SMM July 8 News:

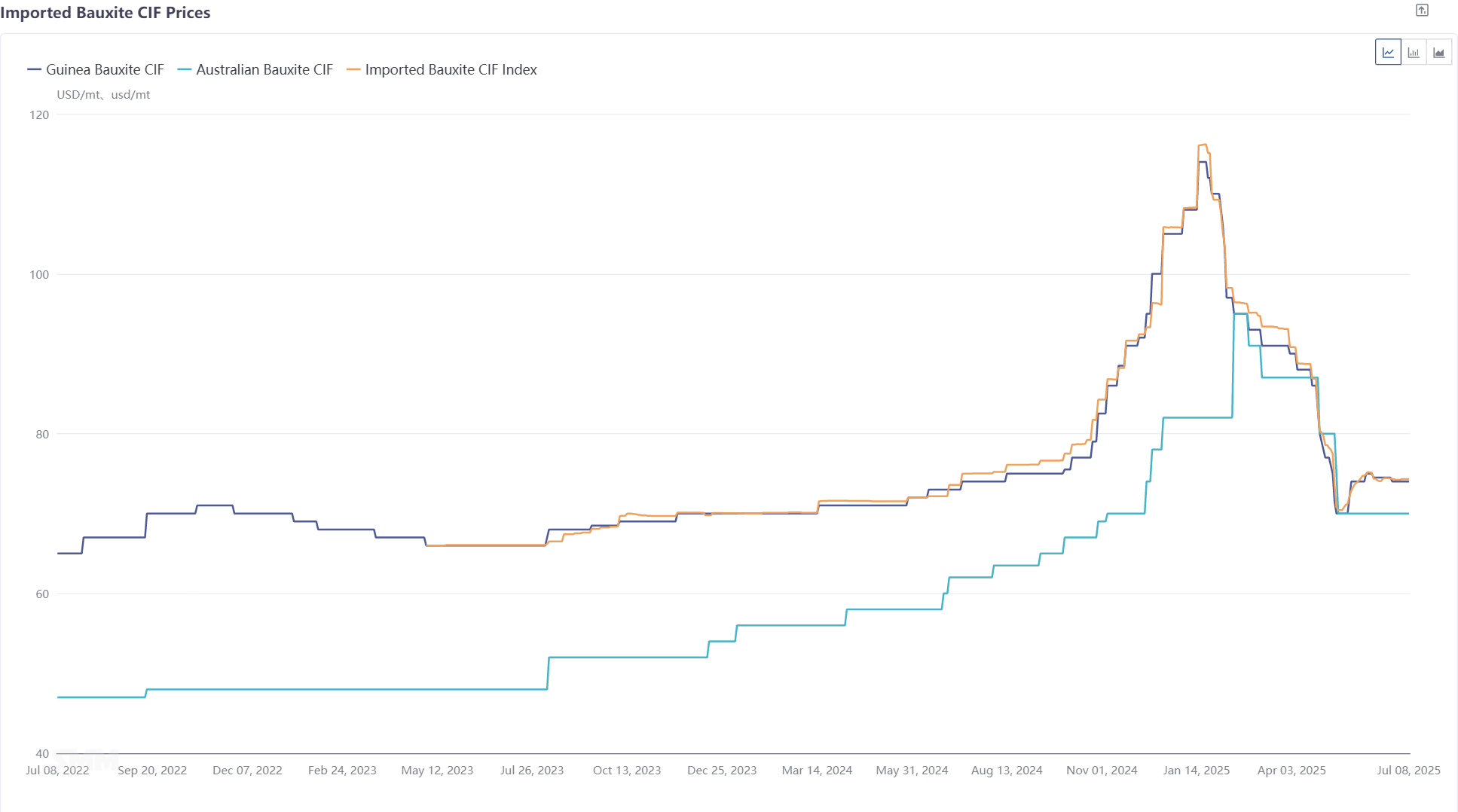

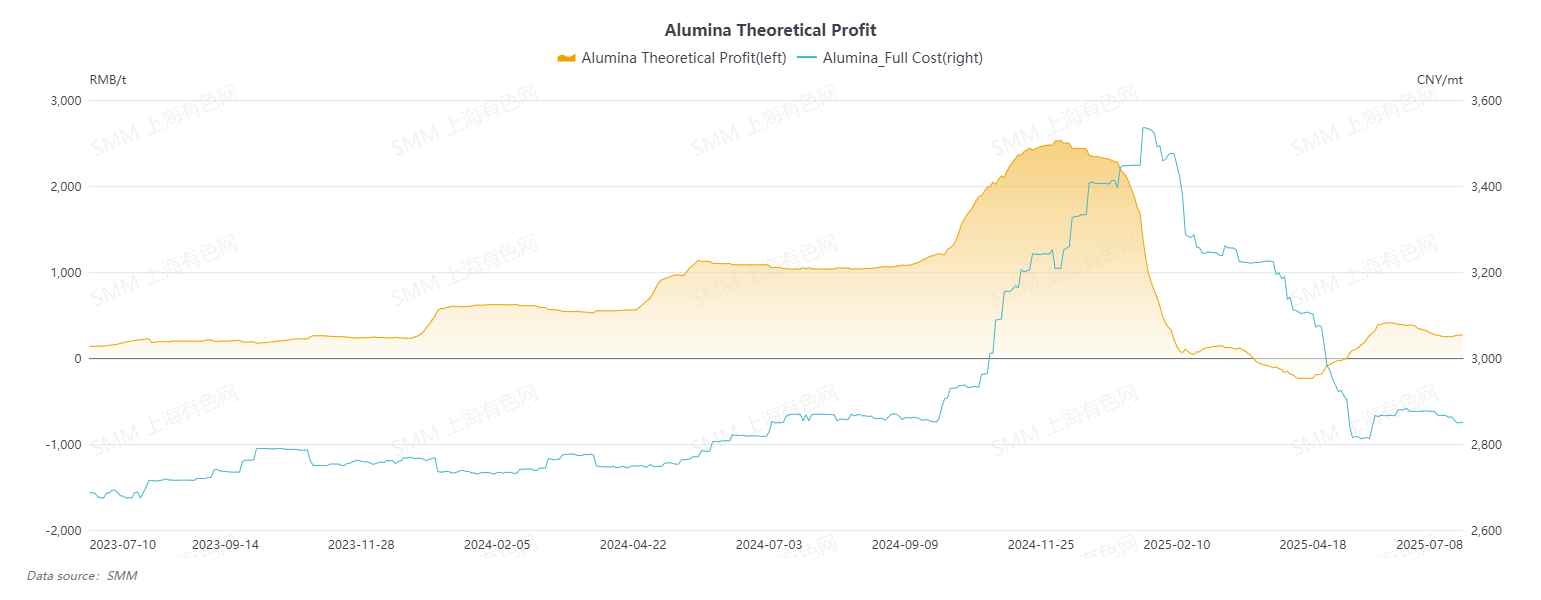

From the end of 2024 to the beginning of 2025, alumina production was highly profitable, with operating capacity of alumina remaining high. However, alumina refineries had low inventory levels of bauxite raw materials and actively purchased bauxite. Affected by this, bauxite prices surged significantly. With limited domestic bauxite supply, imported bulk bauxite became the main source of raw material supplementation, with frequent transactions and continuously rising prices. In mid-January, the SMM CIF index for imported bauxite peaked at $116.19/mt.

