Malaysian Iron Ore

Malaysia is located in the heart of Southeast Asia, consisting of the Malay Peninsula and the states of Sabah and Sarawak on the island of Borneo, with a total area of approximately 330,000 square kilometers. The country is divided into eastern and western parts by the South China Sea. West Malaysia borders Thailand and Singapore, while East Malaysia is adjacent to Indonesia and Brunei. Its economy is supported by manufacturing, services, and commodity exports, making it an important newly industrialized country in Southeast Asia. Benefiting from its unique strategic geographical location and the Strait of Malacca, Malaysia has historically been a crucial trade hub and a key period of the Maritime Silk Road.

Malaysia has relatively abundant iron ore resources, with reserves of approximately 85 million mt, distributed in states such as Terengganu, Johor, Pahang, Kedah, and Negeri Sembilan. The main ores resources are magnetite and hematite, accompanied by resources such as ilmenite, pyrite, and chromite. Typical deposits include the Bukit Besi mine in Terengganu, the Pelepah Kanan mine in Johor, and the Tavai mine in Sabah, with an average iron content ranging from 40% to 45%.

I. Iron Ore Supply in Malaysia: Malaysia Have Over 80 Small and Medium-Sized Low-Grade Iron Ore Mines

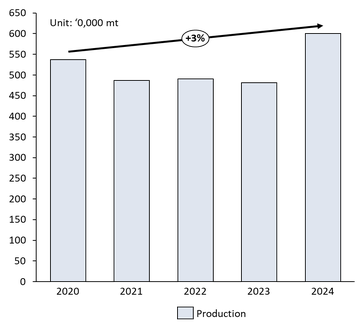

The iron ore production industry in Malaysia is characterized by low concentration, with output distributed across numerous small mines, and the products are predominantly low-grade ore. According to a report by the Malaysian Mining Association, Malaysia's iron ore production in 2023 was approximately 4.82 million mt, produced by 73 mines located in Pahang and Terengganu states. In 2024, Malaysia's annual iron ore production reached about 6 million mt, with the number of mines increasing to 81.

Although Malaysia's iron ore production capacity has grown slowly in recent years, many enterprises are currently actively engaged in mergers and acquisitions and developing new projects. Additionally, an increasing number of overseas miners are expanding into Malaysia, indicating potential for future growth in the country's iron ore production.

Malaysia Iron Ore Production (2020-2024)

Data Sources: Chamber of Miner Malaysia ; Transitionasia ; SMM

II. Iron Ore Mines in Malaysia

The Malaysian iron ore market is currently led by three large-scale enterprises: the blending and distribution center established by Brazil's Vale in Malaysia, along with two local mining companies, Fortress Minerals and Southern Alliance Mining (SAM).

Vale Distribution Center

When discussing the Malaysian iron ore market, it is essential to mention the iron ore distribution center operated by Brazil's Vale. Established in 2014 and located in Teluk Rubiah, Perak, adjacent to Lumut Port and the Strait of Malacca, the center has an annual handling capacity of approximately 25 million mt.

Iron ore shipped from the Malaysian distribution center reaches Asian customers in about 1 to 10 days. The facility features a deep-water berth capable of accommodating 400,000 mt bulk carriers, complete loading and unloading facilities, as well as a stockyard with a storage capacity of about 3.2 million mt and blending facilities. It serves as a crucial hub for the company in Asia.

Fortress Minerals

Fortress Minerals' primary mine is the Bukit Besi Mine, located in Terengganu, 86 kilometers from the trading port of Kemaman Port, with reserves of approximately 7.79 million mt of raw ore averaging an iron grade of Fe 38.88%. Its main product is magnetite concentrate with Fe 65, along with some hematite coarse fines and lump ore with Fe 55–60.

It also owns the Mengapur Mine under development in Pahang, adjacent to Kuantan Port, 85 kilometers away, with iron ore reserves of about 2.1 million mt and an average raw ore iron grade of Fe 30.30%. The mine comprises two mining areas: Cermat Aman (CASB) and Star Destiny (SDSB). CASB commenced production in July 2022 and is now expected to build a new integrated processing plant. This facility will enhance the production capacity of the CASB mine, enabling it to produce high-grade iron ore. The combined sales volume of Fortress Minerals' two mines in 2024 was 632,400 mt.

