Comprehensive Overview:

China's steel exports currently face dual challenges: On one hand, anti-dumping policies in traditional markets such as the EU, the U.S., Japan, and South Korea are tightening; on the other hand, Southeast Asian countries are accelerating local production capacity. In 2024, China's crude steel output experienced its first negative growth, with its global share dropping to 55%. Meanwhile, the export structure is undergoing positive changes: exports of high-value-added products continue to rise, and overseas capacity deployments—such as Dexin Steel in Indonesia—have achieved notable results.

Facing these challenges, Chinese steel companies are seeking breakthroughs across multiple dimensions: optimizing export structures (with machinery and steel products accounting for 72%), expanding into emerging markets (notable growth in Southeast Asia, the Middle East, and Latin America), and accelerating technological innovation to drive high-end product development. These shifts reflect the industry's determination to transition from scale advantages to quality and efficiency.

Looking ahead, for sustainable development, China's steel industry must adhere to innovation-driven growth, green development, and open cooperation. It must not only accelerate R&D in high-end products to enhance international competitiveness but also deepen global collaboration for mutual benefit.

China's exports in the first half of 2025: A way out of the pressure of overcapacity?

Source: GACC, WorldSteel, NBS, SMM

Source: GACC, WorldSteel, NBS, SMM

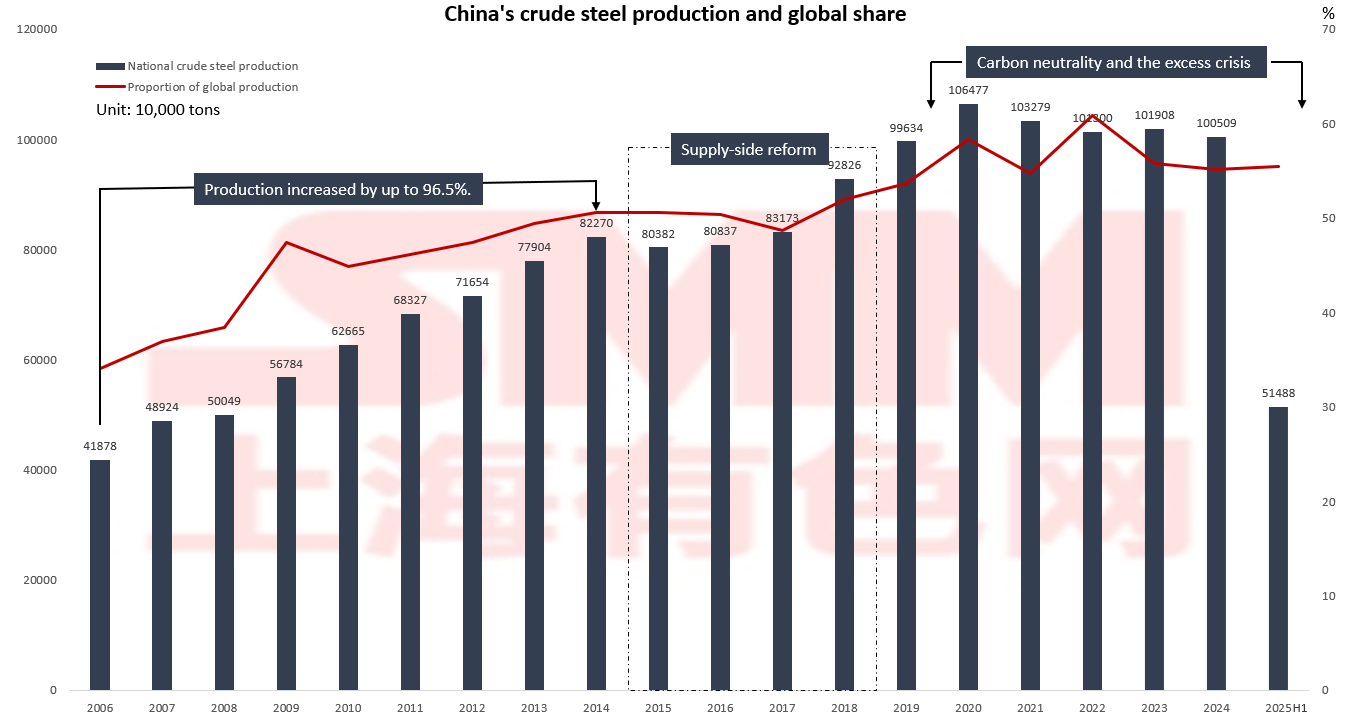

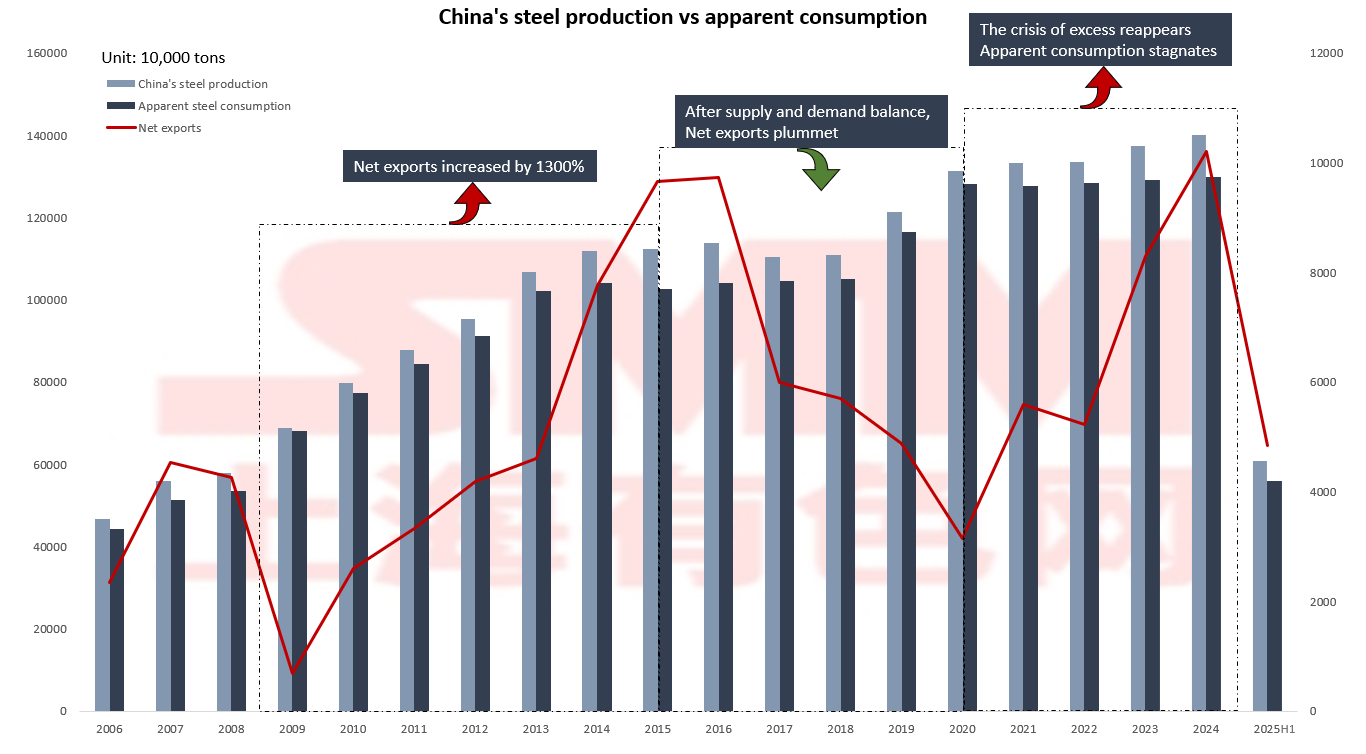

