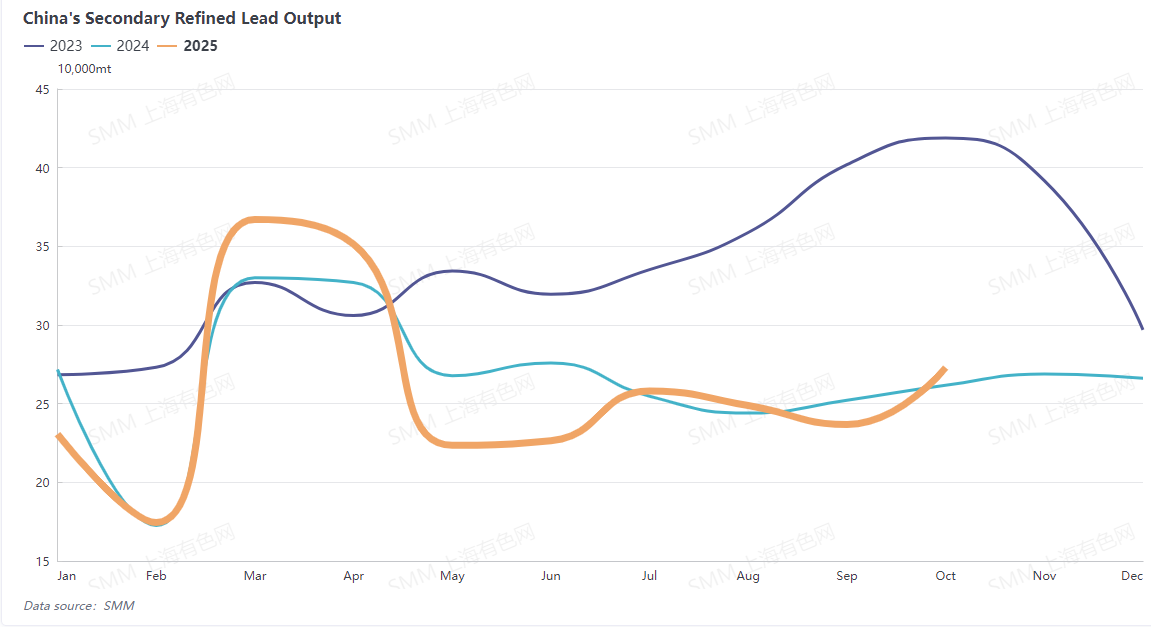

China's secondary lead production in October 2025 increased significantly, up 9.24% MoM and 11.86% YoY; secondary refined lead production rose 15.25% MoM and increased 4.27% YoY.

Lead prices fluctuated upward in October, with SMM #1 lead hitting a near six-month high. Meanwhile, supply in the waste lead-acid battery market remained stable, and prices did not follow the upward trend significantly. With raw material costs stable and lead prices rising, secondary lead smelting profits performed well. The early part of October included the National Day & Mid-Autumn Festival holidays, and most secondary lead smelters scheduled production resumptions for mid-month, with several large smelters in east China and north China resuming production. As secondary refined lead supply showed no significant short-term loosening, coupled with new maintenance at primary lead smelters, lead prices continued to fluctuate at highs. Downstream battery producers were cautious about purchasing at high prices, and some large smelters stopped purchasing lead ingots. Lead prices weakened slightly in late October; during this period, a smelter in east China decided to halt production due to unstable operations over several months, and a smelter in north China stopped for equipment maintenance.

Looking ahead to November, two smelters in east China and north-west China have been baking their furnaces for several days and are expected to officially begin feeding and resume production after entering November. Additionally, newly expanded capacity in north-east China will officially produce lead after coming online. These three enterprises will have a positive impact on refined lead supply in November. The secondary lead industry is undergoing a transformation, with some enterprises shifting their raw materials from solely waste lead-acid batteries to "mainly lead concentrates, supplemented by waste batteries." After the transformation, secondary refined lead production will decline, while primary lead production will increase. Overall, the increases and decreases in secondary refined lead production in November will largely offset each other, with the net increase likely less than 20,000 mt.

Data Source Statement: Except for publicly available information, other data are derived by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.