SMM July 21: at the online zinc market live broadcast conference hosted by SMM on July 21, Han Zhen, a zinc analyst at SMM, gave a detailed explanation on the theme of "the pattern of increasing supply, demand and decreasing, continuing the upward test of zinc prices." she believes that short-term zinc prices will continue to fluctuate at high levels, and the follow-up depends on the situation of dumping and storage, after the actual landing in August. If there is an actual accumulation of inventory, we can gradually test the high and light positions.

Although there is a disturbance of "double control of energy consumption" in Inner Mongolia, the output of domestic mines has recovered steadily.

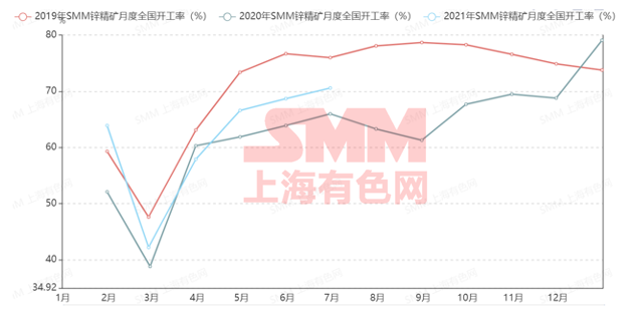

According to SMM research, despite the disturbance of "double control of energy consumption" in Inner Mongolia, domestic mine production is still steadily recovering. According to statistics, the output of zinc concentrate reached 330900 metal tons in June, with an operating rate of 70.6%, an increase of 3.9% from the previous month. As can be seen from the chart below, the overall output of domestic zinc mines showed an increasing trend in June, one reason for the increase is that Yunnan Lanping restored and made up the previous monthly production in June, and the other is the periodic resumption of production in Galqi, Inner Mongolia. However, the enterprise's original ore inventory is low, and the production plan was reduced in July. In addition, Sanguikou in Inner Mongolia resumed dual-system production and increased production in June.

However, from the end of June to the beginning of July, due to the limited production of "July 1" environmental protection, explosives were limited in some areas, and low raw ore stocks led to the suspension of production. According to SMM survey data in July, although some enterprises stopped production in the first week, normal production resumed after the explosive restrictions were lifted, and the overall impact was smaller than that in June, and the mining industry in Sanguikou, Inner Mongolia and southern Qinghai also increased production. Therefore, taken together, SMM expects domestic mineral production in July to be 335200 metal tons, an increase of 4300 metal tons compared with the previous month.

The inflow of imported zinc mines to reduce the steady recovery of domestic mineral production is the key.

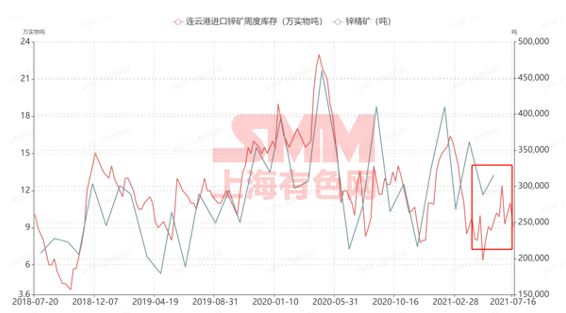

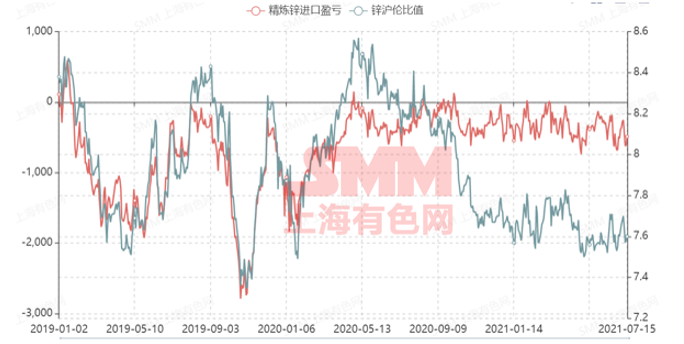

According to customs data, imports of zinc concentrate reached 315700 physical tons in May, an increase of 9.53% from the previous month, but 11.5% lower than the same period last year. The reason for the increase in import volume in May compared with the same period last year is that Australia's long unit import volume returned to a high level and increased compared with the same period last year, on the other hand, the domestic mineral output is high, and the processing fee of 3900 yuan per ton is also more advantageous. Enterprises are highly favored.

