ด้วยการกระตุ้นจาก “คำสั่งบังคับใช้การเชื่อมต่อกับระบบไฟฟ้า 531” ระยะเวลาการกำหนดอัตราค่าไฟฟ้า 90 วัน และภาวะฉุกเฉินของระบบไฟฟ้าในยุโรป อัตราการดำเนินงานของอุตสาหกรรมจึงเกินมาตรฐานประวัติศาสตร์ แม้ว่าจะมีการแบ่งส่วนอย่างรุนแรงก็ตาม ราคาได้แข็งค่าขึ้นท่ามกลางความตึงเครียดด้านการจัดหาหลังจากการแข่งขัน แต่แรงขับเคลื่อนในทางบวกที่ยั่งยืนยังคงหาได้ยาก

การแบ่งส่วนการผลิตในครึ่งปีแรก:

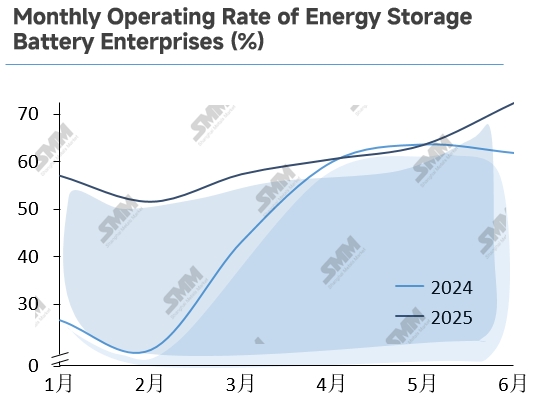

ไตรมาสที่ 1 ปี 2568 ความยืดหยุ่นในช่วงนอกฤดูที่ขัดกับแนวทางปฏิบัติ

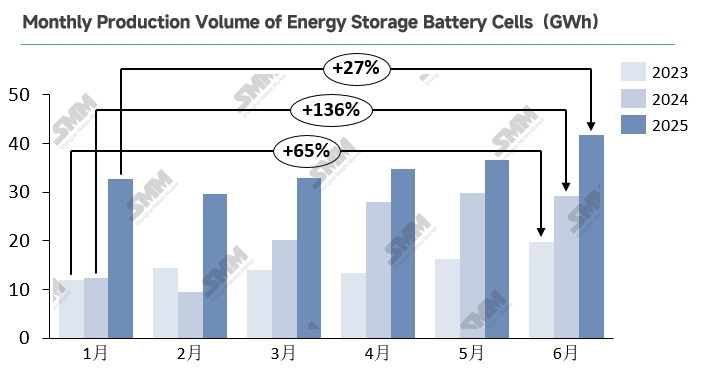

ในไตรมาสที่ 1 ปี 2568 ตลาดการจัดเก็บพลังงานของจีนแสดงให้เห็นถึงความแข็งแกร่งในช่วงนอกฤดูที่ผิดปกติ โดยมีอัตราการดำเนินงานในเดือนมกราคม-กุมภาพันธ์เกินกว่า 50% แม้ว่าในเดือนกุมภาพันธ์จะลดลงเนื่องจากความเหนื่อยล้าจากการเร่งรีบหลังจากเชื่อมต่อกับระบบไฟฟ้าและช่วงเวลาที่เงียบเหงาในช่วงเทศกาลตรุษจีน แต่การยกเลิกการจัดสรรการจัดเก็บพลังงานบังคับตาม เอกสารหมายเลข 136 ได้กระตุ้นให้ผู้พัฒนาเร่งรีบ โครงการต่าง ๆ ได้แข่งขันกันเพื่อล็อกไทม์ไลน์ก่อนที่การคำนวณรายได้ที่ซับซ้อนและความไม่แน่นอนของตลาดการค้าจะมีผลบังคับใช้ ซึ่งก่อให้เกิดการผลิตเซลล์ที่เร่งรีบตั้งแต่เดือนมีนาคมเป็นต้นไป

ไตรมาสที่ 2 ปี 2568 ความผันผวนของความต้องการ: ความผันผวนสามระยะท่ามกลางการเติบโตอย่างต่อเนื่อง

