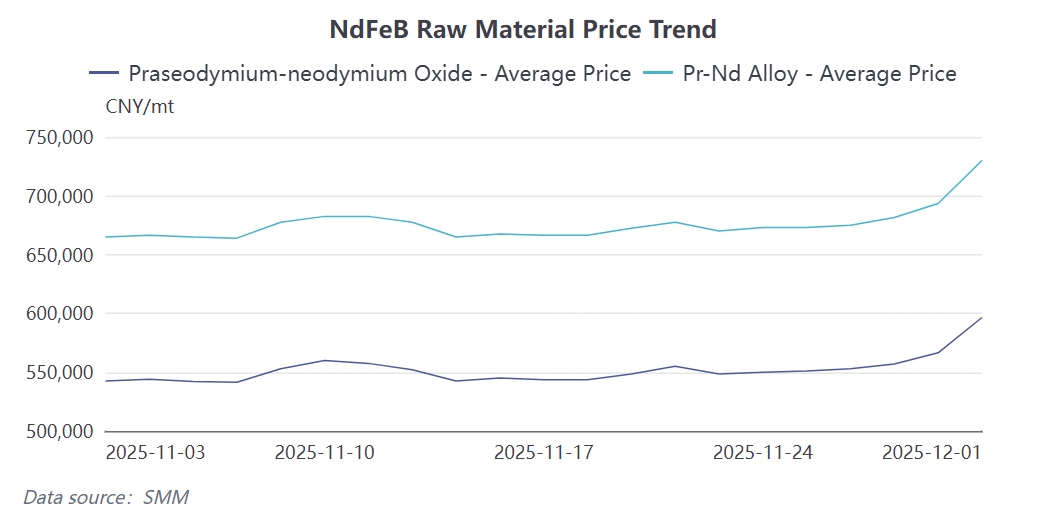

Recent sharp price increases in Pr-Nd have significantly impacted the NdFeB permanent magnet industry chain. On the first day of December, spot Pr-Nd oxide quotes surged by 30,000 yuan/mt to 596,500 yuan/mt in a single day, while Pr-Nd alloy prices rose by 36,500 yuan/mt to 730,000 yuan/mt. This price surge is primarily driven by tightening supply expectations: rare earth supply is becoming constrained, while demand from sectors such as wind power and NEVs remains robust, leading to a pronounced supply-demand imbalance.

Faced with cost pressures, magnetic material enterprises are showing a divergent trend: some small and medium-sized magnetic material factories have suspended quotations or are cautiously taking orders, while top-tier enterprises maintain stable shipments by leveraging their earlier inventory advantages. End-users, on the other hand, generally adopt a wait-and-see approach, with inquiries increasing but actual transactions remaining scarce, as they await price stabilization before making purchases.

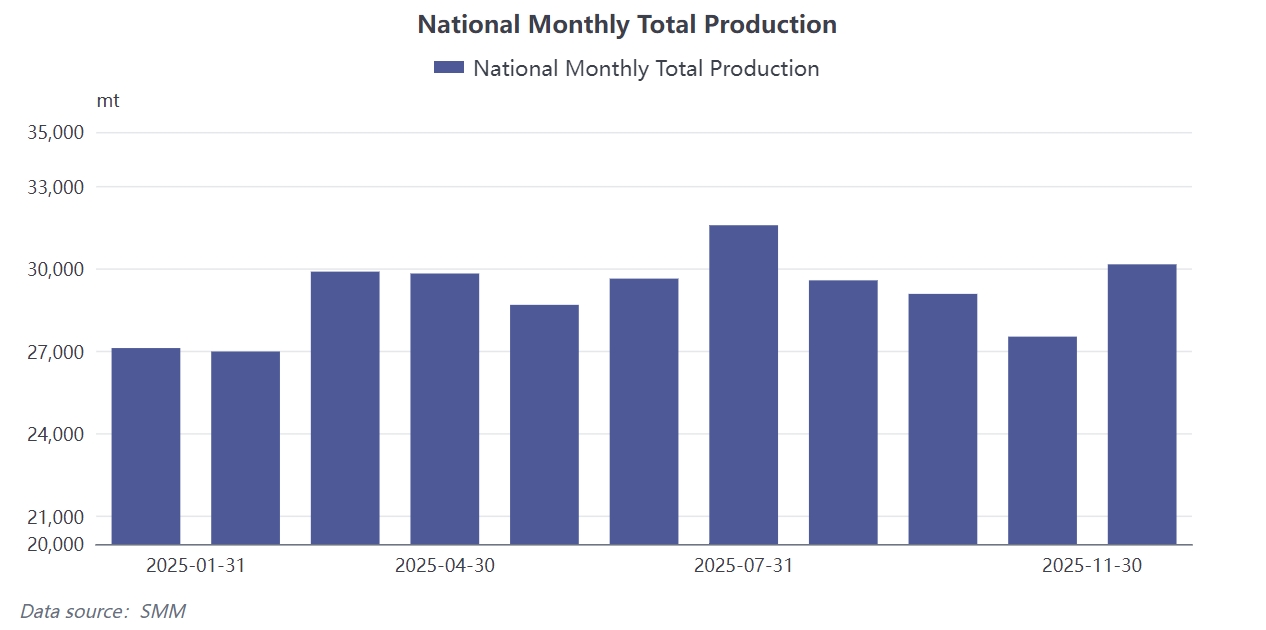

NdFeB production in November increased by 9.55% MoM to 30,182 mt, with the operating rate rising to 70.18%. This round of growth primarily benefited from the combined effect of short-term policies and market sentiment. The easing of China-U.S. rare earth issues at the end of October boosted overseas inquiry activity, driving up the prices of raw materials such as Pr-Nd oxide, which in turn stimulated defensive purchasing by domestic motor enterprises. On November 8, new export control policies further spurred overseas stockpiling demand, while domestic NEV manufacturers ramped up procurement to meet annual targets, collectively pushing up production for the month. However, this growth partly relied on downstream "defensive purchasing" behavior, the sustainability of which is significantly affected by price fluctuations.

NdFeB production in December is expected to pull back to 29,540 mt, with the operating rate dropping to 69.1%, down approximately 2% MoM. This adjustment is primarily driven by three restraining factors:

First, the rapid short-term increase in Pr-Nd prices has led end-users to generally suspend the signing of long-term contracts, shifting toward consuming existing inventories, resulting in a noticeable contraction in new order volumes for magnetic material plants;

Second, some enterprises have completed their pre-year stockpiling plans ahead of schedule, leading to a natural contraction in production schedules toward year-end; third, in a high-price environment, magnetic material plants are selectively screening orders to protect profits, abandoning some low-margin product lines.

Notably, industry concentration continues to increase during this process, with the production share of top-tier enterprises reaching 73.5%, while the shares of mid- and lower-tier enterprises are further compressed, indicating that scaled enterprises exhibit stronger risk resistance amid cost fluctuations.

Despite short-term production being under pressure, the long-term demand fundamentals of the industry remain unchanged. Emerging sectors such as new energy vehicles, industrial robots, and the low-altitude economy continue to provide growth momentum. Current price fluctuations are accelerating industry consolidation, with top-tier enterprises leveraging their resource and technological advantages to continuously expand production (e.g., JL MAG Rare-Earth plans to increase its capacity to 40,000 mt by 2025). Industry concentration (CR4) is expected to rise from 29% in 2024 to 42% by 2026.

The market should monitor the outcome of the interplay between raw material supply control policies and end-user restocking pace after December, as well as the long-term risks associated with rare earth technology substitution.