From 2006 to 2015, driven by infrastructure investment and a real estate boom, crude steel production surged from 419 million tons to 804 million tons, with China's share of global production jumping from 34% to 50% and net exports increasing by nearly 1,300%. However, this extensive growth also led to severe environmental pollution issues. Starting in 2015, China launched supply-side structural reforms, promoting a shift from “quantity-driven” to “quality-driven” development through the elimination of outdated capacity and strict environmental production restrictions. Net exports fell from 96.64 million tons in 2015 to 31.41 million tons in 2020. Although the scale contracted, industry concentration and environmental standards significantly improved. Currently, China's steel industry faces new challenges. In 2024, net exports once again exceeded 100 million tons, but apparent consumption has stalled. Meanwhile, Southeast Asian countries are accelerating the localization of their production capacity, using anti-dumping policies to support domestic steel mills, thereby eroding China's traditional price advantage in steel. In 2024, China's crude steel production saw its first negative growth, with its global share dropping from 61% in 2022 to 55%. Industry transformation and upgrading are now urgent priorities.

Meanwhile, Southeast Asian countries are accelerating the localization of steel production capacity, using anti-dumping policies to create development space for domestic emerging steel mills. This trend directly undermines China's low-price advantage. Southeast Asian countries are not only meeting their own needs but also beginning to抢占 regional market share.

Focus on Indirect Exports: A New Path for China's Steel Capacity Adjustment!