It is worth mentioning that under normal circumstances, the inventory of Lianyungang is highly consistent with the import of zinc concentrate, but the inventory of Lianyungang in June has been fluctuating in the range of 9-120000 tons, and no further recovery has been seen. it is mainly because the domestic mineral production is steadily increasing, the dependence on overseas mines is low, the import window is not opened, and the processing fees in foreign countries such as South Korea and Japan are on the low side, which are more favored by bulk orders. Therefore, the domestic import is mainly long single, and the bulk order signing is very small, which is the reason why the amount of zinc ore imported in June is only 236500 tons.

In July, SMM expects imports to rise from a month earlier to around 300000.

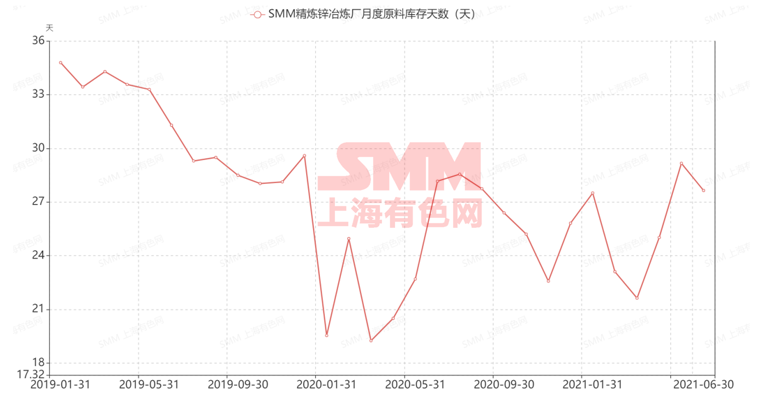

The number of days of raw material inventory in the smelter decreased by 1.52 days to 27.65 days in June compared with the previous month.

In June, the number of days of raw material inventory at the smelter decreased by 1.52 days to 27.65 days from the previous month, while in July, when there were no import orders and only relied on domestic mines and long orders, SMM predicted that as domestic smelter production continued to increase, there would be a slight shortage of mines, and raw material inventories might decline slightly again. It is mainly because the issue of winter storage is involved in the fourth quarter. In terms of import prices, according to SMM, the transaction price in the fourth quarter has exceeded US $100. in this case, the shortage of mines in the fourth quarter may be alleviated, and we can pay more attention to the processing fees in the fourth quarter.

The storm of power restriction in many places in July has once again dragged down the production of zinc refining.

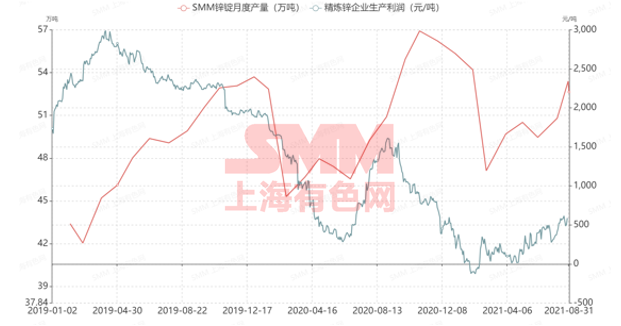

According to SMM research, the output of refined zinc in June exceeded expectations by 508000 tons, an increase of 13300 tons from the previous month, a comprehensive operating rate of 81.34 percent, and an increase of 2.13 percent from the previous month. The main reason for the higher-than-expected increase is the rapid increase of refineries in Shaanxi, while the power cuts in Yunnan in June and routine maintenance in Gansu have also affected a certain amount of production.

From the production profits of the refinery, we can see that the profits of the refinery have been repaired at present, which will stimulate the operation of the smelter to increase production. Recently, although the production of electric refineries in Guangxi, Yunnan and other places has been affected to a certain extent, the overall win is limited. Overall, SMM expects domestic refined zinc production to increase by 19500 tons to 528000 tons month-on-month in July. In August, domestic refined zinc production decreased by 4000 tons to 524000 tons compared with the previous month.

