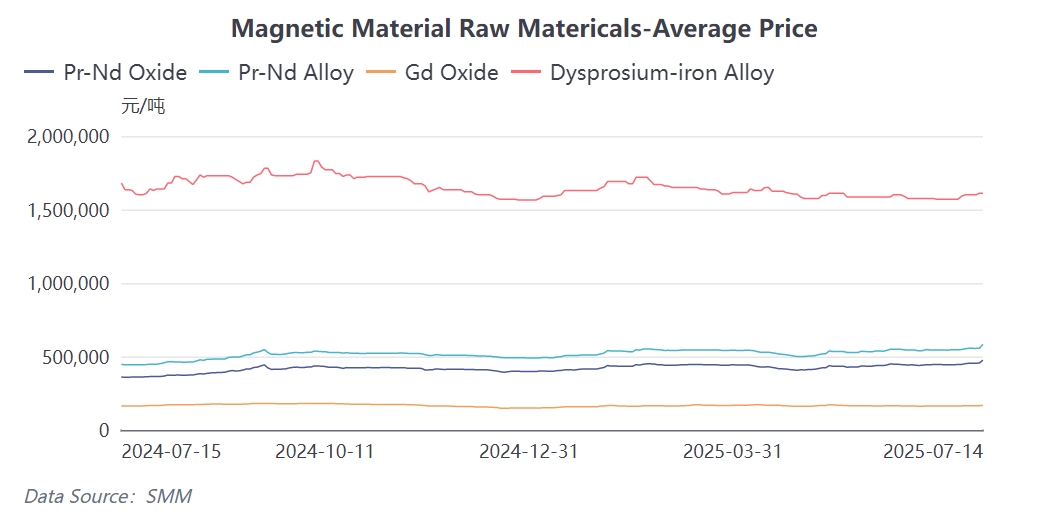

SMM News: Today, rare earth market prices have risen significantly. Specifically, in the oxide market, the price of Pr-Nd oxide has increased to 474,000-476,000 yuan/mt, and the price of gadolinium oxide has risen to 165,000-170,000 yuan/mt. In the metal market, the price of Pr-Nd alloy has increased to 580,000-586,000 yuan/mt, and the price of dysprosium-iron alloy has risen to 1.6-1.62 million yuan/mt. Under these circumstances, how have downstream magnetic material enterprises, which are facing export controls and rising raw material prices, responded to this price increase?

First, let's examine the reasons behind the current round of raw material price increases:

The current round of raw material price increases is primarily influenced by sentiment:

1. Continuous price hikes for upstream concentrates: China Northern Rare Earth and Bao Gang United Steel have raised concentrate prices for four consecutive quarters. In Q3 2025, the price excluding tax reached 19,109 yuan/mt, up 1.5% MoM. The rising cost of concentrates has laid the sentiment foundation for the price increases.

2. US policies fuel sentiment: The US Department of Defense injected $400 million into MP Materials and signed a ten-year price guarantee agreement, ensuring that the price of neodymium-praseodymium mixed rare earths would not fall below $110/kg (equivalent to 770,000 yuan/mt domestically), a 70% premium over the domestic price of 450,000 yuan/mt at that time. This move directly stimulated suppliers' reluctance to sell, triggering strong market expectations that "overseas pricing would force domestic price increases."

Next, let's examine the different responses from magnetic material enterprises amid this round of price increases:

Supported by the cost of oxide prices, the metal quotation reached 580,000-586,000 yuan/mt on July 14, with a single-day increase of up to 26,000 yuan. This increase is relatively rare in the recent market, reflecting not only the cost pressure transmitted downstream due to the rise in raw material prices, but also the market's strong expectations for the short-term trend of rare earth metals. From the price range perspective, the quotation of 580,000-586,000 yuan/mt has already reached a relatively high level, creating a significant gap from previous prices and posing considerable challenges for magnetic material enterprises in cost control.

