On Tuesday, US President Trump mentioned during a press conference with South Korean President Lee Jae-myung that if China were to halt the export of rare earth magnets again, "countermeasures such as imposing 200% tariffs would be taken." However, he acknowledged that such high tariffs would signify a breakdown in bilateral trade. Subsequently, China's Foreign Ministry responded, stating that China consistently handles and advances China-US relations based on the principles of mutual respect, peaceful coexistence, and win-win cooperation, while firmly safeguarding its own sovereignty, security, and development interests.It expressed hope that the US would reciprocate and jointly promote stable, healthy, and sustainable development of bilateral relations.

Two months ago, US President Trump unexpectedly announced during a White House event the signing of a trade agreement with China, causing global market turbulence. The White House later clarified that this was not an entirely new agreement but a supplementary understanding to the framework negotiated in Geneva in May.

Almost simultaneously, a spokesperson for China's Ministry of Commerce confirmed that China would legally review export applications for controlled items that meet the requirements, while the US would lift a series of restrictive measures against China. The supplementary agreement, officially signed on June 24, clearly outlined a strategic "rare earths-for-technology" trade framework.

In the short term, the unpredictable stance of the Trump-led US administration has raised additional concerns about China-US rare earth cooperation. However, in reality, the two sides share broad consensus on rare earths.

01 The Strategic Significance of the China-US Rare Earth Agreement

According to details disclosed by the US Department of Commerce, China will resume exports to the US of seven key medium-heavy rare earth elements, including samarium, gadolinium, terbium, and dysprosium—materials indispensable for military and high-tech industries.

These rare earths are widely used in products ranging from wind turbines to jet aircraft. In exchange, the US pledged to lift export restrictions on ethane, wafer design software, and aircraft engine materials.

The agreement specifically established a reciprocal enforcement mechanism, whereby the withdrawal of US measures would be contingent upon "China's actual delivery of rare earths." This design reflects the lack of mutual trust accumulated during prolonged trade frictions but also demonstrates the political will to resolve disputes through pragmatic means.

02 The Realistic Basis of Interdependence

The US reliance on China's rare earth elements far exceeds expectations. In 2024, over 90% of US rare earth imports depended on China, despite possessing its own rare earth mines, as domestic processing capacity remains severely inadequate.

The US once attempted to establish a rare earth purification plant in Texas, but the project ultimately failed due to costs three times higher than those in China. China holds core technologies in rare earth purification and deep processing, particularly dominating the high-purity rare earth magnet sector.

According to US statistics, from 2020 to 2023, approximately 70% of rare earth metals and compounds imported by the US originated from China. This dependency rendered Trump's threat to impose 200% tariffs on Chinese rare earths a double-edged sword—if the US levied hefty tariffs, the immediate consequences would include soaring production costs for domestic enterprises, higher consumer prices, and worsening inflationary pressures.

03 Rational Perspective on the Balance Between Competition and Cooperation

China's dominance in the rare earth sector was not achieved by chance. As early as the 1980s, the Chinese leadership designated rare earths as a strategic industry, establishing this position through decades of strategic investment, scientific expertise, and unique geological endowments.

China boasts over 100,000 professionals with specialized skills in the rare earth field, along with dozens of university programs dedicated to the sector, producing approximately 2,200-3,000 engineers annually. In contrast, the US has only a few hundred experts and limited academic pathways, lagging far behind China in rare earth talent development.

Industry experts note that China has capitalized on the US's "complete vulnerability" in the rare earth sector. Assessments indicate that rebuilding a comprehensive rare earth supply chain in the US would require 15 years and an investment of $120 billion—double the budget of the CHIPS Act.

04 Future Trends and Collaboration Pathways

Following the signing of the China-US rare earth agreement, the market responded swiftly: US rare earth mining and processing companies saw their stock prices surge by 5%-8%, while Tesla and General Electric rose by 2%-3%. This reflects the market's positive reaction to bilateral cooperation.