Source: GACC, SMM

Source: GACC, SMM

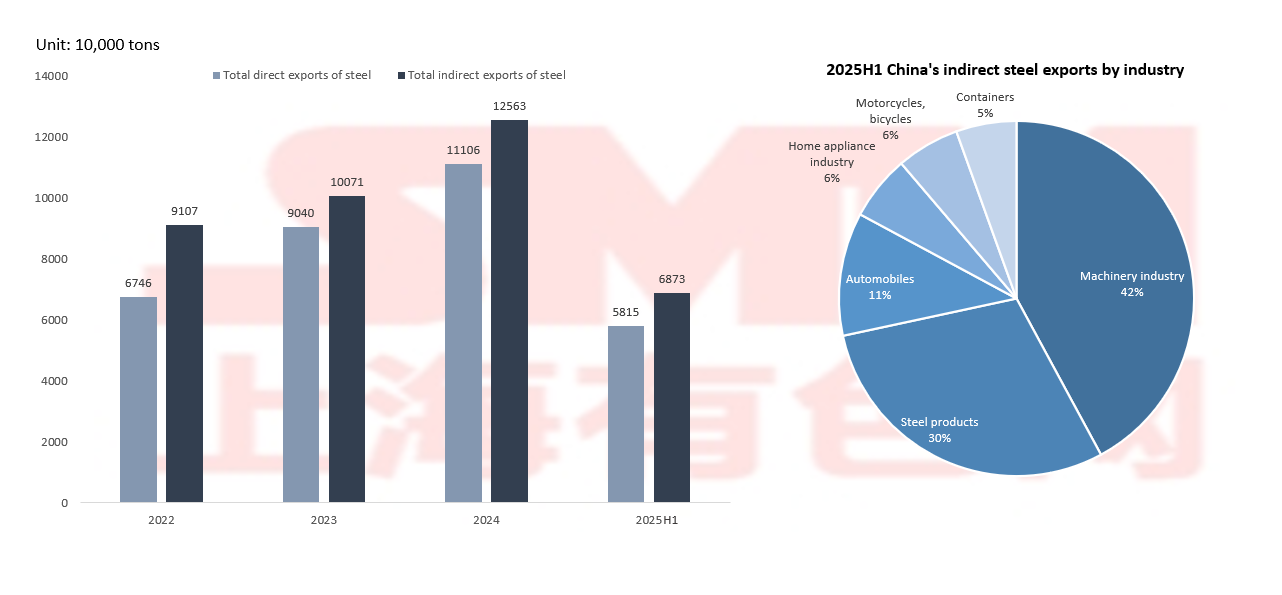

Under pressure from the EU's carbon tariffs and Southeast Asia's anti-dumping policies, the scale of China's indirect steel exports has surpassed direct exports, with the machinery industry and steel products accounting for as much as 72%, highlighting China's supply chain advantages in manufacturing; exports of high-value-added products such as automobiles and home appliances grew by 20% year-on-year, though the total volume remains small, the transformation has already shown initial results.

Currently, rush exports and transshipment trade have become emergency measures, but such tactical approaches are unsustainable. Notably, the EU is planning to expand its anti-dumping scope to include steel structural components, which will pose new challenges for China's steel exports. This trend underscores the urgency of accelerating industrial upgrading and enhancing product value-added.

Export Panorama: Geographic Layout, Market Strategy, and Price Competition Source: GACC, NBS, SMM

Source: GACC, NBS, SMM

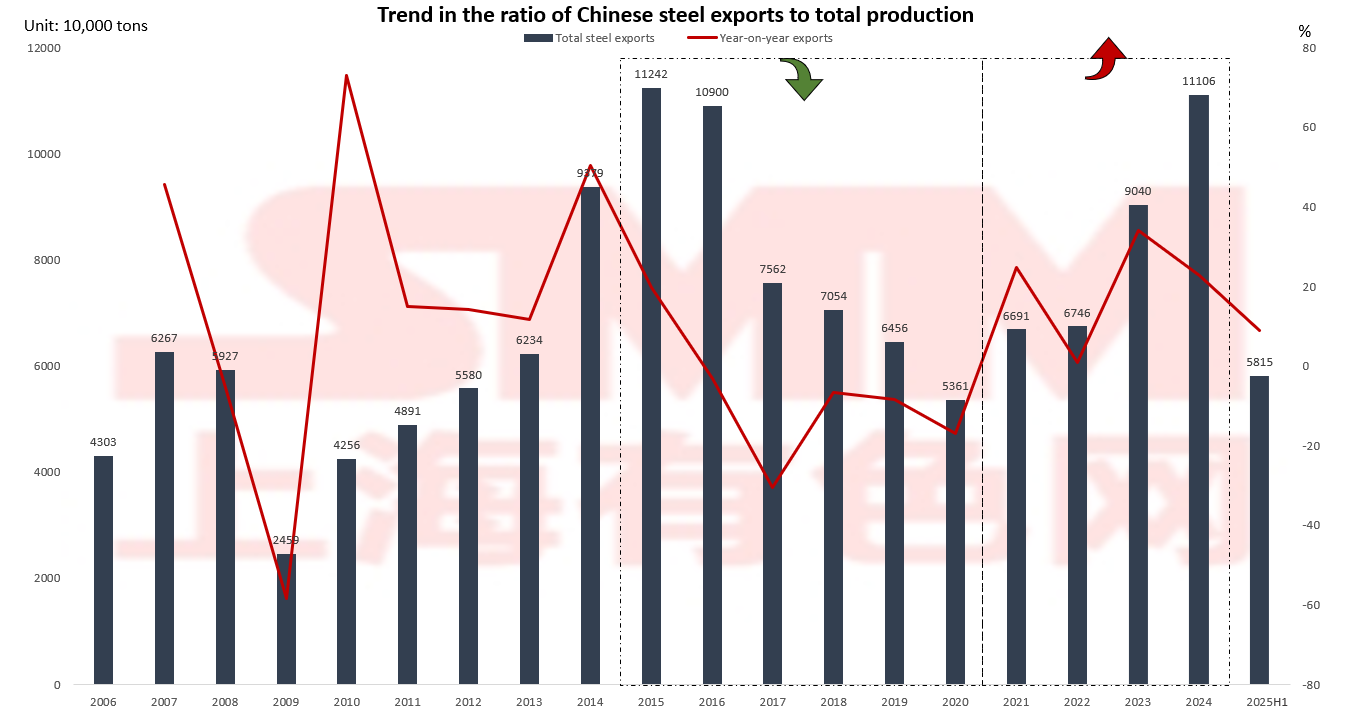

Earlier export growth reached 161%, driven by domestic capacity expansion and robust global market demand, enabling Chinese steel companies to swiftly capture international markets through their scale advantages. However, as supply-side structural reforms deepened, steel exports adjusted back to 53.61 million tons, reflecting a reasonable contraction in export scale following the balancing of domestic demand. In 2024, China's steel exports once again surpassed the 100 million ton mark, but the growth model has undergone a qualitative leap. On one hand, the proportion of high-value-added products in the export structure continues to rise; on the other hand, steel companies are accelerating overseas capacity expansion to actively address new international trade challenges such as the EU carbon tariff.

