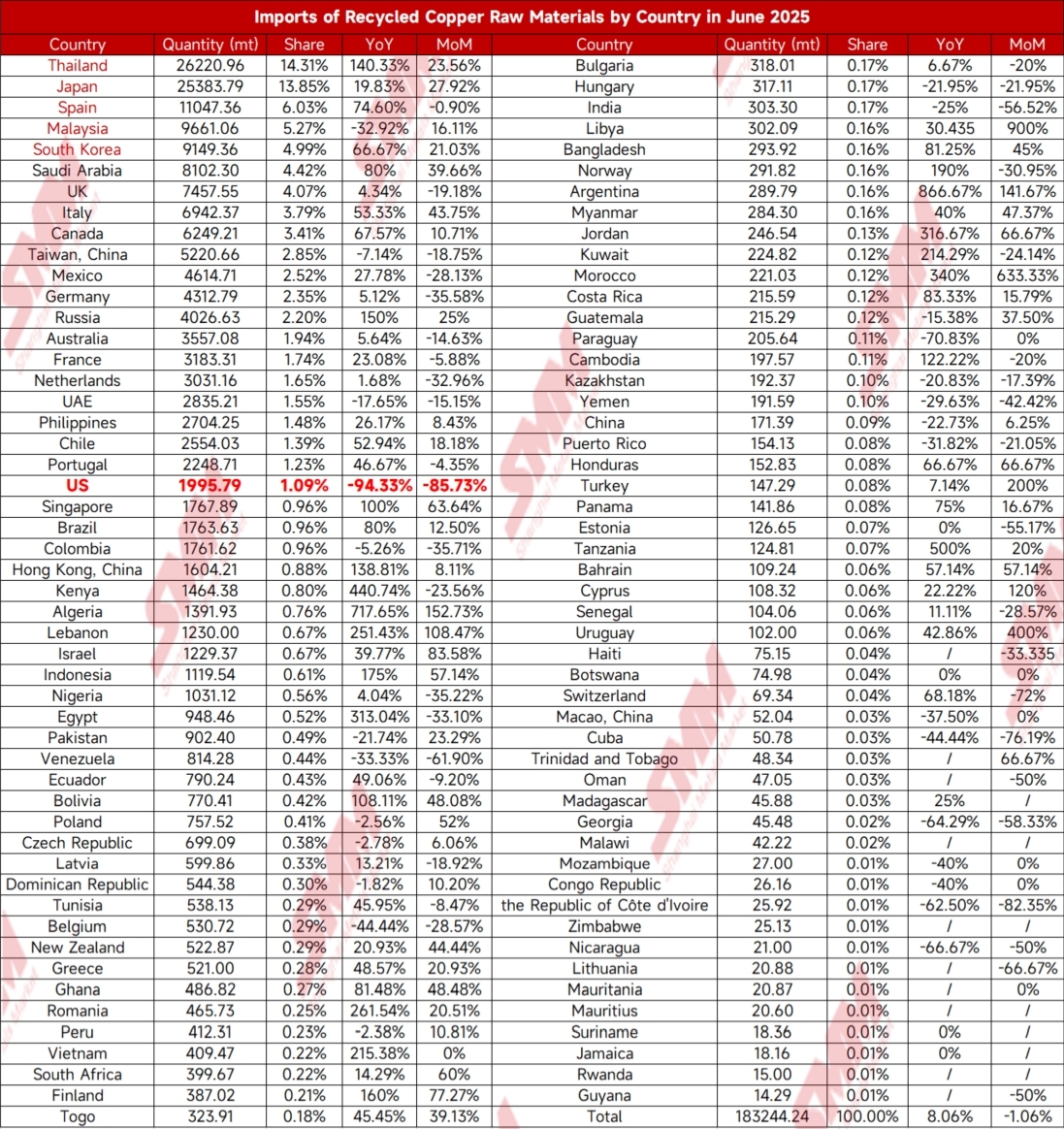

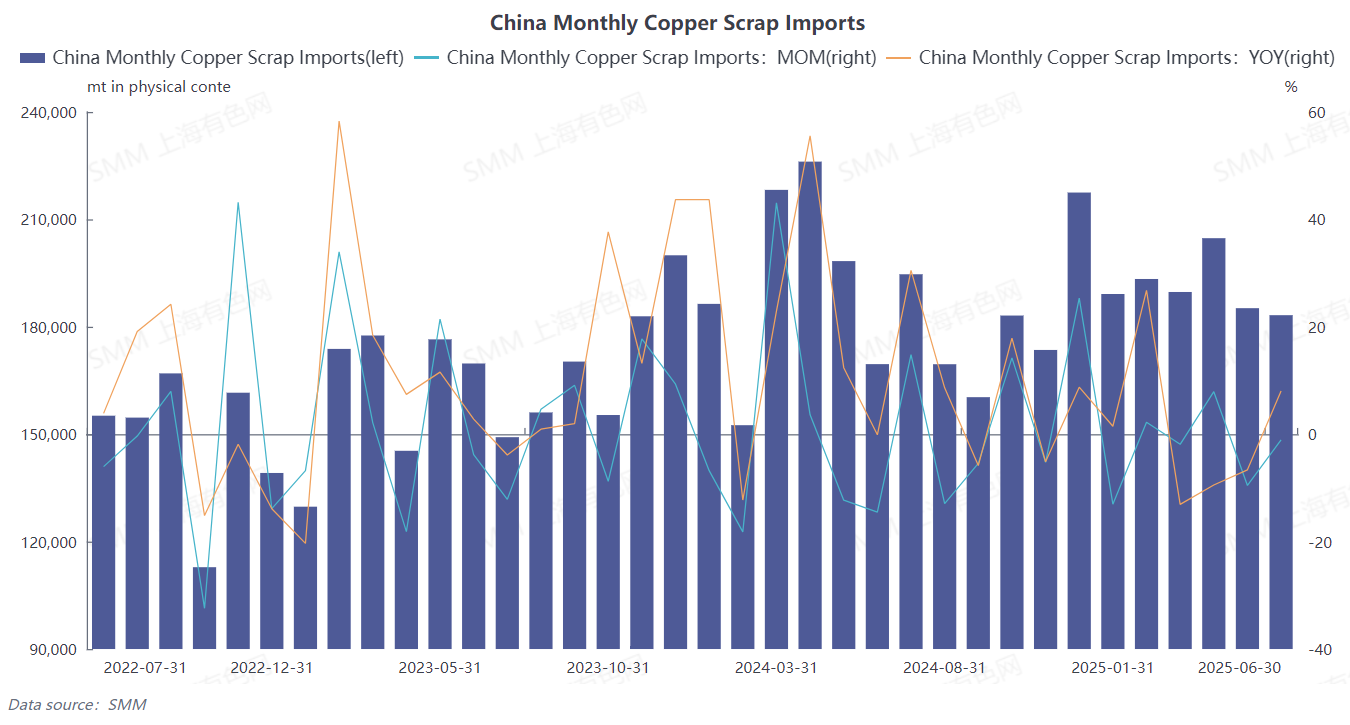

According to the latest data from the General Administration of Customs, China's imports of copper scrap and shredded copper scrap reached 183,200 mt in June 2025, down 1.06% MoM and up 8.06% YoY. From the cumulative data of January-June, imports stood at 1.1454 million mt, down 0.5% YoY. (HS code 74040000).

In June, there was no significant unexpected decline in the imports of recycled copper raw materials. SMM believes there are three main reasons:

1. Strong smelting demand support: Due to the tight supply of copper concentrates (TC has remained around -$43/mt since the end of April this year), domestic copper smelters have increased their reliance on recycled copper raw materials, which have become a key supplementary raw material.

