An Overview of Downstream End-Use Demand: Resilience and Differentiation

NEVs: Growth Continues, but with a Slight Slowdown in the Engine

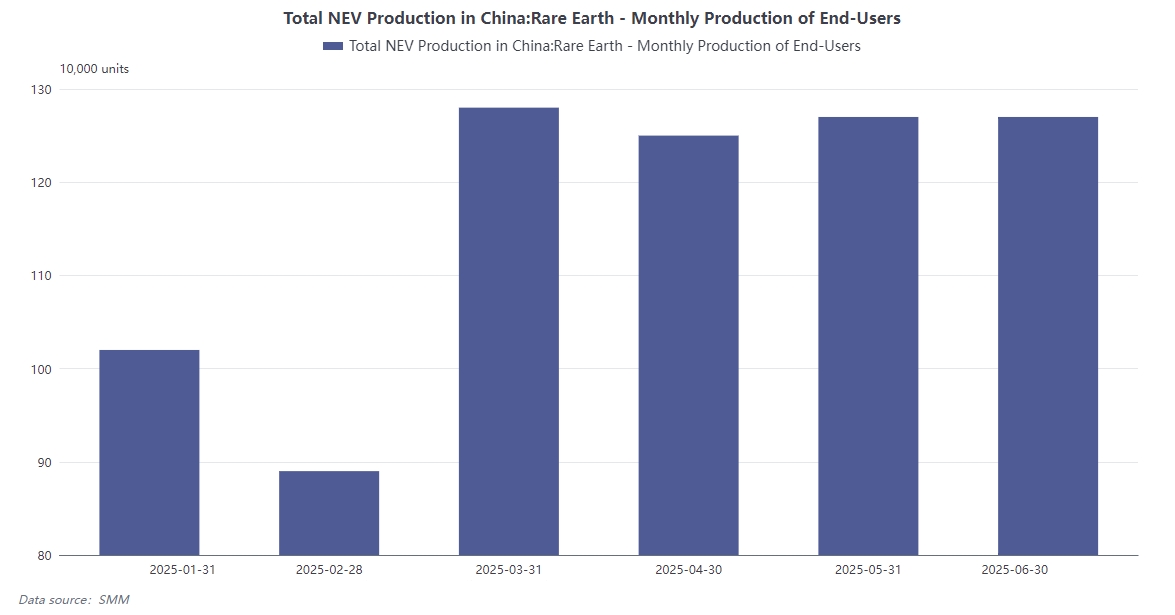

According to CAAM data, domestic NEV production reached 6.98 million units in H1 (with monthly average production exceeding 1.2 million units from March onwards, and reaching 1.268 million units in June), boosting NdFeB demand by approximately 25,000 mt. The NEV industry demonstrated a steady growth trend in H1, with sustained production increases driving demand for related materials such as NdFeB. The stable monthly average production from March onwards indicated that the industry was gradually maturing, with relatively stable market demand. The MoM stability in June's production also reflected continuous progress in market expansion and production capacity among enterprises.

H2 Outlook

Based on information from multiple sources, the industry focused on destocking in H1 with a stable production pace. SMM estimates that nationwide NEV sales in H2 this year will reach approximately 9 million+ units (including domestic sales and exports, passenger vehicles and commercial vehicles), with a YoY growth rate of around 25.6% for the full year. The YoY growth rate in H2 is expected to slow down compared to H1.

The main reasons for the expected slowdown in NEV sales YoY growth rate in H2 2025 are: 1) The high base formed in H2 2024 due to the enhanced national trade-in policy for NEVs; 2) The available amount of trade-in subsidies in H2 2025 will be less than that in H1, potentially failing to support sales until the end of the year; 3) The state advocates for the NEV industry to avoid "rat race" competition, weakening the effectiveness of volume discount strategies.