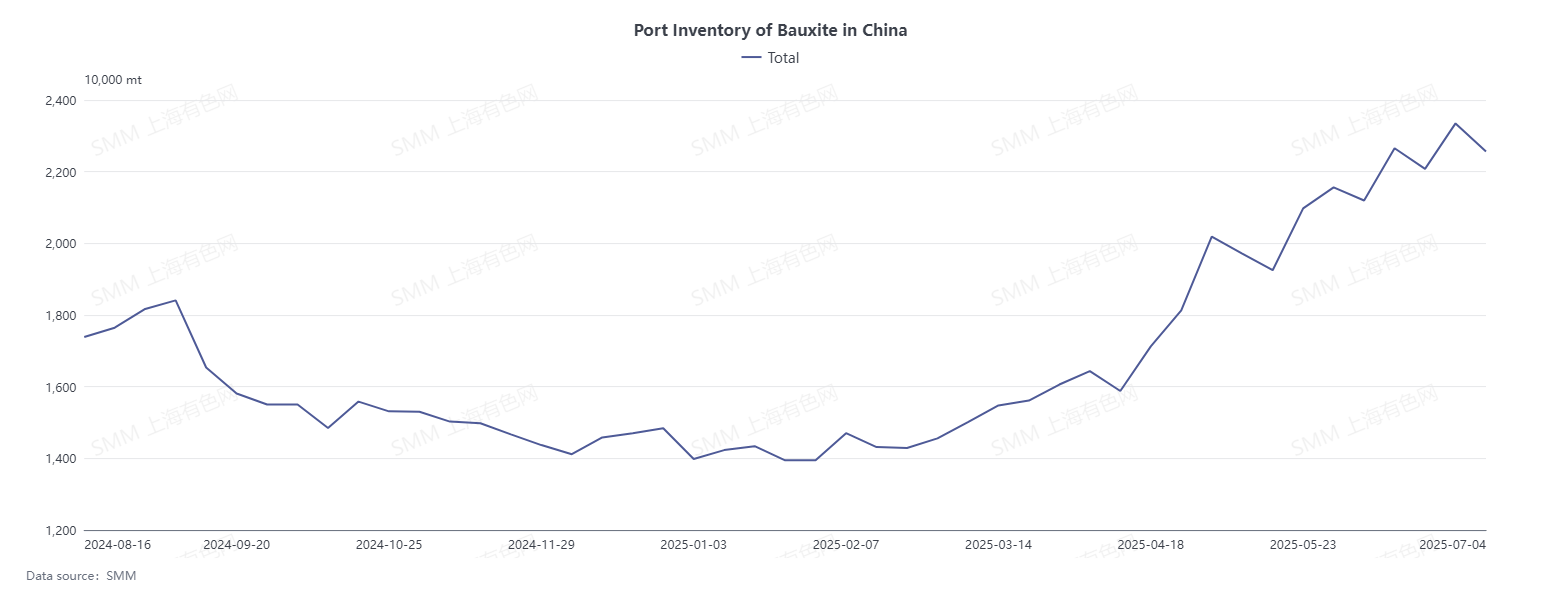

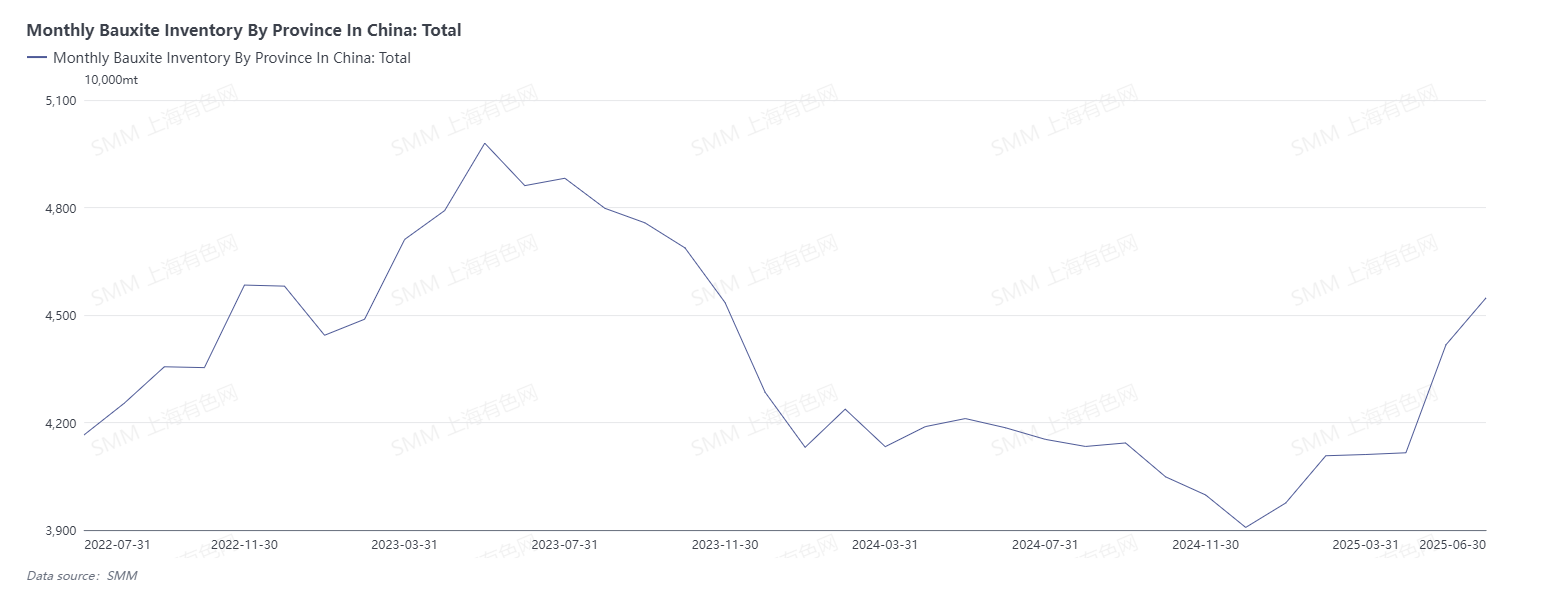

Driven by high prices, Guinea's bauxite shipments surged, and the supply of imported bauxite reached record highs, leading to a clear surplus in bauxite. By the end of June, SMM data showed that port bauxite inventory had increased by approximately 9.5 million mt compared to the beginning of the year, and alumina refineries' bauxite raw material inventory had increased by approximately 6.5 million mt compared to the beginning of the year.

With a continuous surplus in bauxite and alumina refineries shifting from profitability to losses, leading to bargain down purchasing prices of raw materials, bauxite prices pulled back.

