Recently, bidding and annual long-term contract negotiations in the African refined-copper market have heated up. Driven by shifts in the global supply-demand structure, geopolitical tensions and tariff policy shocks, intense bidder competition has pushed the market into an early phase of resource scrambling and contractual bargaining. Especially from Q3 2025 onward, clear signals have emerged — such as upward revisions to FCA long-term contract premium in the DRC and Zambia, and sharp spikes in tender bids for spot lots.

Supply tightening amid capacity transition

As old and new capacity cycles overlap, the supply-demand landscape is being reshuffled and the supply side is tightening: 2025–2026 are widely viewed as the two tightest years for the copper concentrate balance, with frequent cutbacks and shutdowns at overseas smelters. Outside China, Africa and Indonesia are seen as the largest incremental sources over the next two years, making them focal points for global buyers.

Incremental import demand from US demand reshaping

Following the US Section 232 that placed a 50% tariff on semis copper products, demand for imported semis products is expected to progressively shift toward refined-copper imports. Under an assumption of a full transfer within two years, this implies an incremental refined-copper import requirement on the order of roughly 400,000 tonnes per year within the next 1–2 years. Given that traditional suppliers such as Chile, Peru, Mexico and Canada are unlikely to fully meet this increment in the near term, the US and other demand centres will inevitably seek supplementary supplies from alternative resource countries.

Structural increase in downstream demand

Longer-term demand from sectors such as new energy, AI and electronic information has risen rapidly in recent years, imparting to copper some characteristics of a “strategic energy resource.” The US has already designated copper as a strategic resource for national security, further intensifying competition for high-quality long-term supply.

Traders accelerate resource allocation; regional premiums rise, with both long-term and spot-lot prices climbing

