may continue to increase in March, up 8.44% from the previous month, mainly due to the resumption of normal production after the factory festival in March and the continued climbing of new production capacity.