However, it is worth noting that despite the relatively slow auto sales in July, the traditional peak consumption seasons of September and October are expected to drive steady growth in NEV sales, following the previous trend. With the phasing-out of the NEV purchase tax policy in 2026 (from full exemption to a 50% reduction), a portion of NEV demand in early 2026 may be brought forward to the end of this year, supporting year-end sales.

Although OEMs do not directly purchase raw materials, they will strengthen communication with leading magnetic material enterprises in cases of severe price fluctuations or extreme scenarios, as their core concern lies in supply chain security and production stability. In the event of significant fluctuations in Pr-Nd raw material prices, leading NEV OEMs will actively communicate with their corresponding magnetic material enterprises to ensure a stable supply of raw materials and safeguard smooth production.

Wind Power and Industrial Robots: Steady Support, Cost Sensitivity Emerges

Wind Power Sector

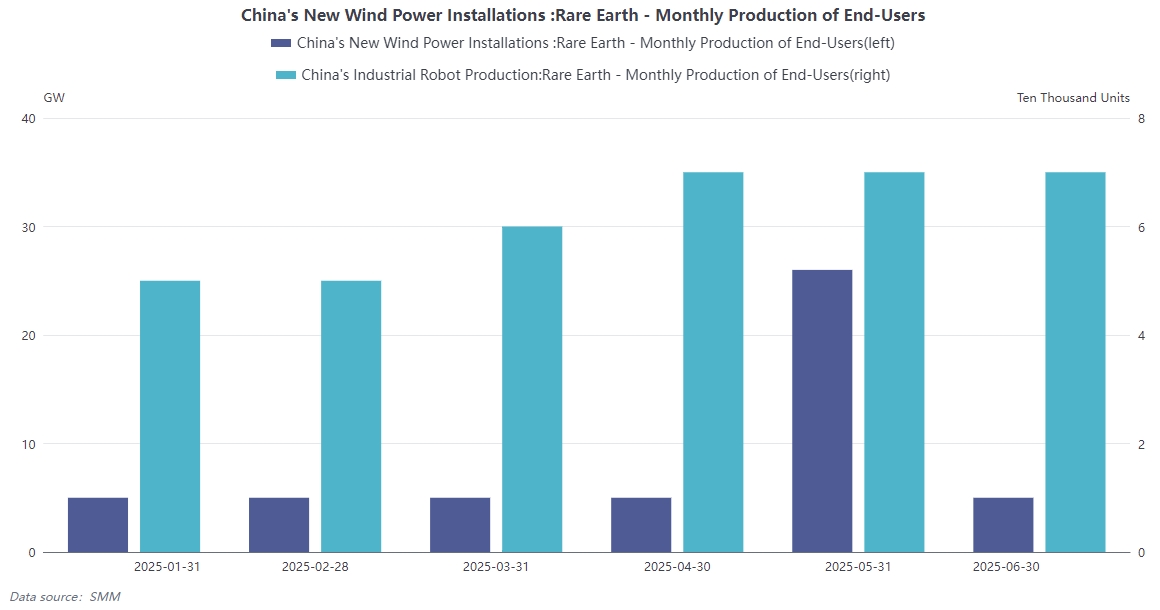

In H1, wind power installations reached approximately 51GW, with expectations of remaining flat or slightly declining in H2.

The shift in technological routes is noteworthy: in direct-drive wind turbines, the cost of generators (including rare earth permanent magnets) accounts for as high as 31.5%! In contrast, this proportion is only about 7% in doubly-fed induction generators (DFIGs). The high price of rare earths is accelerating the trend of DFIGs' resurgence.

The H1 wind power installation situation reflects the phased characteristics of industry development, and the expected flat or slightly declining trend in H2 is also related to market environment and policy adjustments.

In terms of technological routes, due to the high cost proportion of rare earth permanent magnets in the generators of direct-drive wind turbines, there is significant cost pressure amid rising rare earth prices. DFIGs, on the other hand, have cost advantages in this regard, leading more and more enterprises to focus on and adopt DFIGs, which has also contributed to the resurgence trend of DFIGs. This shift in technological routes not only affects the production decisions of wind power equipment manufacturers but also has a certain impact on the rare earth permanent magnet market.

