Summary of basic Metal production in China in April 2019

Electrolytic copper:

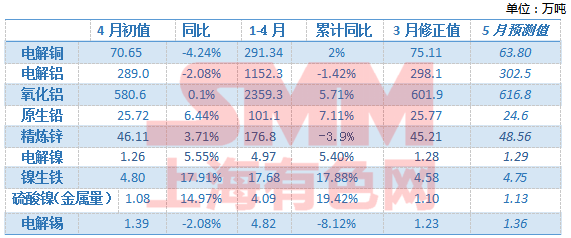

In April 2019, SMM China's electrolytic copper production was 706500 tons, down 5.94 percent from the previous month, down 4.24 percent from the same period last year, and the cumulative output from January to April was 2.9134 million tons, an increase of 2 percent over the same period last year.

The output in April was slightly higher than the previous forecast, mainly due to the fact that the actual output in April in Yanggu Xiangguang, Jinchuan, Guangxi and Dongying was higher than the original plan. The production of electrolytic copper in Guangxi Nanguo Copper Industry, which was officially fed in April, is still very limited, and the complete production time of Chinalco Ningde has also moved backward. In addition, the interference with the output in the second quarter basically comes from the maintenance of major refineries. In the face of the sharp decline of spot copper concentrate TC, some small and medium-sized smelters with low proportion of long single began to say that the production pressure is greater. Production at the reclaimed copper smelter in operation was normal in April, but there were concerns that scrap copper was tightening raw materials because of import restrictions, while the approval of the "six" import scrap copper license was not yet clear, and there were risks in importing scrap copper.

SMM research shows that most smelters will be affected by maintenance in May, and the output will be significantly reduced. A large smelter in Shandong plans to have no output in May. In May, the smelters whose output was damaged by maintenance mainly came from the West Mine Qinghai Copper Industry, the Central Plains Gold smelter, Dongying Fangyuan, Shandong Jinsheng, Yanggu Xiangguang, Yuguang Gold lead and so on. The overall impact is much higher than in April, which may also be the most concentrated month in 2019, according to SMM's current updated maintenance schedule. According to the production schedule in May, China's electrolytic copper production in May will be significantly reduced by nearly 70, 000 tons from the previous month to 638000 tons, a decrease of 14.63 percent from January to May. The cumulative output from January to May reached 3.5514 million tons, a cumulative decrease of 1.45 percent.

Alumina:

According to SMM data, China's alumina (metallurgical grade) production in April (30 days) was 5.806 million tons, an increase of 0.1 percent over the same period last year, with an annualized operating capacity of 70.6397 million tons and an average daily output of 194000 tons, which was basically the same as in March.

From January to April, China's alumina production totaled 23.593 million tons, an increase of 5.71 per cent over the same period last year. The alumina production in April was not as expected, and the main variable was that the environmental protection technical transformation in Weiqiao, Shandong Province, had affected some of the production capacity. The discharge quality of alumina from the Shuijiang River in Nanchuan, Boxi, was still unstable, and Sanmenxia hoped that the operating capacity would be reduced to about 2.1 million tons. Chinalco mining industry due to losses reduced production of 1 million tons, Shanxi Fusheng and Inner Mongolia Xinwang maintenance also affected some of the production capacity and so on.

China's alumina production in May (31 days) is expected to be 6.168 million tons, an increase of 1.86 percent over the same period last year, with an average daily output of 199000 tons, an increase of 5000 tons from the previous month. In May, it is expected that the production capacity will be relatively stable, the previous production capacity reduction, such as Shanxi Huaxing Aluminum also raised operating capacity expectations, while March-April due to environmental protection and technical transformation of the impact of production capacity will be partially released. But Guangxi Xinfa stopped another 600000-ton production line in May, with an operating capacity of between 180 and 1.9 million tons.

Electrolytic aluminum:

China produced 2.89 million tons of electrolytic aluminum in April, down 2.08 per cent from a year earlier, according to SMM data.

