SHANGHAI, Apr 26 (SMM)—The SHFE/LME copper price ratio fell to a three-year low last week as LME copper outperformed SHFE copper prices, expanding import losses. Some smelters have begun to export as export profit occurred. With increased reverse arbitrage operations and exports, SHFE copper prices are expected to strengthen this week.

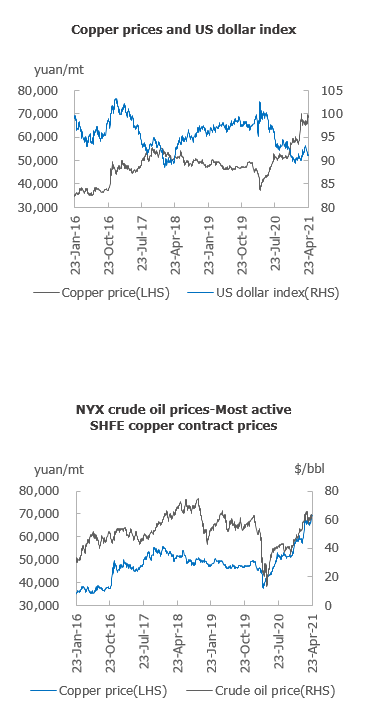

On macros, US data remained upbeat, with initial jobless claims falling to a low two weeks ago. US existing home sales in March also performed well. However, the US dollar index continues to fall as accelerated recovery in Europe has bolstered the euro. The US dollar index is unlikely to fall given strong economic figures.

Domestic fundamentals failed to improve. The import volume of copper concentrate in March hit a new high, and the import of copper scrap increased by 114% month-on-month to 172,000 mt. The import volume of copper cathode stood at 339,000 mt in March, an increase of 28.7% on the month. Downstream buying interest did not improve substantially against high copper prices. Most of the companies moved cargoes under long-term contracts. Ample supply and weak demand should pressure copper prices.

Technically, open interest increased last week amid market bullishness. SHFE copper is expected to trade at 68,500-70,000 yuan/mt this week and LME copper prices are expected to move between $9,380-9,550/mt.

Spot discounts in Shanghai moved between 150-70 yuan/mt last week. Some downstream processing plants have begun to stock up on cargoes for Labour Day holidays. However, most traders and sellers will liquidate stocks at the month-end. Meanwhile, the inflow of high-quality copper like CCC-P and a small inflow of Peruvian cargoes last Friday have weighed on high-quality copper prices. As such, spot discounts are expected to stand at 170-100 yuan/mt this week.