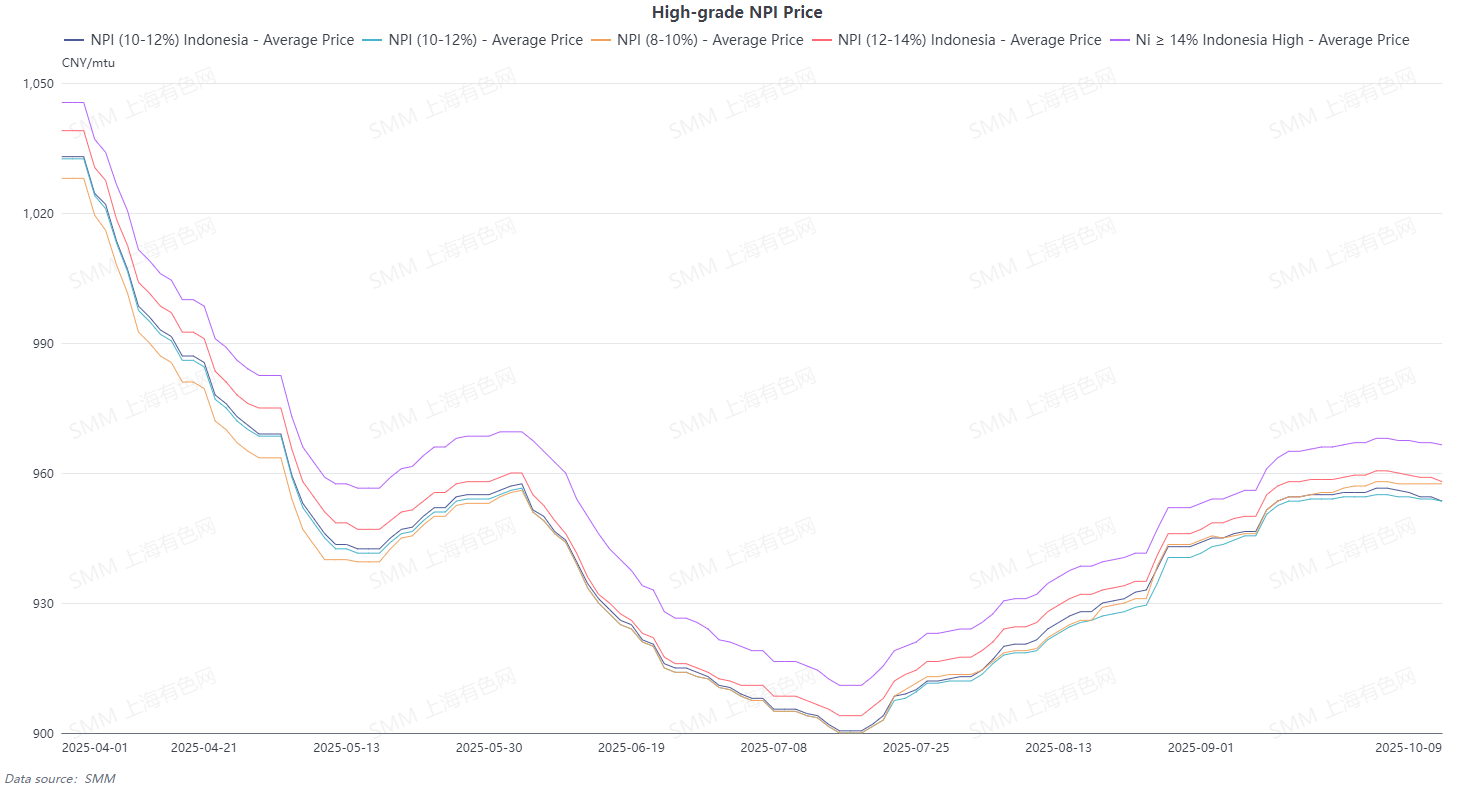

After the National Day holiday, as of October 9, 2025, the average price of SMM 10-12% high-grade NPI (ex-factory, tax included) fell by 0.5 Yuan/nickel unit MoM to 953.5 Yuan/nickel unit, while the average price of SMM 10-12% high-grade NPI (CIF, tax included) dropped by 1 Yuan/nickel unit MoM to 953.5 Yuan/nickel unit. Post-holiday, high-grade NPI prices continued their decline. What changes occurred in the market during the holiday, and how are future market expectations shaping up? The detailed analysis is as follows:

According to SMM prices, high-grade NPI prices have struggled to rise since mid-September. Approaching the National Day holiday, market transactions gradually became sluggish, market activity continued to decrease, most enterprises held a strong wait-and-see sentiment towards the future market, and high-grade NPI prices had already shown a downward trend.

