(17 April)

< 1 > in terms of epidemic situation.

The new situation of the domestic epidemic situation: the total number of imported cases was 1549, asymptomatic infection was 1038, and the number of deaths was revised to 4642.

Overseas epidemic: > 2.11 million / 142791 deaths.

Epidemic situation in Europe and the United States:

The first square array of the United States: more than 678000 confirmed cases, 34641 deaths, the United States gives priority to no one to move! Go, go!

Europe: second Square Array (diagnosis / death): Italy (> 168000 / 22170), Spain (> 184000 / 19315), France (> 165000 / 17920), United Kingdom (> 104000 / 13759), Germany (> 13.8 4093).

Third Square: Belgium, Russia, Netherlands, Portugal, Ireland, Switzerland, Sweden, (1w / 4W), Austria. The Russian outbreak phase.

Asian and stone related countries: kangaroos in Iran and Australia continue to improve. Brazil is only increasing by 208 people, whether the inflection point is concerned.

Iran (> 77000), Turkey (> 74000), Israel (> 12000), Canada (> 30000), Brazil (> 30000), India (> 13000), Peru (> 74000), Japan (> 9500), Australia kangaroo (6497), Malaysia (5182), Indonesia (5923), Singapore (4427), South Africa (2608), Philippines (5878).

< 2 > current playback:

1. Spot prices are generally strong and volatile, strong in the north and weak in the south.

The northern part of the country rose, by 10 yuan and 30 yuan per ton. Southern stability in the strong: South China Guangzhou, East China, Shanghai, Hangzhou market rose 20-30% in early trading, macro data sunrise back to give up the increase.

Trading volume is still strong!

The market mentality is stable and positive.

Tangshan area billet upward 10 to 3080 yuan / ton.

Raw material end:

Scrap prices continued to soar in some parts.

Coke prices remain stable and stable.

The market for imported main coking coal continued to decline.

Iron ore market: the port spot market fell slightly by 2 yuan / ton, steel mills still purchase on demand, merchants' willingness to ship increased, investment weakened. The transaction of PB powder in Shandong area is 650-655 yuan / ton, and that of PB powder in Tangshan area is 650-655 yuan / ton.

2. Futures: the overall rise and fall.

RB2010 main force contract: in the day between 3435 and 3374 sharply reduced positions to fall back, the end of 3381.

HC2010 main contract: in the day between 3277 and 3215 rose and fell back, the end of 3235.

Iron ore i2009 main contract: in the day between 621.5 and 606.5 rushes down, the end of the day.

Coke J2009 main contract: within the day between 1738.5 and 1703 horizontal plate concussion, the end of 1717.5.

Coking coal JM2009 main contract: within the day between 1148.5 and 1121 horizontal disk concussion, the end of 1136.5.

< 3 > current forecast for next week

Preface: this week, the rebar market generally rebounded 100 yuan / ton, the rest also rebounded to varying degrees. The author's forward-looking deduction after the festival Xiaoyangchun cash landing. The main reason is that there are beautiful women in the north, the strong return of demand, and the quietly changing fundamentals.

1. Spot aspect: rush high fall probability is big, but space is limited.

2. Futures: RB2010 main contract: concussion between 3470 and 3320.

HC2010 main contract: concussion between 3300 and 3150.

I2009 main contract: concussion between 628 and 590.

J2009 main contract: concussion between 1750 and 1670.

JM2009 main contract: concussion between 1180 and 1100.

3. Spot operation tips: continue to high throw low suction rolling operation.

Futures trading tips:

Thread, hot coil: within the range of high altitude, low multi-operation is appropriate.

Iron ore: trend high empty single holding, short-term range of high-altitude low-level rolling operation is appropriate.

Coke: trading within the range is neutral.

Coking coal: tasteless wait-and-see or neutral trading within the range.

Timely stop profit stop is a hard road.

RB2010 main force contract: support level 3370, 3340.