Southern Alliance Mining (SAM)

Southern Alliance Mining's primary mine is the Chaah Mine, located in Johor. It benefits from a strategic location, adjacent to Johor Port and the road network. The main product is hematite concentrate with Fe 62–65%. The group's existing supporting infrastructure and equipment include four fixed crushing stations, two mobile crushing production lines, and two beneficiation plants, all operating 24/7 in shifts, with an annual capacity of approximately 720,000 mt.

The reserves are about 1.42 million mt, with an average raw ore iron grade of Fe 49.9%. Chaah Mine fully transitioned from open-pit mining to underground mining in 2024, with production reaching approximately 310,000 mt. Additionally, SAM has three ongoing exploration projects: Mao'Kil, Chaah Baru, and Kota Tinggi.

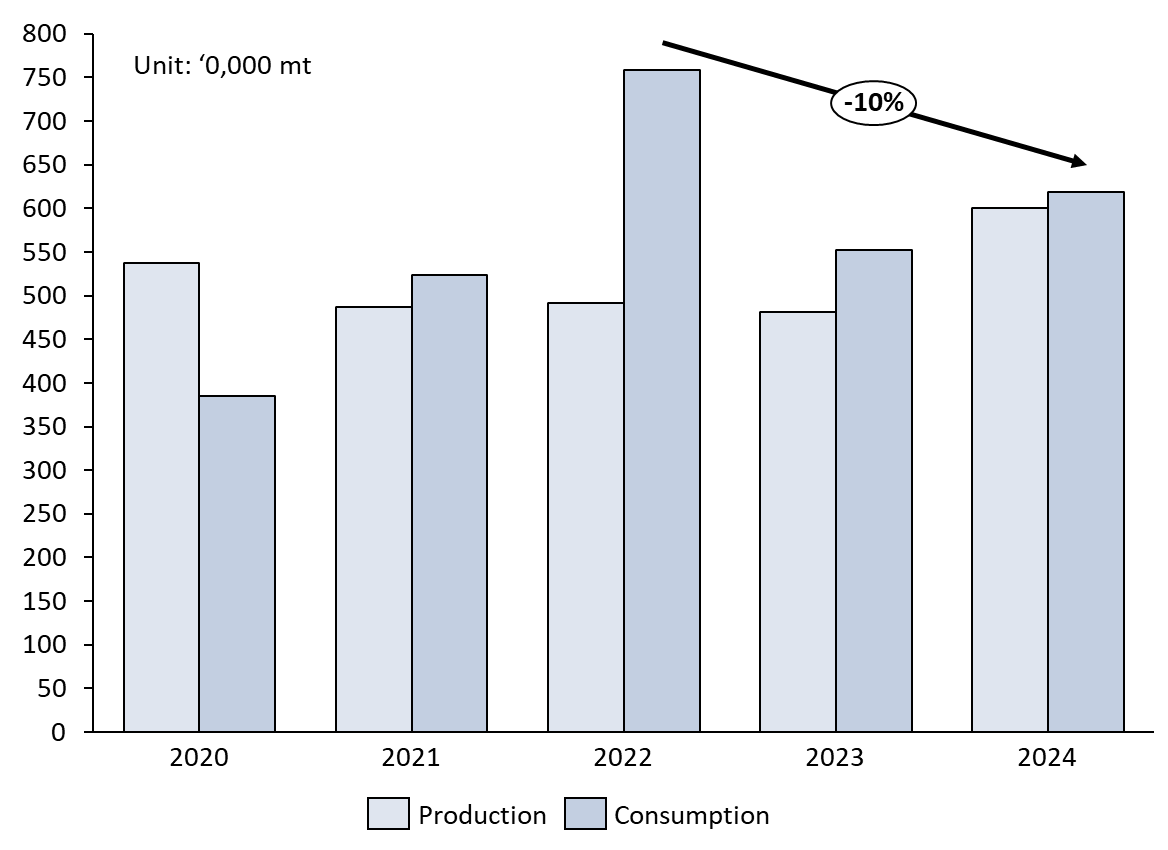

III. Malaysia's Annual Iron Ore Consumption: 6.19 Million mt, Primarily Consumed by 3 Blast Furnace Steel Mills and 1 Direct Reduced Iron (DRI) Plant

According to SMM statistics, Malaysia's operational hot metal capacity in 2024 was approximately 7.3 million mt/year, with blast furnace-based hot metal capacity from long-process steel mills accounting for about 6.4 million mt/year, produced by three steel mills located in Pahang, Penang, and Terengganu. Direct reduced iron (DRI) capacity was 900,000 mt/year, produced by one DRI plant in the Labuan region.