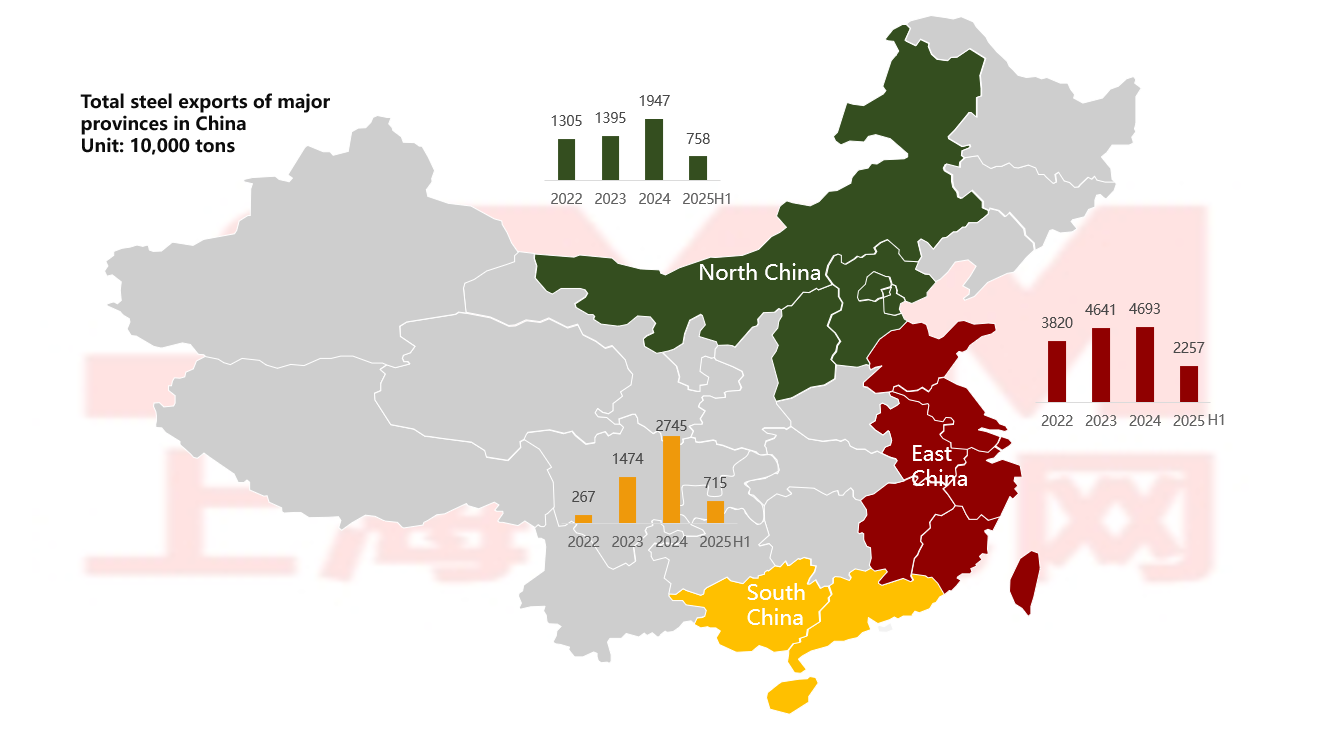

Coastal provinces dominate China's steel exports: Is excessive concentration a good or bad thing? Source: SMM

Source: SMM

China's steel industry is highly concentrated in coastal regions, with North China, East China, and South China accounting for 72% of the country's crude steel production capacity. Leveraging port advantages and a complete industrial chain, these regions have developed significant export competitiveness. Taking North China as an example, the efficient synergy between steel clusters and ports such as Tianjin Port and Caofeidian Port has significantly enhanced export efficiency. However, this concentrated layout also poses risks, as environmental production restrictions in the Beijing-Tianjin-Hebei region directly impact the national export market.