Import window closed in June, refined zinc imports decreased

According to the latest customs statistics, refined zinc imports were 57500 tons in May and 37500 tons in June. The monthly imports in the first half of this year showed a trend of increase compared with the same period last year. However, it is worth mentioning that although the Shanghai-Lun ratio has been repaired in June, the import window has been closed and can only rely on long orders, so refined zinc imports decreased by 20,000 tons month-on-month in June. In July, SMM expects refined zinc imports to remain at around 40, 000 tons.

In June, northern environmental protection limited production and assisted galvanizing started to go down.

According to SMM research, the operating rate of galvanizing was 78.71% in June, down 8.64% from the previous month. Mainly due to weather reasons, coupled with galvanizing in the traditional off-season and environmental production restrictions and steel price fluctuations, the comprehensive effect of many factors led to the decline of galvanizing operation rate in June. In July, with the digestion of terminal inventory, the purchase of galvanized tubes increased and the inventory of finished products decreased, but overall consumption did not improve significantly.

Rising steel prices lead to start-up differentiation of galvanized plates

Galvanized pipe, galvanized profits still exist downside risks. Survey data show that although the recent galvanized pipe profits have been repaired, but the current steel prices rise again, galvanized pipe profit space will be further compressed. At present, most galvanized pipe factories are operating at about 80% to 90%. If the loss extends to the critical value of the enterprise, it may force the enterprise to reduce production again.

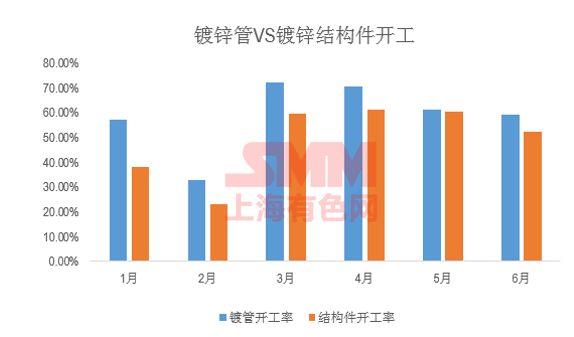

As can be seen from the picture above, the start of construction of galvanized tubes is higher than that of galvanized structural parts, because most of the sales of galvanized pipes are distributed in real time through dealers, so their sales prices are obviously affected by the rise and fall of steel. In addition, dealers generally buy up but not buy down. When steel prices rise, dealers have a certain mood of hoarding, while galvanized structures generally receive projects or pre-orders. After 2000, the price of steel is too high, the profits of enterprises are seriously compressed, the enthusiasm of production is not high, and small and medium-sized enterprises are closed. Therefore, there are differences between galvanized tubes and galvanized structures.

2021 the planned investment of the State Grid will increase by 2.8% to 473 billion yuan in the real estate market to cool down.

2021 State Grid plans to increase its investment by 2.8% to 473 billion yuan, but the increase in zinc consumption may be reduced taking into account the rise in the price of raw materials. Taking into account the overall investment ratio, SMM believes that Electroweb's investment will increase in the second half of the year, but at the same time, affected by the current rise in raw material prices, the increase in zinc may be compressed to a certain extent.

New real estate construction began in May to cool down, but there may still be support for completion. SMM believes that in the past two years, the real estate market may still show a relatively moderate trend, while the construction of national infrastructure projects is also increasing. According to the latest 14th five-year Plan, such as the traffic planning of the Yangtze River Delta, the increase of high-speed rail stations, ports and airports will be carried out by factories, while Shandong will also realize the city-to-city high-speed rail plan during the 14th five-year Plan period. The construction of these infrastructure projects will also support the galvanized plate in the future.

The consumption support of automobiles and household appliances is slightly degraded.

The problem of "lack of core" will still affect automobile production in the future, while the domestic climate will also delay consumption in the field of home appliances.

However, on the whole, SMM still maintains a steady and good view of the galvanized plate. With the arrival of the follow-up Jinjiu Silver Ten, SMM predicts that orders will gradually improve in mid-late August, and taking into account that there may be some strength after the completion of the previous national investment, galvanized orders are expected to increase gradually. And recently SMM learned that overseas galvanized exports are good, overseas galvanized sheet prices are high. Thus it can be seen that even if the export tax rebate is abolished, the export profit is still very considerable.

The start-up of die-casting zinc alloy is weak in the off-season of consumption.