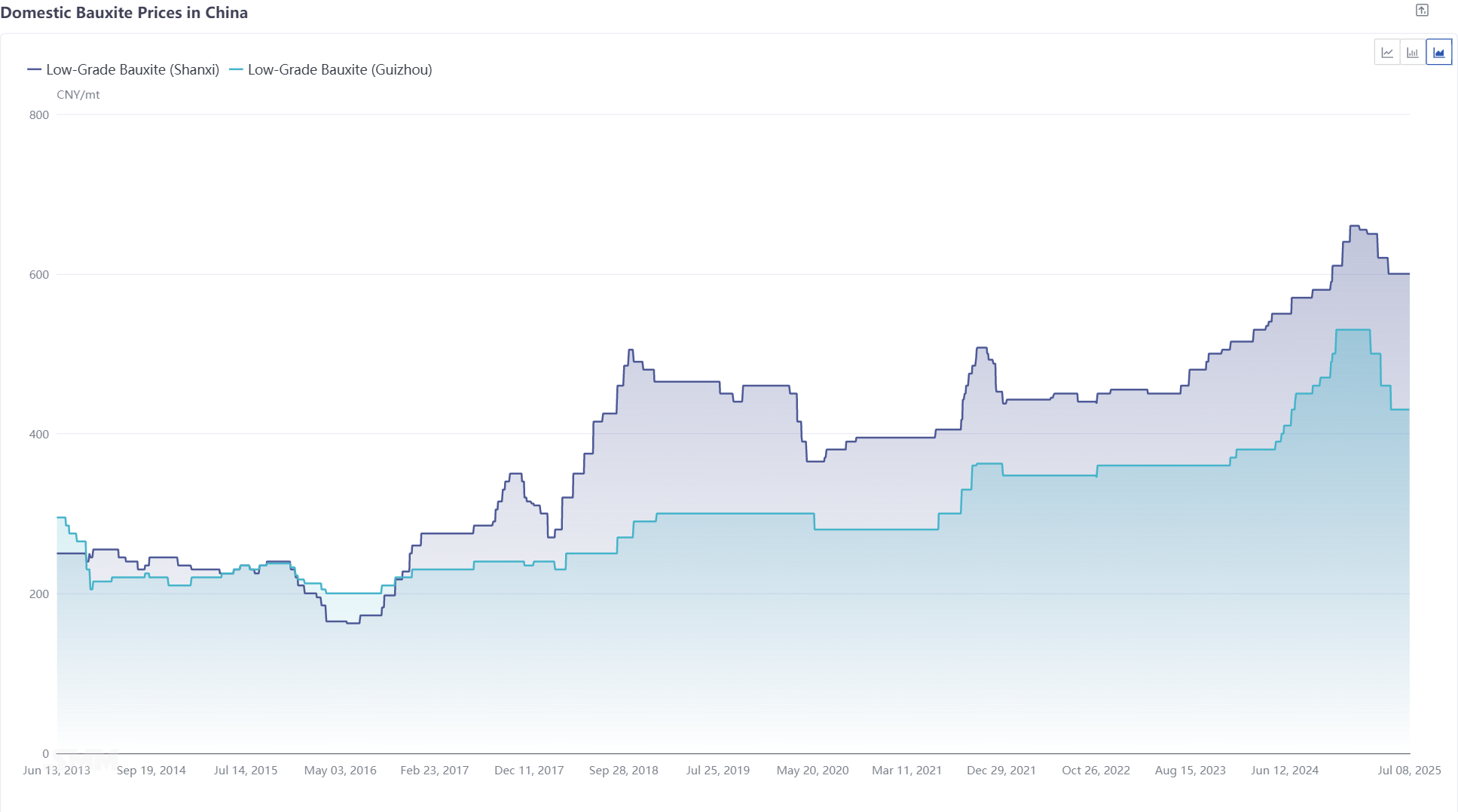

Due to the cost advantages of using domestic bauxite for production, the domestic bauxite market did not experience a surplus. However, as alumina profit margins narrowed, alumina refineries engaged in bargain down purchasing of raw materials. Under this pressure, domestic bauxite prices pulled back, with cumulative price drops of 60 yuan/mt in Shanxi, 30 yuan/mt in Henan, and 100 yuan/mt in Guizhou.

The price pullback of imported bauxite was more pronounced. By June 30, 2025, the SMM CIF index for imported bauxite was reported at $74.21/mt, a decrease of $31.58/mt from the beginning of the year, representing a 29.9% drop, and a decrease of $41.98/mt from the highest price point in H1, representing a 36.1% drop. Breaking it down, the price of imported bauxite mainly went through the following five stages during the year:

- High profits supported alumina refineries' willingness to purchase bauxite at high prices, driving bauxite prices even higher.

In the first half of January, the average profitability of the alumina industry remained above 1,000 yuan. Under such high profitability, alumina refineries had moderate acceptance of high-priced imported bauxite, driving bauxite prices even higher. The SMM CIF index for imported bauxite peaked at $116.19/mt, with some sporadic transaction prices for Guinea's bauxite reaching above $120/mt.

- Alumina prices fell rapidly, and the acceptance of high bauxite prices declined, leading to a price drop.

From mid-January to February, the alumina industry maintained an average profitable situation. With the increase in bauxite supply, the constraints on production increases at alumina refineries due to raw material shortages were gradually lifted. The annualized operating capacity of metallurgical alumina increased to over 90 million mt, and supply continued to be in surplus. Alumina prices fell from around 5,000 yuan/mt to 3,250 yuan/mt, with profits narrowing to within 100 yuan.

During this period, although bauxite maintained a tight balance monthly, providing some support to imported bauxite prices, as alumina profit margins narrowed, alumina enterprises faced the prospect of losses. Alumina refineries' acceptance of high-priced imported bauxite gradually weakened, and imported bauxite prices pulled back from highs. By the end of February, the SMM imported bauxite index was reported at $96.26/mt, a nearly $20/mt drop from mid-January, representing a 17% decline.