Industrial Robots

In H1, domestic deliveries of industrial robots reached approximately 330,000 units, with relatively small monthly fluctuations, demonstrating stable demand. (Note: Although the acceleration of humanoid robot industrialisation is a future demand highlight (with magnetic material usage per unit potentially reaching 4kg), its contribution to Pr-Nd demand in the short term is limited.)

The industrial robot market maintained stable demand in H1, with steady monthly delivery fluctuations indicating a relatively mature industry and stable market demand. Although humanoid robot industrialisation has significant development potential in the future, with high magnetic material usage per unit, currently, due to the early stage of the industrialisation process, its contribution to Pr-Nd demand in the short term is still very limited. This also makes the industrial robot market relatively insensitive to Pr-Nd raw material prices at the current stage.

Consumer Electronics and White Goods: Marginal Improvement, but Minimal Absolute Impact

Magnetic Material Usage Model

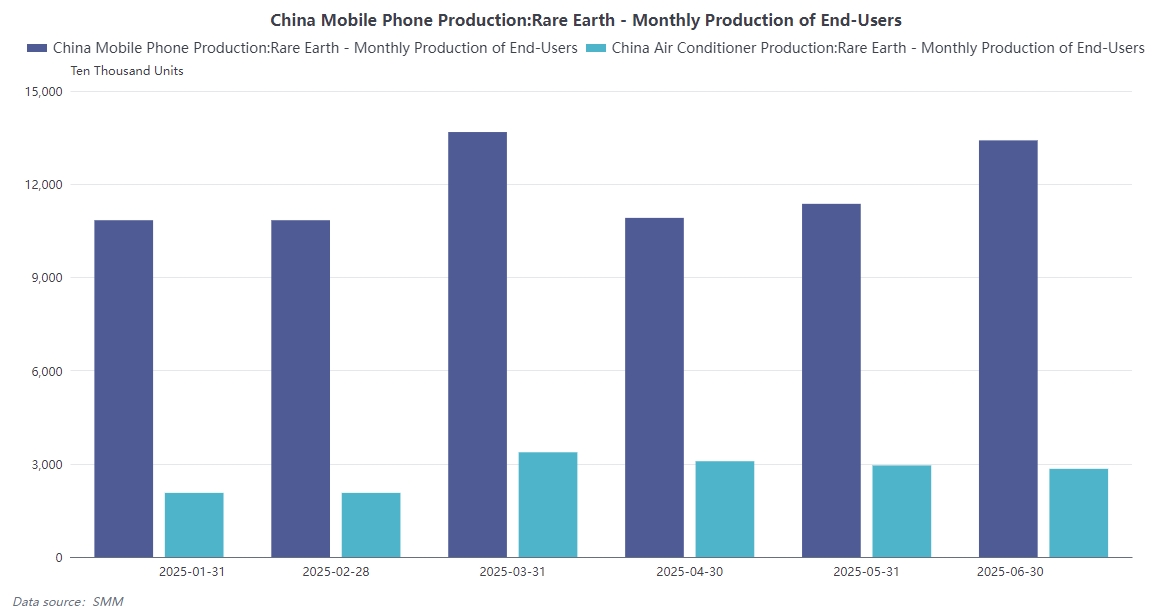

A single smartphone uses approximately 2g of magnetic material, while a single variable-frequency air conditioner uses about 90-110g. From the magnetic material usage model, it can be seen that the consumption of magnetic materials in consumer electronics and white goods products is relatively small.

Due to their compact size, smartphones use only about 2g of magnetic material per unit, making the impact of a single smartphone on the cost of Pr-Nd raw materials almost negligible. Although variable-frequency air conditioners use a relatively higher amount of magnetic material per unit, their overall demand for Pr-Nd raw materials accounts for a relatively small proportion of the total market.