Malaysia's iron ore consumption peaked in 2022, reaching approximately 7.59 million mt, before declining to about 5.52 million mt in 2023 due to the impact of a suspension order on the steel industry. In 2024, consumption was around 6.19 million mt.

Evolution of Malaysia's Iron Ore Production and Consumption (2020-2024)

Data Sources: Chamber of Miner Malaysia ; SMM

Blast Furnace and Direct Reduced Iron (DRI) Plants in Malaysia:

Alliance Steel Kuantan Plant

Operated by Alliance Steel (M) Sdn Bhd, a joint venture between Guangxi Beibu Gulf International Port Group and Guangxi Shenglong Metallurgy, the steel mill is located in Kuantan, Pahang. It features two 1,080 m³ blast furnaces with a total hot metal capacity of approximately 3.5 million mt per year, supported by upstream sintering lines and a coke production line with a capacity of about 1.1 million mt. The steel mill currently has a Phase II expansion plan, which is expected to increase hot metal capacity to 6.5 million mt and steel capacity to 10 million mt.

Ann Joo Integrated Steel Penang Plant

Operated by Ann Joo Integrated Steel Sdn Bhd, located in Bukit Mertajam, Penang. The plant operates one blast furnace (BF) with a volume of 450 m³, with a hot metal capacity of approximately 500,000 mt/year. It is equipped with one sintering line with an area of 75 m².

Eastern Steel Kemaman Plant

Operated by Eastern Steel Sdn Bhd, located in Kemaman, Terengganu. The plant operates two blast furnaces (BF) with volumes of 600 m³ and 1,380 m³, respectively, with a hot metal capacity of approximately 2.4 million mt/year. It is equipped with three sintering lines with areas of 36 m², 100 m², and 200 m², respectively, and a coke production line with a capacity of about 800,000 mt.

Esteel Antara Labuan Iron Plant

Operated by Antara Steel Mills Sdn Bhd, located in Labuan, Malaysia’s offshore financial hub. It uses the hot briquetted iron (HBI) process with a capacity of 900,000 mt/year and is a wholly-owned subsidiary of the Lion Group.

In addition, there are two mothballed direct reduced iron plants in Malaysia:

Maju Perwaja Steel Plant, located in Kemaman, Terengganu, with a capacity of approximately 120,000 mt/year. It has been idle since 2013 due to financial issues of the operator. An attempt to revitalize the company through Chinese investment in 2017 was unsuccessful. Market rumors suggest the plant may be taken over by JXR Manufacturing Sdn. Bhd., a subsidiary of China’s Jianlong Group, for production resumption and capacity expansion, but no concrete news has emerged so far.

Amsteel Banting Steel Plant, owned by the Lion Group, located in Klang, Selangor, with a capacity of approximately 154,000 mt/year. It has been suspended since 2016 due to unfavorable domestic and overseas steel market conditions. It was originally scheduled to resume operations by the end of 2021 and reach full production by 2022, but as of September 2025, no specific news about production resumption has been reported.

