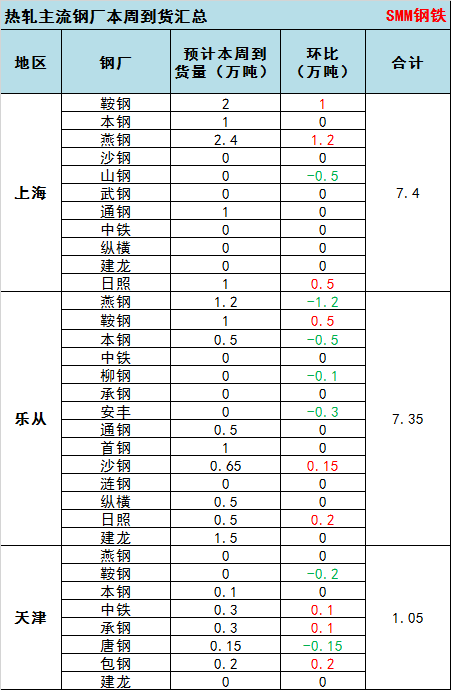

As can be seen from the above table, the overall arrival volume of hot rolling mainstream steel mills this week is 158000 tons, an increase of 10, 000 tons over the previous month, of which: Shanghai market: 74000 tons of resources arrived this week, + 22000 tons month-on-month. Mainly because, in order to avoid the port restrictions during the Expo, the steel mill resources shipment has been adjusted, resulting in some resources arrived in the market ahead of time, but the total amount of the overall long Association resources has not changed. Among them, the main resources are Yanshan Iron and Steel Co., Ltd. And Angang. Recently, with the arrival of low-cost imports of resources, the market bearish sentiment continues, resulting in continued weak demand in the near future. Therefore, this week's increase in resources will undoubtedly cause greater pressure on the fundamentals of supply and demand in the current market, resulting in spot prices still have downside risks. However, there is no need to panic that next week, as Import Expo approaches, the ports around Shanghai will enter the state of restricted port berthing, and landing vessels will be prohibited from unloading, so it is expected that there will be a significant reduction in the arrival of resources next week, when the market will speed up the digestion of inventories. Fundamental pressure will ease compared with this week. Lecong market: 73500 tons of resources arrived this week, month-on-month-12500 tons. Since the second week after National Day, the continued decline in the arrival of resources in the market, coupled with overall demand relative to other regional preferences, so the recent fundamental pressure on supply and demand has eased. Among them, the main reason for the reduction in resources this week is still caused by the early northern environmental protection and production restrictions, and the reduction steel mills are mainly Yangang, Anfeng and Benxi Iron and Steel Co., Ltd. However, it is still worth noting that the spot price in the market is still high (the price difference between Lecong and Shanghai is about 100 yuan / ton), and the heat released by steel mills is not reduced. The following weather is getting colder and the northern resources are moving south one after another, then the supply pressure in the market will continue to increase. At the same time, the peak season is gradually fading, demand is relatively falling, so it is expected that the subsequent contradiction between supply and demand in the market will further increase, spot prices may fall with it.

Tianjin market: resources arrived at 1.05 this week, basically flat on a month-on-month basis. The overall supply and demand fundamentals are more stable, and the spot price is more resilient than other markets.

Overall, although the recent mainstream market supply and demand fundamentals pressure to alleviate the degree of differentiation, but the overall supply is greater than the demand pattern has not changed. In addition, some steel mills will put in new production capacity in November (Shenglong Metallurgical 1780mm hot rolling line will be put into production in early November), and foreign import resources will arrive in the market one after another, when the market supply pressure will further increase and spot price pressure will intensify.