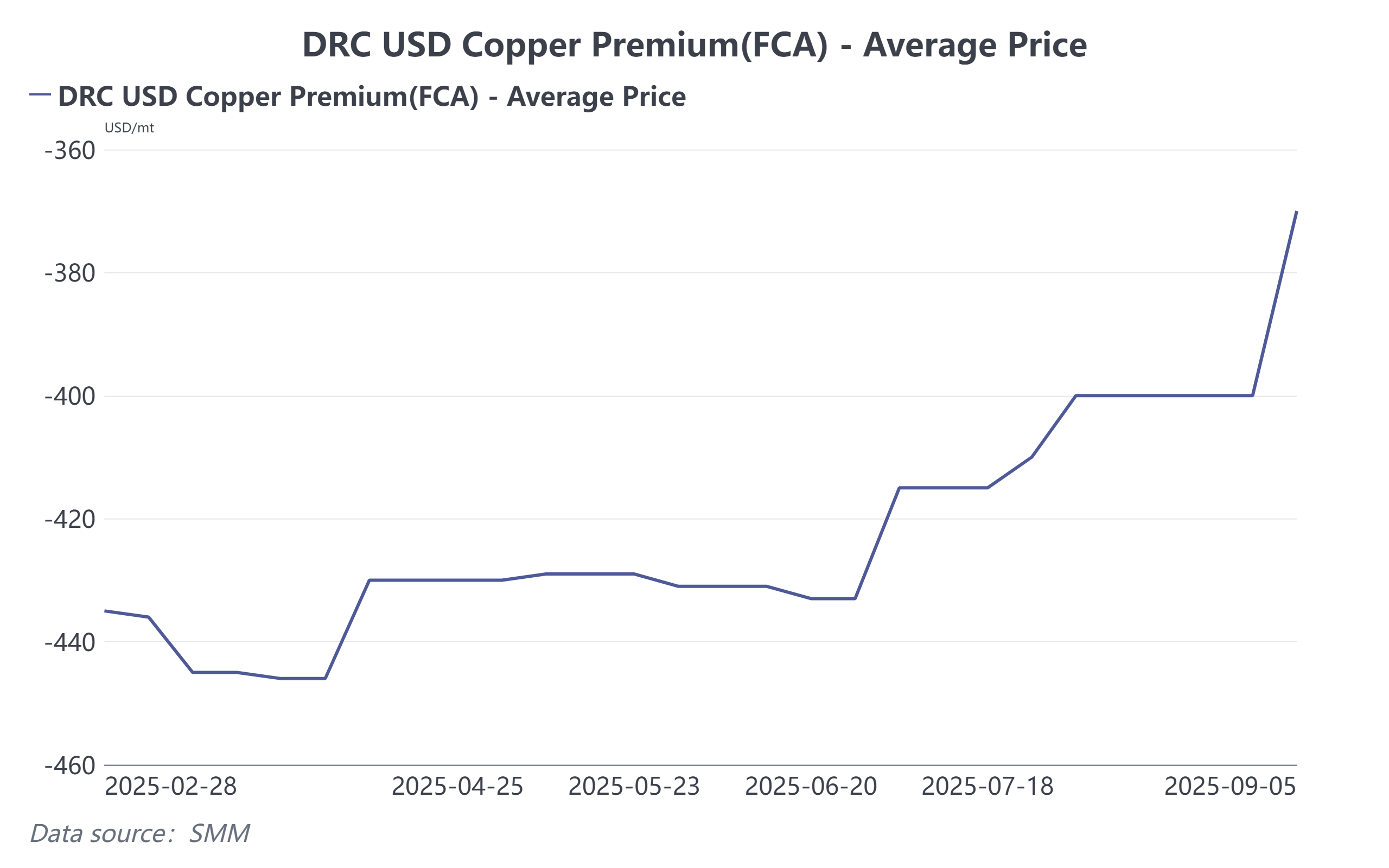

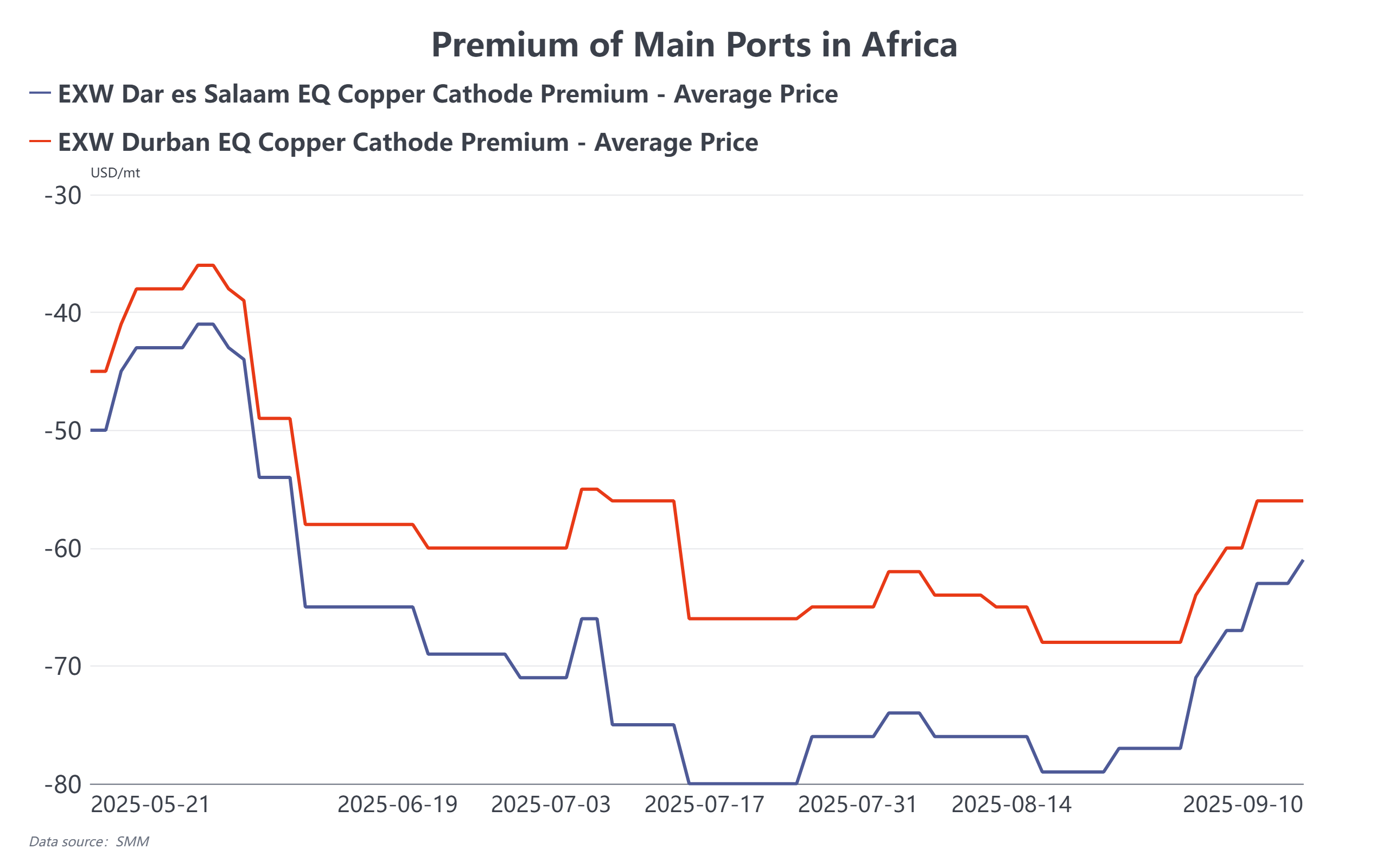

According to SMM, since Q3 DRC FCA long-term contract prices have been raised by about $30–40/tonne. At the same time, a small number of spot-lot tenders have cleared at around −$300/tonne (winning bids at QP M+1 — note: these were individual spot-lot awards), representing a notable increase from prior levels over 100$/tonne. EXW spot-lot premiums at Durban and Dar es Salaam ports have risen week-on-week; some recent trades were around −$50/tonne (QP M+0). Competition among traders for Q4 and 2026 cargoes is fierce, and market expectations continue to ratchet higher.

Supply-demand and strategic competition already focused on Q4/2026

With annual long-term negotiations imminent, uncertainty is high over whether tariff disputes or other policy shocks will re-emerge in 2026. From macro narratives (economic development, resource security) to funding/arbitrage and supply allocation perspectives, preparations for the 2026 round of strategic competition are already underway — pushing up negotiation tempo and price expectations.

Outlook

Although many of these contests are not yet settled, 2026 looks set to be another year of strained resource allocation. Regional trade fragmentation increases pressures on supply security, and by the year-end long-term negotiations, premiums priced into 2026 are expected to be higher than those for 2025.