List Of Malaysia Operating Steel Plant

Data Sources: SMM

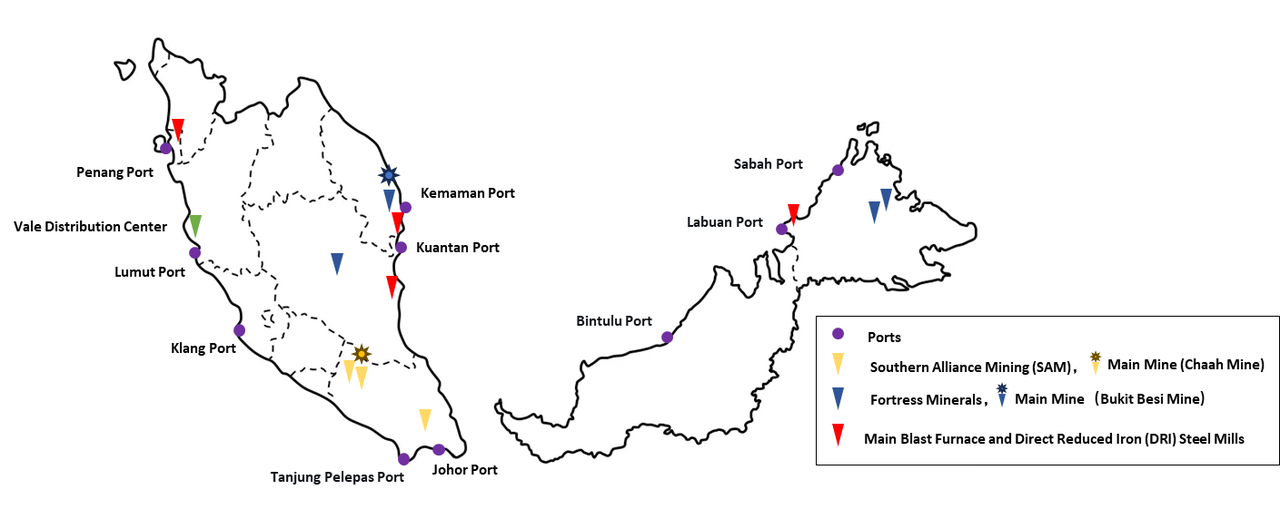

Distribution Map of Major Players in Malaysia's Steel Industry Chain:

Data Sources: SMM

IV. Malaysia's Steel Industry Moratorium

The Malaysian steel industry faces overcapacity issues, particularly in low-end products such as rebar and wire rod, while there remains a supply gap for flat products. Currently, high-end steel products like hot-rolled coil (HRC) cannot be produced domestically, leading to Malaysia's long-term reliance on imports for high-end materials.

To restructure the domestic industry chain in line with the New Industrial Master Plan 2030 (NIMP 2030) and provide a window for domestic steel manufacturers to enhance production capacity to address low-end overcapacity, the Malaysian government, through the Ministry of Investment, Trade and Industry (MITI), issued a two-year moratorium on the steel industry on August 15, 2022. The suspension covers all inquiries for manufacturing licenses, evaluation of existing applications, new applications, license transfers, and procedures for the formalization and diversification of manufacturing licenses. Additionally, the government has restructured industry institutions such as the Malaysia Steel Association and the Steel Council. The moratorium, originally set to end in August 2025, was approved for an extension in February 2025, but the Malaysian side has decided to reassess the extension once the capacity utilization rate of upstream enterprises reaches nearly 80%. SMM continues to track and report on developments related to the moratorium.

