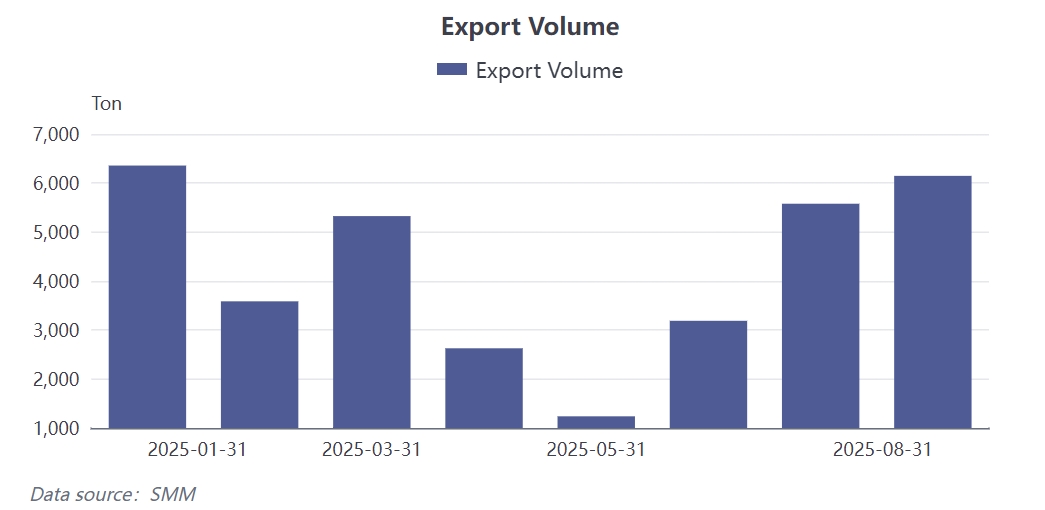

Rare earth permanent magnets, known as the "vitamins" of modern industry, play an indispensable role in fields such as new energy vehicles (NEVs), wind power generation, and industrial robotics. In August 2025, China's rare earth permanent magnet exports showed a strong rebound, with monthly exports reaching 6,145.623 mt, up 10.19% MoM and 15% YoY, hitting a new high since January this year. Of the monthly increase of 600 mt, Europe contributed over 90%.

01 Export Data Analysis: Overall Rebound and Regional Divergence

As of August 2025, China's cumulative exports of rare earth permanent magnets reached 34,041.06 mt. Although this figure decreased 10% YoY, the strong performance in August indicates a recovery in market demand.

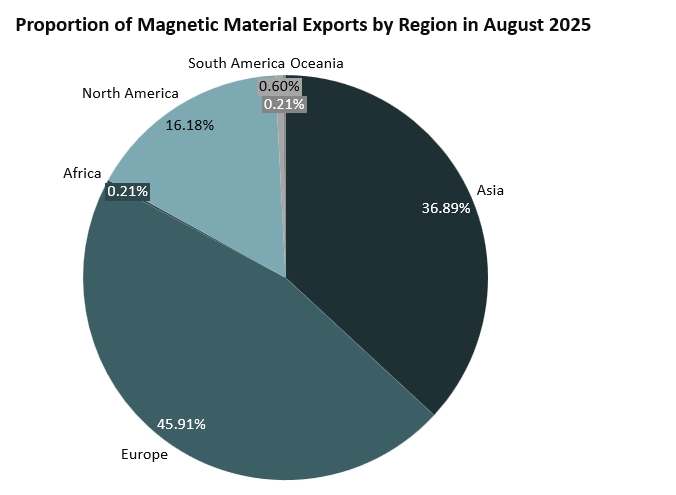

Regionally, the export landscape showed significant divergence. Exports to Asia totaled 2,267.21 mt, basically flat from July; exports to Africa, North America, South America, and Oceania were 13.195 mt, 994.085 mt, 36.808 mt, and 12.949 mt, respectively, also remaining stable.