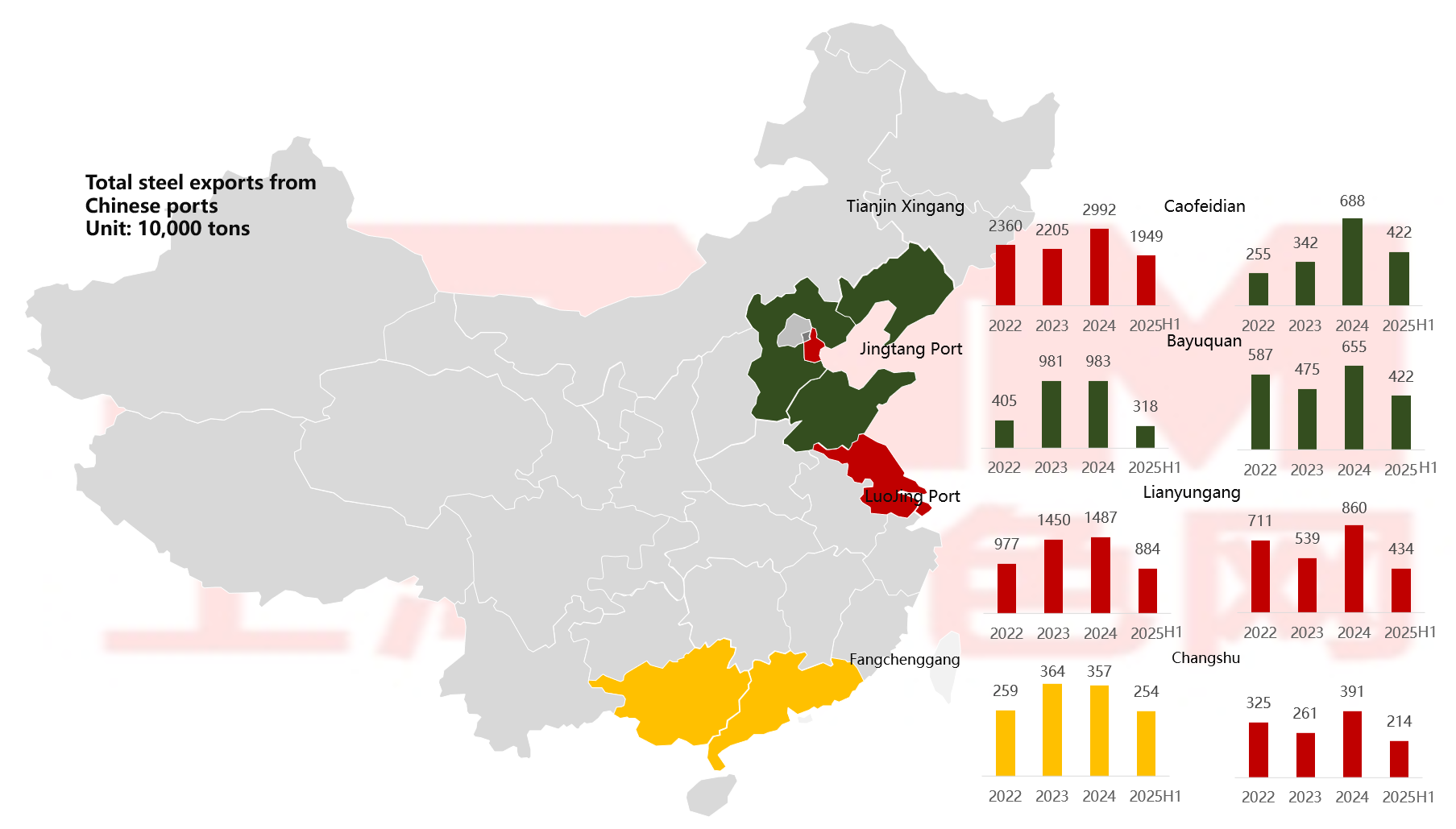

China's steel exports defy the trend, with northern ports remaining the main export hub Source: SMM

Source: SMM

From a port perspective, Tianjin New Port has consistently maintained its core hub status. Notably, “buy-and-export” transactions have emerged in some new ports. This workaround, which involves purchasing others' customs declarations, has addressed the short-term export needs of some small and medium-sized enterprises. However, it poses multiple risks, including inability to claim tax refunds and financial risks.

