September, a critical period for the sodium-ion battery industry's push towards mass production, saw differentiated performance across the industry chain segments — production of some materials surged YoY but faced pressure MoM, some segments maintained growth resilience, while mass production bottlenecks, cost pressure, and demand fluctuations remained common challenges for the industry. From cathode and anode to electrolyte and battery cell end-users, operational details and future expectations across segments collectively outline the current development profile of the sodium-ion battery industry.

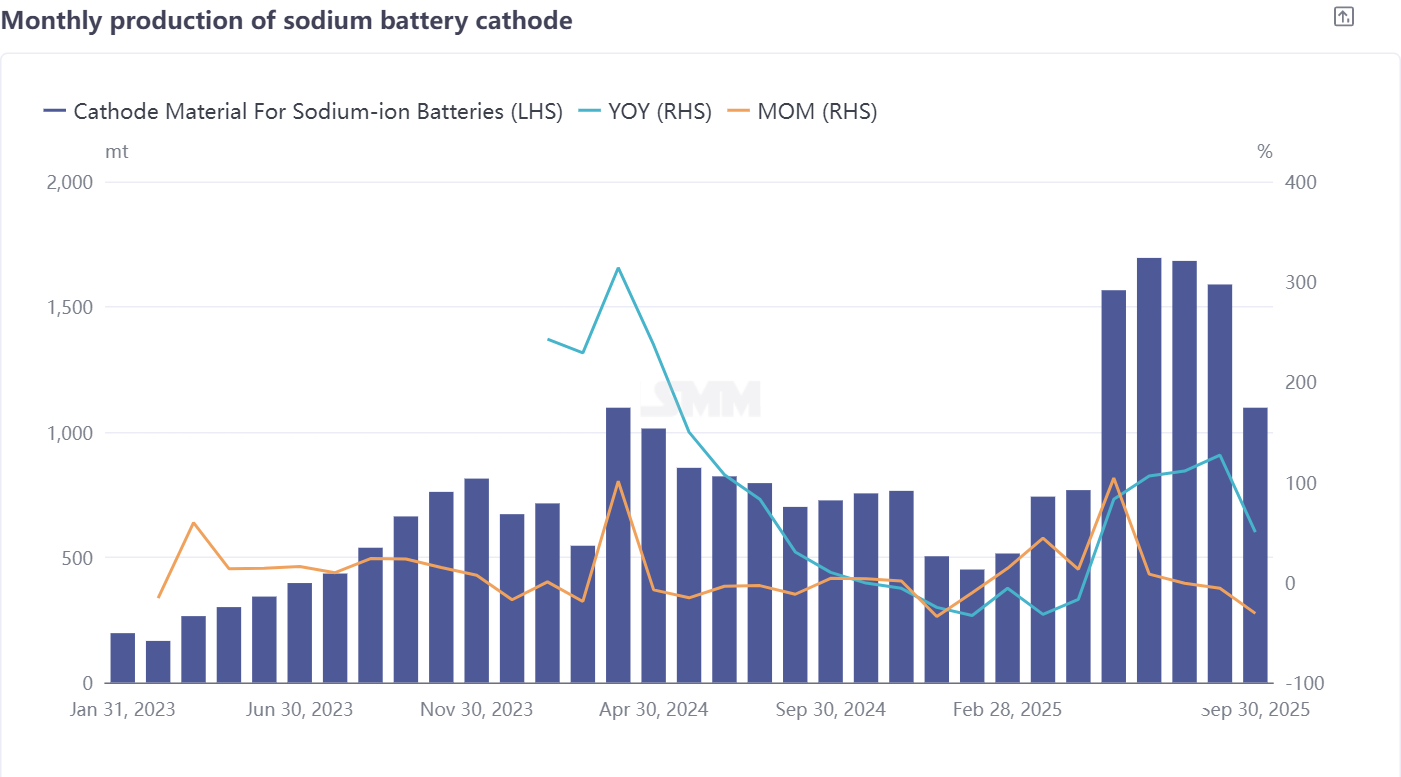

Cathode Material: NFPP Share Increase Fails to Mask Production Decline, Under Pressure from Both Mass Production and ESS

Sodium-ion battery cathode material production in September exhibited characteristics of "high YoY growth, sharp MoM decrease": it decreased significantly by 31% MoM, and although it still showed a 50% increase YoY, underlying industry concerns are gradually emerging. In terms of product structure, polyanion NFPP remained the absolute dominant type, accounting for 69% of total monthly production, with its share increasing by 2 percentage points compared to August; however, in terms of production volume, NFPP decreased by over 300 mt MoM, with supply-demand contradictions directly constraining its scale release.