From January to April, the total domestic electrolytic aluminum production was 11.523 million tons, down 1.42 percent from the same period last year. The first four months of 2019 continued to be affected by the loss and reduction of production by electrolytic aluminum enterprises from June 2018 to February 2019. as a result, the scale of operating capacity remained relatively low. Although some of the production capacity has gradually returned to production since April, its contribution to the overall output in April is limited. At the end of April, the domestic electrolytic aluminum operation capacity was 36.23 million tons, and the average starting rate of the industry was 88.8%, 0.3 percentage points higher than that at the end of March. After May (31 days), the contribution of compound production to yield increased gradually.

The output of electrolytic aluminum is expected to be 3.025 million tons in May, down 1.56 percent from the same period last year, and the reduction in output growth rate is narrowed. Under the steady situation of consumption, the level of domestic electrolytic aluminum inventory is expected to drop to about 1.3 million tons by the end of May.

Primary lead

In April 2019, China's primary lead production was 257200 tons, down 0.2 percent from the previous month and up 6.44 percent from the same period last year. From January to April 2019, primary lead production was 1.014 million tons, up 7.11 per cent from a year earlier.

According to SMM research, in April, among the primary lead smelting enterprises, Anhui Tongguan, Yunnan Chihong, Jiangxi Copper and other enterprises entered and overhauled, while Xinling, Henan Province, resumed after overhauling, while the production of most other refineries remained basically normal. The month's primary lead production fell by only about 500 tons from March, in line with expectations of a slight decline in the previous report.

Compared with April 2018, the production of primary lead continued to increase in April this year, mainly due to the concentrated maintenance of smelting enterprises in the same period last year, and most of them were overhauled (all production lines), with a longer impact time (from March to April). Although there are repairs in April this year, but most of them are minor maintenance (part of the production line), the impact time is still short (starting from April 20).

Looking forward to May, according to SMM, Anhui Tongguan and Jiangxi Copper Industry have not fully recovered their full production in May after they were overhauled in April, while Henan Yuguang, Hunan Jingui and the south of Hechi have entered and overhauled one after another. During this period, Yunnan Chihong overhauled and repaired the impact on production in May, so SMM expects the production of primary lead to decline by more than 10,000 tons to 246000 tons in May.

Refined zinc:

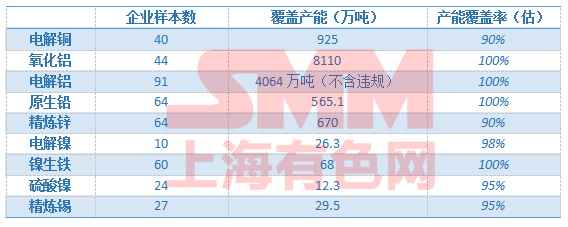

In April 2019, SMM China produced 461100 tons of refined zinc, an increase of 1.99 percent over the previous month and an increase of 3.71 percent over the same period last year. The SMM survey sample has a production capacity of 6.085 million tons.

In April, the processing fee of domestic zinc concentrate continued at an all-time high level, which continued to stimulate the enthusiasm of refineries. The increase in output is mainly from Hunan: among them, the output of the first system of Zhuzhou smelter has increased significantly to 10,000 tons; the production of Sanli Group has fully recovered and the output has increased; Xuanghua has also begun to resume work recently, and the contribution of Hunan is mainly incremental. Some refineries in other areas, such as Gansu and Liaoning, have entered the state of routine maintenance, reducing the increase in national output.

In May, although some enterprises in Qinghai and Yunnan still added some repairs, the output of Hanzhong zinc industry increased, silver nonferrous maintenance recovered, and some refineries also increased their output slightly under the stimulation of profits in some refineries.

