SHANGHAI, Jul 27 (SMM) - Monetary policies in Europe and the United States are unlikely to tighten any time soon, and expectations over inflation continued to rise. The decline of commodity prices last week was mainly driven by reserves offered by the State Reserve Bureau. Nickel prices fell before rebounding in the wake of reserves injection by the SRB. Macroeconomic developments are expected to buoy nickel prices.

On fundamentals, nickel ore prices continued to rise last week. Port inventories accumulated amid higher shipments arrivals at ports, but most of the arriving shipments have been booked. Overall supply of spot nickel ore remains tight. NPI prices climbed further and stainless steel companies accepted higher NPI prices. The current NPI supply is tight and supply of stainless steel was lower than expected in July, driven by the recent power and production restrictions.

Planned output of #300 stainless steel is expected to stand at around 1.58 million mt, weakening demand for pure nickel. However, nickel prices are expected to rise further should stainless steel prices remain strong. On the new energy front, prices of battery-grade nickel sulphate were quoted at a high of 38,000 yuan/mt last week, 25,000 yuan/mt higher than nickel briquette prices.

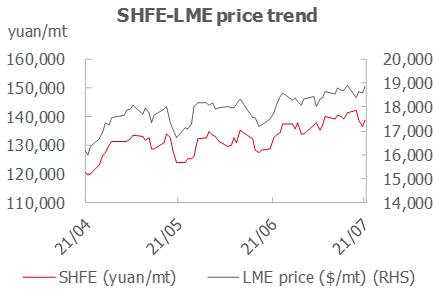

Profits of nickel sulphate using dissolved nickel briquette remained at high levels. Over half of the expected shipments arrivals of nickel briquette have been booked. Meanwhile, LME and domestic nickel briquette inventories continued to decline. This combined with promising demand for nickel briquette will keep nickel fundamentals optimistic. LME nickel prices are expected to move between $18,600-19,500/mt this week. SHFE nickel prices are likely to fluctuate between 139,000-146,000 yuan/mt.