HC2010 main force contract: support level 3210, 3170.

I2009 main contract: support level 590, pressure level 624.

J2009 main contract: support level 1670, pressure level 1750.

JM2005 main force contract: support level 1100, pressure level 1180.

< IV > Information and heart language.

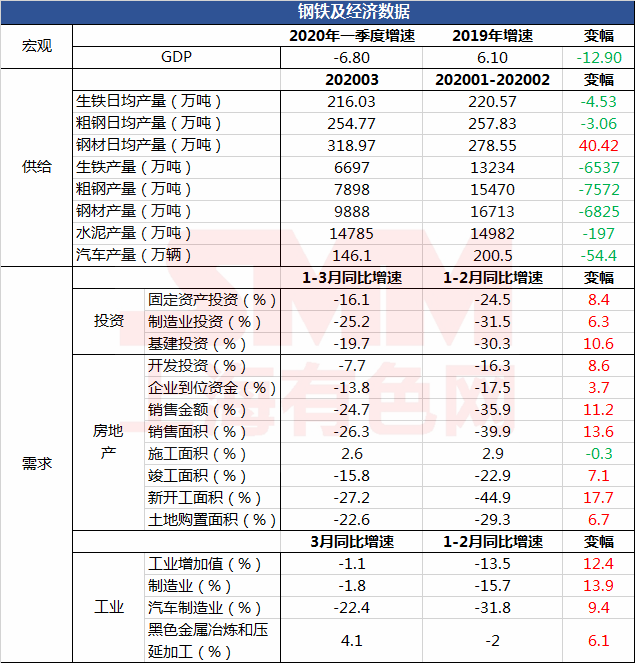

1. [national Bureau of Statistics: China's GDP fell 6.8 percent in the first quarter compared with the same period last year]. In the first quarter, China's gross domestic product (GDP) totaled 20.6504 trillion yuan, which was 6.8 percent lower than the same period last year. In terms of sub-industries, the added value of the primary industry was 1.0186 trillion yuan, down 3.2%; the added value of the secondary industry was 7.3638 trillion yuan, down 9.6%; and the added value of the tertiary industry was 12.268 trillion yuan, down 5.2%.

Generally speaking, in the first quarter, under the impact of the new crown pneumonia epidemic, the overall economic and social situation in China remained stable. At the same time, it should also be noted that the current international epidemic continues to spread, the downside risks of the world economy have intensified, the uncertain factors of instability have increased significantly, and the pressure on China to prevent the epidemic has been increasing, and the resumption of work and production and economic and social development are facing new difficulties and challenges.

2. [national Bureau of Statistics: national fixed investment fell 16.1% in the first quarter compared with the same period last year] from January to March, national fixed asset investment (excluding farmers) was 8.4145 trillion yuan, down 16.1% from the same period last year, a decrease of 8.4 percentage points from January to February. In terms of month-on-month rate, fixed asset investment (excluding farmers) increased by 6.05% in March.

In the tertiary sector, infrastructure investment (excluding electricity, heat, gas and water production and supply) fell 19.7% from a year earlier, down 10.6 percentage points from January to February. Of this total, investment in the water conservancy management industry fell by 13.6%, a decrease of 14.9 percentage points; investment in the public facilities management industry fell by 20.5%, a decrease of 11.6 percentage points; investment in the road transport industry fell by 17.5%, a decrease of 11.4 percentage points; and investment in the railway transport industry fell by 28.6%, a decrease of 3.1 percentage points.