ความต้องการการจัดเก็บพลังงานของจีนแสดงให้เห็นถึงเส้นทางการขึ้นลงของจุดสูงสุด-จุดต่ำสุด-การฟื้นตัวในไตรมาสที่ 2 ตั้งแต่เดือนเมษายนถึงกลางเดือนพฤษภาคม “วันสุดท้ายของการเชื่อมต่อกับระบบไฟฟ้า 531” ได้กระตุ้นให้มีการเปิดใช้งานโครงการอย่างเข้มข้น ซึ่งเร่งการผลิตและการจัดส่งเซลล์ หลังจากวันสุดท้าย (ปลายเดือนพฤษภาคม-เดือนมิถุนายน) คำสั่งซื้อลดลงอย่างรุนแรง ลดการประมูลลงถึง 38% เมื่อเทียบกับเดือนก่อนหน้า แต่การขยายเวลาการให้เงินอุดหนุนในภูมิภาคได้รักษาความยืดหยุ่นของการจัดเก็บพลังงานเชิงพาณิชย์และอุตสาหกรรม (C&I) ไว้ได้

ในต่างประเทศ มีแรงขับเคลื่อนหลายประการ: อัตราภาษีของสหรัฐฯ เพิ่มขึ้นจาก 34% เป็น 125% ทำให้การส่งออกในเดือนเมษายน-ต้นเดือนพฤษภาคมหยุดชะงัก อัตราภาษี 10% ต่อมาพร้อมกับระยะเวลา 90 วัน ได้ก่อให้เกิดการเพิ่มขึ้นอย่างรุนแรงในช่วงปลายเดือนพฤษภาคมเพื่อหลีกเลี่ยงภาษี ซึ่งกลายเป็นเสาหลักหลักของไตรมาสนี้ ตัวขับเคลื่อนความต้องการที่คู่กันไปได้แก่:

-

ออสเตรเลีย: การเร่งรีบก่อนเดือนกรกฎาคมเพื่อรับเงินอุดหนุนที่อยู่อาศัยมูลค่า 2.3 พันล้านดอลลาร์ออสเตรเลีย

-

ยุโรป: หลังจากการลดลงของสินค้าคงคลัง + การฟื้นตัวของคำสั่งซื้อที่ขับเคลื่อนด้วยการไฟฟ้าดับในสเปน

รวมกันแล้ว ปัจจัยเหล่านี้ได้รักษาแรงขับเคลื่อนความต้องการระดับโลกที่โดดเด่นไว้ได้

การทบทวนและแนวโน้มราคาเซลล์การจัดเก็บพลังงานในครึ่งปีแรกของปี 2568

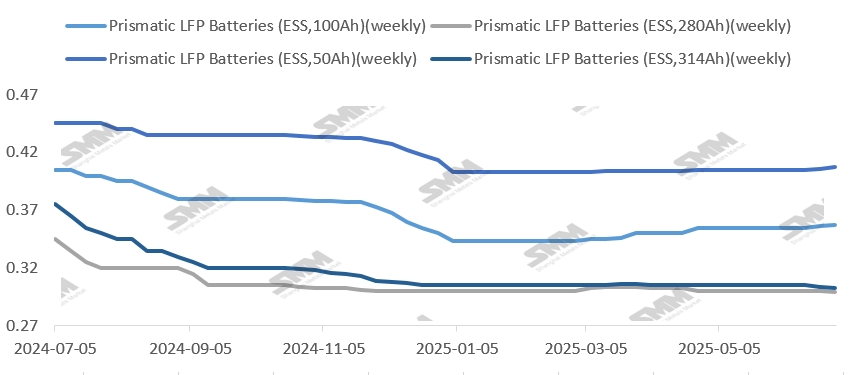

ความผันผวนของราคาเซลล์การจัดเก็บพลังงานได้ลดลงอย่างมากในปี 2568 เมื่อเทียบกับปี 2567 หลังจากที่ราคาต่ำสุดเป็นวงจรในช่วงปลายปี 2567 “สงครามราคา” ในประเทศก็ดำเนินไปตลอดครึ่งปีแรกและขยายไปยังตลาดตะวันออกกลางกลยุทธ์ที่ให้มูลค่าตามตลาด — แม้ว่าจะต้องใช้เงินทุนสำรองจำนวนมาก — ก็ยังคงเป็นไปได้สำหรับผู้เล่นบางรายภายในขอบเขตความยั่งยืน