The core reason lies in the batch shipment and application phase of NFPP before Q3, where some minor potential issues gradually surfaced — upon identifying problems, battery cell manufacturers initiated a series of debugging efforts while reducing cathode procurement volume, directly leading to a significant drop in orders for NFPP cathode enterprises. Furthermore, constrained by factors such as high production line construction costs, some NFPP enterprises were forced to postpone mass production plans, further exacerbating production instability in recent months. Notably, development of the layered oxide O3 route is even more sluggish, with some enterprises gradually abandoning this technical direction, leading to further concentration in cathode material technology routes.

From the downstream application perspective, the promotion of sodium-ion battery ESS projects in H2 of this year has fallen short of expectations, with the number of mandatory demonstration projects significantly reduced compared to the same period last year, while the cost advantage of lithium battery ESS remains a core challenge that sodium-ion battery ESS cannot easily circumvent. Overall assessment suggests NFPP production is still unlikely to achieve a good recovery in October, with its recovery pace highly dependent on the actual adjustment and improvement efficiency of downstream battery cell manufacturers; broadly, sodium-ion battery cathode material production in October is expected to increase by 3% MoM, with the YoY growth rate narrowing to 49%.

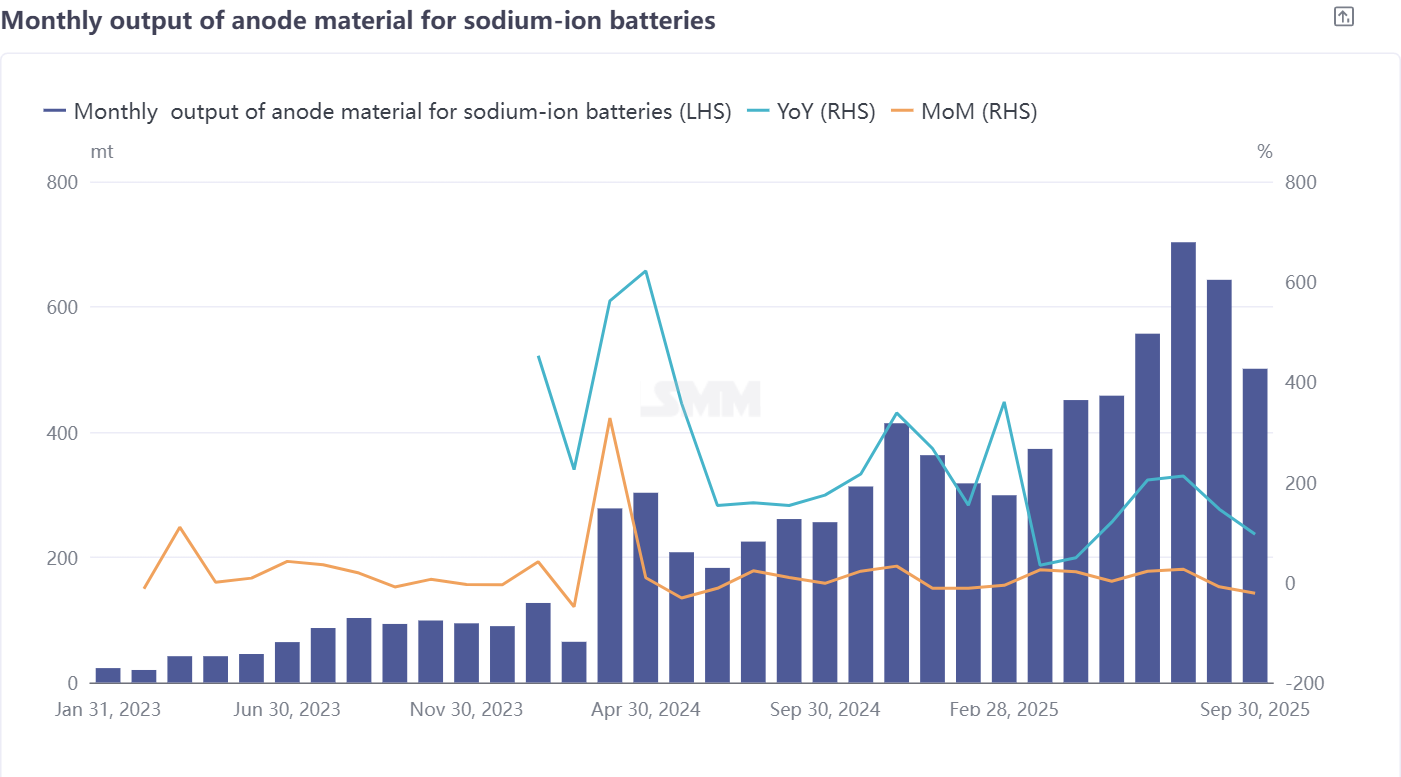

Hard Carbon Anode Material: Demand Fluctuations Drive Production, Full-Chain Production Capacity Awaits Breakthrough

