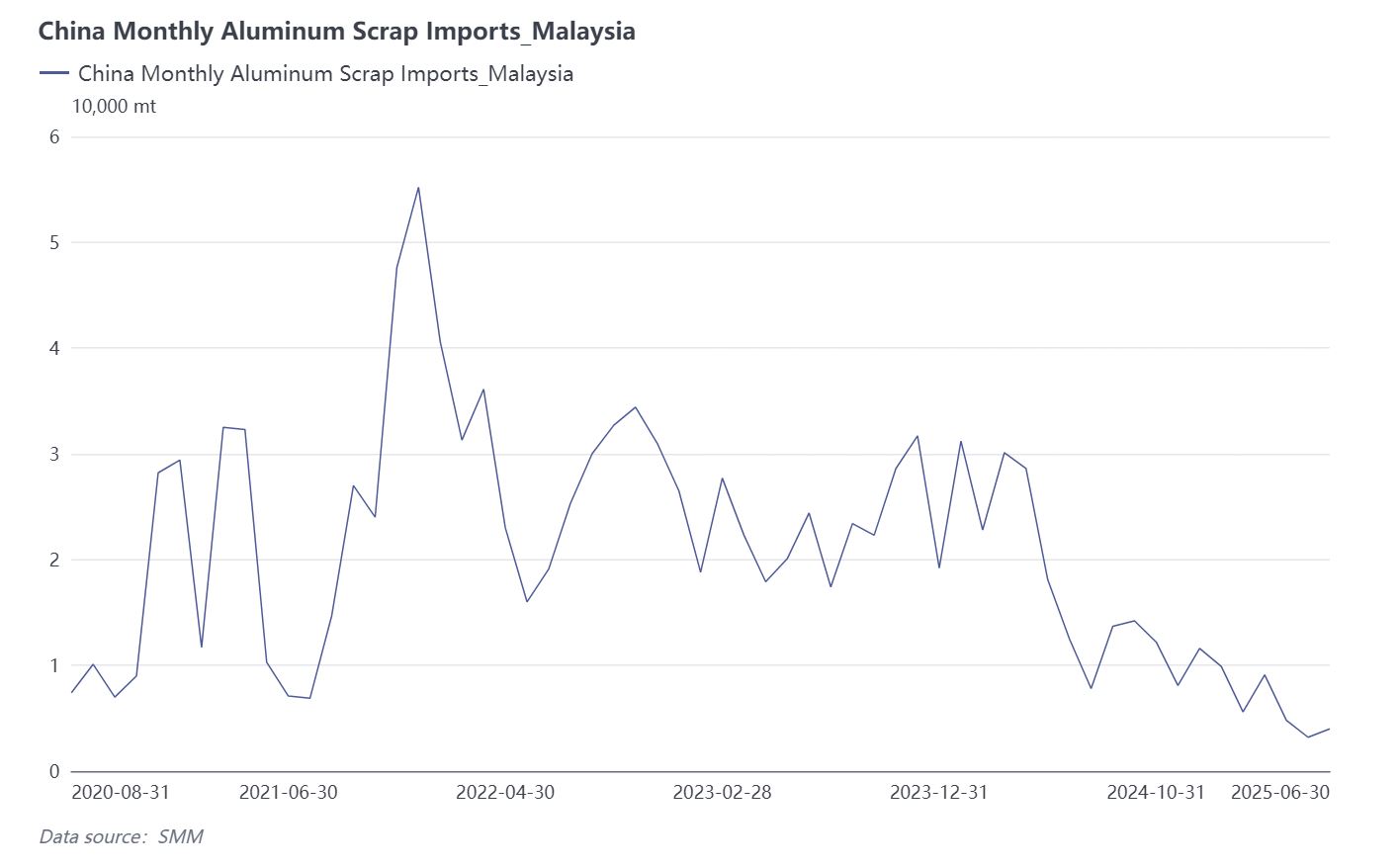

SMM Scrap Aluminum Market Analysis: Four Converging Factors in 2025 Undermine Southeast Asia’s Comparative Advantage

In 2025, Southeast Asia’s scrap aluminum market plunged into a deep contraction, with export volumes dropping sharply. This downturn is expected to persist throughout the year. A synthesis of the macro environment and industry operations reveals four primary pressures: sudden tightening of local policies and geopolitical risks, rapid expansion of regional recycled-aluminum demand, port congestion coupled with declining logistics efficiency, and the imposition of steep U.S. tariffs. The combined resonance of these factors makes it unlikely that Southeast Asia’s export competitiveness in scrap aluminum can recover in the short term.