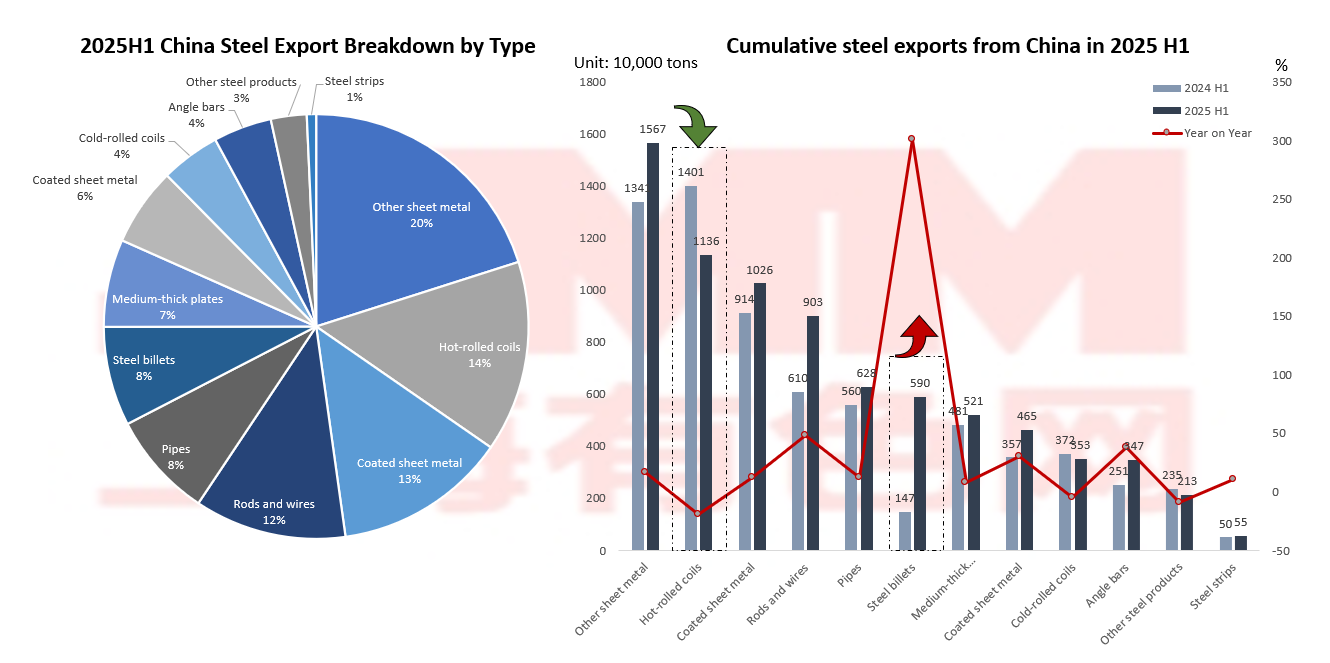

Surge in billet exports: How far can barrier avoidance go? Source: GACC, SMM

Source: GACC, SMM

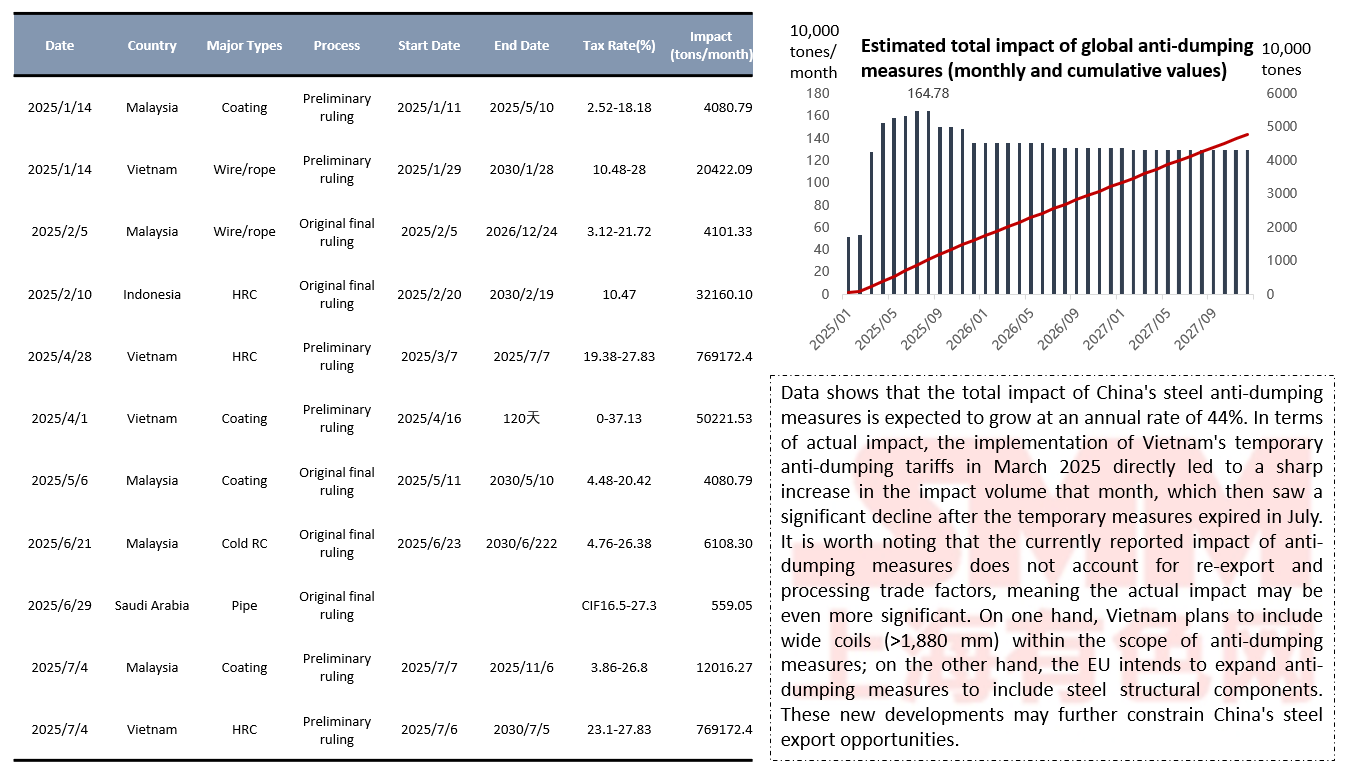

Billet exports have experienced explosive growth, with a year-on-year increase of 300% in the first half of 2025. The reasons behind this include China's billet having significant price competitiveness and being exempt from anti-dumping policies. This shift reflects China's steel enterprises actively adjusting to changes in the international trade environment. Meanwhile, traditional mainstay export products like hot-rolled and cold-rolled steel are facing severe challenges. The implementation of the EU carbon tax and the intensification of anti-dumping policies by Southeast Asian countries have directly led to sustained pressure on exports of these two product categories, with cumulative export volumes showing a significant year-on-year decline. Data shows that Vietnam imposed an anti-dumping duty rate of up to 27.83% on Chinese hot-rolled products in 2025, severely eroding their price advantage.

