SMM June 29th's News:

The Aluminum Sheet/Strip industry PMI composite index remained in contraction territory, with domestic end-user demand weakening further. Downstream customers slowed their pickup pace, finished product inventory indices stayed elevated, compounded by lackluster export recovery. Companies reduced production, necessitating continued monitoring of destocking progress and policy stimulus effects. Aluminum foil producers saw profit margins squeezed by their "price-for-volume" strategy during the month, putting corporate cash flow under pressure. Coupled with downstream production cuts dragging on orders, July is unlikely to see improvement. In construction profiles, companies reported the property market has yet to recover, new orders were severely insufficient, and backlogged orders couldn't support monthly production. Construction aluminum profile PMI is expected to remain below the boom-bust line in July as the sector stays mired in the traditional off-season. For industrial profiles, aside from a few segments with stable customer bases unaffected by the off-season, the off-season atmosphere prevailed elsewhere. Against the backdrop of intense processing fee competition, corporate profitability was squeezed. Little improvement is expected in July, requiring close attention to actual order fulfillment. In aluminum cable/wire, the next delivery cycle has yet to arrive, with insufficient market rigid demand. Cable manufacturers plan to reduce both raw material and finished goods inventories to ease capital pressure. In the primary alloy sector, constrained by the triple pressures of weak traditional off-season demand, unresolved China-US tariffs, and negative feedback from high aluminum prices, industry downward pressure intensified significantly, and the PMI may face further pressure. For recycled alloys, despite the formal listing of cast aluminum alloy futures on June 10 boosting market trading activity, actual terminal consumption remained sluggish and failed to effectively support the market.

Details by product type:

Details by product type:

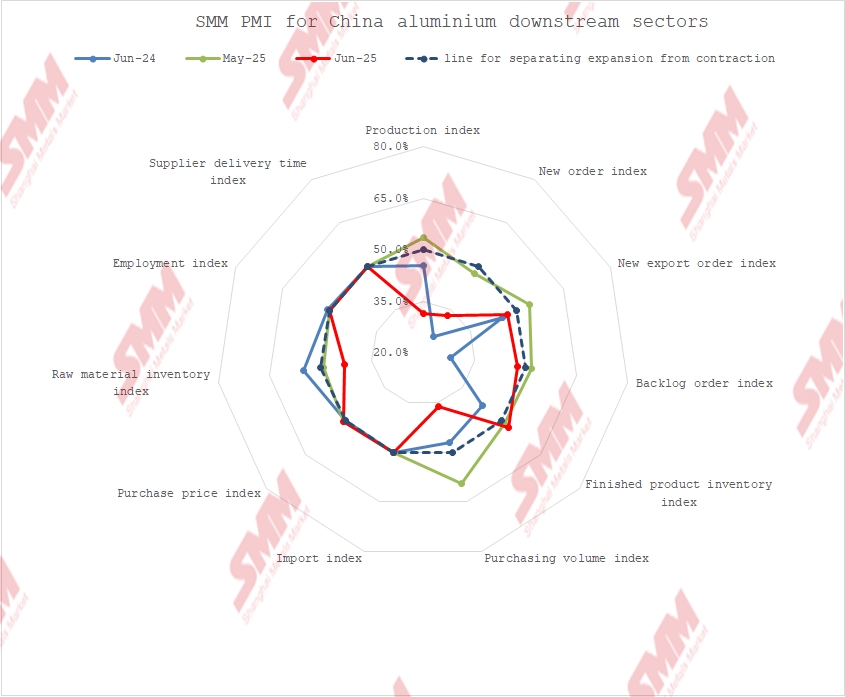

- Aluminum Sheet/Strip: The June China Aluminum Sheet/Strip industry PMI composite index recorded 39.1%, plunging 10.5 percentage points from the previous month, deeply entrenched in contraction. Sub-indices showed both the production index (29.2%) and new orders index (29.2%) were significantly below the boom-bust line, reflecting intensified weakness in domestic end-user demand, particularly a month-on-month decline in construction sector orders. Compounded by high aluminum prices hovering (approaching 21,000 yuan/ton), downstream customers slowed their pickup pace, and the finished product inventory index remained high (60.8%), forcing companies to cut production. Although the new export orders index (42.8%) was higher than the production index, export support was limited. Benefits from China-US consultations only supported sectors like home appliances and kitchen/bathroom, insufficient to offset overall consumption weakness. The purchasing volume index (44.5%) and raw material inventory index (46.1%) indicated cautious restocking by enterprises. Overcapacity and insufficient domestic demand heightened the risk of price wars. Looking ahead, with the off-season deepening and inventory overhang, the aluminum sheet/strip PMI is expected to remain weak. Progress on production cuts, destocking, and policy stimulus effects warrant attention.