Overall, according to the refinery production plan for May, domestic refined zinc production is expected to increase by 24500 tons to 485600 tons in May from a month earlier, an increase of 14.75 per cent from a year earlier and 5.3 per cent from a month earlier. The cumulative output of the refinery is expected to fall only slightly by 0.41% from January to April compared with the same period last year.

Electrolytic nickel:

In April 2019, the national natural monthly output of electrolytic nickel was 12600 tons, an increase of 5.55 per cent over the same period last year. In April, the national electrolytic nickel production decreased by 2% compared with March. The production of electrolytic nickel remained normal in April, and the slight decline in production was mainly due to the decrease in natural days. According to a preliminary investigation by SMM, electrolytic nickel production continued to stabilize in May, with production rising by about 2.6 per cent from April to 12900 tons, also due to the increase in natural days.

Nickel pig iron:

In April, the national nickel pig iron increased by 4.64 per cent to 48000 nickel tons, an increase of 17.91 per cent over the same period last year.

In terms of taste, the output of high nickel pig iron increased by 3.20% to 41700 nickel tons in April compared with March, mainly due to the increase in new production of large nickel pig iron plants in Shandong Province. Low nickel pig iron production increased by 15.17 per cent to 6300 nickel tons in April from a month earlier, mainly due to the continued release of low nickel pig iron production from the Southern Steel Plant.

In May, the national nickel pig iron production is expected to decrease by 0.88% to 47500 nickel tons compared with the previous month, of which the high nickel pig iron production decreased by 1.36% to 41100 nickel tons, mainly due to factory maintenance in East China, South China and North China. The production of low nickel pig iron increased by 2.29 per cent to 6400 nickel tons over April, mainly due to the end of maintenance at the North Steel Plant.

Nickel sulfate:

In April, China produced 10813 tons of nickel sulfate and 49200 tons in kind, down 1.4 percent from the previous month and up 14.97 percent from the same period last year. On the one hand, production at a nickel sulfate plant in the north has been affected this month and production has declined; on the other hand, production has been reduced due to tight supply of raw materials, high prices and meagre profits in some small factories. However, the production capacity of the precursor integration plant continued to climb, and the increased production made up for some of the reduction. The national nickel sulfate production may increase in May, an increase of 4.17% from the previous month, mainly due to the continued increase in the output of nickel sulfate plants with new production capacity and the resumption of production in the northern plants.

Refined tin:

Refined tin production in April was 13911 tons, up 13.4 per cent from March.

The output of the domestic mainstream smelter was stable in April, and Huaxi Company resumed normal production in April, contributing to the output growth. Jiangxi Province suspended production in the early stage due to equipment maintenance, and basically returned to normal production in April. In addition, the output of some tin factories increased steadily and moderately. Although the production of domestic tin factories has been basically stable recently, the import of tin mines in WA State was suspended for about a week due to traffic control in April, and the stock of raw materials in some smelters accelerated down. In addition, the recent reduction in concentrate processing fees will slightly reduce the production enthusiasm of the smelter, which may affect the production of tin ingots in May, and the domestic refined tin production is expected to be slightly reduced to 13600 tons in May.

Description:

Research methodology:

SMM production survey is conducted by professional analysts by telephone, field research and other methods, regular monthly tracking of Chinese metal production enterprises, and based on this to issue a report on China's metal production.

In the process of research, ensure the basic coverage ratio of the sample, and continue to expand; at the same time, consider the production capacity scale, regional distribution, enterprise nature and other detailed factors to reasonably select and distribute the sample, so that each itemized data is representative.

The production data include last month's output (initial value), the previous month's output (revised value) and the forecast for the current month's production. In general, SMM rarely modifies the output, that is, the correction value = the initial value, but still retains the possibility of correction.

On the 10th of each month, it was released through the official website of Shanghai Color Network (www.smm.cn), WeChat Subscription account (Today Colored), mobile phone station (m.smm.cn) and other official channels.

"[Note] with the advent of brainstorming, many bigwigs interpret the hot spots in the metal market!

"Click to enter the registration page

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business