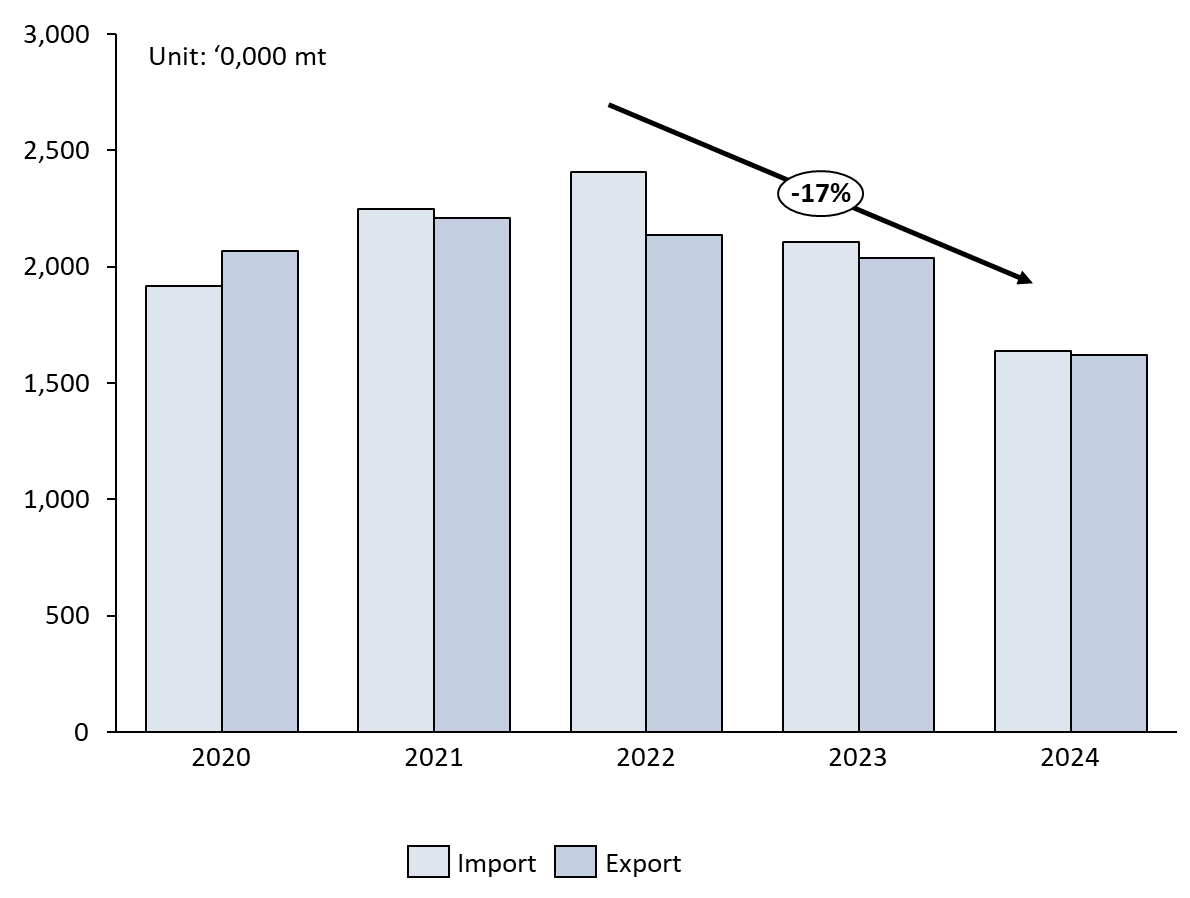

V. Analysis of Iron Ore Imports and Exports

Evolution of Malaysia's Iron Ore Imports and Exports, 2020–2024

Data Sources : Chamber of Miner Malaysia ; SMM

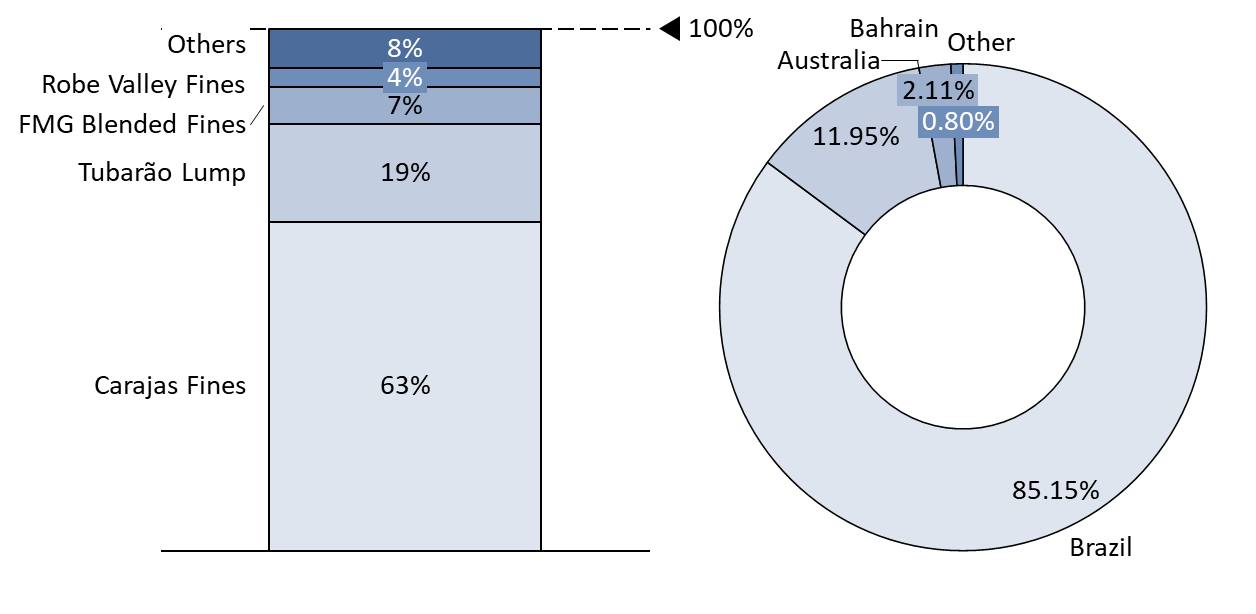

Looking at Malaysia's iron ore import and export landscape, it is characterized by both high imports and high exports. In 2024, total imports reached approximately 16.38 million mt, with major import sources being Brazil (85%) and Australia (11.95%). The primary variety was Carajás pellets, accounting for about 63%, followed by Tubarão lumps at around 19%, and FMG blended fines at approximately 7%.