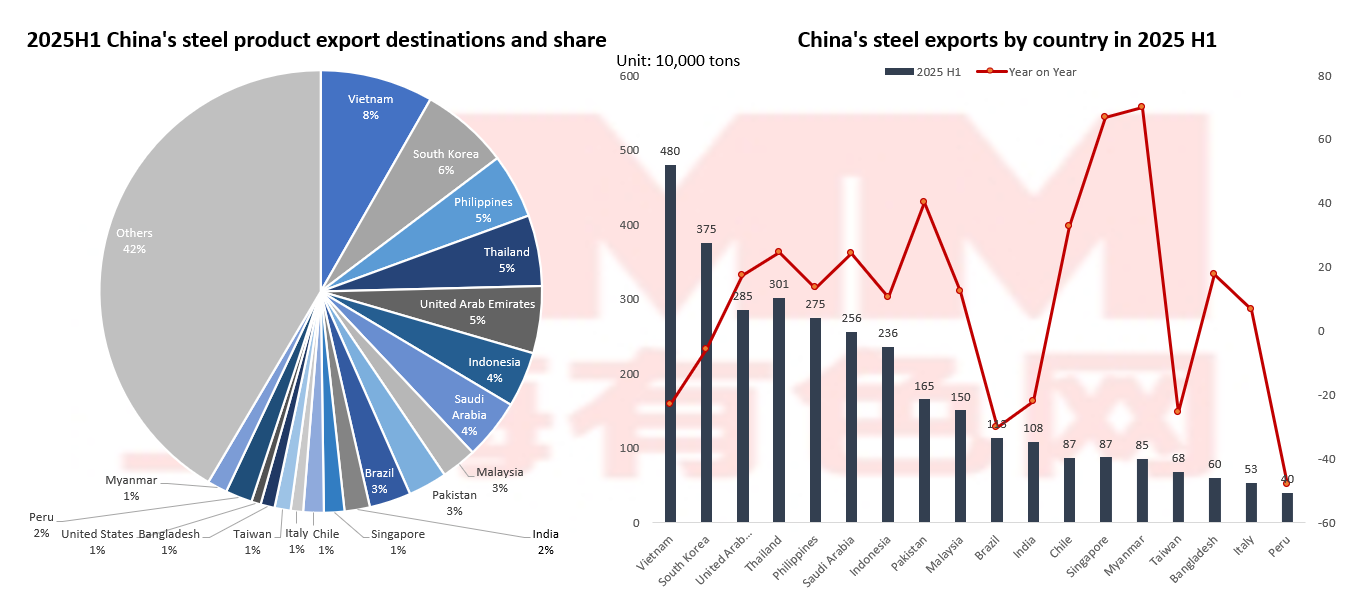

Anti-dumping measures drive export shifts: China's steel industry's “breakthrough strategy in emerging markets” Source: GACC, SMM

Source: GACC, SMM

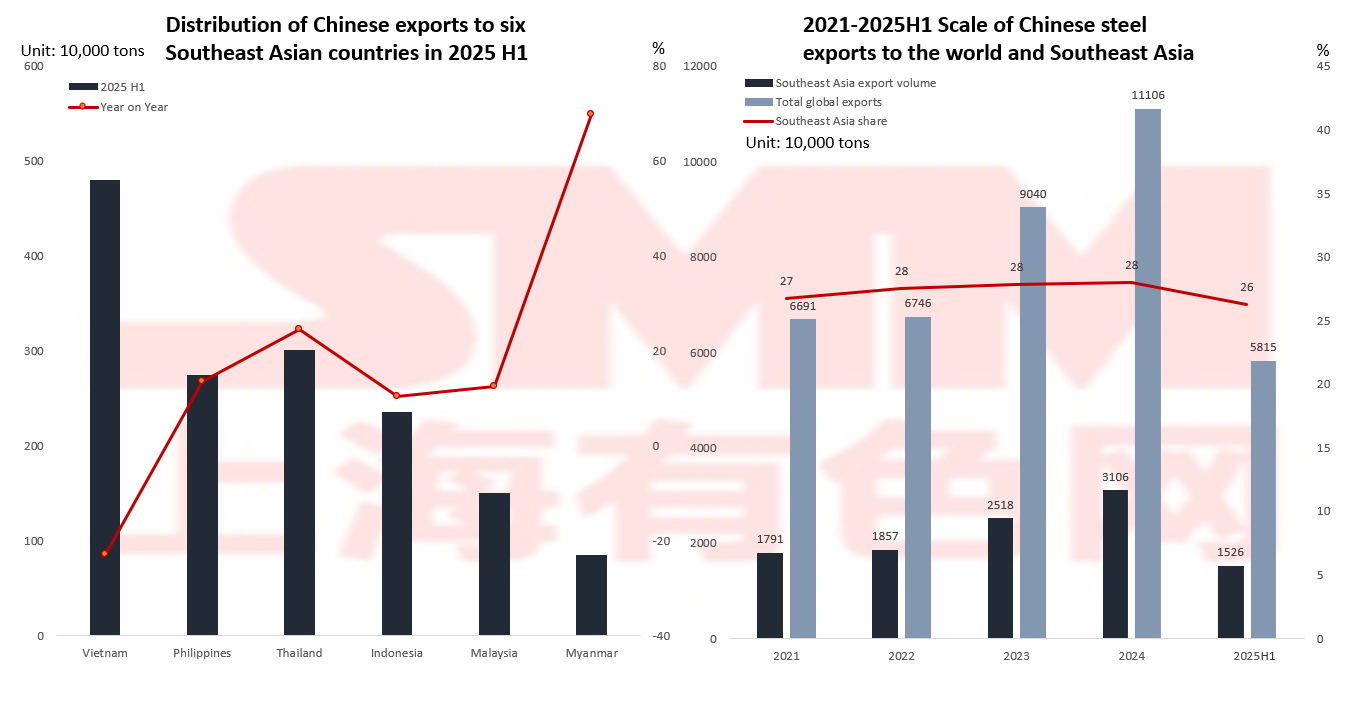

Facing anti-dumping barriers in traditional markets such as Europe, the United States, Japan, and South Korea, China's steel companies are undergoing a profound market transformation. Data shows that the Southeast Asian market has become the primary destination, accounting for 26% of China's total steel exports. Among these, Indonesia, Malaysia, and Myanmar have achieved rapid growth due to their re-export trade advantages and infrastructure demand. Exports to Myanmar grew by 70% year-on-year in the first half of 2025. Emerging markets such as the Middle East and Latin America also performed strongly: Saudi Arabia saw a 24% increase due to infrastructure demand growth, while Thailand became an alternative market due to Vietnam's anti-dumping measures, growing by 24.6%. While this market shift has alleviated the pressure from the contraction of traditional markets, it has also brought new challenges.

It is worth noting that emerging markets generally have lower profit margins, and countries like the Philippines have launched anti-circumvention investigations, with new trade barriers emerging. More concerning is that over-reliance on exports of raw materials like steel billets may trap China's steel industry in a “low-end lock-in” dilemma.