Faced with such significant price fluctuations, magnetic material factories, based on their own scales, order structures, inventory conditions, and other factors, have provided differentiated responses, which can be broadly categorized into the following types:

The first is the steady response of top-tier magnetic material enterprises. These enterprises, leveraging their long-term accumulated industry advantages, demonstrate strong risk-resistance capabilities. From the orders perspective, they hold a large number of top-tier orders, and with export licenses being gradually opened, this provides a solid foundation for their stable production. In terms of capacity, top-tier enterprises have significant capacity advantages, enabling them to further secure domestic orders and ensure production continuity. As raw materials are essential for daily production, a good order volume and reasonable inventory levels mean that they do not need to make special adjustments due to the current round of metal price increases. Instead, they maintain a normal production, order-taking, and delivery rhythm, adopting a wait-and-see attitude to await the pullback of this round of prices. This response strategy not only reflects the strength of top-tier enterprises but also their judgment on market trends, namely that the current price increases lack long-term support and there is no need for excessive panic.

Secondly, some magnetic material enterprises passively take orders. Due to time constraints in production planning, some end-users have urgent order requirements. To complete production tasks on time, they have to accept the relatively high raw material prices at present. This demand pressure is transmitted upwards to magnetic material enterprises, making them willing to take orders for production despite rising costs. The decisions of such magnetic material enterprises are more based on short-term order demands. To maintain cooperative relationships with end-users, they have to bear higher raw material costs. However, this order-taking mode may have a certain impact on the enterprises' short-term profits, but its purpose is to ensure production continuity and stabilize customer resources.

The third factor is the pricing suspension strategy adopted by some enterprises. Similar to upstream metal manufacturers, some enterprises have chosen to suspend their pricing. It is worth noting that the core reason for this pricing suspension is not simply the rise in raw material prices, but rather the excessive and rapid increase in raw material prices. From the perspective of stable production, magnetic material manufacturers and end-users are concerned that volatile prices will disrupt production plans and increase the difficulty of cost control. Therefore, they have chosen to suspend pricing temporarily, hoping to conduct transactions after metal prices stabilize. This strategy is a self-protection measure for enterprises to cope with severe market fluctuations, helping to avoid operational risks caused by price uncertainty.

Finally, let's look at the future trend.

After SMM analysts communicated with major magnetic material factories immediately following the price increase, they found that almost all magnetic material enterprises believed that the current metal market prices were difficult to accept in the end-use market. From the perspective of market laws, sustained price increases require actual demand support, but currently, the end-use market has low acceptance for high-priced raw materials, indicating a lack of sustained momentum for this round of price increases.

It is anticipated that the subsequent rare earth market will enter a stalemate of back-and-forth negotiations between upstream and downstream enterprises. Both sides will engage in a battle over prices, seeing which side will compromise first. Upstream enterprises, due to previous cost increases and their pursuit of profits, hope to maintain high prices to safeguard their own interests. However, downstream enterprises, constrained by cost pressures, find it difficult to accept high-priced raw materials. If they are forced to accept them, it may lead to a decline in product competitiveness or a severe squeeze on profit margins.

The resolution of this stalemate may depend on various factors. From the perspective of market demand, if downstream demand remains sluggish and the purchase willingness of end-users further declines, upstream enterprises may have to appropriately reduce prices to facilitate transactions. Conversely, if there is an unexpected increase in demand, leading to an increase in the demand for raw materials by end-users, they may accept price increases to a certain extent, thereby pushing downstream enterprises to exert pressure on magnetic material enterprises, which in turn may compromise with upstream enterprises. From a policy perspective, adjustments to relevant policies may impact market supply and demand and prices. For example, national regulatory policies and export policies for the rare earth industry may alter the current market landscape. From the perspective of international market dynamics, relevant measures taken by countries such as the US in the rare earth sector may also continue to affect market sentiment and price trends. If there are new changes in their policies, it may disrupt the balance of competition between upstream and downstream enterprises in China.

Against the backdrop of fluctuating raw material prices, the rare earth magnetic material market is undergoing a complex adjustment process. Enterprises need to closely monitor market dynamics and flexibly adjust their business strategies to cope with market uncertainties and strive for survival and development in the fiercely competitive market. For upstream enterprises, it is necessary to pay attention to changes in downstream demand and policy orientation, and reasonably adjust pricing strategies. For downstream magnetic material enterprises and end-users, it is crucial to optimize inventory management and enhance cost control capabilities to cope with the impact of fluctuations in raw material prices.