- Macro Engine: Twin Drivers of Economy and Population Fuel Long-Term Steel Demand Growth

India's economy continues to grow at a remarkable pace. According to the latest data, its GDP has surged from $2.84 trillion in 2019 to $3.91 trillion in 2024, a growth rate of 38% over five years, ranking among the fastest-growing major economies globally. Of particular note, India surpassed the UK in 2024 to become the world's fifth-largest economy, marking a significant elevation of its global economic standing. Fueling this economic miracle is its vast population base – reaching 1.451 billion in 2024 – with a distinctly young demographic structure. This "demographic dividend" provides sustained momentum for India's industrialization and urbanization, simultaneously creating a solid foundation for steel consumption.

Delving deeper into steel consumption potential, India's current per capita steel consumption is only about 104 kg. This figure is not only far below China's approximately 600 kg and Japan's roughly 500 kg but also significantly lower than the global average of about 230 kg. This gap reflects both the current state of its industrial development and a definitive space for future demand growth. Given that India is in the mid-stage of industrialization and accelerating urbanization, this disparity is set to translate into strong catch-up momentum, driving sustained growth in steel demand.

- Demand-Side Analysis: Policy-Driven Domestic Demand Boom Creates Diversified Demand Structure

Source: SMM, WSA.

Source: SMM, WSA.