Case Interpretation

In June, 134 million mobile phones were sold domestically, corresponding to a demand for only about 268 mt of magnetic materials — less than the monthly capacity of a medium-sized magnetic material factory. The same applies to white goods such as air conditioners. Taking the domestic mobile phone sales data in June as an example, although the sales volume of mobile phones is enormous, the corresponding total demand for magnetic materials is relatively limited due to the low usage of magnetic material per unit. Similarly, although the sales volume of white goods such as air conditioners in the market is considerable, the overall impact on the magnetic material market is relatively small due to the limitation of magnetic material usage per unit. This also results in a relatively weak feedback from the consumer electronics and white goods sectors to the market when there are fluctuations in the price of Pr-Nd raw materials.

Demand Dynamics

Summer promotions, back-to-school seasons, and various consumer stimulus policies (such as consumption vouchers and home appliance subsidies) have a certain boosting effect on short-term consumption. However, overall, the impact of this sector on the rare earth price system is almost negligible. Summer promotions, back-to-school seasons, and various consumer stimulus policies can promote the sales of consumer electronics and white goods products to a certain extent, having a certain boosting effect on the short-term consumer market. However, from a long-term and overall perspective, the impact of these factors on the rare earth price system is minimal. Although the market size of the consumer electronics and white goods sectors is enormous, due to their relatively stable and small proportion of demand for magnetic materials, it is difficult to have a substantial impact on rare earth prices.

Energy-Saving Elevators: Data "Highlights" Can't Hide the Overall Downward Trend

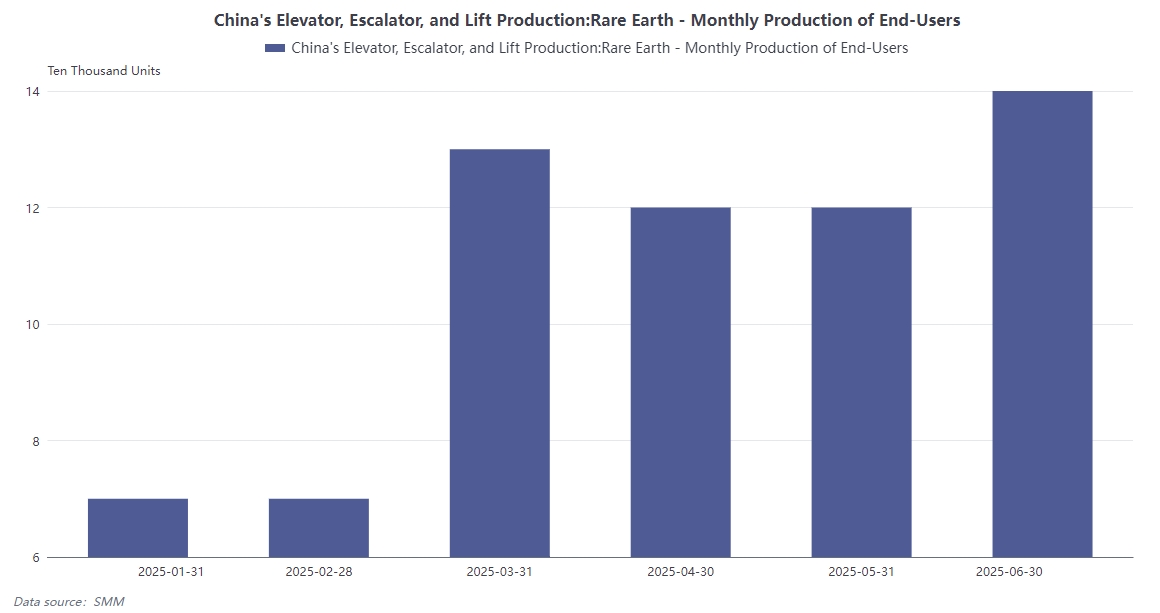

NBS Data: Elevator production in June reached 137,000 units, up 16.7% MoM. From the perspective of elevator production data in June, the significant MoM growth seems to indicate a positive development trend in the industry. However, behind this data lies a different truth.