- Aluminum Foil: The June aluminum foil industry PMI composite index was 45.3%, edging down month-on-month but remaining in contraction. Among sub-indices, both the production index (41.2%) and new orders index (41.2%) were below the boom-bust line. The main reason was packaging foil demand plummeting since April, mired in price wars (processing fees as low as 5,800 yuan/ton). Companies' "price-for-volume" strategy squeezed profit margins, and the finished product inventory index (52.8%) remained under pressure. The new export orders index (47.3%) contracted, indicating insufficient export support. Normal production scheduling for battery foil and brazing foil provided partial support, but downstream production cut plans dragged on orders. High aluminum price volatility had limited impact (monthly average price settlement buffered risk), but destocking fell short of expectations, leaving an inventory crisis looming. Aluminum foil demand is expected to weaken overall in July, with the industry PMI forecast to contract further. Processing fees will stay under pressure, and corporate cash flow faces tests.

- Construction Profiles: The June construction aluminum profiles PMI index edged down to 40.44%, falling below the boom-bust line. The construction profiles industry officially entered its traditional off-season. Most enterprises in Shandong, East China, Hebei, and South China reported significant production declines in June. Companies reported the property market has yet to recover, new orders were severely insufficient, and backlogged orders couldn't support monthly production. This caused the production index to plunge to 29.6% and the new orders index to fall to 37.69%, dragging the purchasing volume index down to 29.15%. Compounded by intense competition in spraying and thermal break processing fees, companies widely adopted low raw material inventories to maintain healthy cash flow, pushing the raw material inventory index down to 34.75%. Overall, the construction profiles industry is expected to remain shrouded in the traditional off-season atmosphere in July, with the construction aluminum profiles PMI continuing below the boom-bust line.

- Industrial Profiles: The June industrial profiles industry PMI composite index recorded 37.61%, falling sharply below the boom-bust line. Looking at sub-indices: the production index was 30.33%, new orders index 29.0%. According to SMM, leading PV frame manufacturers in East China reported significant output declines in June, coupled with expectations of lower new orders in July, leaving end-of-month production orders unable to connect with next month's. Meanwhile, although other industrial profiles like rail transit, aerospace profiles, and 3C deep processing maintained stable customer bases and normal production during the month, auto parts companies reported intense industry competition persists, with severely insufficient backlogged orders and continuously declining operating rates. Processing companies also indicated current processing fees may decline further, potentially further compressing corporate profitability. Enterprises showed insufficient enthusiasm for raw material stockpiling, with most maintaining only safety stocks. This caused the purchasing volume index to drop to 21.05% and the raw material inventory index to fall to 28.68%. The industrial profiles industry PMI is expected to operate weakly, with the industrial aluminum profiles PMI continuing below the boom-bust line. SMM will continue to monitor actual order fulfillment.

- Aluminum Cable/Wire: The June domestic aluminum cable/wire industry PMI composite index recorded 40.2%. After running above 50 for four months, the index fell back below 50, indicating a slight industry slowdown. Entering June, the first half State Grid concentrated delivery cycle ended, replaced by slow new order matching. Industry shipment volumes shrank, and corporate operating rates fell noticeably, with the production index recording 37.11%. For new orders, while some State Grid orders saw concentrated bidding openings in early June, the pace of State Grid bidding slowed significantly in mid-to-late June. Consequently, the new orders index recorded 31.42%, indicating a clear month-on-month decline from May. On procurement, aluminum prices trended higher throughout June. However, reduced shipments and lower operating rates weakened rigid demand and slowed procurement pace. Companies are reducing raw material inventories, reflected in the raw material inventory index of 43%. The finished goods inventory index recorded 37.76%, showing companies are currently in a phase of reducing finished goods inventory to ease operational capital pressure. Compounded by the next delivery cycle not yet arriving, companies maintain a wait-and-see attitude. Looking to July, industry shipments are expected to decline further, market rigid demand appears insufficient, and coupled with high aluminum prices, cable manufacturers aim for dual reductions in both raw material and finished goods inventories to alleviate capital pressure. The July 2025 aluminum cable/wire PMI index is expected to operate below the boom-bust line.