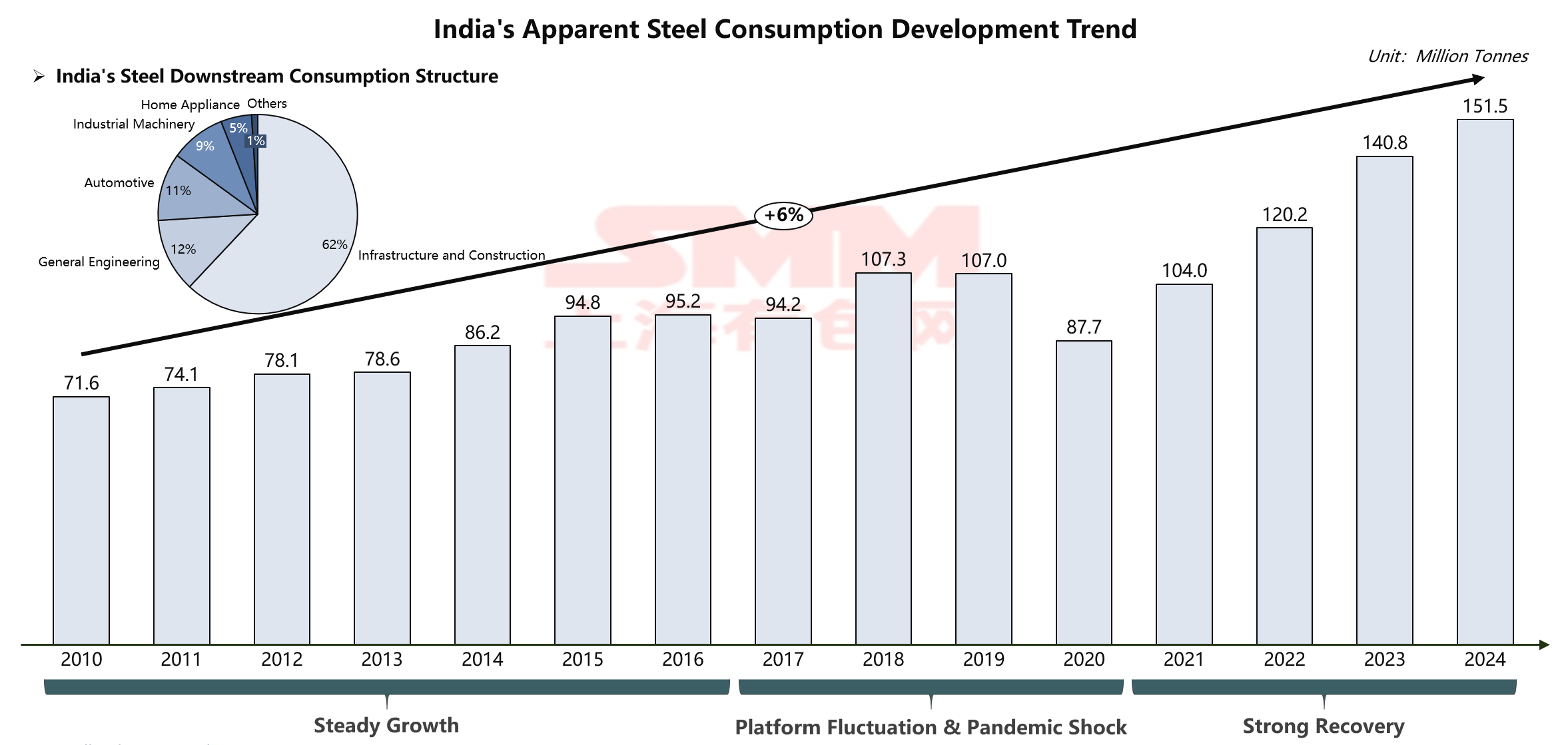

India's steel consumption market is experiencing an unprecedented growth cycle. Consumption surged from 71.6 million tonnes in 2010 to 151.5 million tonnes in 2024, more than doubling. Behind this staggering growth lies a uniquely Indian demand structure – the infrastructure and construction sector uniquely accounts for 62% of consumption, making it the primary engine driving steel demand.

This distinctive consumption structure directly reflects the Indian government's strategic direction. Currently, the government is driving the nation into a new era of infrastructure construction through historic levels of budgetary allocation. Specifically, the 2025-26 fiscal year plans for a record annual infrastructure investment outlay of ₹11.21 trillion (approximately $133 billion). These funds are primarily directed towards key sectors like transportation, energy, and urban development: the Bharat Mala Pariyojana national highway program aims to develop numerous road projects over the next five years; the Urban Development Plan (2024-28) allocates massive funding for metro expansion, housing, and smart cities; concurrently, the modernization of the railway network and the expansion of high-speed rail are progressing rapidly.

Beyond traditional infrastructure, the Indian government is systematically promoting manufacturing upgrades through the Production Linked Incentive (PLI) scheme. This scheme covers 14 key sectors, including specialty steel, electronics, and automobiles, aiming to incentivize domestic manufacturing expansion and exports through subsidies. In the specialty steel segment alone, the first round attracted investment commitments of ₹25 billion from 35 companies; electronics manufacturing, aided by PLI and other policies, is advancing from mobile phone assembly towards high-value component manufacturing. The implementation of these industrial policies not only expands the total steel demand but also continuously optimizes the demand structure, fostering growth in demand for high-end steel products.

- Supply-Side Analysis: Steady Capacity Expansion Faces Structural Challenges, Struggling to Match Demand Growth

Source: SMM, WSA.

Source: SMM, WSA.

