SMM August 11 News:

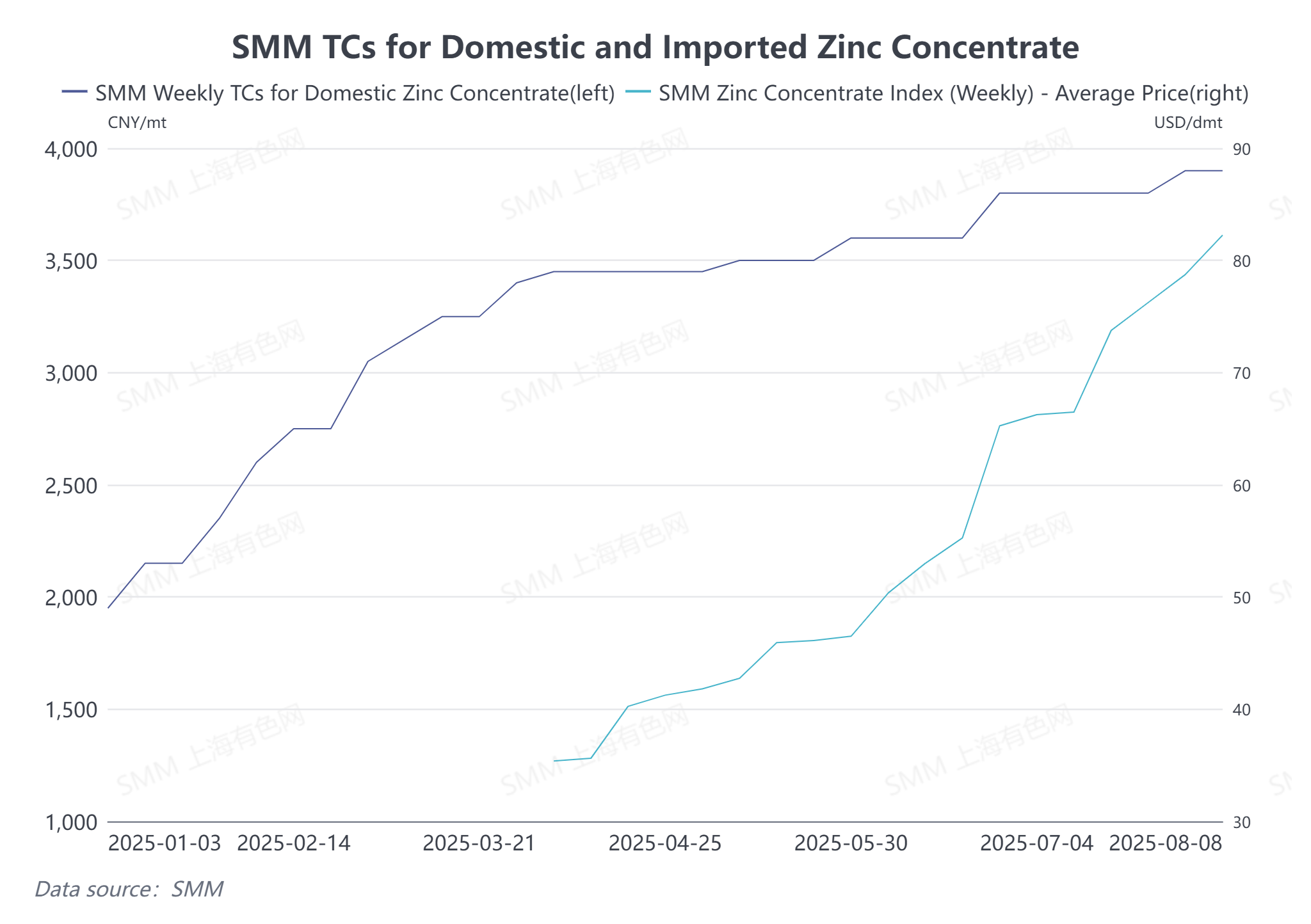

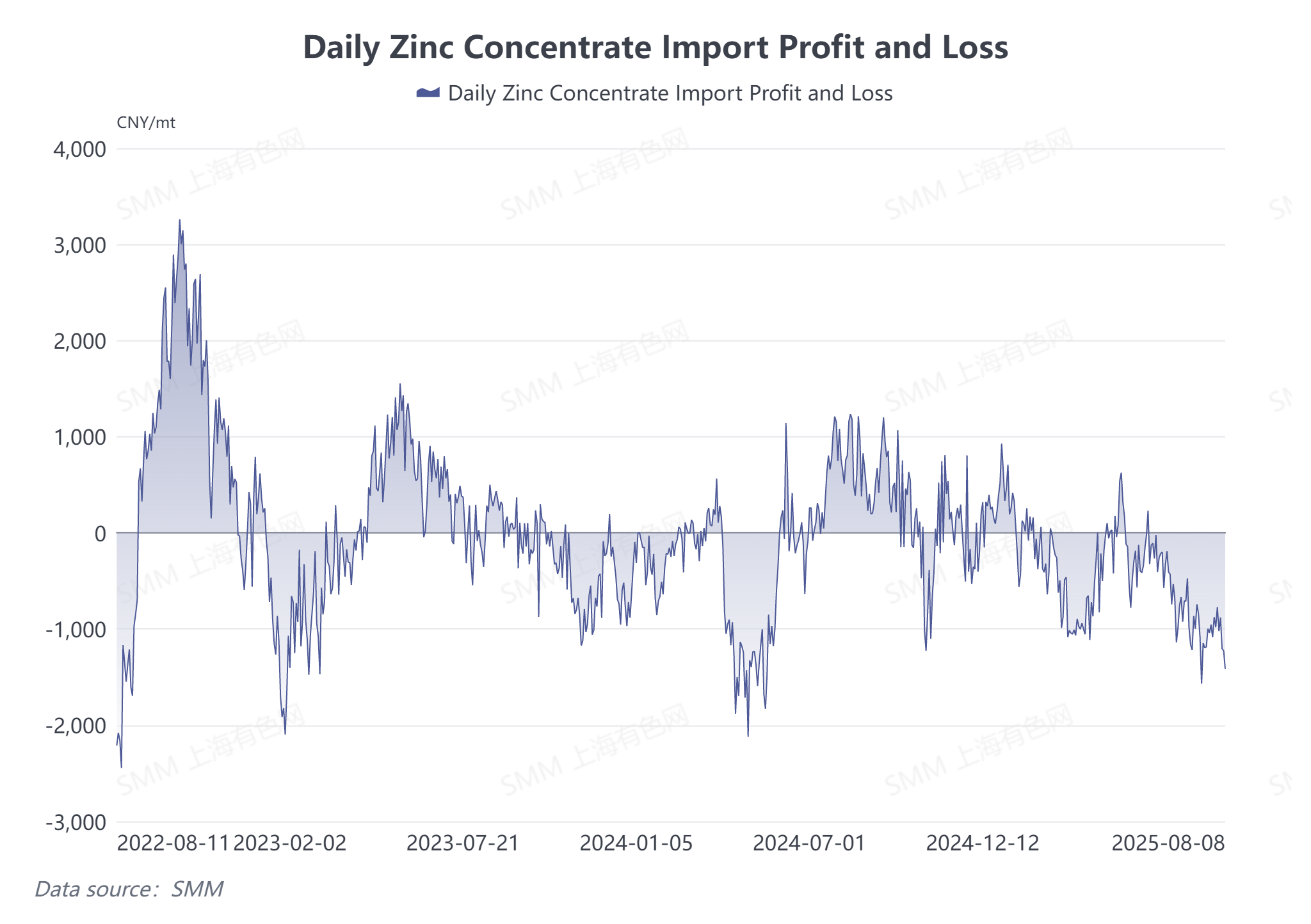

As of August 8, the domestic zinc concentrate processing fee stood at 3,900 yuan/mt (metal content), while the imported zinc concentrate index surged to $82.25/dmt, marking increases of approximately 2,000 yuan/mt (metal content) and $100/dmt, respectively, compared to the beginning of the year. The overall increase has been remarkably significant. Why have imported zinc concentrate processing fees been rising? What is the outlook going forward.