First, Malaysia and Thailand both faced simultaneous policy and geopolitical shocks in 2025, narrowing their export channels. In July, Malaysia’s Home Ministry and the Anti-Corruption Commission launched “Operation Metal Storm,” a criminal probe into export-licensing chains for scrap metals. Multiple exporters, customs officers, and local government officials were detained. The Royal Malaysian Customs Department began manually re-verifying all scrap-metal declarations, stretching clearance times from 3–5 business days to 12–15 business days, and triggering spikes in demurrage, storage, and financing costs. That same month, an armed standoff erupted along the Trat–Koh Kong border between Thailand and Cambodia, prompting Thailand to close the Aranyaprathet–Poipet crossing. As a result, overland shipments from eastern Thailand to Laem Chabang Port were halted, freight forwarders hiked rates by 25%, and shippers were forced to reroute via Hat Yai–Penang–Port Klang—adding 480 kilometers by land. Feedback from market participants indicates that scrap-aluminum transactions collapsed after July; only a relaxation of border tensions and a return to routine policy reviews by late 2025 can potentially restore exports.

Second, regional demand for recycled aluminum has expanded structurally, exerting a strong pull on scrap-aluminum supplies. Since 2022, Malaysia has rolled out systematic incentives for its electric-vehicle supply chain: from 2022 to 2027, locally assembled EVs are exempt from profile-import duties and the 10% excise tax, while battery-PACK components enjoy zero VAT on raw-material imports. Thailand followed in 2024 with its EV3.5 incentive scheme, extending purchase-tax waivers and subsidies beyond EVs to include pickups and motorcycles. Scrap aluminum accounts for up to 32% of the average aluminum usage in EV body panels, battery trays, and chassis components; downstream sectors such as building curtain walls, food packaging, and consumer-electronics heatsinks are growing at a 6%–9% CAGR. As a result, local scrap-aluminum procurement prices in Malaysia and Thailand surged. By August 2025, the ex-works price for ADC12 scrap in both countries had climbed to USD 2,555 per ton—which is higher than Chinese imported ADC12 prices CIF of USD 2,470 per ton at the same time—erasing export-economics advantages. Several large recycler-smelters have already launched integrated melting-extrusion projects to lock in domestic feedstock, further depleting export availability.

Third, port congestion and deteriorating shipping efficiency have amplified time and capital costs on the logistics front. Since the Red Sea crisis erupted in October 2023, vessels on the Eurasian mainline have been forced to reroute around the Cape of Good Hope, adding 5,500–11,100 kilometers to voyages and delaying schedules by 10–14 days. In a bid to save on fuel and canal surcharges, carriers have adopted “ad hoc port skipping,” wreaking havoc on berth windows at Port Klang (Malaysia) and Laem Chabang (Thailand). As of July 2025, average vessel-waiting times at Laem Chabang stretched to 10–24 hours, while Port Klang’s West Port reached 40 hours. To mitigate risk, traders have shifted load ports to India’s Mundra or China’s Qinzhou, conceding market share from traditional Southeast Asian gateways.

Finally, U.S. tariff policies have directly choked off demand. In March 2025, President Trump issued an executive order imposing punitive tariffs of up to 50% on imported aluminum products. Southeast Asian countries have long served as suppliers and transshipment hubs for U.S. aluminum imports including scrap. Once the tariffs took effect, export offers from Malaysia and Thailand instantly lost competitiveness. Scrap aluminium instantly became highly demanded in the United States, leading to a decrease in the scrap flow from Europe and the Americas and Asia, where demand is increasing and export channels continue to narrow.

In summary, the confluence of tightened policy and geopolitical risks, booming regional recycled-aluminum demand, worsening port congestion, and steep U.S. tariff barriers has driven Southeast Asia’s scrap aluminum market into deep contraction in 2025. In the short term, traders must adapt to a “low-volume, high-cost, slow-turn” reality, directing exports mainly to domestic and intra-regional consumers. Only adjustments to external tariff policies, an easing of regional tensions, and expansions in port infrastructure can gradually restore Southeast Asia’s comparative advantage in scrap-aluminum exports.