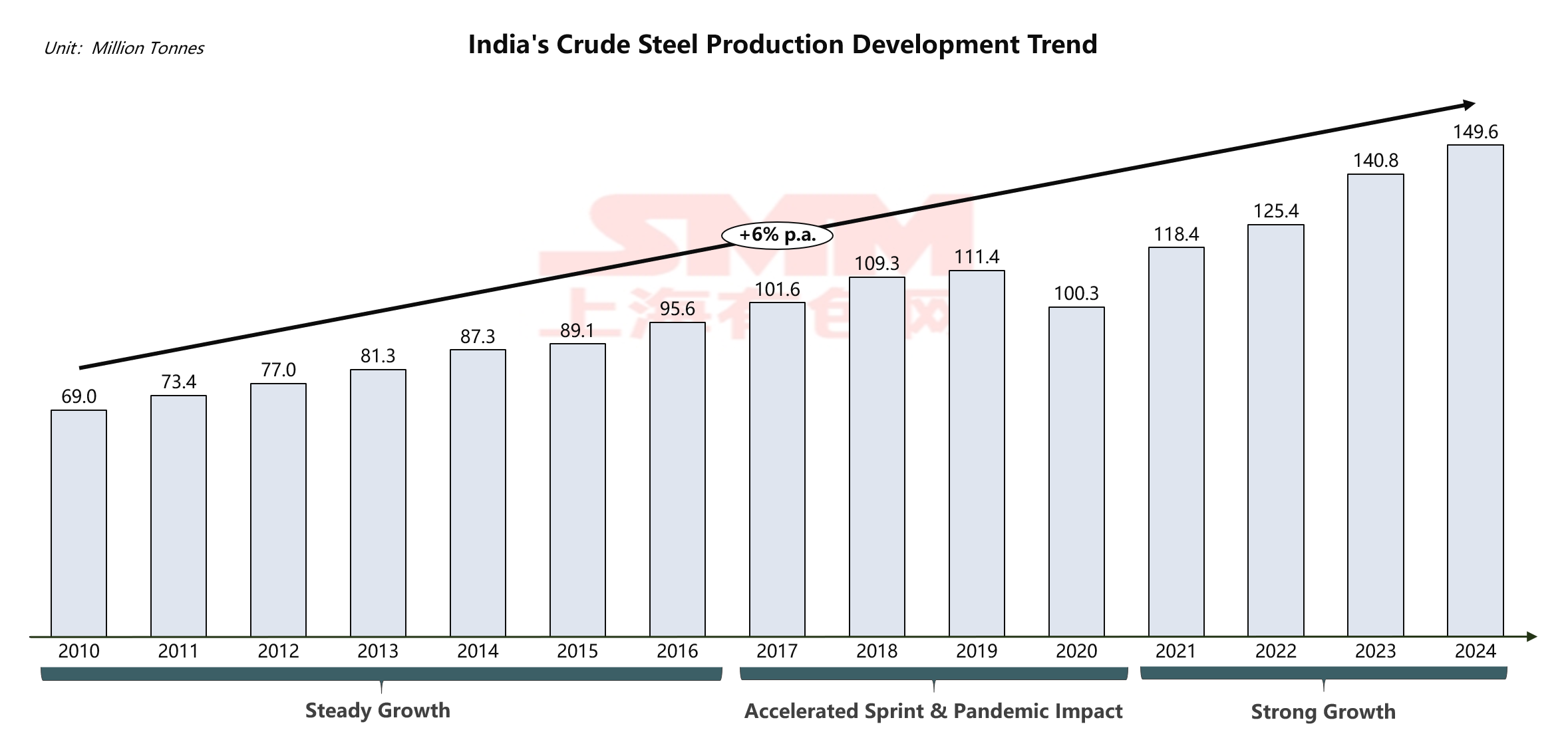

Facing rapidly expanding market demand, India's steel industry demonstrates strong resilience. Its crude steel production grew steadily from 69.0 million tonnes in 2010 to 149.6 million tonnes in 2024, maintaining a stable compound annual growth rate (CAGR) of around 6%. This growth trajectory fully illustrates the vitality and potential of India's steel sector.

High Industry Concentration, Dominated by Major Players

Source: SMM, WSA, GEM.

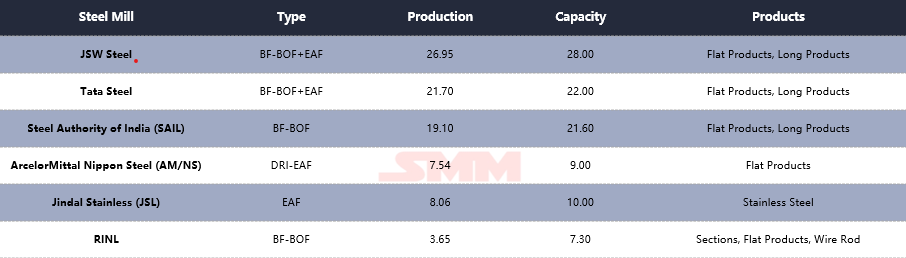

India's steel industry has formed a complete industrial system dominated by a few major players. Among them, JSW Steel leads with an annual production of 26.95 million tonnes, followed closely by Tata Steel at 21.70 million tonnes, and Steel Authority of India Ltd. (SAIL) ranking third at 19.10 million tonnes. These three industry leaders, together with ArcelorMittal Nippon Steel (AM/NS) India, Jindal Stainless (JSL), and others, constitute the core strength of India's steel industry. It is particularly noteworthy that these companies feature diverse technological routes, coexisting from traditional Blast Furnace-Basic Oxygen Furnace (BF-BOF) to more flexible Electric Arc Furnace (EAF) processes, forming a diversified production technology landscape. This technological diversity not only enhances the industry's ability to cope with raw material fluctuations but also provides a process foundation for meeting the precise needs of different market segments.

Geographically, major Indian steel producers show a clear dual-core pattern: the "Eastern Resource Zone" and the "Western Coastal Zone". In the east, Tata Steel, SAIL, and Jindal Stainless have deep roots in traditional steel corridors like Jharkhand and Odisha, establishing production bases leveraging local rich iron ore resources, embodying a typical resource-oriented layout. In the western and southern coastal areas, JSW Steel, AM/NS India, and RINL utilize the advantages of deep-water ports in Gujarat, Karnataka, and Andhra Pradesh to build a market and logistics-oriented layout characterized by importing coking coal and exporting finished steel. This geographical distribution directly shapes India's unique cross-logistics system of "eastward ore transport" and "westward coal transport," profoundly impacting corporate cost structures and indicating that future capacity expansion will continue to concentrate in coastal areas to strengthen strategic control over global resources and markets.