2. Structural adjustment of import sources: Despite a sharp decline in imports of recycled copper raw materials from the US, imports from major suppliers such as Thailand and Japan increased MoM, offsetting part of the shortfall. US recycled copper raw materials have been redirected to Thailand, India, Japan, Taiwan, and other places, resulting in a global supply mismatch rather than a reduction in total volume.

3. Periodic opening of the import window: The early-stage advantage of the SHFE/LME price ratio became apparent, and the import profit window opened, stimulating the arrival of some recycled copper raw materials and supporting overall orders for June imports.

Specifically, in June 2025, there was an adjustment in the structure of import sources. Thailand continued to hold the position as China's largest supplier of copper scrap and shredded copper scrap, with imports reaching 26,200 mt, accounting for 14.31% of the total, up 23.56% MoM and 140.33% YoY. The US, once a major supplier, slipped to third place in May and further fell to 21st place in June, with monthly imports of only 2,000 mt, accounting for just 1.09% of the total, down 85.73% MoM and 94.33% YoY. In June, Japan's exports of copper scrap and shredded copper scrap to China reached 25,400 mt, up 27.92% MoM and 19.83% YoY, ranking second in China's total imports. Spain's exports to China in June were 11,000 mt, down 0.9% MoM and up 74.6% YoY, ranking third.

According to SMM, the current tight supply of recycled copper raw materials persists. Affected by the US tariff policy, traders lack willingness to purchase from the US, and there is almost no US supply in the market. Meanwhile, the prices of supplies from other countries remain high, leading to severe losses for traders.

Ningbo traders indicated that supply is currently tight. Despite SHFE copper rising by nearly 1,000 yuan today, Zhejiang bare bright copper is still quoted at -800 yuan/mt below the online price, and traders choose to refuse to budge on prices when shipping goods. Additionally, secondary brass traders reported that copper prices have fluctuated significantly recently. However, due to weak downstream demand, brass billet prices have only fluctuated by 300-500 yuan/mt, making it difficult for domestic secondary brass spot prices to follow the futures market significantly higher. Meanwhile, overseas brass prices are extremely high, with import supply prices being 1,000-1,500 yuan/mt higher than the domestic transaction price. Overall, supply in the Zhejiang region is relatively tight.

Looking ahead, SMM believes that China's recycled copper raw material imports may exhibit a "decline first, then rise" trend in the coming months (July-October 2025).

Short-term main pressure factors:

1. Seasonal off-season effect: High temperatures in July-August inhibit domestic copper scrap dismantling and recycling activities, coupled with seasonal reductions in overseas supply (e.g., summer holidays in Europe and the US), leading to a potential slight MoM decline in imports.

2. The import profit window closed at the end of June, which will dampen enterprises' import enthusiasm.

3. Uncertainty surrounding the US tariff policy: If the US's 232 investigation policy on imported copper scrap is actually implemented on August 1, it will lead to a further contraction in domestic copper scrap imports from the US (currently accounting for nearly 1%, down from around 20% previously).

Potential supporting factors:

1. To meet annual production targets, domestic smelters may purchase copper scrap in advance (especially when copper concentrate TCs remain low) in Q4, driving a MoM rebound in imports.

2. After the US copper scrap export shifts to Southeast Asia (e.g., Thailand, Malaysia), the volume reprocessed and re-exported to China may gradually increase, forming a new supply chain balance.

Overall, despite a slight pullback in China's imports of recycled copper raw materials in June 2025, resilience remained. SMM believes this was mainly due to the support from smelting demand and the diversified adjustment of import sources. In the short term, affected by seasonal factors, the closure of import windows, and US tariff policies, imports are expected to face pressure in Q3. However, in Q4, with the rebound in stockpiling demand from domestic smelters and the supplement of transshipment supply from Southeast Asia, imports are expected to stabilize and rebound. In the future, close attention should be paid to overseas policy changes and the substitution relationship between copper concentrates and recycled copper raw materials. Under the global supply chain restructuring, price fluctuations and regional supply-demand mismatches will become the norm.

(Attached below are the import data by source for June 2025)