【SMM Analysis】LME Aluminium Prices Hit a Three-Year High in 2025 – Overseas Views on 2026 Outlook

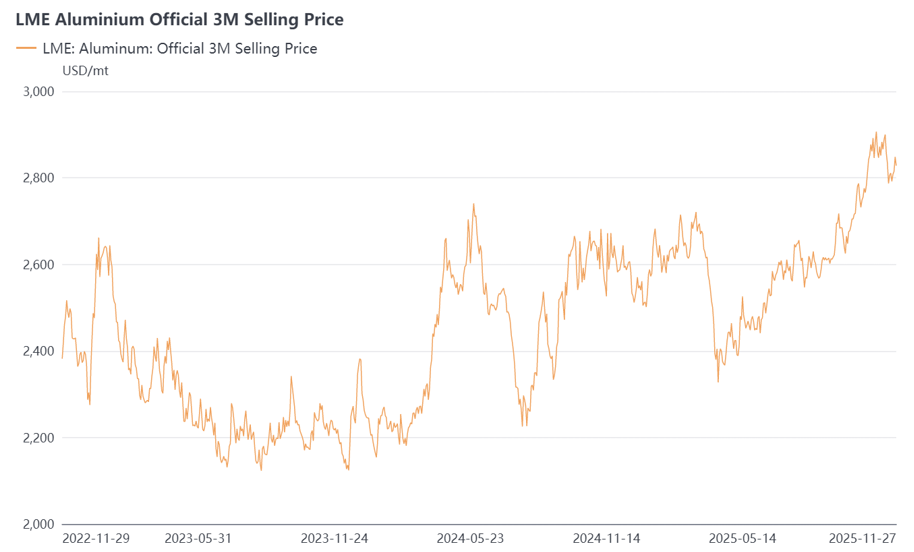

In 2025, LME aluminium prices showed a volatile upward trend. From the beginning of the year to mid-March, prices remained relatively stable, before retreating to around USD 2,400/tonne in late March. After April, the market gradually stabilized and edged higher, until a new round of increases began in late October. By November, aluminium prices were fluctuating in the USD 2,800-2,900/tonne range, marking the highest level since the surge triggered by the Russia–Ukraine conflict in 2022.

As prices continued to rise, demand in several global markets, especially Southeast Asia and India, fell short of expectations even outside traditional off-season periods. Rising prices for aluminium, scrap, and related products suppressed end-user consumption, leaving upstream, midstream, and downstream players caught in a dilemma of “hard to buy, hard to sell.” Against this backdrop, and with the EU’s Carbon Border Adjustment Mechanism (CBAM) set to take effect in 2026, market attention on the trajectory of LME aluminium prices in 2026 has intensified.

According to reports from multiple overseas institutions and SMM research, the main international perspectives on aluminium’s structural outlook can be summarized as follows:

- Primary aluminium supply tightness: China’s output is approaching the 45 million tonne capacity ceiling, creating a structural global shortage.

- Scrap supply under pressure: The EU will implement CBAM in 2026, and scrap export tariffs may be introduced in spring 2026. Policy uncertainty is already affecting global scrap prices and tightening supply.

- Demand-side support remains: Solar, new energy vehicles, construction, and infrastructure continue to drive steady growth in aluminium demand, providing fundamental support.

- High European energy costs: Persistently elevated electricity and natural gas prices in Europe are significantly impacting smelter operating rates and production costs.

- Short-term bullish sentiment: By late 2025 and early 2026, LME aluminium prices may test the USD 3,000/tonne threshold. Many traders and downstream buyers are stockpiling despite high prices.

- High hopes on new production capacities: With new capacity gradually coming online in Indonesia and elsewhere, the tight global supply situation may ease, leading to possible downward adjustments for LME aluminium prices in the later half of 2026.

Summary & Outlook: Finding New Balance Amid Uncertainty

The 2025 aluminium price trajectory has already set the tonne for 2026: high volatility and heightened attention. The aluminium market is at a complex turning point. On one hand, geopolitics, energy transition, and trade policies are reshaping cost structures and supply chains. On the other, strong “green demand” and the reality of supply ceilings form the core contradiction driving price swings.

Looking ahead to 2026, aluminium prices may stage a “breakthrough and return” scenario. In the short term, structural supply bottlenecks and policy uncertainty could push prices toward the USD 3,000/tonne psychological level. However, market mechanisms will eventually take hold, and the gradual release of new capacity in Indonesia and elsewhere is expected to rebalance supply. SMM forecasts a “high first, then lower” pattern, with prices ultimately finding equilibrium in the USD 2,700–2,800/tonne range.

For overseas enterprises, the challenge lies not only in predicting prices but in adapting to an aluminium industry fundamentally reshaped by energy transition and new trade regulations.

![Cast Aluminum Futures Drift Lower, Spot Demand Under Off-Season Pressure [ADC12 Price Daily Review]](https://imgqn.smm.cn/usercenter/KXEYG20251217171725.jpg)