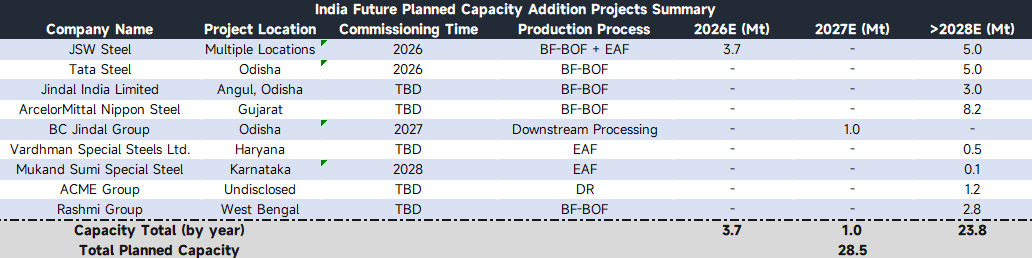

Looking ahead, India's steel industry is ushering in a new cycle of capacity expansion, showing strong market participant confidence in the industry's prospects. According to verifiable capacity plans, major steel enterprises will phase in capacity construction over the coming years. However, due to varying project progress and some plans not yet being finalized, the actual pace of capacity release may exhibit volatile characteristics. This uncertainty in supply growth, coupled with steadily rapid demand growth, is expected to create a persistent supply-demand mismatch in the coming years.

Source: SMM, GEM.

From a product structure perspective, this round of capacity expansion shows a trend towards diversification. Leading companies like Tata Steel and ArcelorMittal Nippon Steel continue to strengthen their presence in high-end flat products and comprehensive steel products, aiming to increase value-added. Simultaneously, investment activity in the specialty steel sector has significantly increased. Companies like Vardhman Special Steels and Mukand Sumi Special Steel focus on niche markets like automotive and engineering special steels, planning to build specialized capacity. In the basic materials sector, BC Jindal Group's cold rolling project and Rashmi Group's long product capacity provide important supplements to meet manufacturing and infrastructure demands.

From a product structure perspective, this round of capacity expansion shows a trend towards diversification. Leading companies like Tata Steel and ArcelorMittal Nippon Steel continue to strengthen their presence in high-end flat products and comprehensive steel products, aiming to increase value-added. Simultaneously, investment activity in the specialty steel sector has significantly increased. Companies like Vardhman Special Steels and Mukand Sumi Special Steel focus on niche markets like automotive and engineering special steels, planning to build specialized capacity. In the basic materials sector, BC Jindal Group's cold rolling project and Rashmi Group's long product capacity provide important supplements to meet manufacturing and infrastructure demands.

It is noteworthy that structural contradictions persist between the current capacity layout and market demand. The construction cycle for high-end capacity is long, making it difficult to alleviate dependence on imported high-end steel in the short term. Meanwhile, some low-to-mid-end capacity, due to product specifications, cost structures, and other factors, has limited alignment with the vast domestic infrastructure demand, leading to the peculiar phenomenon of simultaneous domestic supply gaps and some resources seeking export markets.

From a process technology route perspective, new capacity continues the pattern dominated by BF-BOF supplemented by EAF, reflecting the realistic choice of India's steel industry based on resource conditions. Concurrently, projects for green direct reduced iron (DRI) promoted by companies like ACME Group demonstrate the industry's active exploration towards sustainable development transformation, offering valuable attempts for future low-carbon development paths.

