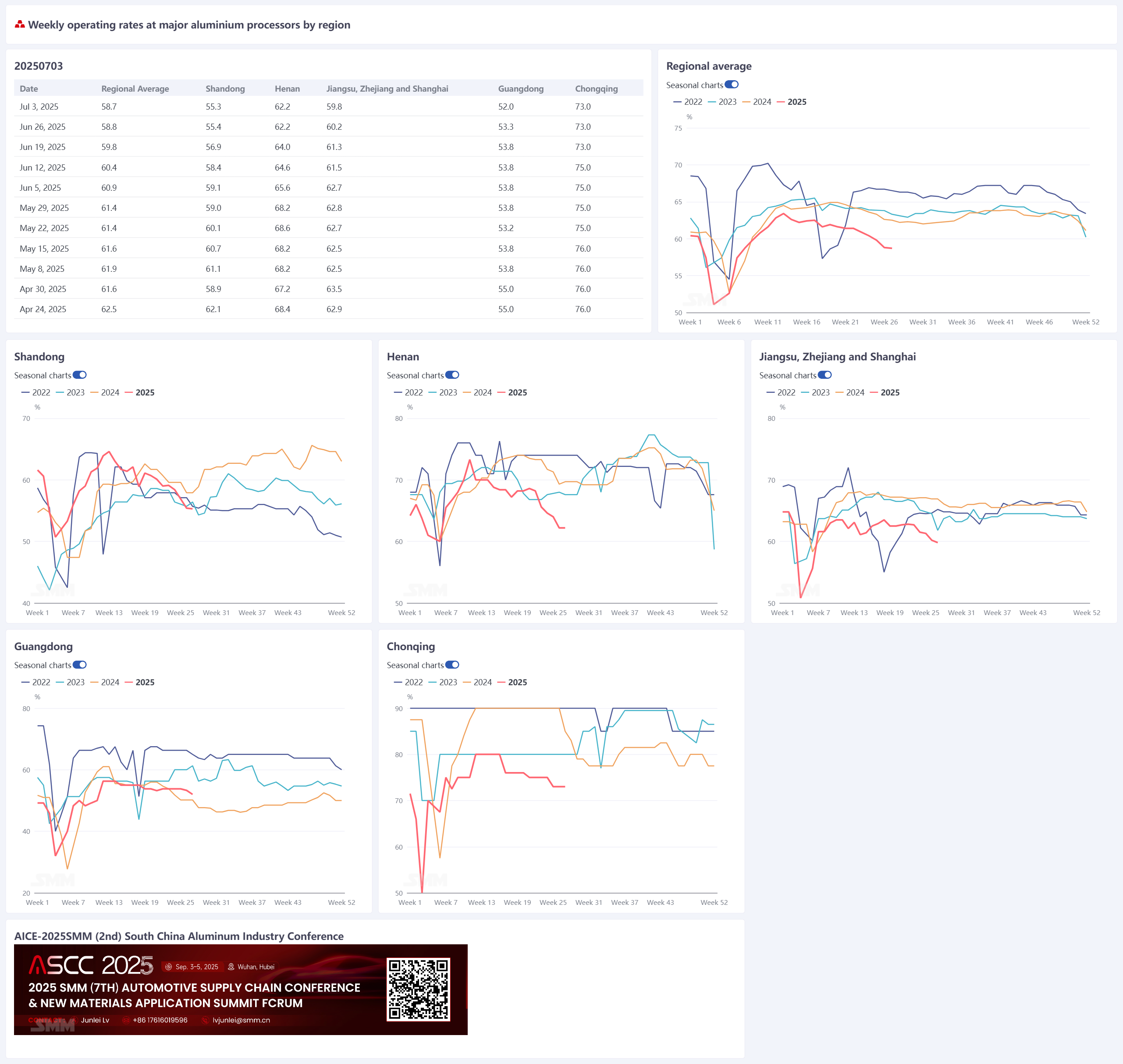

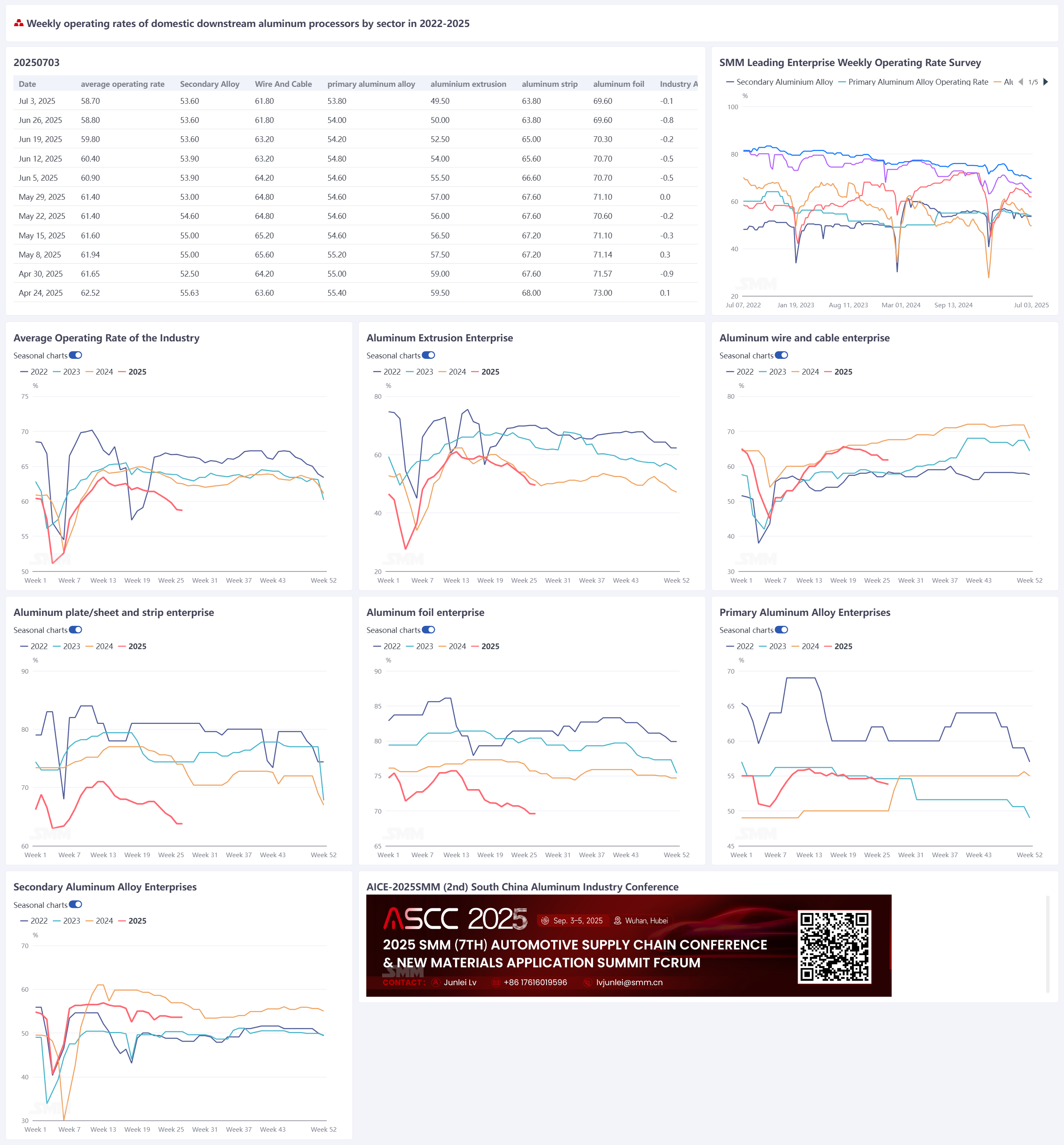

July 3, 2025:

Affected by factors such as the high-temperature off-season, high aluminum prices, insufficient profit margins, and weak downstream demand, the operating rate of the aluminum processing industry this week fell by 0.1 percentage point week-on-week (WoW) to 58.7%. By sector:

-

Primary Alloy: Despite continuous marginal support from aluminum liquid alloying tasks and conversion strategies for aluminum rods, enterprises exhibit low expansion willingness and limited capacity expansion momentum against the backdrop of the off-season. The operating rate may continue to weaken.

-

Aluminum Plate/Sheet/Strip: Faced with the dilemma of insufficient orders and high inventories, producers proactively reduced output, putting pressure on the overall industry operating rate.

-

Aluminum Wire & Cable: Enterprises remain pessimistic about July orders, but the expectation for State Grid order deliveries in the second half of the year remains positive, potentially providing some support to future operating rates.

-

Aluminum Extrusions: Generally experiencing weak new order intake due to the consumption off-season and severe internal competition in processing fees, enterprises face pressure on their operating rates.

-

Aluminum Foil: Terminal demand shows no signs of short-term recovery under the influence of the traditional consumption off-season. The operating rate may continue to decline.

-

Recycled Aluminum Alloy: Pressure on both the demand and cost sides has intensified. Some recycled aluminum enterprises have adopted measures such as short-term furnace maintenance or output reduction. SMM expects the downstream aluminum processing weekly operating rate may fall by 0.4 percentage points WoW to 58.3% next week.

Primary Alloy: This week, the operating rate of the primary aluminum alloy industry edged down slightly by 0.2 percentage points WoW to 53.8%, continuing its weak and stable trend. Although aluminum liquid alloying tasks and aluminum rod conversion strategies continue to provide marginal support, constrained by multiple factors including weak terminal demand, insufficient new orders, thin profit margins, and the approaching high-temperature holidays, enterprises exhibit low expansion willingness and limited capacity expansion momentum. Coupled with the uncertainty brought by the approaching July 9th US-China tariff deadline, a substantial industry recovery still awaits the clarification of trade policies and effective mitigation of cost pressures. SMM expects the industry to continue its game pattern dominated by "aluminum liquid allocation with significant demand drag" in the near term, with the operating rate likely to show a continuous weakening trend.