เดือนมิถุนายนเป็นจุดเปลี่ยน เมื่อความต้องการที่แข็งแกร่งขับเคลื่อนให้ราคาทั่วไปมีเสถียรภาพ ณ วันที่ 18 กรกฎาคม:

-

เซลล์ LFP แบบสี่เหลี่ยมผืนผ้า 314Ah ลดลงเพียง 0.33% เมื่อเทียบกับช่วงเวลาเดียวกันของปีก่อน

-

เซลล์ LFP แบบสี่เหลี่ยมผืนผ้า 280Ah ฟื้นตัวกลับมาอยู่ในระดับเดียวกับเดือนมกราคมหลังจากปรับกลางทาง

-

เซลล์ 100Ah และ เซลล์ 50Ah เพิ่มขึ้น 4.08% และ 0.74% ตามลำดับ

มุมมองการแบ่งกลุ่มสินค้า

จากมุมมองการแบ่งกลุ่มสินค้า เซลล์เก็บพลังงาน 314Ah ได้เสร็จสิ้นการเปลี่ยนแปลงกำลังการผลิตเต็มรูปแบบในปี 2568 และครองส่วนแบ่งตลาดภายในประเทศมากกว่า 70% ขนาดใหญ่ของเศรษฐกิจช่วยลดต้นทุนลงอย่างมาก ในขณะที่คำสั่งซื้อจากต่างประเทศที่เพิ่มขึ้นและการติดตั้งล่วงหน้าที่ขับเคลื่อนโดย "วันสุดท้ายของการบูรณาการเข้ากับระบบไฟฟ้า 531" ที่รวมศูนย์ได้สร้างสถานการณ์การผลิตเกินความต้องการเล็กน้อย ซึ่งผลักดันให้ราคาเซลล์ 314Ah ลดลงเล็กน้อย ในขณะเดียวกัน เซลล์ 280Ah มีเป้าหมายหลักไปที่ตลาดยุโรปและออสเตรเลียที่ให้ความสำคัญกับความปลอดภัย (ส่วนแบ่งภูมิภาคมากกว่า 50%) ซึ่งความสมดุลระหว่างอุปทานและความต้องการที่มั่นคงจำกัดผลกระทบต่อราคาโดยรวมของพวกเขา แม้ว่าราคาลิเธียมคาร์บอเนตจะลดลงอย่างต่อเนื่อง — ซึ่งในทางทฤษฎีจะลดต้นทุนลง — แต่การประหยัดเหล่านี้ก็ล้มเหลวในการส่งผ่านไปยังราคาผลิตภัณฑ์สุดท้ายอย่างมีประสิทธิภาพ โดยมีอิทธิพลเพียงเล็กน้อยของวัตถุดิบต่อการเปลี่ยนแปลงของราคาที่ค่อยๆ ลดลง ทั่วช่วงครึ่งปีแรก พลวัตของอุปทานและความต้องการยังคงเป็นตัวขับเคลื่อนหลักของการเคลื่อนไหวของราคาการเก็บพลังงานขนาดใหญ่ การเพิ่มขึ้นของราคาเซลล์ความจุน้อยมาจากสองปัจจัยหลัก: อย่างแรก คือ ความต้องการที่พุ่งสูงขึ้นจากตลาดที่อยู่อาศัยในต่างประเทศ — การสนับสนุนเงินช่วยเหลือการเก็บพลังงานที่อยู่อาศัยของออสเตรเลียมูลค่า 2.3 พันล้านดอลลาร์ออสเตรเลียที่มีผลบังคับใช้ตั้งแต่วันที่ 1 กรกฎาคม ร่วมกับการเติบโตอย่างต่อเนื่องในยุโรปและตลาดเกิดใหม่ และอย่างที่สอง คือ ข้อจำกัดของกำลังการผลิตที่แข็งแกร่ง — สายการผลิตขนาดเล็กมีส่วนแบ่งของกำลังการผลิตทั้งหมดเพียงเล็กน้อย ในขณะที่ต้นทุนการเปลี่ยนแปลงข้อกำหนดสูงทำให้ผู้ผลิตไม่เปลี่ยนแปลงการผลิตในระยะสั้น ซึ่งรักษาสภาพการสมดุลระหว่างอุปทานและความต้องการที่เข้มงวดซึ่งสนับสนุนแนวโน้มราคาที่เพิ่มขึ้น