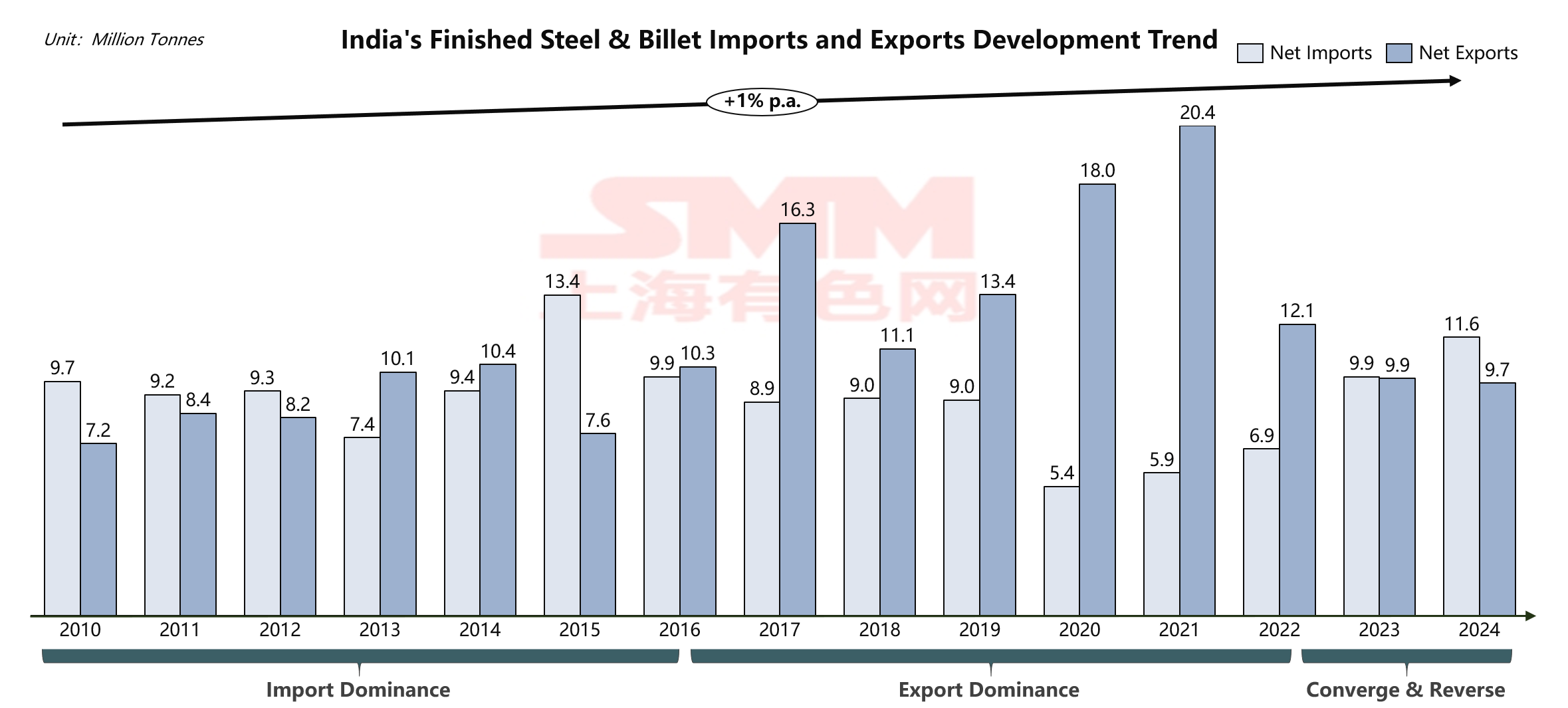

- Trade Dynamics: Strategic Shift from Net Exporter to Net Importer Highlights Structural Industrial Contradictions

Source: SMM, WSA.

Source: SMM, WSA.

India's steel trade balance is undergoing profound structural changes, directly linked to the explosive growth in its domestic apparent steel consumption. In 2024, while achieving a record high of 151.5 million tonnes in apparent steel consumption, India recorded a net import of approximately 1.9 million tonnes, representing only about 1.25% of its total domestic consumption. This indirectly indicates that the vast majority of India's steel demand is still met by domestic capacity, with imports serving merely as a structural supplement. However, recalling 2021-2022, India was a net exporter, with domestic capacity not only fully covering domestic consumption but also having surplus to supply international markets. The shift to a net importer clearly indicates that the growth rate of domestic consumption has significantly outpaced the expansion of domestic capacity, forcing India to seek additional supply from the global market to fill this widening gap.

Source: TradeMap, UNComtrade.