- Alumina shifted from profit to loss, alumina refineries engaged in bargain down purchasing prices of raw materials, but sellers remained firm in refusing to budge on prices, leading to a gradual pullback in imported bauxite prices amid the tug-of-war.

In March, alumina prices fell further, and alumina enterprises shifted from profit to loss, with a growing intention to bargain down purchasing prices of raw materials. However, due to good profitability in the early period, most alumina enterprises did not immediately cut production, and alumina operating capacity remained high, with high demand for bauxite. Additionally, the inventory levels of bauxite at ports and within alumina refineries were still low, providing confidence to bauxite sellers in refusing to budge on prices. Amid the tug-of-war between buyers and sellers, imported bauxite prices gradually pulled back. By the end of March, the SMM CIF index for imported bauxite was reported at $93.1/mt, a $3.16/mt drop from the end of February.

- Under the pressure of losses, alumina production cuts occurred, demand decreased, and amid a significant surplus, bauxite prices fell sharply.

From April to May, maintenance and production cuts at alumina refineries were frequent, alumina operating capacity dropped sharply, and demand for bauxite decreased. Meanwhile, bauxite imports remained high, and bauxite surplus was evident. Over these two months, bauxite inventory at ports increased by 5.5 million mt, and alumina refinery inventory increased by about 3 million mt. Imported bauxite prices came under pressure and pulled back. By May 16, the SMM imported bauxite index was recorded at $70.41/mt, a $22.69/mt drop from the end of March, representing a 24.4% decline.

- Driven by the Guinea incident, bauxite prices rebounded slightly, and are expected to remain largely stable thereafter.

Starting in mid-May, the Guinean government began to revoke over 300 mining rights licenses, including some for bauxite mines. On the night of May 16, the market learned that some operating companies were affected, involving significant capacity. This boost led to a slight rebound in imported bauxite prices, with the SMM imported bauxite index peaking at $75.2/mt.

After market sentiment gradually stabilized, the imported bauxite market entered a relatively calm state. With continuous inventory buildup of bauxite and average profitability in the alumina industry being moderate, alumina producers had an intention to bargain down purchasing prices of bauxite. However, the impact of the rainy season in Guinea is expected to gradually set in, and the previous mining license revocation incident has not yet been fully resolved. There is an expectation of a decline in Guinea's bauxite shipments, and suppliers have an intention to refuse to budge on prices. Amid the tug-of-war between buyers and sellers, imported bauxite prices are expected to remain largely stable.

H2 Outlook:

Entering the second half of 2025, supply risks for bauxite still exist, especially in terms of Guinea's imported bauxite supply. Frequent policy disruptions have occurred in Guinea. On July 2, media reported that Bouna Sylla, Guinea's Minister of Mines and Geology, announced a series of "bold" reform measures targeting the country's mining industry. Meanwhile, the previous mining license revocation incident has not yet been fully resolved, making it difficult to quantify the impact on Guinea's bauxite supply. In the second half of the year, there are still significant risks for China's imported bauxite supply.

However, it is certain that the rainy season in Guinea is gradually approaching, and bauxite shipments are expected to decline. Shipping data shows that Guinea's weekly bauxite port departures have already seen a significant drop. The average weekly bauxite port departures in May were about 3.54 million mt, in June were 3.32 million mt, and in the first week of July were 2.58 million mt. Extrapolating to domestic arrivals, it is expected that China's bauxite imports from Guinea will decrease starting from August. Overall, domestic bauxite imports in the second half of the year are expected to decline compared to the first half, and there is a risk of a monthly balance turning into a deficit for bauxite. However, considering that some companies have prepared inventories in advance to cope with the rainy season, the supply-demand imbalance for bauxite is expected to be not obvious in the short term, and bauxite prices are expected to remain largely stable in Q3. But if shipments remain low and domestic bauxite continues destocking, with the imbalance gradually becoming prominent, bauxite prices may turn to hold up well in Q4.