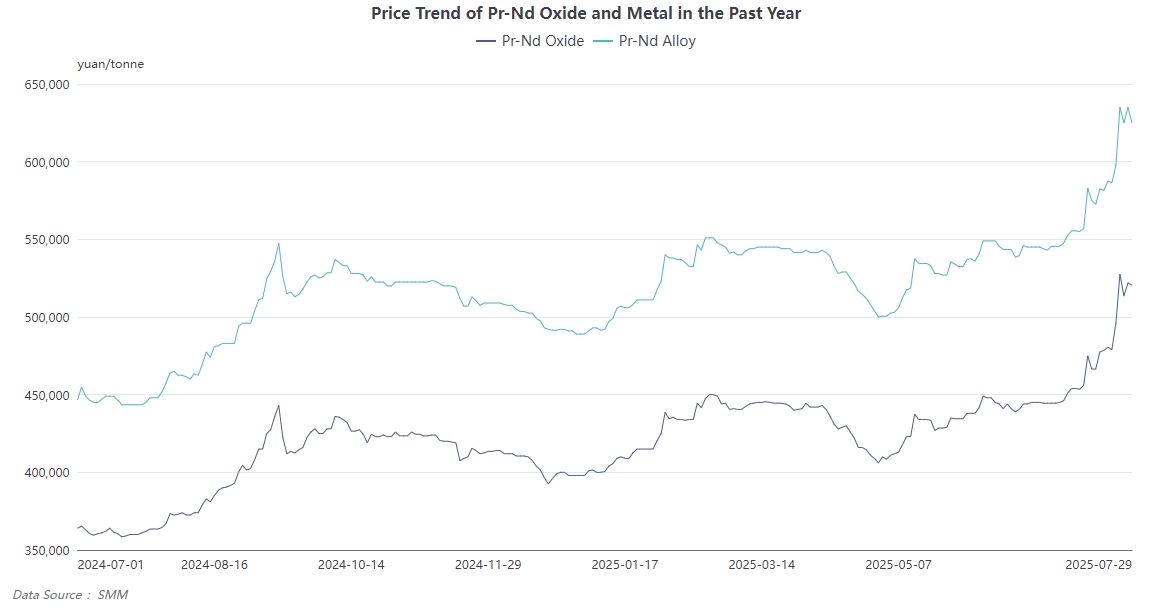

In July, the price trend of Pr-Nd alloy continued to rise, increasing from an average price of 545,000 on July 3rd to 635,000 on July 28th, with a monthly increase exceeding 16%, marking the highest year-on-year increase since 2011.

The previous article provided a detailed explanation of the price support from the fundamental factors, namely supply and demand. In this article, we will only offer a brief review:

Tightening of the supply side: ① US ore imports dropped to zero (a monthly reduction of 300+ mt of Pr-Nd oxide); ② Kachin State in Myanmar announced a ban on rare earth mining by the end of 2025 (potentially reducing monthly output by 500 mt). Although there are still uncertainties regarding the policy, the market has reacted based on the premise of a ban, triggering rumors of production cuts by a top-tier enterprise.

Increasing demand: After the clarification of export controls on magnetic materials, enterprises concentrated on securing overseas orders for September-October in July (with exports expected to increase to 4,000 mt). Coupled with the stockpiling period during the September-October peak season, the production of magnetic materials increased by 8% MoM.

Strong price signals: Within a week, rare earth metals from top-tier enterprises were "sold out instantly" twice at auction, with the transaction price jumping from 572,000 yuan/mt to 579,500 yuan/mt, objectively boosting the spot price to 620,000 yuan/mt.

Terminal support: The clear increase in new energy vehicle production, the drive for air conditioning production due to high temperatures, stockpiling for consumer electronics, and the injection of new demand from robots have all strengthened the resilience of demand.

Admittedly, the fundamental factors have provided rigid support for the current price increase. However, the influence of sentiment, in addition to the tightening supply and improving demand, has also played a significant role and has even become a key factor supporting rare earth prices at many times. So, what does sentiment mean in the rare earth industry? And what is the core logic behind it? In this article, we will discuss these questions together.