3. [national Bureau of Statistics: investment in China's Real Estate Development fell by-7.7% in the first quarter from a year earlier]

From January to March, investment in real estate development across the country totaled 2.1963 trillion yuan, down 7.7 percent from a year earlier, down 8.6 percentage points from January to February. Of this total, residential investment totaled 1.6015 trillion yuan, down 7.2 percent, or 8.8 percent. From January to March, the housing construction area of real estate development enterprises was 7.17886 billion square meters, up 2.6 percent from the same period last year, down 0.3 percentage points from January to February. Among them, the residential construction area was 5.04616 billion square meters, an increase of 4.1 percent. The new housing construction area was 282.03 million square meters, down 27.2 percent, or 17.7 percent. Of this total, the new residential construction area was 207.99 million square meters, down 26.9 percent. The completed housing area was 155.57 million square meters, down 15.8 percent, or 7.1 percent less. Of this total, the completed residential area was 109.28 million square meters, down 16.2 percent.

Macroeconomic data are intuitively shown in the table

Note: macroeconomic data GDP fell to negative market expectations, real estate market data in line with expectations. Overall interpretation, do not use chicken feathers as a sword! Counter-cyclical regulation runs on the road. No, no.

4. As of April 17, iron ore stocks at 35 ports were 108.14 million tons, down 300000 tons from the previous week and 20.55 million tons from the same period last year, according to SMM. The volume of dredging on Sunday rose slightly from the previous week by 24000 tons to 2.749 million tons. The inventory of the two ports in Tangshan area increased slightly month-on-month, mainly due to the recent arrival of ships and a small increase in the number of open ports; among them, the Beijing-Tangshan port due to individual low products and the shortage of Brazilian resources tradable minerals, resulting in a low volume of port opening. Some steel enterprises turned to increase Caofeidian port procurement, Caofeidian port daily average open port continued to pick up. The main port radiation steel enterprises in Shandong continue to purchase a small amount of on-demand procurement strategy, the overall daily average of port opening decreased, at the same time, due to the reduction of shipments to Shandong in the first ten days, port inventory decreased month-on-month. In view of the fact that the demand side is stable and improving in the near future, the daily average opening of the port iron ore may be expected to increase slightly. [SMM Steel]

5. Hanging mirrors judge supply and demand!

(1) on the demand side: demand for steel and silver samples reached 4.75 million tons on Thursday. There are three worries or doubts in the market: first, steel traders feel that goods are not easy to sell, second, terminal demand hoarding, recessive explicit, and third, speculative demand comes into the market a lot. The author believes that do not worry about the ancients! What about the shutter? There is no speculative demand in the month-on-month peak season? Is demand this good compared to the peak season? At the same time, whenever the recent steel fall, can maintain 220000 tons of rebar trading volume, such trading volume accounted for speculative demand? There is no denying that there is terminal demand from the end of February to early March, and the virtual table of food should be removed from the social library in advance, but at the same time, should we not consider that there is a quantitative inventory of terminal demand in normal times (without the impact of the epidemic)? This is naked care for one thing and the other! In short, the author believes that the return period of demand is not only indisputable, but also should think about the return period of rush demand!

(2) supply side: on Thursday, the total output of the five major varieties reached 10.12 million tons, the output of rebar was 3.435 million tons, and the peak output in 2019 was 1107 and 3.815 million tons of rebar (see Table 2 for details). The operating rate of long process is about 81%, and that of independent arc furnace steel plant is 70%. Driven by profits, there is no doubt that output is expanding, but it is not far from the peak! It is expected that it will take another two weeks (early May), and it can be seen that the expansion of production is predictable and limited.

(3) the expectation of replenishing inventory before May Day in the market, the author does not agree, the market inventory is still high face, why not worry about buying goods? At the same time, there is a disturbance of weather factors in late April!

(4) despite the acceleration of destockpiling, there is still some way to go before the peak of the impact of the epidemic. What is the driving force for a sharp rebound?.

(5) deduced from the supply side, the high demand for raw materials remains for about 2 weeks, and how long can the long story of iron ore be told. No, no. The author's mid-term point of view remains unchanged, the epidemic affects the demand for stone more brilliantly. No, no.

To sum up, steel prices continue to rebound difficult to continue, from late April to early May to save the probability of the last decline in the second quarter!