In September, the production of sodium-ion battery hard carbon anode material also exhibited a "MoM contraction and high YoY growth" characteristic: down 22% MoM, with a YoY increase of 96%. There remains a significant imbalance between the "volume" and "stability" of industrial growth. The core challenges currently facing the hard carbon anode industry are concentrated in three areas: first, the supply of high-quality capacity is limited and cannot fully match potential demand; second, the process of raw material substitution lags behind, as the transition from overseas coconut shell raw materials to domestic raw materials has not been completed, affecting supply chain stability; third, there is significant volatility in orders, although market demand exists, the stability of orders is insufficient, increasing the difficulty of production planning for enterprises.

Constraints on the production side are even more pronounced: hard carbon production is a high-energy-consuming industry, and some enterprises, in order to control costs and energy consumption, focus their business on the R&D of precursors, while the critical high-temperature calcination process tends to be outsourced, making it difficult for a single enterprise to build a complete hard carbon production chain. More importantly, the high-temperature calcination process requires extremely high equipment precision and process stability, and the external cooperation model further increases the difficulty of product quality control.

From the perspective of demand, the current demand for hard carbon anodes is mainly concentrated in the small power and start-stop markets, where the requirements for product performance are relatively stable, supporting the steady price of hard carbon. Looking ahead to October, with the gradual recovery of downstream demand, it is expected that the production of hard carbon anode material will grow by 22% MoM, with the YoY growth rate narrowing slightly to 95%.

