I. Nickel Sulphate Market Overview

Since mid-July, SMM battery-grade nickel sulphate prices have shown an upward trend, with the average price rising from 27,220 yuan/mt on July 15 to 27,800 yuan/mt on September 1. Prices are expected to fluctuate upward overall in Q3.

Key reasons include:

**Cost side**, some enterprises need to procure raw materials for new refined nickel projects in Q3, while the September-October peak season for ternary precursors further drives demand for nickel salt raw materials. Buyer-side demand has pushed up intermediate product coefficients, strongly supporting nickel sulphate production costs.

**Supply side**, tight raw material supply has affected production plans at some nickel salt smelters, coupled with maintenance shutdowns at certain producers in August, reducing spot order supply in the nickel sulphate market.

**Demand side**, downstream enterprises are stockpiling for the traditional auto sales peak season ("September-October peak season"), leading to increased precursor orders. Strong sales of certain car models this year have also boosted raw material demand upstream in the supply chain, driving higher nickel sulphate procurement demand in Q3. Additionally, some nickel salt smelters have their own precursor orders, and the growth of these orders has reduced their available nickel sulphate supply for external sales in August-September.

Overall, the current nickel sulphate market reflects weak supply alongside growing demand, driving continuous price increases.

II. Sustainability of Nickel Sulphate Price Rally

After the September-October peak season, nickel sulphate prices may ease in Q4, but the expected decline is likely to be milder than in previous years. Key reasons include: (1) the intermediate product market is expected to remain tight, with currently high coefficients supporting nickel sulphate production costs; (2) as the market faced shortages in Q3, large-scale destocking is unlikely in Q4, resulting in a smaller YoY price drop for nickel salts. Moreover, strong precursor demand from certain domestic car models in H2 will provide additional support.

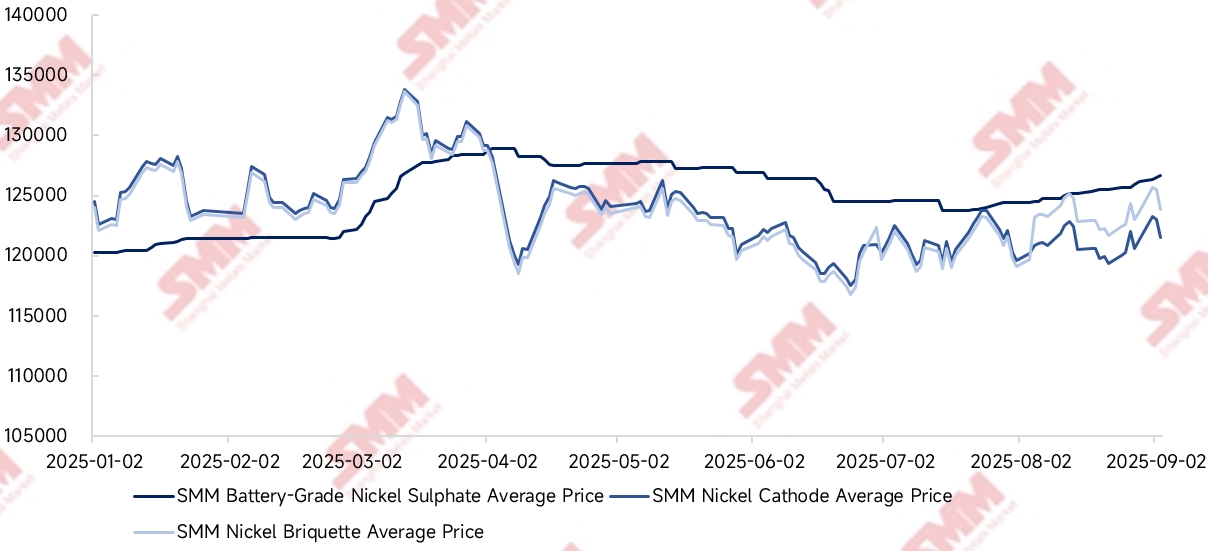

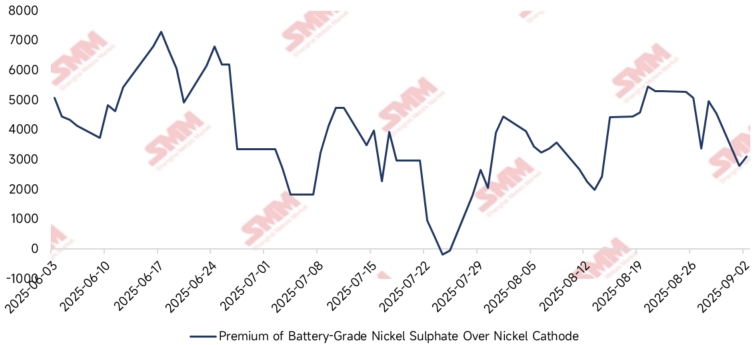

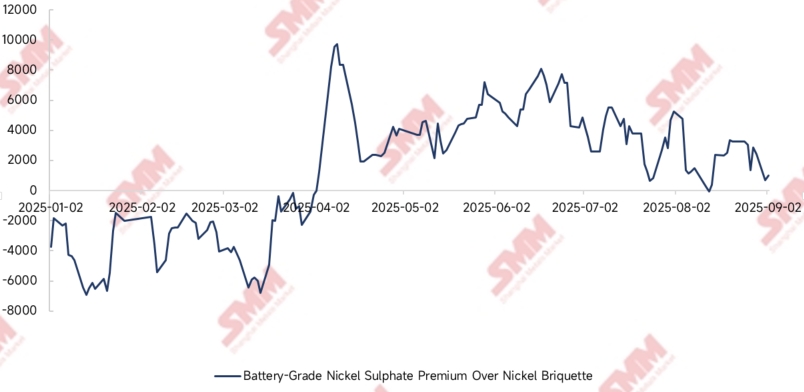

III. Economic Analysis of Interconversion Between Refined Nickel and Nickel Sulphate

The interconversion primarily takes two forms:

1. **Nickel Sulphate to Refined Nickel**:

SMM analysis shows the industry processing cost for producing electrodeposited nickel from nickel sulphate is around 7,000 yuan/mt Ni. Thus, when nickel sulphate prices trade at a discount of over 7,000 yuan relative to refined nickel, the conversion channel may theoretically open. Since April, nickel sulphate prices have maintained a premium over refined nickel, keeping this channel closed from a cost perspective.

2. **Nickel Briquette Dissolution to Nickel Sulphate**:

The processing cost for dissolving nickel briquettes into nickel sulphate solution ranges between 3,000-5,000 yuan/mt Ni. The conversion channel may theoretically open when the nickel sulphate premium over nickel briquettes exceeds this fee. Currently, China’s nickel briquette supply relies mainly on imports (primarily from Australia and Madagascar), with relatively small market circulation. Despite recent nickel sulphate price increases, the premium over nickel briquettes averaged around 3,000 yuan in August, leaving the dissolution window closed.

In summary, as neither the nickel sulphate-to-refined nickel nor nickel briquette-to-nickel sulphate conversion channels are open, interconversion is unlikely to significantly impact short-term nickel sulphate supply and demand. The market is expected to remain tight in September.

![[SMM Nickel Sulphate Daily Review] March 11, Raw Material Uncertainty Persisted, and Nickel Salt Prices Remained Stable](https://imgqn.smm.cn/usercenter/NHXhQ20251217171733.jpg)

![[NPI Daily Review] Market Procurement and Sales Activity Recovered, and High-Grade NPI Prices Still Had Upside Room](https://imgqn.smm.cn/usercenter/UpZsx20251217171731.jpeg)