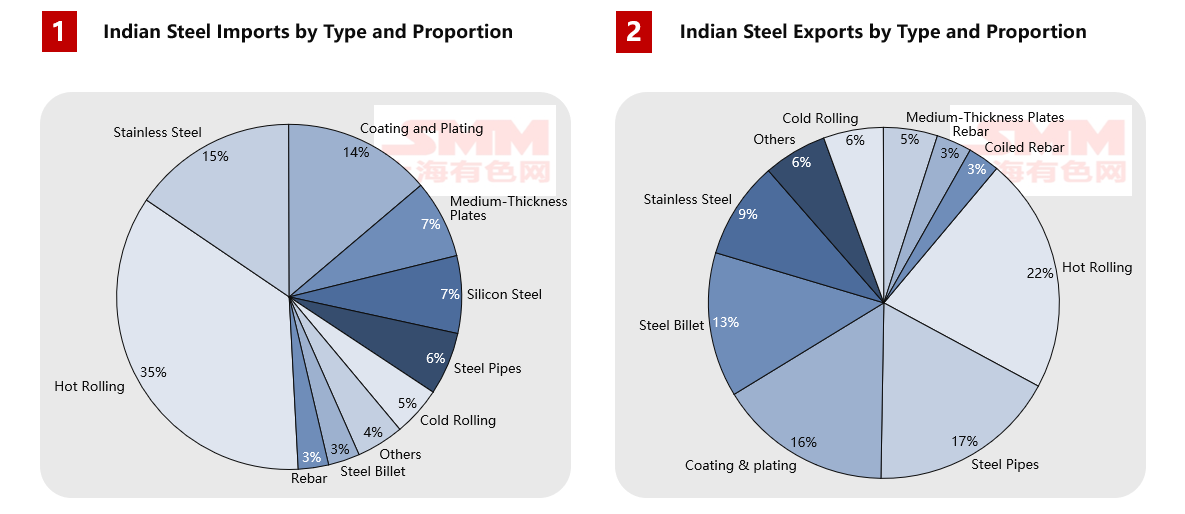

Analyzing the product structure reveals sharper contradictions. India heavily relies on high-end steel products, with annual imports reaching 4.01 million tonnes of hot-rolled products, 1.76 million tonnes of stainless steel, 1.57 million tonnes of coated plates, and 820,000 tonnes of silicon steel, clearly pointing to technological shortcomings in its high-end manufacturing sector. Export products are predominantly semi-finished (like 2.06 million tonnes of hot-rolled coil and 1.26 million tonnes of billets) and low-to-mid-range finished goods, showing a clear pattern of lower-value output. This trade structure deeply reflects the transitional dilemma faced by India's steel industry during its upgrade: high-end capacity is not yet mature enough to support domestic industrial upgrading needs, while low-to-mid-range capacity, although substantial in scale, fails to fully serve the domestic infrastructure and manufacturing base due to differences in profitability between domestic and international markets or product mix issues.

Source: TradeMap, UNComtrade.

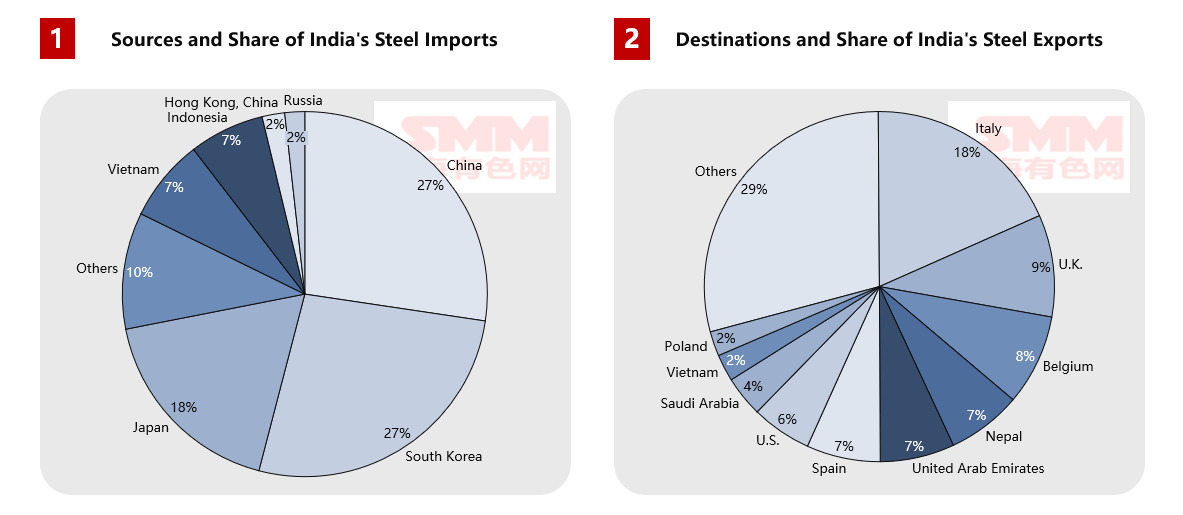

A deeper analysis of geographical trade flows shows that for exports, Italy is the largest destination for Indian steel with 1.75 million tonnes, followed by Belgium, the UK, and other European countries, demonstrating India's cost competitiveness in the low-to-mid-range steel market. Simultaneously, stable exports to neighboring countries like Nepal and the UAE highlight its regional economic advantages. However, import sources are highly concentrated, with China, South Korea, and Japan collectively accounting for 54%, underscoring India's deep dependence on East Asian high-end supply chains during its industrial upgrade. This trade pattern profoundly reflects the true position of India's steel industry in the global value chain: possessing sufficient capacity to meet domestic basic construction needs, yet being strategically constrained in high-end manufacturing.

