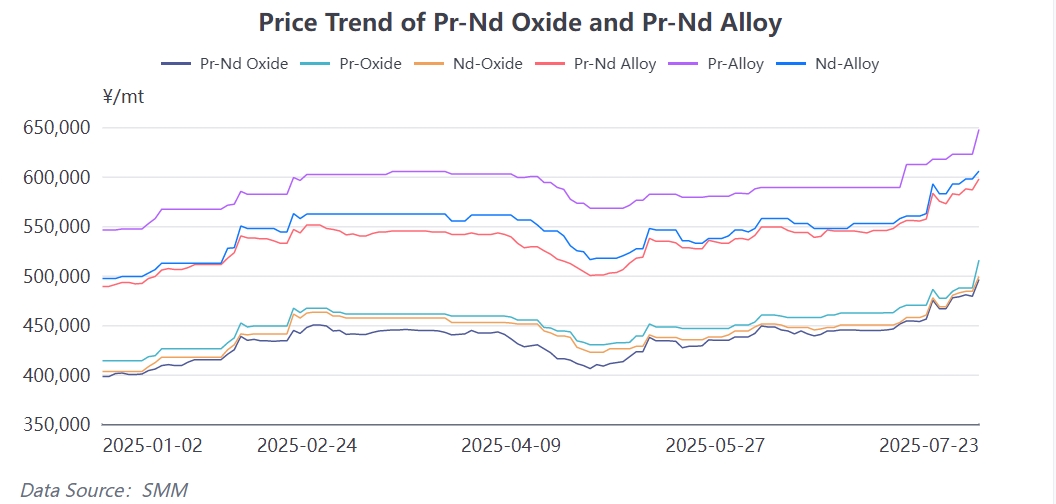

SMM reported that the rare earth oxide market continued its upward trend on July 23. Mainstream quotations for Pr-Nd oxide ranged from 495,000 to 497,000 yuan/mt, with an average price of 496,000 yuan/mt, up 17,000 yuan/mt MoM. Quotations for Pr oxide ranged from 513,000 to 518,000 yuan/mt, with an average price of 515,500 yuan/mt, up 28,000 yuan/mt MoM. Quotations for Nd oxide ranged from 498,000 to 500,000 yuan/mt, with an average price of 499,000 yuan/mt, up 15,000 yuan/mt MoM. Notably, as of the time of reporting, the spot cargo transaction price for some Pr-Nd oxide separation plants had reached 502,000 yuan/mt, which translates to a metal cost of approximately 620,000 yuan/mt.

Cost supports metal prices, Market participation heating up

The continuous rise in raw material prices has provided solid support for downstream metal plants to raise their quotations. According to SMM data, the mainstream quotations for Pr-Nd alloy on that day were 595,000-600,000 yuan/mt, with an average price of 597,500 yuan/mt, showing a daily increase of 11,000 yuan/mt. The quotations for Pr metal were 645,000-650,000 yuan/mt, with an average price of 647,500 yuan/mt, showing a daily increase of 25,000 yuan/mt; The quotations for Nd metal were 603,000-608,000 yuan/mt, with an average price of 605,500 yuan/mt, showing a daily increase of 8,000 yuan/mt.

After the pricing process was finalized, transactions followed swiftly. Pr-Nd oxide producers actively raised their quotes, and metal producers, driven by profits, followed suit. Against this backdrop, NdFeB magnetic material enterprises and high-performance permanent magnet motor enterprises, which are in the midstream of the industry chain, are under cost pressure. Their procurement strategies and the price acceptance of end-users have become the core concerns of the market. This article aims to explore the deep-seated drivers of this round of price increases and their potential subsequent impacts.

Analysis of Price Increase Factors:

Coexistence of Expected Supply Tightening and Rigid Demand Supply-Side Expectations Dominate:

- US rare earth ore imports have dropped to zero (resulting in a monthly reduction of over 300 mt of Pr-Nd oxide supply).

- The Kachin region has announced a ban on rare earth mining by the end of 2025 (estimated to reduce monthly Pr-Nd oxide supply by approximately 500 mt).

- The combination of these events has triggered strong market expectations of a tightening future supply of rare earth Pr-Nd.