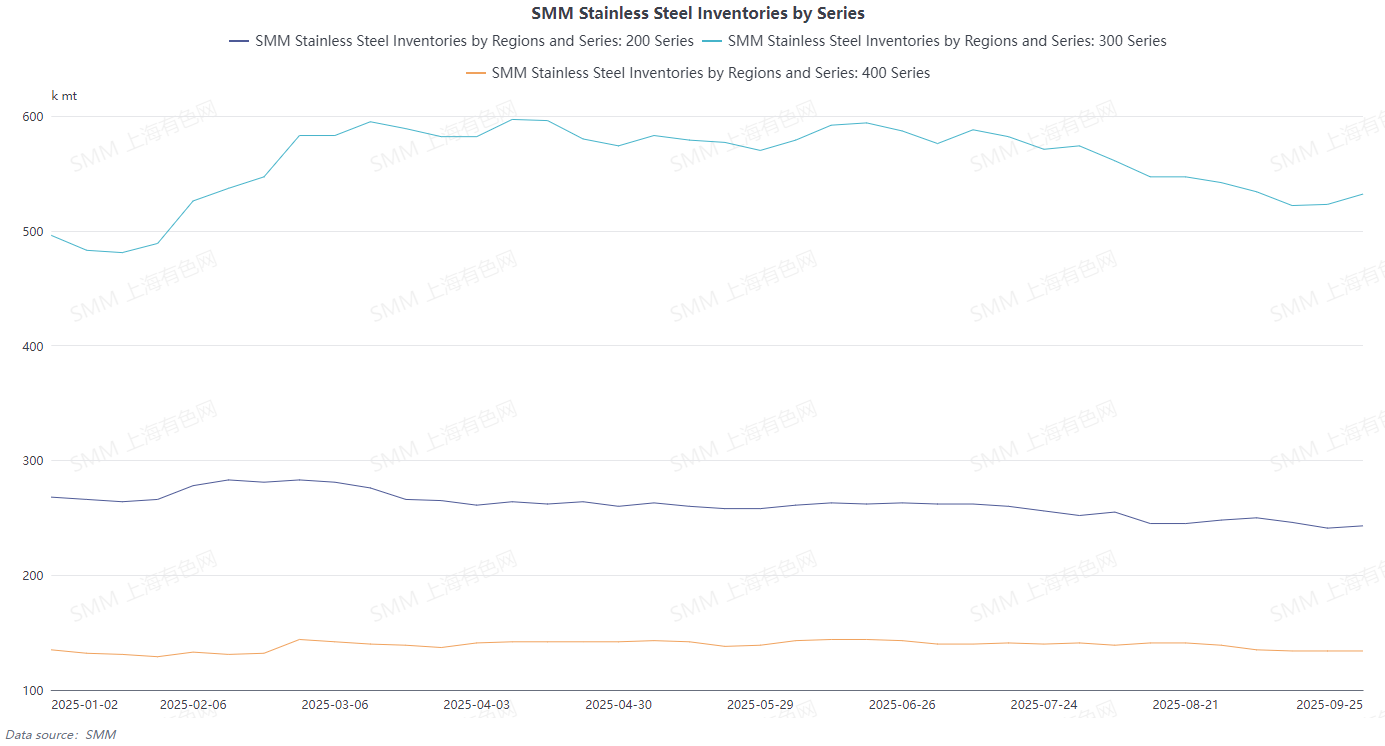

During the National Day holiday, mainstream enterprises did not engage in large-scale spot order procurement. With stainless steel selling prices struggling to increase, NPI, as a key raw material, faced cost pressure from stainless steel, making continued price rises unlikely. Simultaneously, stainless steel inventory destocking ended, reinforcing the wait-and-see sentiment among enterprises. The market is awaiting October's consumption and price performance to provide direction for high-grade NPI prices.

Looking ahead, most enterprises currently maintain a wait-and-see sentiment. Breaking it down by sector, upstream smelters still exhibit reluctance to budge on prices, but influenced by market pessimism, their quoted price center has already declined. Downstream steel mills maintain sufficient raw material inventory. Given the current difficulty in raising finished product prices and high costs, most steel mills kept their high-grade NPI offers flat MoM. Most traders hold bearish expectations for the future market, having already exported their limited inventory before the holiday. Furthermore, transaction prices from some traders have seen significant declines, contributing to a softening market sentiment.

Overall, surplus supply and stainless steel costs are suppressing high-grade NPI prices. Concurrently, the traditional peak season effect is weakening, reducing support for high-grade NPI prices, making continued price increases unlikely within the month. However, from a cost perspective, Indonesian nickel ore prices have risen, and the market holds expectations for tight ore supply. Additionally, auxiliary material prices remain high, keeping high-grade NPI production costs firm. Most domestic smelters are still operating at losses, and profits for Indonesian smelters have also declined somewhat. SMM expects high-grade NPI prices to hover at highs in October, with relatively limited downside room. The price for SMM 10-12% Indonesian high-grade NPI (CIF, tax included) is forecasted to fluctuate between 940-960 Yuan/nickel unit.

![[SMM Nickel Midday Commentary] On March 26, influenced by expectations surrounding the policy of “Indonesia's proposed levy of a nickel export tax,” nickel prices rose significantly](https://imgqn.smm.cn/usercenter/CjEnN20251217171733.jpg)