The rest of the logic remains the same, do not repeat!

6. Keep an eye on overseas outbreaks.

< 5 > prospects for the steel market in the second quarter.

I. Prediction of macro prospects at home and abroad

Domestic macro vision:

First, the epidemic gentleman mistakenly hit the Yellow Crane Tower, counter-cyclical adjustment accelerated.

During the period from the outbreak of the Yellow Crane Tower to the pre-outbreak of the overseas epidemic, the domestic counter-cyclical regulatory factors increased and accelerated, mainly including and not limited to the new infrastructure, tax reduction, reduction of accuracy and other policy incentives to counter epidemic injury and the "six stable" target tasks, even after the "two sessions", because of the overseas epidemic outbreak "six stable" national policy to a certain extent, there is a correction probability, but considering the role of inertia and lag, the second quarter can and must be reflected. That is, strong expectations will be fulfilled in the second quarter.

Second, there is uncertainty in China's monetary policy in the later period.

In order to rescue the current liquidity crisis in the market, and in response to possible economic turmoil, the Fed has launched an unlimited, bottomless QE monetary easing stimulus. There is no doubt that all non-US countries have paid for it, and no matter what measures they take, imported inflation is doomed.

In the short term, stimulated by the Fed's unlimited easing program, suspended the liquidity crisis, calmed the market sentiment is effective, U. S. stocks rebounded sharply.

In the medium term, the main contradiction of the US Emperor is the epidemic situation. At the beginning of the epidemic, there is uncertainty about the extent to which the epidemic has deteriorated, and this year's recession is deterministic. The recession began with an epidemic. Consumers had to spend less because of the epidemic, and producers had to shut down because of the epidemic. Enterprises can not produce normally because of the impact of the epidemic, at the same time, they have to face a sharp reduction in orders brought about by shrinking consumption in the future. Many enterprises will have to face the risk of bankruptcy because of the cash flow crisis caused by the sharp decline in income, and the resulting rising unemployment rate will aggravate the economic recession. These economic activities, the Fed injection of liquidity to promote the role is very limited.

Bet all the money on the bottom of the deposit box on the gambling epidemic! Premature excessive consumption of policy space, what if the epidemic gets out of control? Can the trick of sucking blood and non-American people's sweat in 2008 come true again? Let's see.

In the long run, the great change in the world pattern is deterministic, but who is in charge of uncertainty!

Looking at the great China, China's monetary policy is facing a big test again! Is it possible to follow in the footsteps of the non-US developed economies and follow the old path of 2008? Or are you sure to move on? Or is the "six stable national policy" adjusted to "protect finance and employment"?. No, no. Test the wisdom of decision makers again! In short, hard wounds can not escape! After the "two sessions", the monetary policy of a great country is full of uncertainty, and the market is now strongly expected to cut interest rates in April. The G20 meeting delivered 35 trillion yuan in monetary stimulus to deal with the epidemic and hedge against the global recession! Listen to his words and observe his deeds. The author foolishly believes that if the water release of Chinese currency can stop in the direction of world epidemic control and "Belt and Road", that is, to implement a community with a shared future for mankind, and to export inflation to the United States. It's not beautiful! The Federal Reserve needs China to prepare for the policy response to the imported inflation in non-American countries, especially in developing countries, regardless of the consequences of the secondary economic and social disasters brought about by the continuous development of the epidemic.

In short, benevolence sees benevolence and wisdom sees wisdom.

Third: the epidemic sweeps the west wind, how can the secondary disaster endure.

The outbreak period of the overseas epidemic situation, especially the United States Emperor has the tendency to catch up from behind, although the medical level is not moved, but the political and economic interests override the rest of the world.

