SMM August 20 News:

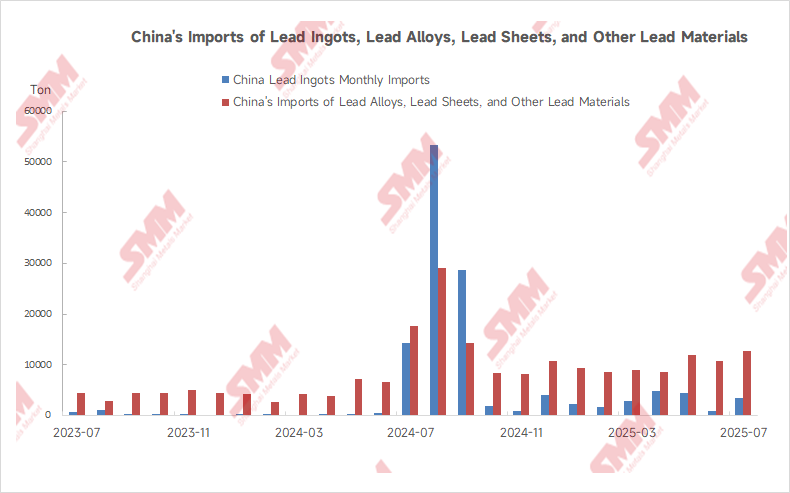

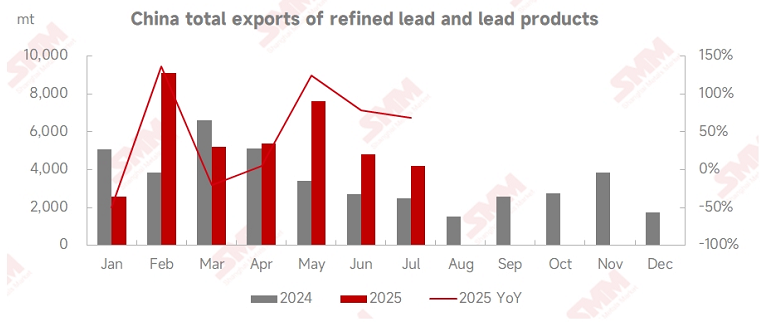

According to data from China Customs, in July 2025, China's refined lead exports were 1,795 mt, down 43.62% MoM and up 408.31% YoY; from January-July, the total exports of refined lead and lead products were 38,947 mt, up 33.17% YoY. In terms of imports, in July, China's refined lead imports were 3,417 mt, and lead alloy imports were 12,784 mt. From January-July, the total imports of refined lead and lead products were 91,329 mt, up 47.89% YoY.

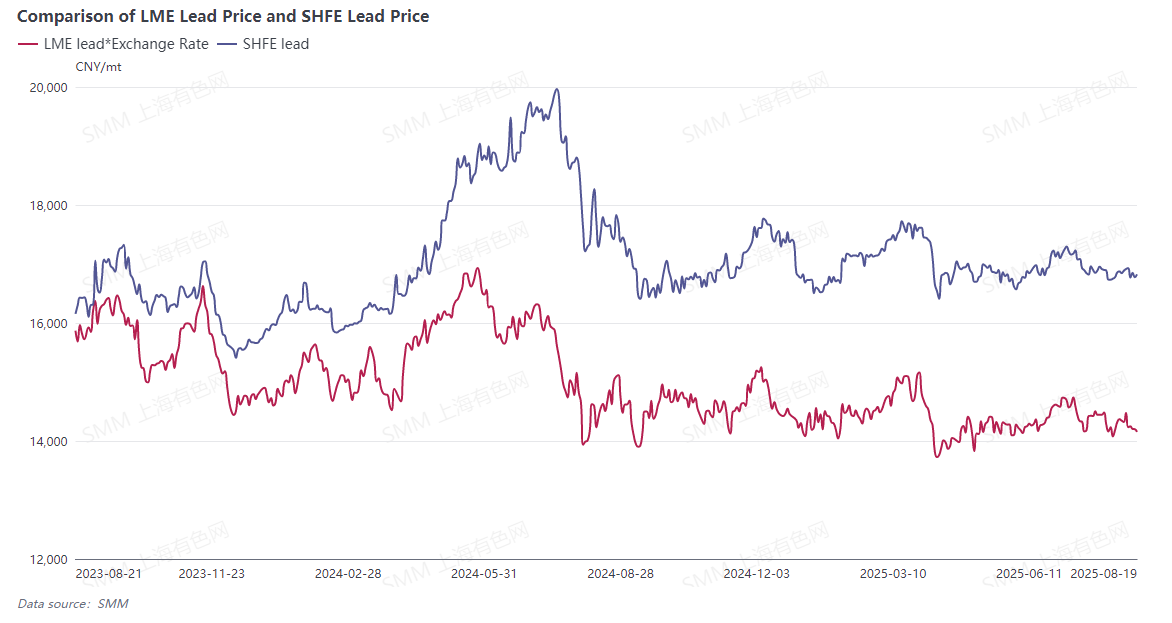

In July, both domestic and overseas lead prices showed a trend of jumping initially and then pulling back. The tariff event and the underperforming peak season for domestic consumption further intensified market pessimism. In early July, overseas lead inventories declined daily, with LME lead inventory falling below 250,000 mt after three months, and LME lead reaching $2,073/mt, while SHFE lead reached 17,340 yuan/mt. By mid-July, LME lead inventory surged, rising above 270,000 mt. Due to the end of the US "reciprocal tariff" suspension period, the US government began notifying countries without trade agreements of new tariff rates starting July 4. The uncertainty of tariff policies heightened concerns about economic recession, leading to a general weakness in non-ferrous metals. Lead prices also gave up most of their gains since late June. Even though there was a temporary supply tightness in the domestic lead ingot market in late July, it did not boost lead prices but only helped them stop falling and stabilize. During this period, the enthusiasm for importing overseas lead decreased, and transactions became sluggish.

In early August, negotiations between the US and multiple countries on new "reciprocal tariffs" were volatile, and the risk of tariffs led to a strong market pessimism. LME lead fell to as low as $1,956/mt, and the most-traded SHFE lead contract dropped to 16,615 yuan/mt. On the 12th, the Tariff Commission of the State Council announced that, to implement the consensus reached during the Sino-US economic and trade talks, based on the "Customs Law of the People's Republic of China," the "Foreign Trade Law of the People's Republic of China," and other laws and regulations, as well as the basic principles of international law, and with the approval of the State Council, starting at 12:01 PM on August 12, 2025, the additional tariff measures specified in the "Announcement of the Tariff Commission of the State Council on Imposing Additional Tariffs on Imports Originating from the United States" (Announcement No. 4 of 2025) would be adjusted. Within 90 days, the 24% additional tariff rate on US imports would be suspended, retaining a 10% additional tariff rate. Thus, the tariff issue temporarily eased, and the impact of macro sentiment on lead prices briefly weakened. From a fundamental perspective, the lead ingot market in August is expected to see an increase in both supply and demand. However, due to the limitations in consumption and raw material supply, it may be difficult to create a significant lead ingot shortage, providing limited support to lead prices and also being unfavorable for lead ingot imports. SMM expects that lead ingot imports in August may remain stable or slightly decrease compared to July.