In June, the operating rate of die-casting zinc alloy enterprises of the old sample was 36.96%, down 2.75% from the previous month, and an increase of 7.96% over the same period last year. Taking into account the current off-season of consumption, SMM expects the operating rate of die-casting zinc alloy in July to be at a downward risk. It is estimated that the operating rate of the old sample of die-casting zinc alloy in July is 35.07%, down 1.89% from the previous month, and an increase of 0.36% over the same period last year.

The consumption toughness of zinc oxide is insufficient and the start-up continues to decline.

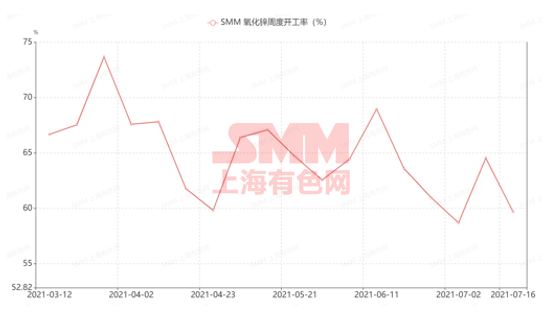

As for zinc oxide, according to SMM survey data, the operating rate of zinc oxide enterprises was 52.69% in June, a month-on-month decrease of 0.51%. It is expected that there is still room for downward operation of zinc oxide in July. On the one hand, because automobile consumption has weakened in the past two months, it has transmitted to the tire industry, on the other hand, because the price of feed-grade zinc oxide has dropped seriously, the stock has decreased, the demand for terminal procurement has declined, and there is no increase in electronic-grade orders. moreover, zinc prices are on the high side, and there is also a serious price crackdown in some areas. on the whole, the production pressure of zinc oxide enterprises is relatively large.

The transmission of upstream raw materials to downstream consumer industries is not smooth.

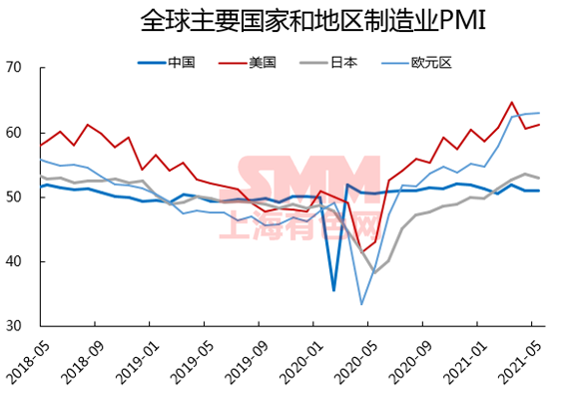

After entering 2021, the marginal improvement of China's manufacturing industry slows down, while European and American economies enter the range of rapid expansion. Under the influence of inflation and the sharp increase in overseas demand, domestic raw material prices rise sharply, but the downstream consumption transmission is not timely, and domestic CPI and PPI split.

According to the research of SMM, the rising price of raw materials has caused the production cost pressure of the whole enterprise to be on the high side. On July 15, the central bank also comprehensively cut the deposit reserve ratio of financial institutions by 0.5%, in order to reduce the production pressure of enterprises, but it will take some time to transmit to the actual production of enterprises.

At present, the logical point of market transaction is inventory.

Data source: SMM database

SMM believes that the trading logic of zinc in the second half of the year lies in inventory, and for zinc, the trading logic has always been supply pricing, which is why SMM has been bearish for a long time, but at present, from the point of view of the matching degree of supply and demand, mines and smelters match well, and then we mainly need to see whether consumption can match the increment of the smelter.

Price trend of zinc ingot dumping and storage

In early July, the state conducted a public sell-off of 30,000 tons, which accounted for about 5% of the consumption quota, based on annual zinc consumption, mainly in warehouses in Anhui, Hebei, Henan and Jiangxi. However, according to the current price trend of zinc ingots, the dumping did not have a greater impact on the price. This week, the state also said that it will arrange the next dumping as soon as possible, and SMM will also track it in time after the specific data come out.

In terms of zinc prices, under the background of generally bearish market, the reason why zinc prices remain high is that, on the one hand, its inventory is still at a historical low level, and zinc valuations have been on the low side compared with copper and aluminum. Bears and bulls will not act rashly, so we should continue to pay attention to the specific amount of reserves.

In terms of the price range, SMM expects that short-term zinc prices will continue to maintain high shocks, and the follow-up depends on the situation of dumping and landing. After the actual landing in August, if the inventory actually accumulates, it can gradually test the high light positions.