Notably, to address these structural contradictions, the Indian government has adopted a series of trade policies with clear orientations. On the import restriction front, although the safeguard duties on key flat products like hot-rolled, cold-rolled, and coated sheets have expired, their protective rationale continues through still-effective anti-dumping duties, countervailing duties, and relatively high basic tariffs, collectively raising the import cost of low-to-mid-end steel and creating market space for domestic mills. Meanwhile, maintained anti-dumping and countervailing duties on specific steel pipes and tubes further restrict imports from countries like China and Vietnam.

On the other hand, the exemption for certain stainless-steel products under the closely watched Quality Control Order (QCO) has been extended until March 2026, primarily covering widely used 200 and 300 series stainless steel flat products in construction and manufacturing. This arrangement clearly reflects that India still faces capacity and quality bottlenecks in the high-end steel sector, requiring continued reliance on imports to meet downstream manufacturing needs in the short term. This policy mix has produced a noticeable trade diversion effect:

- Tariff barriers keep the import cost of ordinary steel high, weakening the price competitiveness of mid-range resources from China, Vietnam, etc.

- The QCO exemption maintains market opportunities for high-end steel suppliers with technical and quality advantages, like Japan and South Korea.

- India's steel import structure is shifting from overall "volume" growth to targeted "quality" supplementation.

These policy adjustments echo the domestic supply-demand contradiction: existing capacity cannot fully cover all tiers of domestic demand. High-end products still need to be imported due to technological limitations, while some low-to-mid-end products, under market mechanisms, "circulate selectively" seeking international profits, resulting in domestic demand not being fully met.

- Future Outlook: India's Supply-Demand Balance and Reshaping of the Global Landscape

Based on an in-depth analysis of the fundamentals of India's steel industry, its future trade pattern will present a complex yet clear development path. From short to medium-term, India's steel trade will transition from net imports towards a structural deficit.

The short-term outlook (until 2027) indicates that India will maintain and expand its net import position. This judgment is based on two key factors: firstly, planned capacity projects have not yet formed effective supply, with many current large projects under construction expected to concentrate production only after 2028; secondly, demand growth driven by infrastructure investment will remain strong, especially against the backdrop of continuous advancement major projects like the Bharat Mala National Highway Plan and the Urban Development Plan. During this period, India's import dependence on key varieties like hot-rolled coil, high-end automotive steel, and electrical steel is likely to increase, providing significant market opportunities for global steel exporters.