Demand-Side Support is Solid:

SMM's survey of major end-use application fields indicates that current demand exhibits rigid characteristics:

Robust Exports: According to June customs data, China's exports of rare earth permanent magnets reached 3,187.76 mt, showing a significant MoM increase of 157%. The industry generally expects July exports to exceed 4,000 mt, continuing the growth momentum.

Inverter Air Conditioners: Driven by the concentrated installation of air conditioners in universities during the summer vacation and high-temperature weather in the north, production demand for air conditioners remains robust in July and August.

Consumer Electronics: Boosted by the summer consumption season and the stockpiling period for the start of the school year in September, total demand is expected to continue growing.

Industrial Robots: The overall development of the industry in 2025 is stable, with new demand for humanoid robots in fields such as education and healthcare providing sustained momentum for the industry.

Industry Focus: New Energy Terminals - Limited Price Variability?

Despite the view that enterprises in the new energy drive motor sector, the largest application area for high-performance NdFeB, may become a key variable in curbing the continued rise in Pr-Nd alloy prices, the SMM survey indicates that their ability to intervene in prices is actually limited:

Cost Structure: The cost of drive motors accounts for a relatively low proportion of the total cost of new energy vehicles, with the cost of magnetic materials (Pr-Nd alloy) being even lower. This results in relatively low sensitivity of OEMs to upstream price fluctuations.

Production Rigidity: OEMs typically do not halt production easily solely due to high prices of magnetic material raw materials, as the stability of the supply chain takes precedence.

Long-Term Agreement Mechanism for Price Locking: Mainstream OEMs usually leverage their scale advantages to sign long-term agreements (LTAs) with magnetic material suppliers or adopt floating pricing formulas to lock in certain price ranges or transfer risks in advance, effectively insulating themselves from short-term fluctuations in raw material prices.

Conclusion: In the short term, although new energy end-users express dissatisfaction with price increases, they generally lack the motivation to significantly cut or halt production due to raw material cost factors.

Micro Dynamics in the Metal Market: Headline Bidding Sparks Market Sentiment

It is noteworthy that a leading metal enterprise has recently conducted consecutive bidding sales activities for Pr-Nd alloy. The bidding alarm price (highest price) has rapidly increased from the initial 572,000 yuan/mt to the current 579,500 yuan/mt, and all transactions except for the first day have been concluded quickly at the starting bid price, significantly shortening the overall transaction duration. This bidding model, which offers a certain "price trough" compared to the spot market, has attracted active participation from numerous magnetic material enterprises. The high transaction prices and enthusiastic participation have further strengthened the market's bullish sentiment, objectively boosting the overall metal quotes for the day.

Midstream Magnetic Material Enterprises: Survival Strategies in a Tight Spot

As the core link connecting upstream and downstream, magnetic material enterprises are currently facing dual pressures: the rising cost of upstream raw materials and the cost pressure on downstream signed orders (especially for locked-price customers). Against the backdrop of intensifying competition in the domestic magnetic material industry, balancing order acquisition with profit protection has become an urgent challenge for every enterprise.

At this stage, actively tracking real-time market conditions, enhancing information acquisition and response efficiency, strengthening communication with upstream and downstream partners, and flexibly employing procurement and pricing strategies (such as appropriately increasing safety inventory, seeking better procurement channels, and negotiating cost-sharing mechanisms with customers) are more realistic choices.

Conclusion: This round of rare earth price increases is primarily driven by expectations of a tightening supply side, and has been reinforced by the micro-behavior of the metal market. Currently, the rigid demand in end-use sectors (especially exports, air conditioning, and consumer electronics) provides fundamental support for prices. Notably, the price transmission mechanism and production rigidity in the largest end-use application sector—new energy-driven electric motors—make it difficult to substantially curb the rise in raw material prices in the short term. Magnetic material enterprises in the midstream of the industry are operating in a complex bargaining environment, and leveraging information advantages and pricing strategies is crucial for their survival. In the future, close attention should be paid to whether top-tier enterprises implement production cut plans, the implementation of policies in major ore-producing regions, and changes in the intensity of end-use demand. These factors will determine the sustainability of this round of rare earth market trends.