SMM September 30 News:

Highlights: Phosphate ore supply and demand maintained a tight balance in September, with prices holding firm at high levels around 1,000 yuan. The proportion of new energy demand rose to 6%-7%, but prices for midstream materials like LFP faced pressure due to overcapacity. Enterprises accelerated deployment of phosphate ore resources and new solid-state battery materials, with a notable trend of vertical integration along the industry chain.

I. Phosphate Ore Market

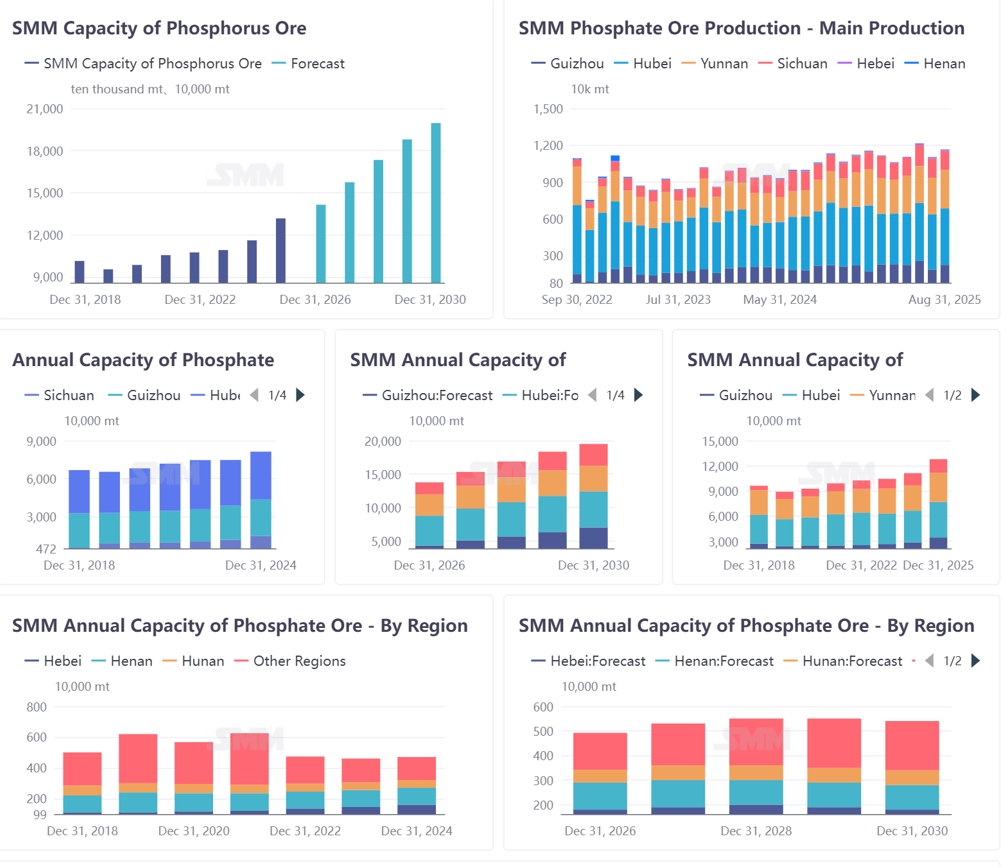

Phosphate ore capacity and production vary across regions. China's phosphate ore is mainly distributed in Hubei, Yunnan, Guizhou, Sichuan, and Hunan. Growth in capacity and production indicates industry expansion, but it also faces constraints from environmental protection policies. In September, phosphate ore prices were relatively stable, though slight fluctuations occurred due to downstream demand.

As a basic raw material for the phosphate chemical industry, price fluctuations in phosphate ore directly impact downstream product costs. Additionally, changes in energy prices (such as coal and natural gas) and raw material prices like sulfur also affect the costs of phosphate chemical products. In September, phosphate ore prices were generally stable, but sulfur prices increased, raising production costs for some phosphate chemical products and providing some support to product prices.