Aluminum Plate/Sheet/Strip: This week, the operating rate of leading aluminum plate/sheet/strip enterprises was recorded at 63.8%. Aluminum prices remained high this week, sustaining strong downstream customer wait-and-see sentiment and poor destocking of finished product inventories. Terminal demand remained persistently weak, with key consumption sectors like automotive and electronics starting to show fatigue, leading to a contraction in new order volumes. Regarding processing fees, in Gongyi, due to inventory pressure, processing fees for cast-rolled coils have fallen below cost levels, halving compared to the peak season, leaving no room for further price-for-volume strategies. Producers proactively reduced output facing the dilemma of insufficient orders and high inventories. Although leading enterprises strive to adjust structures to maintain stability, the overall industry operating rate faces significant pressure. With high finished product inventories, the deepening traditional off-season, and persistently high aluminum prices, the aluminum plate/sheet/strip operating rate is expected to continue declining in the short term.

Aluminum Wire & Cable: This week, the operating rate of leading aluminum wire and cable enterprises was 61.8%, unchanged from last week. According to enterprise feedback, there is apprehension towards current high prices, and the focus remains on reducing raw material and finished product inventories; industry sentiment towards operating has not improved. Simultaneously, enterprises hold a pessimistic outlook for July orders, and terminal pickup pace has slowed. Looking ahead, although current enterprise operations are weak, backlogged orders still provide some support, limiting significant downside for the operating rate. While July expectations are weak, the outlook for State Grid order deliveries in the second half of the year remains positive, potentially providing some support for future operations. It is expected that the aluminum wire and cable operating rate will maintain its weak trend in the near term.

Aluminum Extrusions: This week, the national extruded profiles operating rate fell slightly by 0.5 percentage points WoW to 49.5%.

-

Construction Profiles: Overall operating rate at sample enterprises declined slightly WoW. SMM research indicates that leading enterprises in Central China, South China, and East China all reported weak growth in new orders. Coupled with persistently declining processing fees for powder coating and thermal break profiles, putting pressure on profits, the building profiles operating rate fell again to around 40% this week.

-

Industrial Profiles: Operating rate declined slightly WoW. Some leading PV frame profile enterprises in East China, Southwest China, and Hebei reported relatively saturated orders in the first week of July, with backlogged orders providing some support for the operating rate; a few plants saw a slight WoW increase. However, uncertainty regarding subsequent orders remains high, and output reduction risks persist. Operations are expected to weaken by mid-July.

-

Automotive Profiles: Entering July, some large and medium-sized sample enterprises in East and Central China reported a strong off-season atmosphere, with new orders still weak this week. However, a few East China enterprises reported relatively saturated foreign orders, maintaining operations around 60%. Meanwhile, some enterprises in East China that previously shifted from building to industrial profiles reported severe internal competition in industrial profiles. After comprehensive assessment, they decided to shut down industrial profile lines and optimize staffing. Overall, affected by the consumption off-season, aluminum extrusion enterprises generally face weak new orders and pressure on operating rates. SMM will continue to monitor the actual progress of order fulfillment across sectors.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises was recorded at 69.6%. Overall aluminum foil market demand continued to weaken, and the industry operating rate remained under downward pressure. By product:

-

Packaging foil demand is weak and mired in price competition.

-

Air-conditioning foil has large scale but relies heavily on price-for-volume strategies to barely sustain.

-

Battery foil saw some enterprises increasing output, but downstream output reduction plans led to weakening orders, insufficient to offset the overall downturn.

As the traditional consumption off-season (July-August) sets in, terminal demand shows no signs of recovery. The aluminum foil industry operating rate is expected to continue its downward trend in the short term.

Recycled Aluminum Alloy: This week, the operating rate of leading recycled aluminum enterprises remained stable at 53.6%. Entering July, pressure on the demand side for recycled aluminum intensified significantly. The high-temperature off-season and high aluminum prices continued to impact downstream orders, prompting some die-casting enterprises to reduce output. Cost pressures also intensified simultaneously. Prices of key raw materials like scrap aluminum, silicon, and copper collectively rose, continuously pushing up ADC12 raw material costs. However, product selling prices struggled to keep pace, leading to a further widening of theoretical industry losses and significantly increased production and operational pressure on enterprises. Squeezed by both scrap aluminum supply shortages and weak market demand, some recycled aluminum enterprises adopted measures like short-term furnace maintenance or output reduction. Nevertheless, leading sample enterprises managed to maintain current production scales, but future operating rates face downward pressure.