China's export quotes still hold a strong advantage Export prices anchored above the pressure level of hot-rolled coil prices Source: SMM

Source: SMM

China's export quotes have always held a strong advantage, with significant price differentials compared to other countries, except for those in the Commonwealth of Independent States (CIS). However, the recent sustained rise in China's export quotes is eroding this competitive advantage, directly leading to a significant decline in export orders. This phenomenon is particularly pronounced in key export products such as hot-rolled coil.

China's competition for Southeast Asian market share and anti-dumping battles

Source: GACC, SMM, WorldSteel

Source: GACC, SMM, WorldSteel

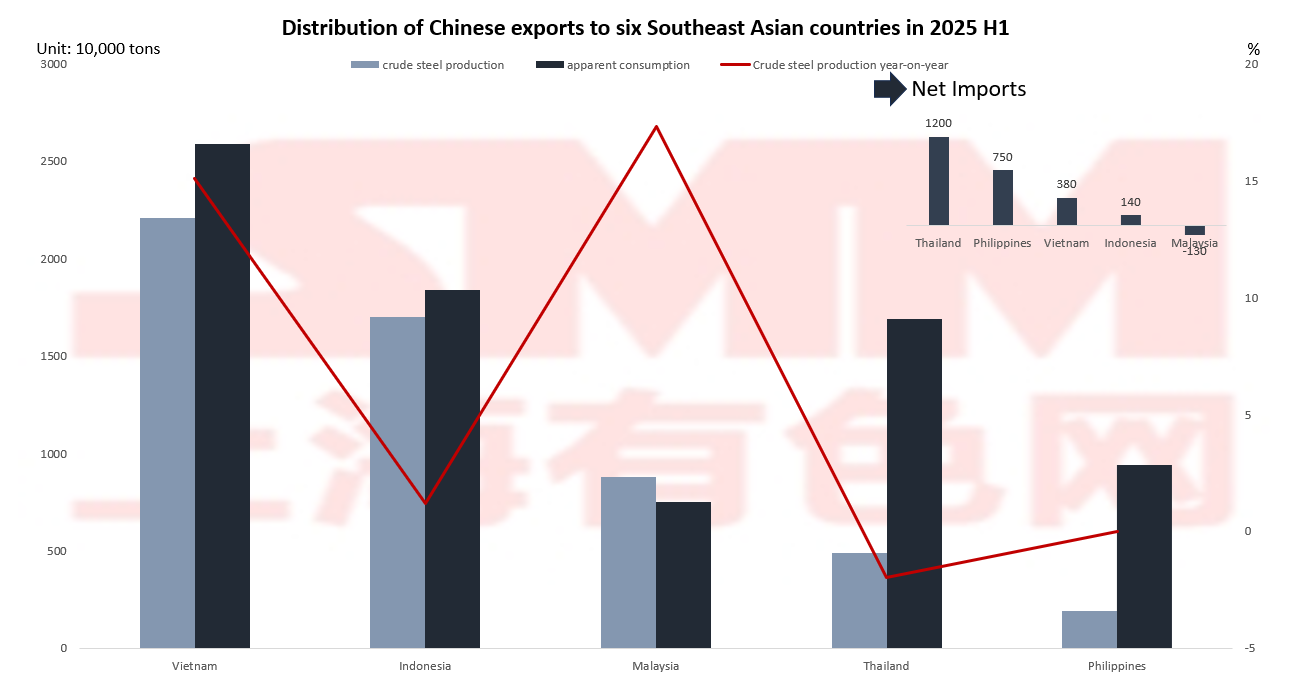

The Southeast Asian market is undergoing profound changes, presenting a new “rise and fall” trend. Although the region maintains a stable 28% market share overall, its internal structure has undergone significant changes: Vietnam's market has shrunk due to a high anti-dumping tax of 27.83%, while Malaysia, Thailand, and Myanmar have grown against the trend, collectively accounting for 35% of the market, becoming new growth engines. Behind this market segmentation lies the restructuring of the industrial chain: Malaysia leverages its re-export trade advantages to circumvent barriers through steel billet processing; Thailand, however, faces insufficient domestic production capacity (with a utilization rate of just 29% in 2024), leading to stable import demand.

Notably, development across Southeast Asian countries remains highly uneven: Malaysia's production growth reached 17.3%, gradually transitioning toward becoming an export-oriented nation; Vietnam's growth slowed to 15.1%; while Thailand remains heavily reliant on imports. This diverse landscape presents both opportunities and risks, requiring companies to dynamically adjust their strategies—seizing Malaysia's re-export opportunities while guarding against potential anti-dumping measures from countries like the Philippines.

11 Investigations! How Is China's Steel Industry Responding to the “Toughest-Ever” Anti-Dumping Wave? Source: China Trade Remedies Information, SMM

Source: China Trade Remedies Information, SMM

Are Chinese overseas steel plants carving out new markets beyond the “anti-dumping wall”?

Chinese steel companies are breaking through trade barriers by establishing overseas plants, with Indonesia's Dexin Steel being a successful example. In July 2025, the plant set a record daily production of 20,008 tons, demonstrating three key advantages: first, it avoids anti-dumping measures from Europe and the US by operating under the “Made in Indonesia” label; second, lower production costs compared to domestic operations; and third, promoting the export of Chinese technical standards. This model points the way forward for Chinese steel companies: overseas expansion can both avoid trade wars and facilitate industrial upgrading. As the Belt and Road Initiative progresses, more Chinese steel companies are expected to go global and achieve international development.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)