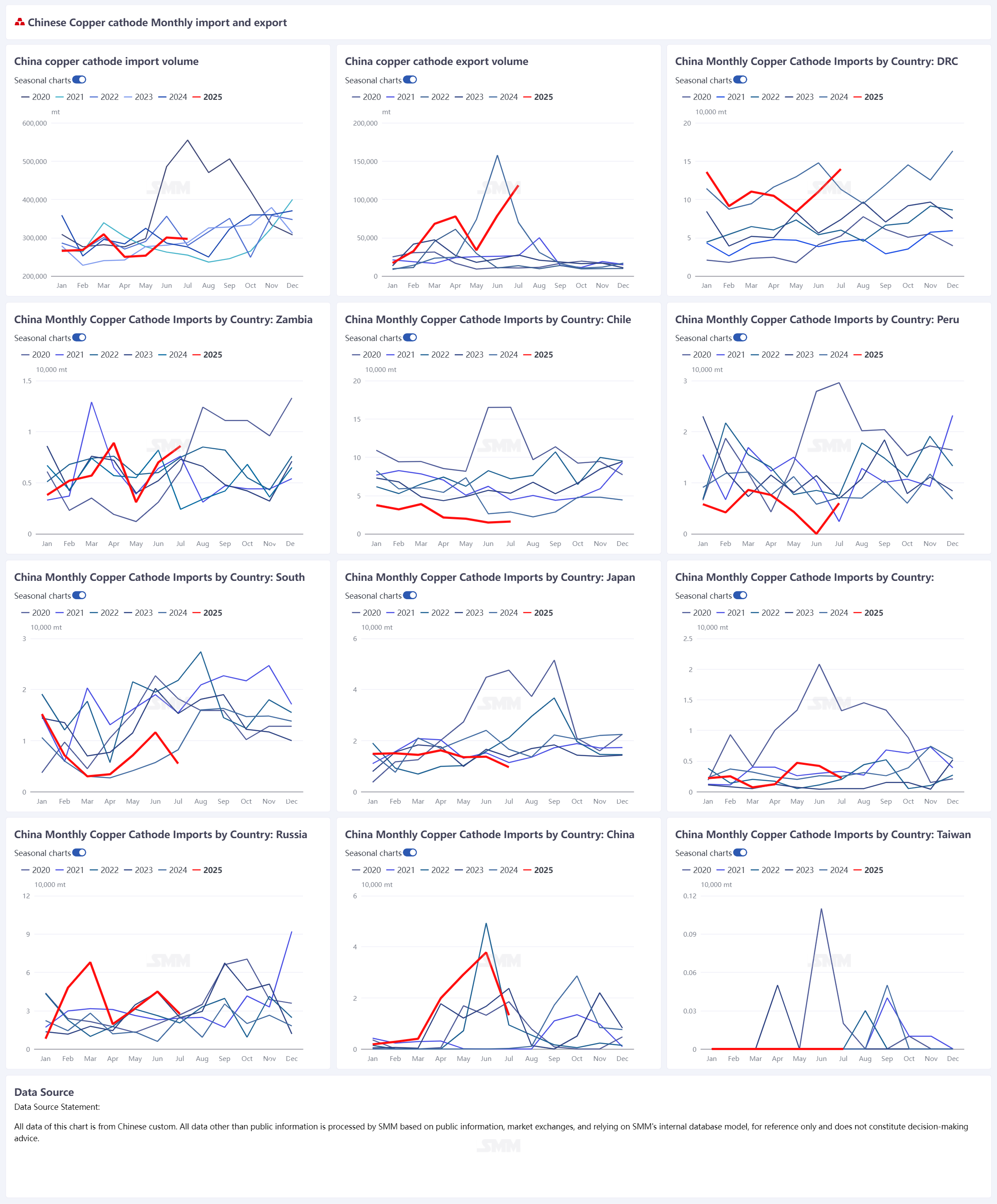

According to customs data, China’s refined copper imports reached 296,900 mt in July 2025, down 1.20% MoM but up 7.56% YoY. Meanwhile, exports surged sharply to 118,400 mt, representing a 49.86% MoM increase and a 69.13% YoY jump. Both import and export volumes exceeded market expectations.

Imports: DRC nearly half, sharp increases from the Netherlands and Peru

By origin, the Democratic Republic of Congo (DRC) remained China’s largest supplier, with July imports of 139,600 mt, accounting for 47.01% of total imports and up 26.75% MoM. Russia ranked second with 27,500 mt (9.27% share), though volumes fell 38.80% MoM. Imports from the Netherlands reached 16,800 mt, soaring 210.20% MoM—market sources indicated these inflows were largely Russian copper previously de-registered from LME warehouses. Peru also recorded a recovery in shipments to 6,000 mt following the end of maintenance at SPCC’s Ilo smelter. In contrast, imports from Chile were only 16,000 mt, down 43.86% YoY.

By trade mode, general trade remained dominant at 145,000 mt, accounting for 48.83% of the total. Imports via bonded zones reached 111,400 mt (37.54%). Processing trade—including both import processing and assembly processing—accounted for roughly 10%, suggesting that processing-related imports remained stable.

Exports: Taiwan, US, and South Korea over 70% of total, with US demand surging

On the export side, China shipped 118,400 mt of refined copper in July, up 49.86% MoM and 69.13% YoY. The main destinations were Taiwan, the United States, and South Korea, which together accounted for more than 70% of the total. Shipments to Taiwan surged to 37,200 mt (31.43% share), up 267.84% MoM; exports to the US stood at 26,300 mt (22.19% share); and South Korea received 25,900 mt (21.87% share), up 54.83% MoM.

Southeast Asian markets also showed robust demand: Thailand and Vietnam imported 6,895 mt and 6,319 mt, respectively, both recording double-digit or higher YoY growth. In addition, Singapore and the Netherlands saw notable increases, consistent with market rumors that Chinese copper was being exported to Europe for swap deals. By trade mode, processing trade and bonded zone logistics dominated, accounting for 53.07% and 46.93% of exports, respectively, while general trade was negligible.

Market outlook: Import margin set to reopen in August

Looking ahead, following the US government’s announcement to impose a 50% tariff on semi-finished copper products effective August 1, the arbitrage between LME and COMEX has effectively ended. However, global trade flows are unlikely to normalize quickly in August, and China’s imports may remain relatively subdued.

With LME inventories continuing to build, relative pricing is gradually improving. As more shipments arrive in mid-to-late August, the import window is expected to reopen. Market activity has already picked up, and Yangshan copper premiums appear to have bottomed, with potential upside ahead. Bonded zone inventories may resume destocking; meanwhile, re-export premiums for bills of lading to the US have normalized, brand price differentials are narrowing, and spot trading is returning to a SHFE/LME ratio-driven logic.

It is expected that some LME stocks will begin to flow back into China, and monthly imports could gradually recover toward the 300,000 mt level.