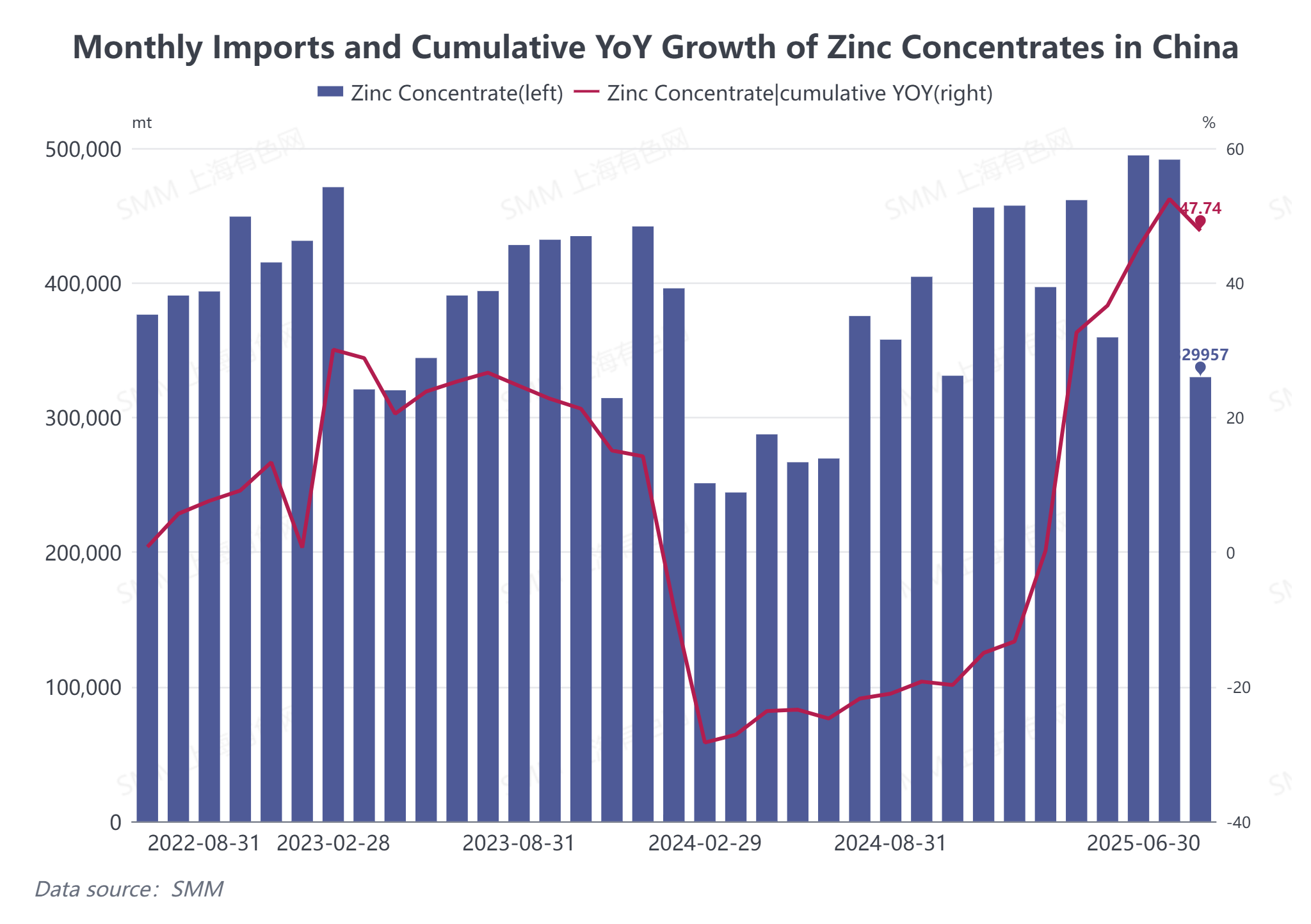

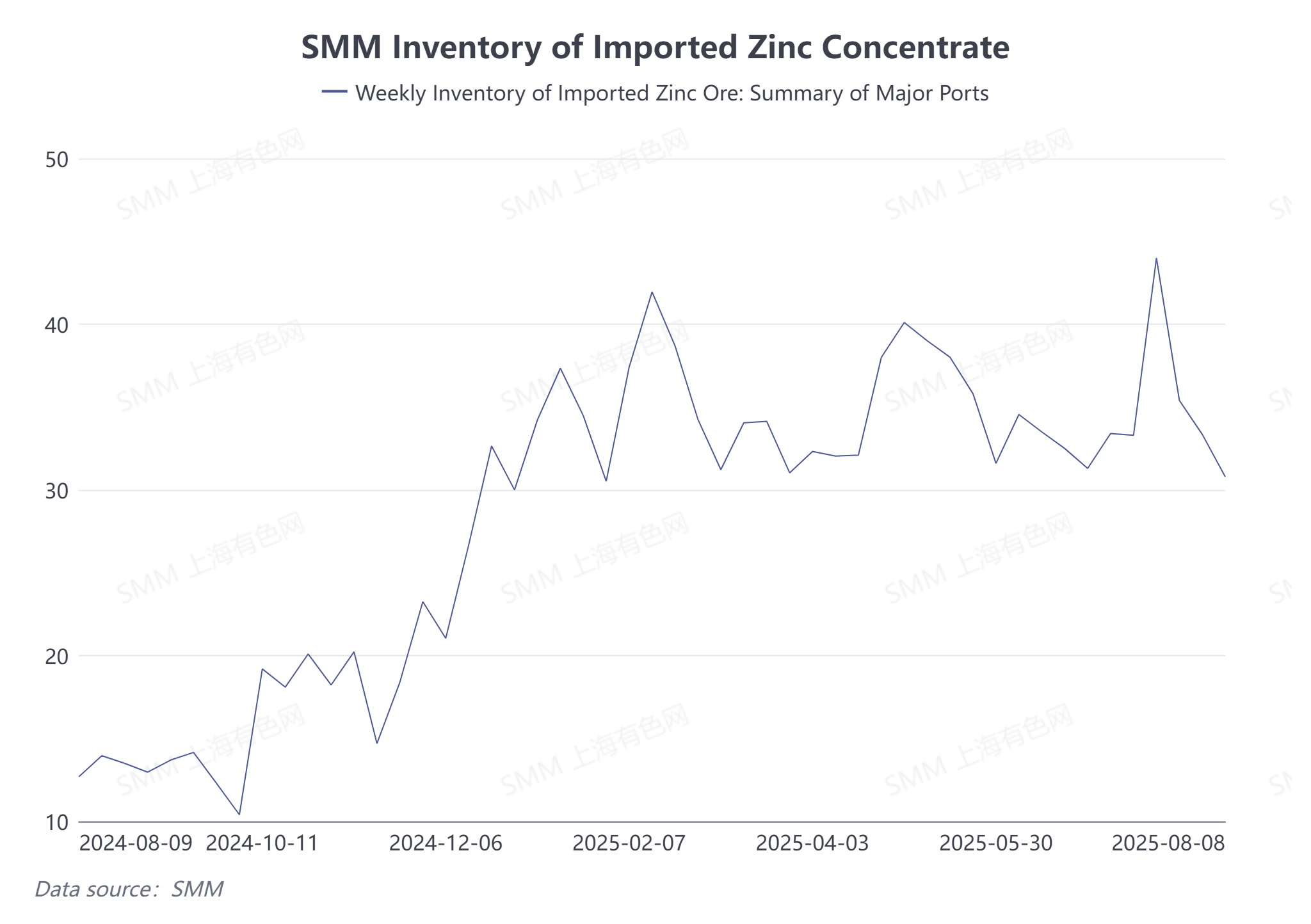

From the supply side perspective. With the release of new overseas zinc mine capacities, such as Kipushi and Oz, and the recovery of production from overseas zinc mines like Antamina and Tara, China's imports of zinc concentrate in the first half of 2025 have increased significantly compared to last year. According to data from the General Administration of Customs, China imported a total of 2.5339 million mt of zinc concentrate from January to June 2025, representing a cumulative YoY increase of 47.74%. Additionally, domestic zinc mines that had previously halted production gradually resumed operations in the first half of the year, continuously supplementing the overall domestic ore supply. The inventory level of zinc concentrate at Chinese ports basically fluctuated above 300,000 mt in the first half of the year, which also confirmed the relatively abundant domestic zinc concentrate supply. Consequently, domestic and overseas processing fees have been boosted and continue to rise.