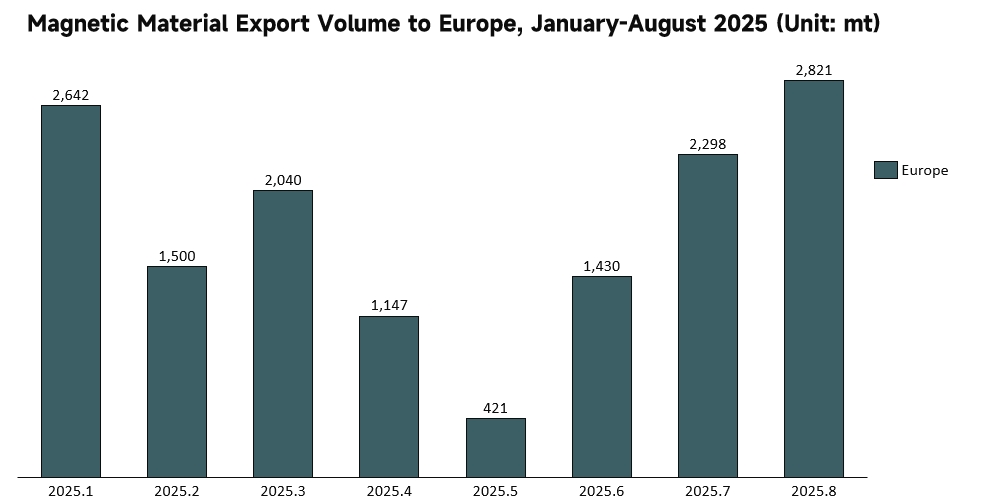

The real growth driver came from Europe—exports to the region surged to 2,821.403 mt in August, marking the third consecutive month of growth.

Among major export destinations, Germany stood out with imports of 1,341.08 mt, up 20.19% MoM; while the US imported 589.85 mt, down 1.6% MoM.

02 Industry Overall Outlook: Short-Term Pressure and Long-Term Growth

From a full-year perspective, the industry generally expects total magnetic material exports in 2025 to be approximately 49,000 mt, a decrease of about 15% compared to 58,120 mt in 2024.

As of August, cumulative exports have already reached 34,000 mt, meaning that an additional 15,000 mt needs to be exported over the next four months, with a monthly average of about 3,500 mt to meet expectations.

In the short term, a large number of orders for essential demand from Europe have been largely released. Affected by the Christmas holiday, growth potential in Q4 is limited, and overall exports will not be substantial.

In the medium and long term, the continuous expansion of demand in emerging sectors is injecting new momentum into the industry. Global demand for high-performance NdFeB is expected to continue growing, particularly in the European new energy vehicle and wind power sectors.

03 Drivers of Export Surge, Dual Impetus from Geopolitics and Industrial Demand

Sino-US rivalry accelerates stockpiling pace in Europe. Overseas customers' stockpiling sentiment is high, extending the stockpiling cycle.

Rigid demand brought about by the peak industrial season in Europe is another key factor. Rare earth magnetic materials are crucial components in high-performance motors and generators, widely used in the renewable energy and automotive industries.

One out of every three NEVs globally relies on Chinese rare earth magnetic materials, and each EV's drive motor requires at least 1.5-8 kg of NdFeB magnets.

Demand in the wind power sector is also robust, with the penetration rate of direct-drive permanent magnet turbines continuously increasing, and each unit requiring a large amount of magnets.

Export control policies highlight the advantages of major manufacturers. Under current regulations, large magnetic material enterprises, due to their direct engagement with top-tier European enterprises, enjoy more convenient export approvals and have more complete magnetic material traceability systems.

This has led to an intensification of industry polarization, with operating rates of top-tier enterprises exceeding 90%, and some even reaching full production capacity.

04 Q4 Export Outlook: Stable Total Volume with Structural Divergence

Integrating industry dynamics and policy guidance, rare earth magnetic material exports in Q4 2025 are expected to feature "stable total volume with structural divergence." On one hand, the European market will see a slowdown in new order growth due to the Christmas holiday and the completion of prior stockpiling demand release; on the other hand, Asian and North American markets may absorb some diverted demand, though overall incremental growth remains limited. Based on cumulative exports of 34,000 mt from January to August and the full-year expectation of 49,000 mt, Q4 requires exports of 15,000 mt, averaging approximately 3,500 mt per month, a notable pullback from the August peak (6,145 mt).

Price-wise, supported by a tight supply-demand balance, rare earth magnetic material prices are expected to remain elevated. Key material prices such as Pr-Nd oxide continue to stabilize, while heavy rare earth demand remains weak with limited upside room for prices. Long-term, emerging sectors like humanoid robots and the low-altitude economy will gradually contribute to demand growth, but substantial boost within 2025 is limited.