1. Capacity and Production: Global and Chinese phosphate ore capacity is steadily expanding, but actual production growth is limited by resource endowment and environmental protection policies. Data shows that China's phosphate ore capacity is highly concentrated in Hubei, Yunnan, Guizhou, and Sichuan (combined share over 80%). Production is forecast at 119 million mt for 2025, up 4.8% YoY, but structural issues such as scarcity of high-grade, high-quality phosphate ore remain prominent.

2. Import Supplement: Phosphate ore imports remained stable, mainly sourced from Egypt and Jordan, with Hubei and Guangxi as the primary importing provinces. However, due to import costs and scale limitations, the impact on the domestic supply landscape is limited.

3. Price Trend: In September, phosphate ore prices continued to hold at high levels. Prices for phosphate ore (30% grade) fluctuated around 1,000 yuan/mt, supported by a tight supply-demand balance.

4. New Energy Proportion

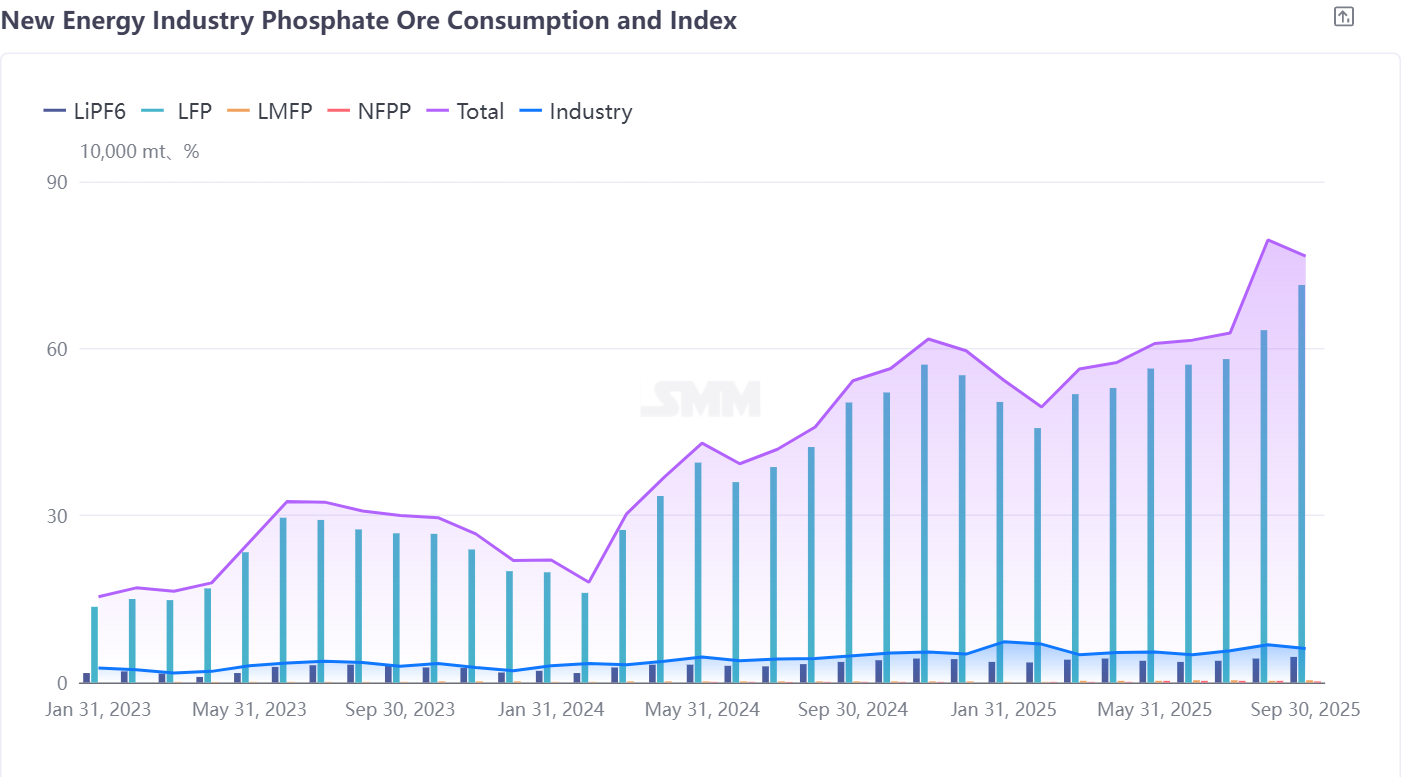

According to SMM estimates, phosphate ore consumption in the new energy sector accounted for 6%-7% in September. II. Phosphate Chemical Market

The fertilizer market has entered the off-season, while demand from the new energy sector has increased, though its proportion remains limited.