Malaysia's Iron Ore Import Varieties and Source Countries (2024)

Data Sources: SMM

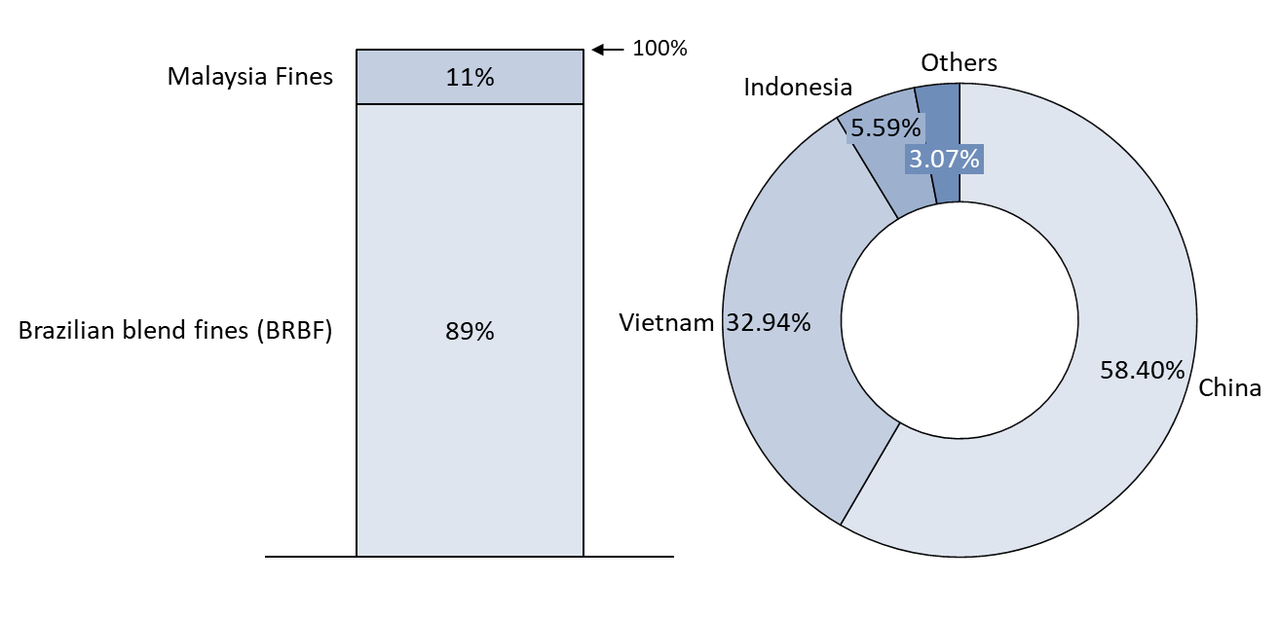

The main export destinations were China (58.40%), Vietnam (32.94%), and Indonesia (5.59%). In 2024, Malaysia's iron ore exports amounted to approximately 16.19 million mt, primarily consisting of Brazilian blend fines (BRBF), which accounted for 89% of total exports, while local ore exports were relatively low, making up 11% of the total.

Malaysian Iron Ore Export Varieties and Destination Countries (2024)

Data Sources: SMM

All in all, Iron ore market in Malaysia shows low concentration, characterized by an oversupply of sellers but a scarcity of buyers. Currently, the market is significantly influenced by policy measures; a two-year suspension order has substantially impacted Malaysia's entire steel market, including the demand for iron ore. With shifts in global capital flows, Malaysia, as a member of ASEAN, is attracting increasing attention. More players are entering the Malaysian market to establish a presence, while local enterprises are actively pursuing mergers and acquisitions and developing new projects. Malaysia's steel industry chain is expected to undergo major changes in the coming years.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)