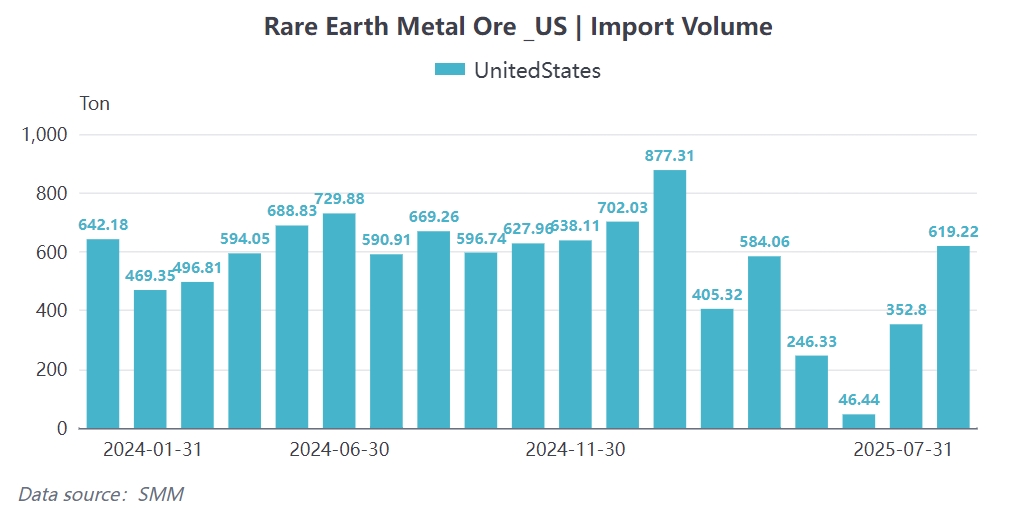

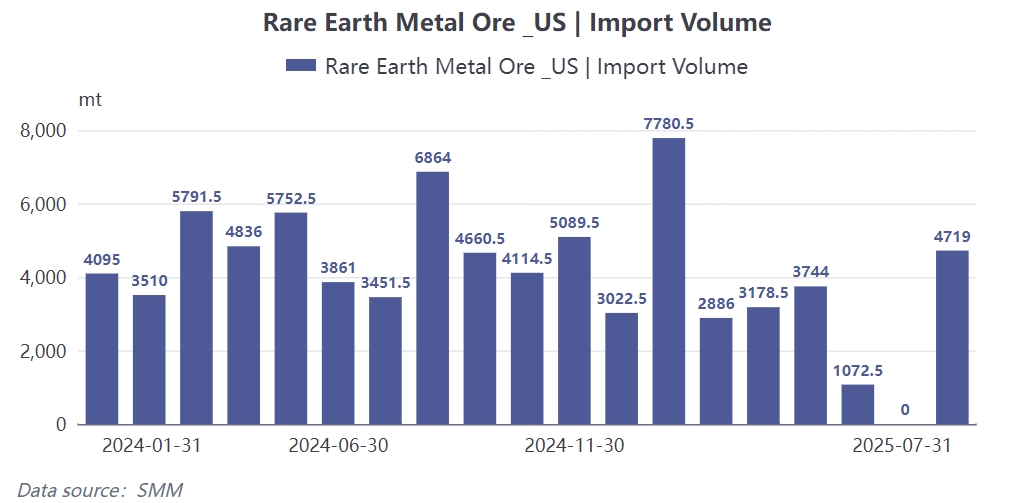

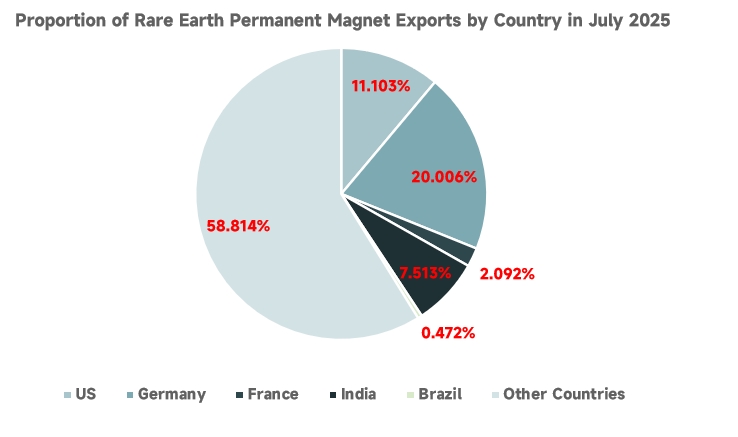

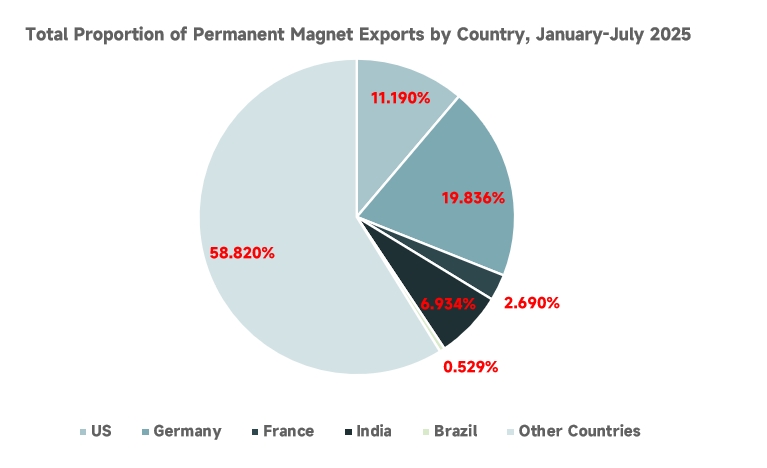

Customs data shows that China's magnetic material exports to the US in July 2025 reached 619.22 mt, up 72.51% MoM, accounting for 11.1% of total exports that month. From January to July, exports to the US totaled 3,121.832 mt, representing 11.19% of total exports. These figures indicate a gradual normalization of trade relations.

US-based MP Materials reported Q2 2025 revenue of $57.393 million, an 84% YoY increase. This growth was driven by two key factors: higher sales revenue from high-value-added neodymium-praseodymium (NdPr) oxide and metal products, and the first large-scale sales of new magnetic material precursors.

However, the US rare earth supply chain remains dependent on China. Even the rare earth concentrate mined by MP Materials must be shipped to its Chinese shareholder, Shenghe Resources, for processing. This interdependence is unlikely to change in the short term.

The China-US rare earth interdependence extends far beyond a simple buyer-seller relationship. Behind MP Materials' 84% YoY revenue growth in Q2 2025 lies the processing technology support from its Chinese shareholder, Shenghe Resources. The US Department of Defense can subsidize domestic rare earth companies at twice the market price precisely because China maintains the stability of the global supply chain.

Rare earth should not be a weapon in trade wars, but rather a bridge for cooperation between the two major economies. This is not only a practical necessity, but also an inevitable choice for the division of labor and development in the global industry chain.