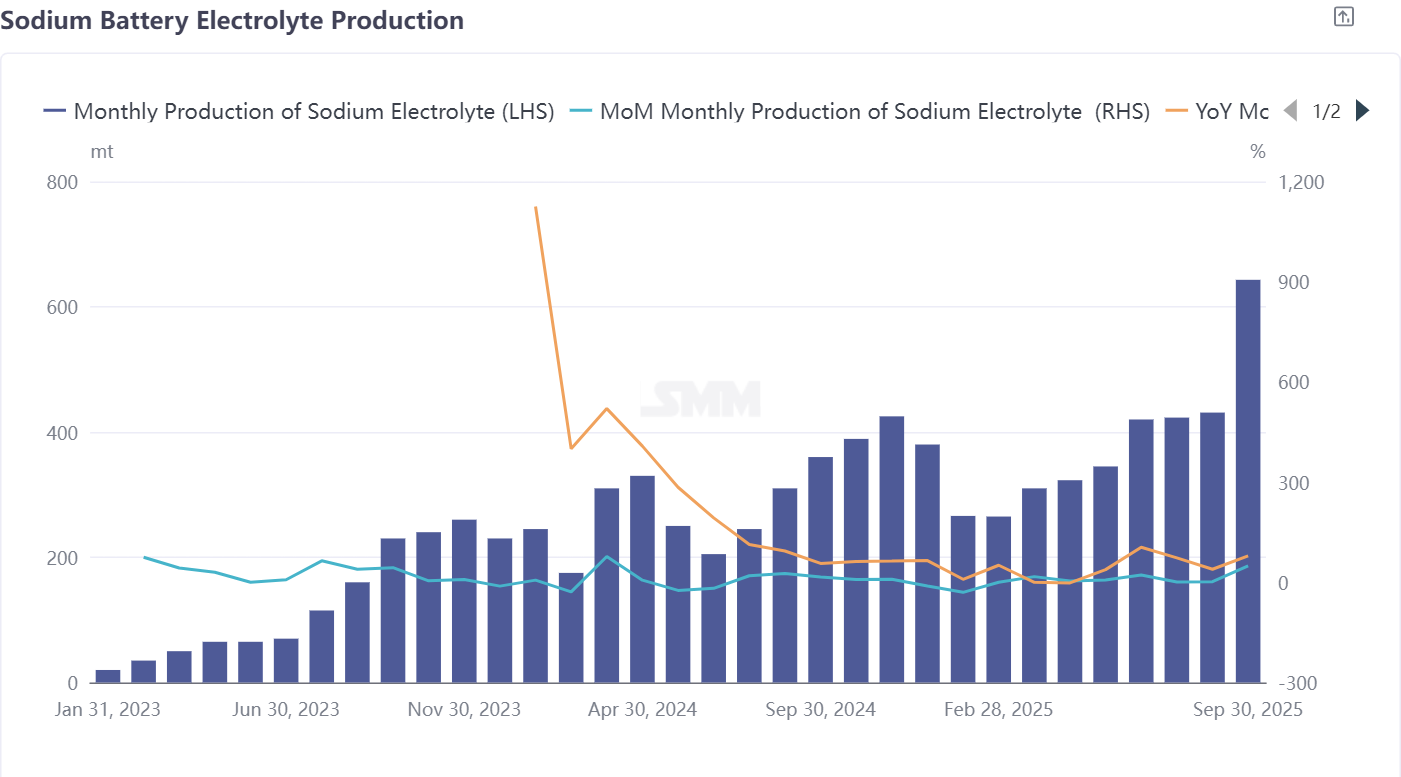

Sodium-Ion Battery Electrolyte: Top-Tier Enterprises Control Core Orders, Stable Costs Support Growth Resilience

Among all segments of the sodium-ion battery industry chain, the electrolyte sector was the most outstanding performer in September: production increased 49% MoM and 79% YoY, demonstrating strong growth resilience. From an industry structure perspective, the production of sodium-ion battery electrolytes is largely dominated by lithium battery electrolyte enterprises with technological expertise, with industry resources highly concentrated among top-tier enterprises — these top-tier enterprises not only hold more orders but also have significantly better order stability compared to small and medium-sized enterprises. Some top-tier enterprises have also expanded into overseas orders, further broadening market space. Cost side stability provides crucial support for the electrolyte segment. Currently, core raw material prices such as electrolytes and additives remain steady without significant fluctuations, keeping electrolyte production costs within a relatively controllable range and providing clearer profit expectations for enterprises. From a market logic perspective, the sodium-ion battery electrolyte industry remains order-driven, with top-tier enterprises leveraging their technological, capacity, and customer advantages to continue dominating the industry's growth trajectory. Sodium-ion battery electrolyte production in October is expected to maintain growth momentum, up 7% MoM and 77% YoY.

