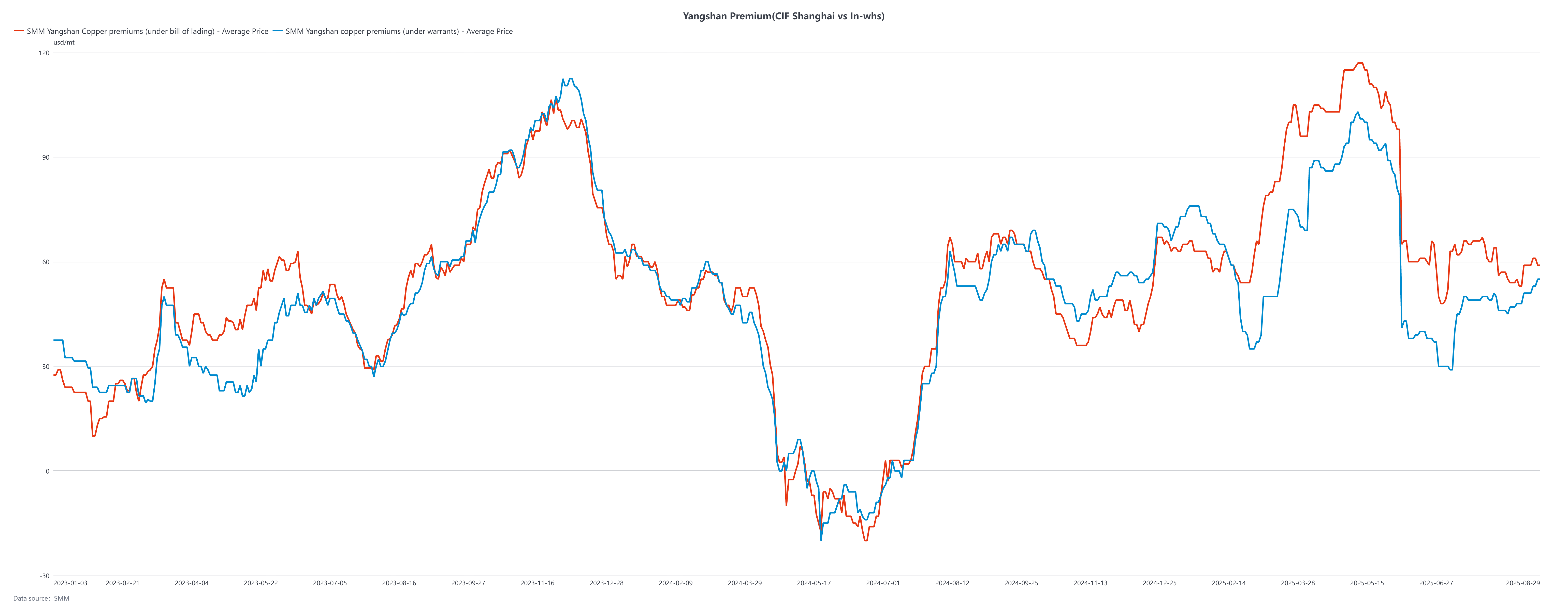

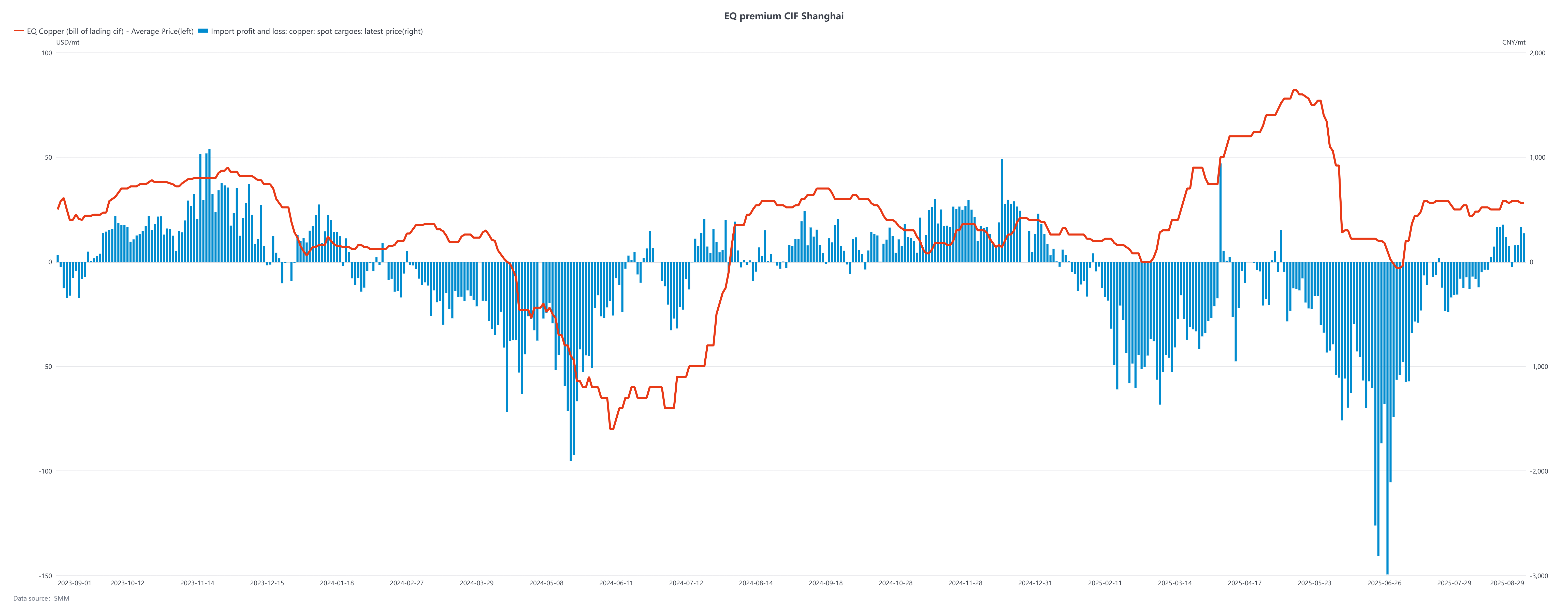

In August, China’s imported copper market remained active, with Yangshan premiums gradually rebounding amid volatility. The average TC/BL premium rose from around $58/mt to $60/mt, while warehouse warrant premiums climbed from $46/mt to $53/mt. EQ copper CIF premiums also strengthened from $24/mt to $28/mt. Trading activity was brisk, with frequent bids and offers from both buyers and sellers, though wide bid-ask spreads meant actual transactions showed only a steady upward shift.

Several factors supported the market’s strength: first, a significant increase in LME inventories widened nearby contango, improving import arbitrage economics and reopening the import window temporarily, prompting some traders to add long arbitrage positions. Second, customs data showed that July copper exports far exceeded expectations, raising market anticipation that some LME stocks could return to China, boosting bullish sentiment. Third, domestic refined copper supply is expected to contract in September, while import growth remains limited, further pushing premiums higher.

Bonded zone inventories trended lower in August, falling from 79 kt at the start of the month to 75 kt by the end. The drawdown was mainly driven by the reopened import window, more active customs clearance by holders, and a recovery in domestic demand. Meanwhile, reduced spot exports from smelters also limited new arrivals into bonded warehouses.

Looking ahead to September, domestic refined output is expected to decline sharply compared with August, with the scrap copper supply gap shifting toward refined copper. Strong SHFE performance and improving import ratios are likely to keep the import window open, supporting continued demand. In the short term, Yangshan copper premiums are expected to move higher.