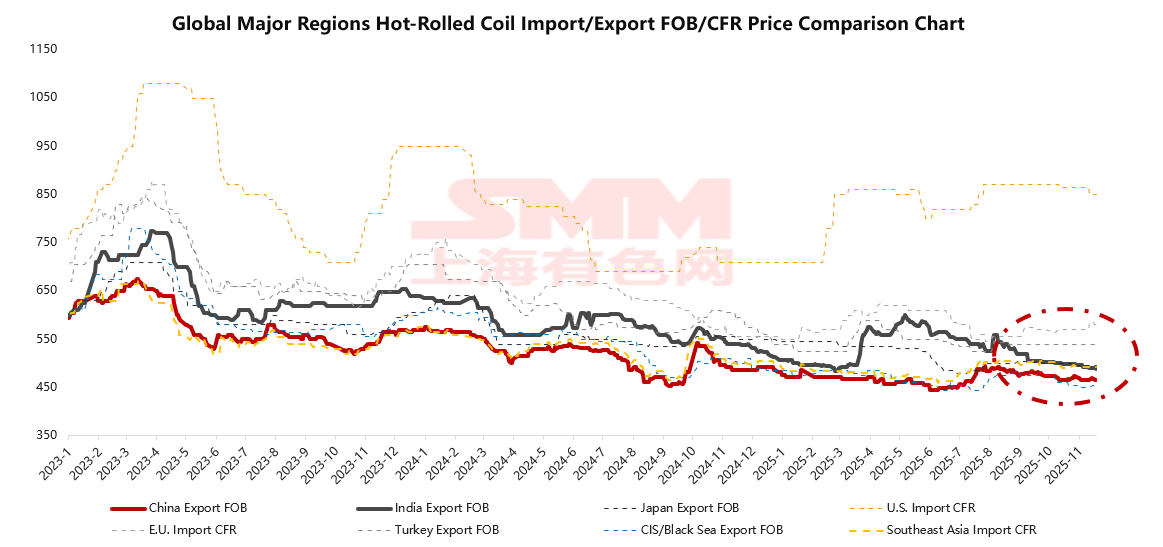

Source: SMM.

Notably, in the current global hot coil market, China, leveraging its complete industrial chain and economies of scale, has FOB offers that remain the lowest globally, setting the market price benchmark. In contrast, India's hot coil export FOB offers are generally $20-40 per tonne higher than China's, mainly due to high dependence on imported coking coal, high domestic logistics and energy costs, and strong domestic demand prompting mills to prioritize the more profitable home market. This price structure creates an inverse relationship between India's hot coil price competitiveness and domestic demand strength – actively exporting when domestic demand cools and withdrawing from the international market when domestic demand is hot.

In the global landscape, Indian hot coil prices sit in the middle tier: lacking cost advantage compared to sanctioned-affected CIS resources, only attractive to Southeast Asian markets when local supply is tight and prices surge, but maintaining some competitiveness for high-cost markets like the EU. This positioning establishes India as a "flexible supplier" rather than a "stable, low-cost source" in global steel trade. Its export behavior exhibits a clear pulsing characteristic, fluctuating with domestic demand.

The medium to long-term outlook reveals that India's steel industry will face the persistent contradiction of "capacity expansion failing to keep pace with demand growth". According to SMM assessment, the 300 million tonnes crude steel capacity target set by India's "National Steel Policy (2017)" is expected to be only about 80% achieved, resulting in actual capacity of approximately 240 million tonnes by 2030. Against this backdrop, if India's steel consumption maintains a 7% average annual growth rate, while crude steel production, constrained by the pace of capacity realization, achieves only about a 5% growth rate, and considering an 85% capacity utilization rate, India's supply-demand gap will continue to widen, with the net import volume projected to reach 25.5 million tonnes by 2030. This trend indicates that the pace of India's steel capacity expansion will consistently struggle to match the robust growth of its domestic demand. Even during the period of concentrated capacity commissioning, its vast domestic market will still need to rely on imports to bridge the supply gap. Simultaneously, in the high-end steel sector, due to gaps in technological accumulation and process levels, India's structural dependence on high-value-added steel will persist long-term, forming a "new normal" of "continuously expanding total gap and difficult-to-improve high-end dependence."

This development trend will profoundly impact the global steel trade landscape in three dimensions: Firstly, India will become the new engine of global steel demand growth, providing a crucial outlet for global steel capacity against the backdrop of plateauing steel consumption in China. Secondly, the continuous expansion of India's domestic low-to-mid-end capacity will intensify direct competition with steel producers in regions like Southeast Asia and the Middle East. Thirdly, under the impetus of industrial policies like the PLI scheme, the enhancement of India's domestic high-end manufacturing capabilities will gradually reshape the global trade pattern for high-end steel.

- India's Steel Industry at a Strategic Turning Point

India stands at a historic turning point in its steel industry development. A robust macroeconomic background, systematic infrastructure development plans, and a continuously releasing demographic dividend have jointly fostered an unprecedentedly prosperous domestic steel market. However, the pace of domestic capacity building and structural upgrades temporarily cannot fully match the explosive growth and rapid evolution of demand. Over the next 5 years, India will solidify its position as a significant net importer of steel globally. SMM estimates that India's net import volume could reach around 1600 million tonnes by 2028. This trend will profoundly affect global steel trade flows, price formation, and capacity configuration. Simultaneously, its massive capacity expansion blueprint and active industrial policies clearly declare: India is not only the world's most important steel consumption market in the coming decade but is also steadily advancing towards the goal of becoming a significant pole in the global steel supply landscape. In summary, India is simultaneously the most critical demand growth engine in the global steel industry, a structural import market still reliant on external supply chains in high-end manufacturing, and a regional competitor continuously expanding in the low-to-mid-range market leveraging cost advantages and supply flexibility.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)