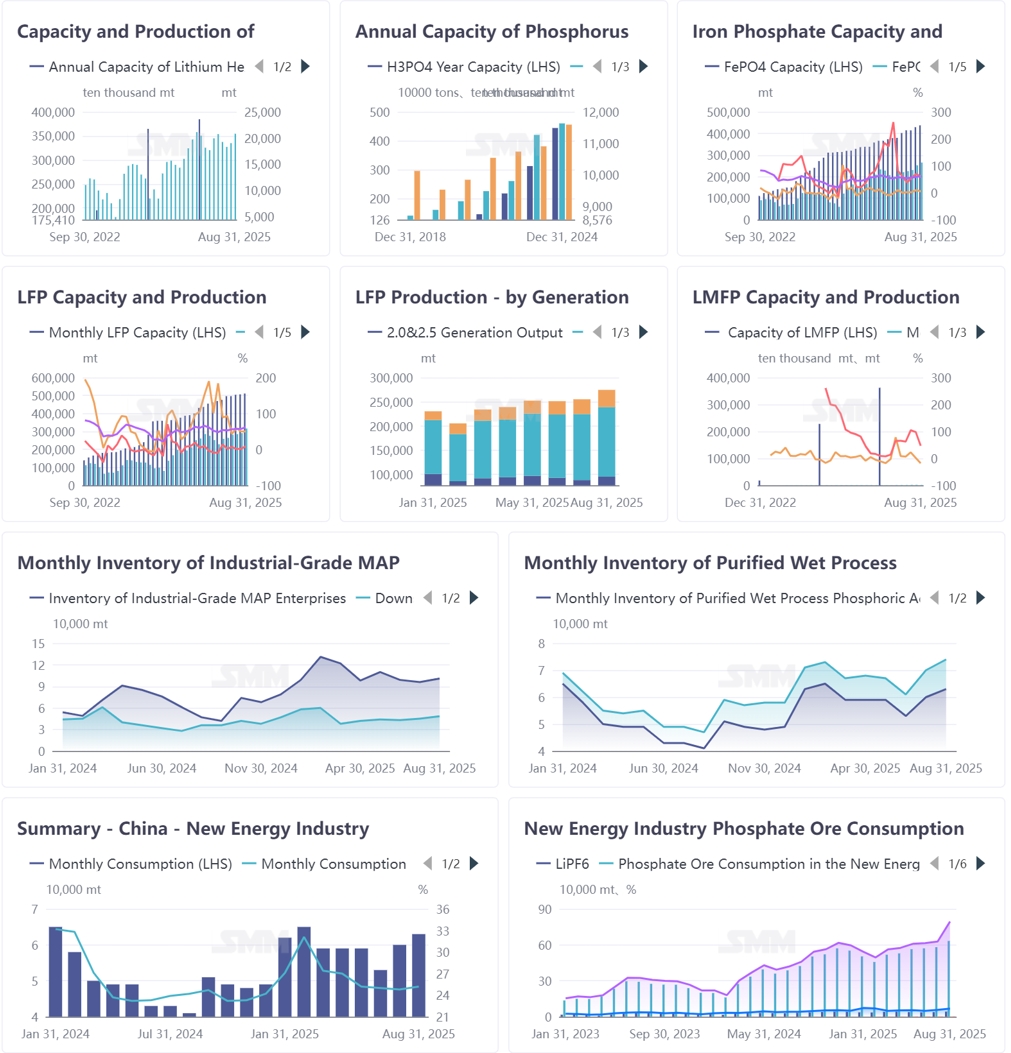

In September, the phosphate chemical market generally showed an upward trend in both capacity and production, but it also faced challenges such as rising raw material costs and fluctuations in downstream demand. Phosphate ore prices remained relatively stable, though minor fluctuations occurred due to downstream demand. Prices of phosphate chemical products were also relatively stable in September but experienced slight variations influenced by raw material costs and downstream demand. Both capacity and production of phosphate chemical products increased in September, primarily driven by rising demand for lithium batteries. Exports of phosphate chemical products decreased in September, mainly due to tight international supply and increased domestic demand. Inventory of phosphate chemical products rose in September, largely because of reduced downstream demand. Consumption of phosphate chemical products increased in September, mainly propelled by growing demand for lithium batteries.

Industry Dynamics in the Phosphorus Chemical Sector for September (Partial)

[Solid-State Battery: Titan's Lithium-Sulfur-Phosphorus-Chlorine Solid Electrolyte Project Under Preparation] On September 1, 2025, Titan Co., Ltd. released a record of investor relations activities. The company stated during a recent institutional survey that, to expand into new fields, it has established a controlling subsidiary primarily engaged in the R&D and production of lithium-sulfur-phosphorus-chlorine solid electrolytes for solid-state batteries. Equipment procurement and other preparatory work are currently underway.