แนวโน้มราคา

เมื่อมองไปข้างหน้า ในช่วงที่อุปทานตึงตัวในปัจจุบัน ราคาตามสปอตจากบางองค์กรเริ่มเพิ่มขึ้นในช่วงปลายเดือนมิถุนายน (โดยทั่วไปอยู่ในช่วง 0.005 หยวนต่อวัตต์ชั่วโมง) การวิจัยตลาดระบุว่าคำสั่งซื้อการเก็บพลังงานในระดับสาธารณูปโภคจากผู้ผลิตระดับ 1-2 มีกำหนดการจนถึงเดือนกันยายน โดยความต้องการที่ยังคงอยู่อาจขยายเวลาการเพิ่มขึ้นของราคาตามสปอตอย่างไรก็ตาม ผู้รวมโครงการในตลาดล่างแสดงให้เห็นถึงความต้องการซื้อที่อ่อนแอ โดยนอกเหนือจากการปฏิบัติตามสัญญาระยะยาวที่มีอยู่ก่อนแล้ว พวกเขายังคงรักษาการจัดซื้อที่จำเป็นเท่านั้นสำหรับคำสั่งซื้อแบบสปอตที่ราคาสูง ในด้านต้นทุน ราคาลิเทียมคาร์บอเนตได้เพิ่มขึ้นอย่างต่อเนื่องตั้งแต่เดือนกรกฎาคม โดยราคาสำหรับวัสดุเกรดแบตเตอรี่ได้ถึง 70,550 หยวนต่อตันเมื่อวันที่ 24 กรกฎาคม ข้อมูลจากอุตสาหกรรมยืนยันว่าการเพิ่มขึ้นของราคาลิเทียมคาร์บอเนต 10,000 หยวนต่อตัน จะทำให้ราคาเซลล์แบตเตอรี่ผันผวนประมาณ 0.002-0.003 หยวนต่อวัตต์ชั่วโมง ซึ่งให้การสนับสนุนราคาในระยะสั้น อย่างไรก็ตาม ในระยะยาว การเพิ่มขึ้นของราคาลิเทียมนี้ยังคงขับเคลื่อนโดยอารมณ์เป็นหลักและมีพื้นฐานทางเศรษฐกิจที่อ่อนแอ ราคาเซลล์แบตเตอรี่คาดว่าจะมีการปรับราคาเล็กน้อยหลังจากเดือนสิงหาคม ก่อนที่จะคงที่