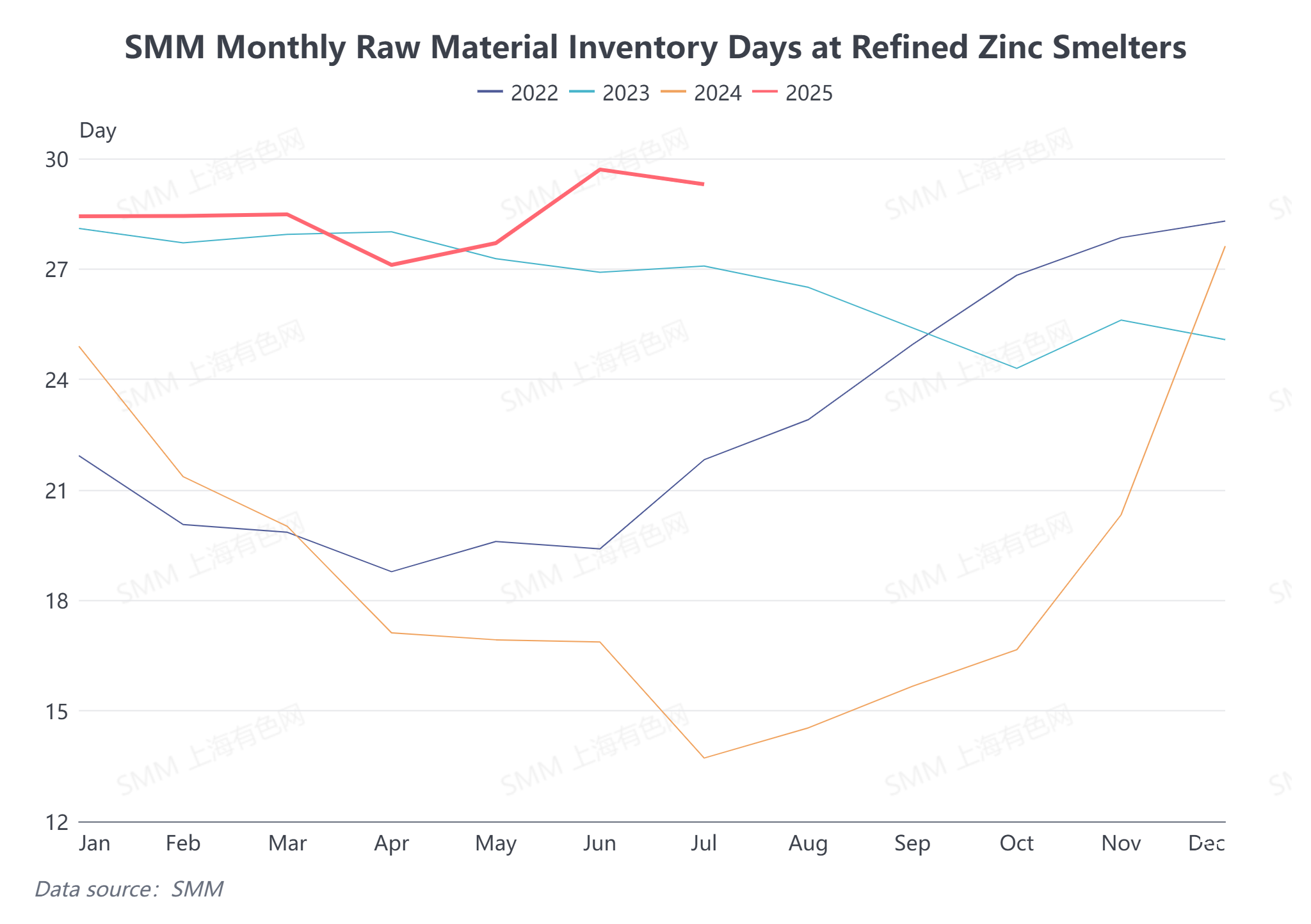

From the demand side perspective. According to SMM, after experiencing a shortage of domestic zinc concentrate last year, some domestic smelters signed long-term contracts for imported zinc concentrate at low prices at the beginning of the year to supplement their zinc concentrate supply for the year. Affected by this, with the continuous arrival of imported zinc concentrate at smelters in the first half of the year, the days of raw material inventories at domestic smelters basically ranged from 27 to 30 days from January to July this year, indicating ample raw material inventory. Smelters have shown strong reluctance to budge on prices, leading to a steady increase in processing fees for both domestic and imported zinc concentrate.

From the perspective of the SHFE/LME price ratio. Since June, the domestic zinc concentrate import window has remained closed, with import losses expanding to over 1,000 yuan/mt (metal content) in Q3. According to SMM calculations, as of August 8, the price of imported zinc concentrate was nearly 2,000 yuan/mt (metal content) higher than that of domestic zinc concentrate, giving domestic zinc concentrate a stronger price advantage. To facilitate transactions, importers have had to continuously raise their TC quotes.

Outlook for the future. Currently, LME zinc ingot inventory continues to decline to a low level for the year, with overseas market outperforming domestic market. Under the low price ratio, there is still some room for imported zinc concentrate TCs to rise. However, caution should be exercised regarding the timing of the start of winter stockpiling by domestic smelters this year. If the demand for imported zinc concentrate increases significantly as a result, processing fee levels may encounter resistance or even experience a correction.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)

![Ongoing Middle East Tensions Continued to Disrupt the Market, with LME Zinc Fluctuating at Lows [SMM Zinc Morning Meeting Summary]](https://imgqn.smm.cn/usercenter/CGlrd20251217171755.jpg)

![SHFE Zinc Maintained a Fluctuating Trend, with Attention on Subsequent Macro Changes [SMM Zinc Morning Comment]](https://imgqn.smm.cn/usercenter/qTzTI20251217171754.jpg)