Realistic Interpretation

Against the backdrop of continuous pressure in the commercial real estate and residential markets, this MoM growth is partly attributed to the delivery of previously backlogged orders and inventory adjustments. The industry generally understands the limitations of this category of data. Therefore, we believe that the recovery signal in this area may be short-lived, and the long-term downward trend remains unchanged, with extremely limited boosting effect on the demand for magnetic materials.

The sluggishness of the commercial real estate and residential markets directly affects the development of the elevator industry. The MoM growth in June production is more due to the delivery of previously backlogged orders and inventory adjustments by enterprises, rather than a genuine recovery in market demand. Industry insiders have a clear understanding of the limitations of this data.

In the long run, the elevator industry faces the dilemma of insufficient market demand, and its boosting effect on the demand for magnetic materials will also continue to weaken. This also makes it difficult for the energy-saving elevator sector to become a significant support point for the demand for magnetic materials in the current rare earth market environment.

Key Insights:

Intensified competition within the industry chain is putting transmission efficiency to the test.

It should be clarified that the aforementioned end-use applications (such as automakers, wind turbine manufacturers, robot manufacturers, and consumer electronics brands) are not direct buyers of magnetic materials. Therefore, when the cost of Pr-Nd raw materials is passed down the industry chain to them, their inherent resistance to price increases is logical.

As the "buyers" at the end of the value chain, they typically have a large scale and strong bargaining power. Their core demands are to pursue business growth while vigorously resisting upward cost pressures. Against the backdrop of the current overall lackluster industrial sector and poor operating rates in some industries, end-users' willingness to compress costs is even more resolute. Enterprises in end-use application sectors such as automakers and wind turbine manufacturers, due to their positions in the industry chain and their own scale advantages, often leverage their bargaining power to resist price increases when faced with rising magnetic material costs. In the current poor overall environment of the industrial sector, enterprises are facing increased operating pressures, and cost compression has become crucial for their survival and development. Therefore, end-users are stricter in cost control and have stronger resistance to price increases in magnetic materials.

Consequently, a delicate "tug-of-war" has emerged in the current market: upstream raw material suppliers attempt to pass on price increases, while end-use demand refuses to fully absorb them. Magnetic material and motor manufacturers in the midstream are the first to bear the brunt of this double-sided squeeze, facing significant challenges in short-term profitability. Upstream raw material suppliers hope to obtain higher profits by raising prices and passing on cost pressures downstream.

However, end-use demand, due to its own cost control needs, is unwilling to fully accept price increases. This has left magnetic material and motor manufacturers in the midstream of the industry chain in a dilemma, having to bear the cost pressures from upstream raw material price increases on one hand and struggling to fully pass on costs to downstream customers on the other, resulting in severe impacts on short-term profitability.

Analyst's Musings

The key to this competition will depend on the efficiency and resilience of price transmission. If the high price of Pr-Nd can remain stable for a sufficiently long period, accompanied by steady growth in end-use demand (especially in major growth areas such as new energy vehicles), end-users may gradually accept the reality of cost transfers. Conversely, if end-use demand remains weak or price transmission is blocked for too long, upstream high prices may struggle to be sustained independently.

In the coming weeks and months, closely tracking the production schedules and actual procurement rhythms of core end-use sectors (especially new energy vehicles) will be crucial in determining the outcome of this "competition". Time will ultimately provide the true answer. If the price of Pr-Nd raw materials can remain stable at a high level while major end-use demand sectors such as new energy vehicles continue to grow, end-users may gradually adapt to rising costs and accept the results of price transmission. However, if end-use demand remains sluggish or obstacles are encountered in the price transmission process, preventing upstream high prices from being recognized downstream, then upstream high prices will be difficult to sustain.

Therefore, tracking the production schedules and procurement rhythms of core end-use sectors is particularly important, as these data will provide key evidence for us to judge market trends. In this competition within the industry chain, time will ultimately decide the outcome.