การวิเคราะห์ตลาดในแต่ละภูมิภาค

จีน: ความกังวลในตอนแรกเกี่ยวกับความต้องการจากฝั่งระบบไฟฟ้าหลังจากที่เอกสารหมายเลข 136 ยกเลิกการจัดสรรพื้นที่เก็บพลังงานไฟฟ้าที่บังคับใช้ได้รับการบรรเทาลงจากการปฏิรูปตลาดไฟฟ้าที่เร่งรัดและการแทรกแซงของรัฐบาลระดับจังหวัดที่ทันเวลา ความต้องการเซลล์เก็บพลังงานไฟฟ้าในครึ่งหลังของปี 2568 คาดว่าจะคงที่ อย่างน่าสังเกต กลไกตลาดกำหนดให้มีความต้องการที่สูงขึ้นสำหรับความสามารถในการรวมระบบและการควบคุมต้นทุน ผู้เล่นที่มีเทคโนโลยีขั้นสูงจะครอบครองความต้องการเพิ่มเติมส่วนใหญ่ ในระยะยาว รูปแบบการดำเนินงานของสถานีเก็บพลังงานไฟฟ้าอิสระยังคงอยู่ในช่วงการสำรวจ การกระจายรายได้ขยายออกไปนอกเหนือจากการซื้อขายในช่วงเวลาที่มีการใช้ไฟฟ้าสูงและต่ำเพื่อรวมถึงการเช่าพื้นที่เก็บพลังงานไฟฟ้า การสนับสนุนจากรัฐบาลสำหรับพื้นที่เก็บพลังงานไฟฟ้า การซื้อขายในตลาด และการลดความต้องการใช้ไฟฟ้าสูงสุดและการควบคุมความถี่ อย่างไรก็ตาม ราคาเช่าพื้นที่เก็บพลังงานไฟฟ้าและระยะเวลาเช่าต่ำกว่าแนวทางการให้ความช่วยเหลือ ซึ่งเป็นข้อเสียสำหรับนักลงทุน การสนับสนุนจากรัฐบาลสำหรับพื้นที่เก็บพลังงานไฟฟ้าแตกต่างกันไปในแต่ละจังหวัด การซื้อขายในตลาดต้องเผชิญกับข้อจำกัดด้านสภาพคล่องและคู่สัญญา และการส่งพลังงานไฟฟ้าที่ควบคุมโดยระบบไฟฟ้าหลักสร้างความไม่แน่นอนสำหรับบริการเสริม ผู้ครอบครองโครงการในตลาดล่างยังคงรักษาทัศนคติที่ระมัดระวัง

สหรัฐอเมริกา: ในระยะสั้น ผู้ผลิตเซลล์แบตเตอรี่ในประเทศยังคงมีความคาดหวังในการเจรจาเรื่องภาษีศุลกากรใหม่ แต่ตัวแปรความต้องการหลักขึ้นอยู่กับพระราชบัญญัติ Big and Beautiful Act ในขณะที่ยกเลิกการลดหย่อนภาษี ITC/PTC สำหรับโซลาร์ พระราชบัญญัติได้ผ่อนคลายข้อจำกัดของการลดหย่อนภาษี ITC สำหรับการเก็บพลังงานไฟฟ้าในเวลาเดียวกัน โดยการให้ความช่วยเหลือต้องมีการบรรลุเกณฑ์ต้นทุนของ "หน่วยงานต่างประเทศที่น่ากังวล" (การลดลงตามลำดับสอดคล้องกับพระราชบัญญัติลดการปล่อยก๊าซเรือนกระจก) ดังนั้น การประกาศกฎระเบียบการดำเนินงานเมื่อวันที่ 18 สิงหาคม จึงกลายเป็นจุดสำคัญสำหรับความต้องการในสหรัฐอเมริกาในอนาคต ในระยะยาว ความต้องการในสหรัฐอเมริกาในครึ่งหลังของปี 2568 คาดว่าจะยังคงให้การสนับสนุนเพิ่มเติมดังนั้น หลังจากที่มีการเพิ่มขึ้นของความต้องการที่ขับเคลื่อนด้วยนโยบายในปี 2568 (ค.ศ. 2025) แล้ว ความกดดันในการชะลอตัวของการเติบโตในปี 2569 (ค.ศ. 2026) จะเพิ่มขึ้น ซึ่งจำเป็นต้องมีการจัดสรรกำลังการผลิตใหม่ไปยังสถานการณ์ที่ไม่ขึ้นอยู่กับการสนับสนุน

![[แบตเตอรี่ลิเธียม: GEM มุ่งเน้นขยายตลาดผลิตภัณฑ์ระดับสูงสำหรับธุรกิจพรีเคอเซอร์สามธาตุ]](https://imgqn.smm.cn/usercenter/ezoBg20251217171730.jpg)

![[การกักเก็บพลังงาน: โครงการแบตเตอรี่กักเก็บพลังงานสามโครงการของ CALB ได้รับการอนุมัติ]](https://imgqn.smm.cn/usercenter/AmiJU20251217171730.jpg)