- Primary Alloy: The June primary aluminum alloy PMI recorded 36.5%, falling sharply by 5 percentage points month-on-month from May. It remained below the boom-bust line with deepening contraction, indicating significantly intensified industry downward pressure. The core contradiction lies in weak domestic demand and cost pressure: both the production index (22.9%) and new orders index (22.9%) hit new lows for the year, reflecting off-season domestic demand contraction combined with high aluminum prices severely suppressing terminal pickup willingness and new orders. Simultaneously, the high product inventory index (58.8%) contrasted with the low purchasing volume index (26.5%), highlighting passive inventory accumulation by enterprises, cautious procurement, and capital pressure transmission. On exports, although the new export orders index (50.0%) was flat with the boom-bust line, relying on structural support from alternative channels like Mexico couldn't offset declining US orders and overall weakening external demand. Production within the month showed "stable early, falling later": orders were temporarily stable in early June, but persistently high aluminum prices in mid-to-late June and seasonal factors slowed pickups. Some companies marginally reduced production due to inventory and capital pressures, and most sample firms have planned production cuts for July. Looking ahead, constrained by the triple pressures of weak traditional off-season demand, unresolved China-US tariffs, and negative feedback from high aluminum prices, the industry's weak and stable pattern is hard to break. The PMI may face further pressure, with substantive recovery awaiting clarification on trade policies and effective mitigation of cost pressures.

- Recycled Alloy: The June recycled aluminum industry PMI edged up month-on-month to 45.0%, but remained below the boom-bust line. Recycled aluminum demand deepened into the off-season in June. Weak terminal order growth constrained ADC12 price upside, while low-priced supply hitting the market further intensified competitive pressure. Despite the formal listing of cast aluminum alloy futures on June 10 boosting market trading activity, actual terminal consumption remained sluggish and failed to effectively support the market. Faced with insufficient new orders and production losses due to high raw material prices, the overall operating rate of the recycled aluminum industry declined again in June. Looking to July, the off-season effect persists. Terminal automakers may reduce production plans due to scheduling high-temperature holidays or facing finished goods inventory pressure. This is expected to further suppress growth in new orders for recycled aluminum plants and their operating levels. The July industry PMI is forecast to remain below the boom-bust line.

Brief Commentary:

Brief Commentary:

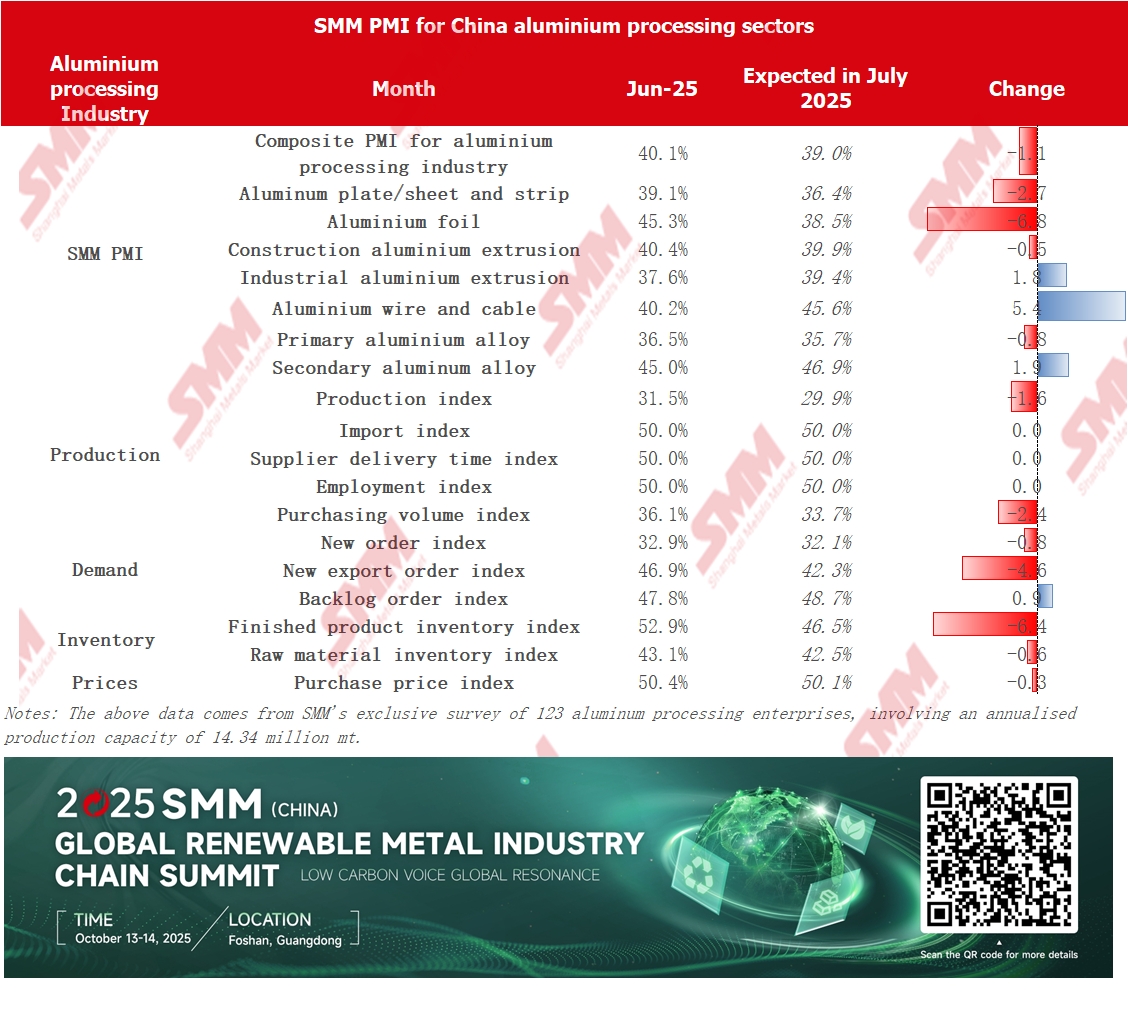

The aluminum processing industry was thick with off-season atmosphere in June, with all sub-sectors generally under pressure. The June aluminum processing industry PMI composite index recorded 40.1%, falling below the boom-bust line, down 9.7 percentage points month-on-month and 1.5 percentage points year-on-year. The main reasons were the strong off-season sentiment combined with high and volatile aluminum prices, leading to weak terminal demand and sluggish new orders, prompting many companies to choose production cuts. By sector: The aluminum sheet/strip industry PMI continued to contract, affected by weak domestic demand, high inventories, and poor exports. Companies have implemented production cuts; subsequent destocking progress and policy effects require attention. Meanwhile, aluminum foil producers faced pressure on both profit margins and cash flow due to their "price-for-volume" strategy, compounded by downstream production cuts dragging on orders. Little improvement is expected in July. For construction profiles, property market weakness caused severe scarcity of new orders. Insufficient backlogged orders couldn't support production, and the sector is deeply mired in the traditional off-season. Its PMI is expected to stay below the boom-bust line. The industrial profiles sector showed divergence: apart from a few segments with stable customers, the overall off-season atmosphere was strong. Fierce competition in processing fees continued to squeeze corporate profits. The outlook for July is similarly pessimistic, requiring close attention to actual order fulfillment. In the aluminum cable/wire market, rigid demand is insufficient as the next delivery cycle hasn't arrived. Manufacturers plan to reduce both raw material and finished goods inventories to ease capital pressure. Primary alloys face the triple pressures of weak traditional off-season demand, unresolved China-US tariffs, and negative feedback from high aluminum prices. Industry downward pressure has intensified significantly, and the PMI may face further pressure. Although trading activity improved in the recycled alloy sector due to the listing of cast aluminum alloy futures, the sluggish actual terminal consumption failed to provide effective market support.