[Phosphorus Chemical Update: Southwest Energy & Mineral's Motianchong Phosphate Ore Mine's 2.5 Million mt Annual Mining and Beneficiation Project Fully Completed] On September 4, 2025, the second mining area of Southwest Energy & Mineral's Motianchong Phosphate Ore Mine commenced trial production, gradually releasing an annual production capacity of 1 million mt from this area. The mine's 2.5 million mt annual mining and beneficiation project has been fully completed, unleashing the mine's total capacity. The Xinhua Phosphate Ore District in Zhijin County, where the Motianchong mine is located, is one of Guizhou's three major phosphate ore districts. In the first eight months of 2025, the first mining area cumulatively produced 1.15 million mt of raw ore and 580,000 mt of phosphate concentrate.

[Iron Phosphate: Safety Incident at Titanium Dioxide Enterprise's Xiangyang Plant May Impact Ferrous Sulphate Prices] On the evening of September 8, 2025, a major titanium dioxide manufacturer announced that production at its Xiangyang subsidiary's sulphuric acid line had been halted for maintenance due to a safety incident on the evening of September 2. This is expected to affect nearly 100 mt of ferrous sulphate production, potentially driving up ferrous sulphate prices and increasing costs for iron phosphate enterprises.

[Taihe Technology: Solid Electrolyte Lithium Aluminum Titanium Phosphate (LATP) in Pilot Stage, No Cooperation with CATL Yet] On September 12, Taihe Technology stated that its solid electrolyte lithium aluminum titanium phosphate (LATP), intended for oxide batteries, is currently in the pilot stage and has not yet generated sales. The company has not established cooperative relationships with top-tier enterprises such as CATL for this product.