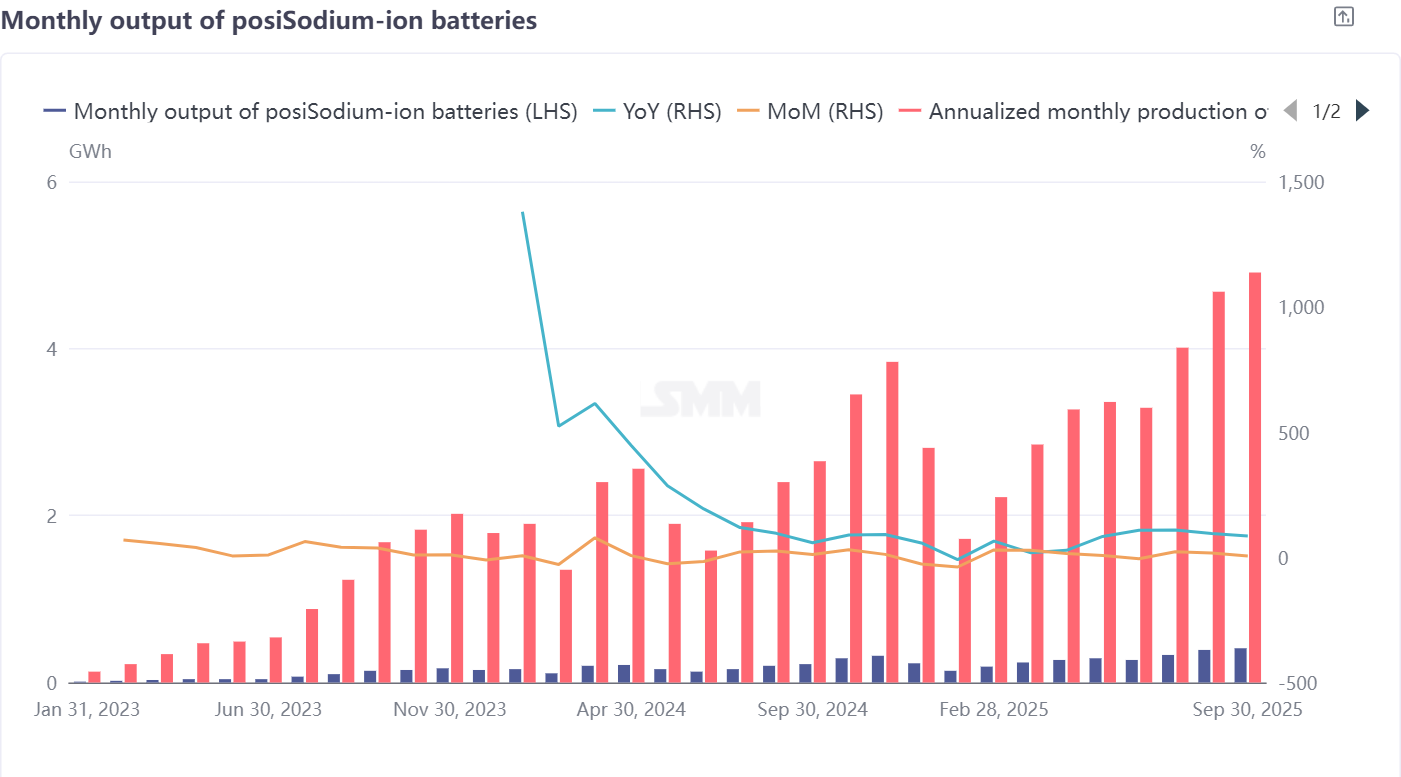

Battery Cell and End-User Applications: Focusing on Small Power and Start-Stop Breakthroughs, Utility ESS Still Requires Progress

Sodium-ion battery cell production achieved double growth in September: up 5% MoM and 85% YoY, with the expansion of end-use applications serving as the primary growth driver. Currently, small power and start-stop applications are key breakthrough areas for sodium-ion battery cell enterprises, widely seen as having the potential to first commercialize sodium-ion batteries—these applications have relatively modest energy density requirements and high cost sensitivity, aligning well with current sodium-ion battery technical characteristics.

However, practical challenges remain in mass production: on one hand, non-ideal issues in real-world applications directly impact short-term sodium-ion battery shipments and adoption rates, requiring cell enterprises to accumulate sufficient sample data and continuously optimize technical processes; on the other hand, the cost gap remains a core weakness—current sodium-ion battery costs still lag behind lithium batteries and lead-acid, with cost-performance advantages not yet fully realized.

Development in the utility ESS sector is more cautious: few domestic enterprises possess mature capabilities for producing large-format sodium-ion ESS cells, and existing products are still under continuous optimization, with the core goal of improving energy density through technical enhancements to strengthen sodium-ion ESS cost competitiveness. Sodium-ion battery cell production in October is projected to accelerate, up 10% MoM and 57% YoY. Summary of Industry Chain Operations

Overall, the sodium-ion battery industry chain in September exhibited a trend of "progress amid divergence": the electrolyte segment, leveraging the order advantages and cost stability of top-tier enterprises, became the primary driver of growth; cathode and hard carbon anode production, affected by mass production bottlenecks and demand fluctuations, faced MoM pressure on output; although battery cell end-use markets focused on breakthroughs in small power and start-stop applications, cost gaps and application challenges still need to be overcome.

The core contradiction in the current sodium-ion battery industry lies in balancing "advancements in mass production" with "technical optimization and cost control"—the NFPP cathode route must address application issues and capacity stability, hard carbon anodes need to achieve breakthroughs in full-chain production capabilities and raw material substitution, while battery cells must narrow cost gaps and accumulate application experience. The pace of the industry chain's subsequent recovery will heavily depend on the efficiency of technical adjustments by downstream battery cell manufacturers, the pace of capacity release by top-tier enterprises, and the realization of demand in end-use markets such as ESS and small power. In the short term, the industry chain as a whole is expected to achieve a mild recovery in October, but in the long run, it will still require technological iteration and economies of scale to truly solidify the market competitiveness of sodium-ion batteries.

![[SMM Analysis] Ternary Cathode Payables May See Modest Increase in Q2](https://imgqn.smm.cn/usercenter/nVnLo20251217171728.jpg)