I. What exactly does "market sentiment" in the rare earth market refer to?

Market sentiment is essentially the irrational decision-making resonance of participants in response to the information flow, which in the rare earth sector is concentratedly manifested as the "news leverage effect" — that is, leveraging fragmented information to amplify expectations of future supply-demand imbalances. Taking the example of Pr-Nd alloy prices surging to 580,000 yuan/mt in early July:

Apparent triggers: The positive performance of China Northern Rare Earth's semi-annual report, with a projected net profit increase of 1,883%-2,015%, coupled with the US Department of Defense's investment of $400 million in MP Materials and setting a price floor of $110/kg (equivalent to 770,000 yuan/mt, an 80% premium over the domestic price at that time);

Actual contradictions: MP's Phase II capacity will not come online until 2028, and its short-term impact on China's supply is negligible, yet the market still seized the opportunity to push up prices — the core lies in sentiment amplifying long-term anxieties about the "scarcity of strategic resources."

The underlying logic of this "sentiment-based pricing" stems from the unique "triple strategic attributes" of rare earths:

Resource control: China ranks first globally in heavy rare earth reserves, versus the US's military and new energy industries' reliance on China;

Technological bottleneck: Overseas smelting costs are 40% higher than those in China, versus China's control of 90% of the global rare earth refining capacity;

Military applications: China holds the resources for heavy rare earth mining and smelting, versus the US's lack of relevant technical talent.

II. International Relations and Strategic Anxieties Hidden Behind Market Sentiment

The root cause of the sensitivity of rare earth market sentiment lies in its role as a "strategic counter" in the US-China tech race:

The Double-Edged Sword Effect of Export Controls

After China implemented export controls on seven types of heavy rare earths, including samarium, gadolinium, and terbium, in April, the US rare earth market was in disarray. Subsequently, China gradually refined its export control policies, issuing licenses to some US customers, which drove a 150% MoM increase in magnetic material exports in June. This "dynamic control" is, in fact, a precise bargaining tool: it allows the West to experience the pain of supply disruptions while leaving room for negotiation leverage.

The "Pie-in-the-Sky" Dilemma of Overseas Expansion

Despite the US accelerating the construction of its domestic supply chain (such as MP receiving funding from the Department of Defense), it faces three insurmountable challenges:

Technological Barriers: The US's rare earth concentrate processing capacity and talent pool still need improvement.

Cost Disadvantages: Domestic smelting efficiency is low, and the target price of 770,000 yuan/mt after exceeding 10,000 mt of capacity in 2028 far exceeds China's cost line.

Time Constraints: Building a complete industry chain requires over 10 years and $250 billion in investment.

III. The Spiral of Sentiment and Fundamentals: Intertwined and Mutually Reinforcing

Currently, the sentiment surrounding rare earths has formed a positive feedback loop of "self-fulfilling expectations":

Sentiment Soars Driven by Fundamentals

With the tightening of rare earth fundamentals in Q3 becoming inevitable, traders have seized the opportunity to speculate and drive up prices, leading to a rapid tightening of low-priced supplies in the rare earth spot market and further increases in rare earth raw material prices.

Long-Term Endorsement from Terminal Revolution

The demand for humanoid robots has become a new pillar of sentiment: Each Tesla Optimus robot requires 3.5 kg of high-performance NdFeB. If 890,000 units are shipped globally by 2030, the incremental demand for NdFeB will exceed 3,000 mt (accounting for 23% of current global production) — even though the current technology is not yet mature, capital has already pre-emptively bet on resource hegemony.

Dynamic Game of Policy Expectations

The market closely tracks the progress of China-US negotiations: If the US makes concessions on chip bans, China may release heavy rare earth quotas; conversely, tighter controls may drive up overseas dysprosium oxide prices rapidly.

IV. Conclusion: The Essence of Sentiment Game is the Contest for Rule-Making Power

Compared to base metals such as copper, aluminum, lead, and zinc, rare earths have their own unique characteristics in terms of metal attributes. They lack genuine futures markets but are always influenced by sentiment. Behind these sentiments often lie not just simple expectations for the future but also attitudes towards macro policies and even the gamesmanship between different countries. As a strategic metal, rare earths often represent more than just a metal; they symbolize a country's future development potential and the confidence to wield rule-making power. Through the sentiment surrounding rare earths, we have rediscovered their uniqueness and are better able to perceive the hidden future development trends behind the sentiment.