[Phosphorus Chemical Update: Wintrue Acquires 49% Stake in Phosphate Mine with Nearly 30 Million mt Reserves] On September 24, 2025, Wintrue (002539) announced that, to increase its phosphate ore resource reserves, the company signed an agreement with Mabian Xinyong Zhiyuan Enterprise Management Co., Ltd. and its wholly-owned subsidiary, Sichuan Mabian Shenglong Mining Co., Ltd., to acquire a 49% equity stake in Shenglong Mining through a capital increase and share expansion. Additionally, to support Shenglong Mining in acquiring and developing the Erba Phosphate-Lead-Zinc Mine, Wintrue plans to provide a loan of up to 500 million yuan proportional to its equity stake. The mine has phosphate ore resources of approximately 29.271 million mt and a designed mining scale of 500,000 mt per year. This cooperation will grant Wintrue a 49% interest in the mine. [Phosphate Chemical Industry Update: Wet Process Phosphoric Acid and Other Facilities in Capacity Ramp-up Phase] On September 24, 2025, Chanhen (002895.SZ) stated on the interactive platform that since 2022, Chanhen Guangxi Pengyue Company has gradually commissioned production facilities in phases. The wet process phosphoric acid, monocalcium phosphate dihydrate, and purified phosphoric acid facilities have reached designed capacity, while the anhydrous hydrogen fluoride facility is still undergoing process optimization and capacity ramp-up. The company will expedite efforts to increase capacity and strive to reach full production as soon as possible. There are currently no new monoammonium phosphate (MAP) production lines under construction in the company's ongoing projects.

[100,000 mt LFP Project is Expected to Commence Production] In September, the 100,000 mt per annum high performance LFP cathode material project of Pengbo New Materials in the Quandong Industrial Park, Yangquan High-tech Zone, Shanxi Province, is expected to commence production, which is anticipated to further improve the lithium battery industry chain in the Yangquan area. The project is invested in and constructed by Hunan Pengbo New Materials Co., Ltd. (hereinafter referred to as Pengbo New Materials), with its wholly-owned subsidiary, Shanxi Pengbo New Materials Co., Ltd., responsible for operations. The planned total annual capacity is 200,000 mt, based on existing ferrous oxalate preparation of high-compaction density LFP, producing the fifth-generation LFP. On April 7 this year, the first phase of the project officially started construction, with an investment of 1.85 billion yuan, planning to build 8 production lines. The project planned to start trial production with feed-in in mid-September, with batch and stable delivery output beginning in October. The project is currently progressing in an orderly manner. Additionally, the second phase with a capacity of 100,000 mt is under preparation.

[Phosphate Ore: China's Phosphate Ore Exports Edged Up 4.1% in August] In August 2025, China's phosphate ore export landscape underwent a significant shift, but the total export volume remained at an absolutely low and stable level. Exports edged up 4.1% MoM, staying at an extremely low level of 11,000 mt for two consecutive months. The main change this month was the complete transfer of export tasks from Fujian Province to Hubei Province.

[Phosphate Ore: Drastic Change in China's Phosphate Ore Import Pattern in August, Source Country and Port of Entry Both Show Single Dominance of "Egypt-Guangxi" Mode] In August 2025, China's phosphate ore imports exhibited prominent characteristics of stable total volume, changed structure, and decreased average price. The patterns of source countries and entry provinces experienced drastic fluctuations, rapidly switching from a dispersed pattern involving multiple countries and provinces in July to a highly concentrated pattern in August dominated by a single country, Egypt, with almost all imports entering through Guangxi ports. Although this led to a slight increase of 8.9% MoM in total imports to 130,000 mt, the abandonment of high-priced sources like Peru caused the total import value to drop 7.3%, and the national comprehensive import average price fell significantly by 14.9% YoY. [SMM Announcement: Announcement on the Addition of Six Regional Price Points for Phosphate Ore] SMM will officially release six regional price points for phosphate ore starting October 9, 2025.

SMM Phosphate Ore (Yunnan 30%) P₂O₅≥30%

SMM Phosphate Ore (Guizhou 30%) P₂O₅≥30%

SMM Phosphate Ore (Sichuan 30%) P₂O₅≥30%

SMM Phosphate Ore (Hubei 28%) P₂O₅≥28%

SMM Phosphate Ore (Hubei 30%) P₂O₅≥30%

SMM Phosphate Ore (Hebei 32%) P₂O₅≥32%