Above, there is no suspense on the European and American epidemic Cup champion podium! For the good is the happiest, for the evil can not escape. A long way of good reincarnation, the vast sky spared who! Coronavirus is the common enemy of mankind at present, the practice of a community with a shared future for mankind is the truth, and the control of the epidemic bean base is the essential work of the United States, and it is also the concrete practice of being responsible to mankind. The United States not only does not face up to the main contradiction of the epidemic bean base, but gives priority to opening up an unlimited easing policy! If you hurt an "enemy" by 1000, you will injure yourself by 800. The Great Recession and the Great Depression are doomed! Similarly, overseas outbreaks have caused secondary disasters in China. There is no doubt that imports and exports shrank greatly in the second and third quarters.

Fourth: the story of farmers and snakes should not be forgotten.

During the period of the Yellow Crane Tower wearing a cover to fight the epidemic, the United States Emperor etiquette and shame, four-dimensional atelectasis. Many senior officials and dignitaries of the US imperialist government are afraid that China will not be disorderly and gloat, hoping that the epidemic will deal a fatal blow to China's economy and geopolitics, constantly attack and stigmatize the Chinese virus, and engage in political "epidemic poison." through the so-called "Taipei Act," the Senate and the House of Representatives have colluded with the jin Party of the people of Taiwan, colluded, grossly interfered in China's internal affairs and continued to escalate, and the media unscrupulously publicized false information by using a powerful network platform. Militarily, show off your muscles and make threats on the doorstep of China. No, no. It's hard to tell!

After the epidemic, the US Emperor further contained Greater China in an all-round way, and it was by no means alarmist! Chairman Mao's quotation: the United States imperialism will not die, we must always raise the police!

II. Prediction of the fundamentals of the Iron and Steel Industry

1. Der Spiegel is a high judge of supply and demand.

Supply side.

At present, the profit of long-process tonnage steel is 300-400, and some of the original long-process shutdown and maintenance are gradually resuming, even if the steel enterprises shut down by the epidemic in Hubei Province will resume production no later than mid-April. Independent electric arc furnace steel mills lose less than 100 yuan or even some of the steel enterprises that enjoy tax rebates and enjoy local government subsidies due to the downward movement of scrap prices. No, no. It can be determined that production in April has become normal.

Quantitative valuation: 6800 / 700 = 75 million tons

The long process output is 7.11 × 1.1 / 80 / 92 / 6.800, that is, 68 million tons.

The capacity utilization rate of independent electric arc furnace is 70%, 7 million tons.

The demand side.

Throughout the table trading volume in late March and eliminate speculative false demand, and combined with including but not limited to cement prices, concrete mixing stations, pipe pile demand, PC steel bar prices verify each other, and then peep at the start of real estate and steel net export trade considerations. The return period of qualitative demand in April is about 95% of the normal.

Quantitative valuation: 6966 tons 350 = 73.16 million tons

Domestic apparent demand: 7333mm 0.956966 (ten thousand tons)

Net exports are estimated at 3.5 million tons.

The relationship between supply and demand is broadly consistent.

2. Solution of towering floating Cloud in inventory

Seek proof according to the inertia of thinking:

The total inventory of five varieties is 35 million tons, and the total stock of rebar is 19.5 million tons. Even if the data in the table are objective and practical, the maximum inflection point of perennial inventory is still higher than about 10 million tons. Absolute high section of the inventory to the perennial inflection point value at least a month, steel price rebound road is a long way to go!

Reverse thinking:

One is: precisely because the inventory is towering and floating clouds, there is now "land price" steel.

The second is: the steel mill price is determined, with the time dimension for the space dimension.

Third: the so-called inventory towering clouds, just used to the concept, get used to it! Inventory is only a static index of the relationship between supply and demand, and the essence of price is determined by the relationship between supply and demand.

3. The epidemic caused the absence of demand, there is no doubt to rush to make up for classes.

4. There is a high probability of retrograde strength along the Belt and Road.

To sum up, steel prices in April are still negative walking, the upper and lower driving forces are limited, in May into the ready stage, June is expected!