Around June 20, the import and export data of cobalt and lithium battery industry chain-related products for May were released. The data showed that China's total spodumene imports in May reached approximately 605,000 mt, down 2.9% MoM, equivalent to about 53,000 mt LCE. Lithium carbonate imports declined both YoY and MoM but remained at a relatively high level above 20,000 mt... SMM compiled the import and export situation of battery materials as follows:

Upstream

Lithium Concentrates

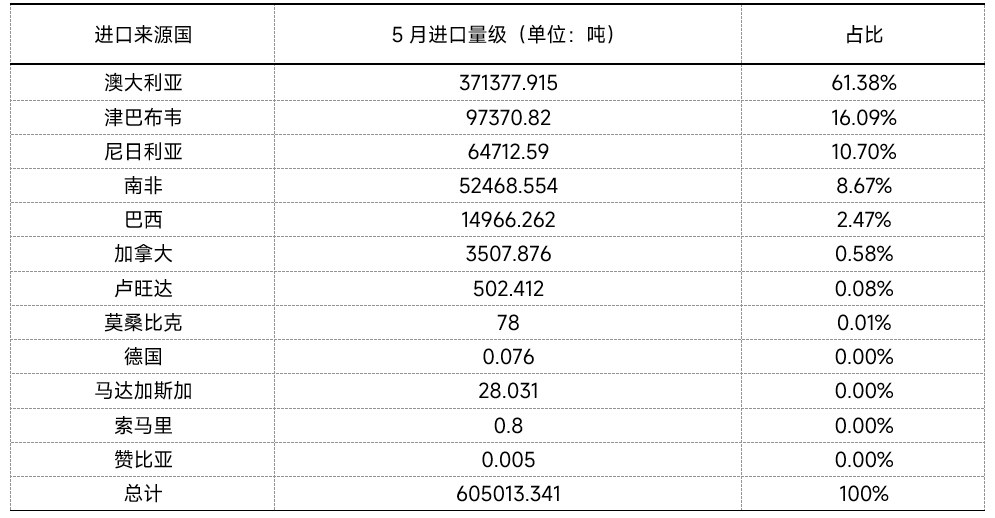

China's total spodumene imports in May reached approximately 605,000 mt, down 2.9% MoM, equivalent to about 53,000 mt LCE.

Specifically, Australia, Nigeria and Zimbabwe remained the top import sources, accounting for 88% of total volume. Imports from Australia and South Africa increased significantly by 24.8% and 29.9% MoM respectively. Lithium ore imports from Zimbabwe stood at 97,000 mt, down 8.2% MoM. Brazilian lithium ore imports totaled 15,000 mt, plunging 71.7% MoM. Canadian lithium ore imports dropped sharply by 89.8% MoM to 3,507 mt.

Additionally, spodumene concentrate imports in May amounted to 517,000 mt, representing 85.4% of total ore imports and remaining basically flat MoM, with most originating from Australia and Zimbabwe.

Data source: China Customs, SMM processed data based on public information

Note: Customs data may not fully reflect the actual spodumeneconcentrateimport volume for the month, with some figures reported only as broad import trends.

[SMM Analysis] China's May Spodumene Imports Hit 605,000 mt, Maintaining High Level

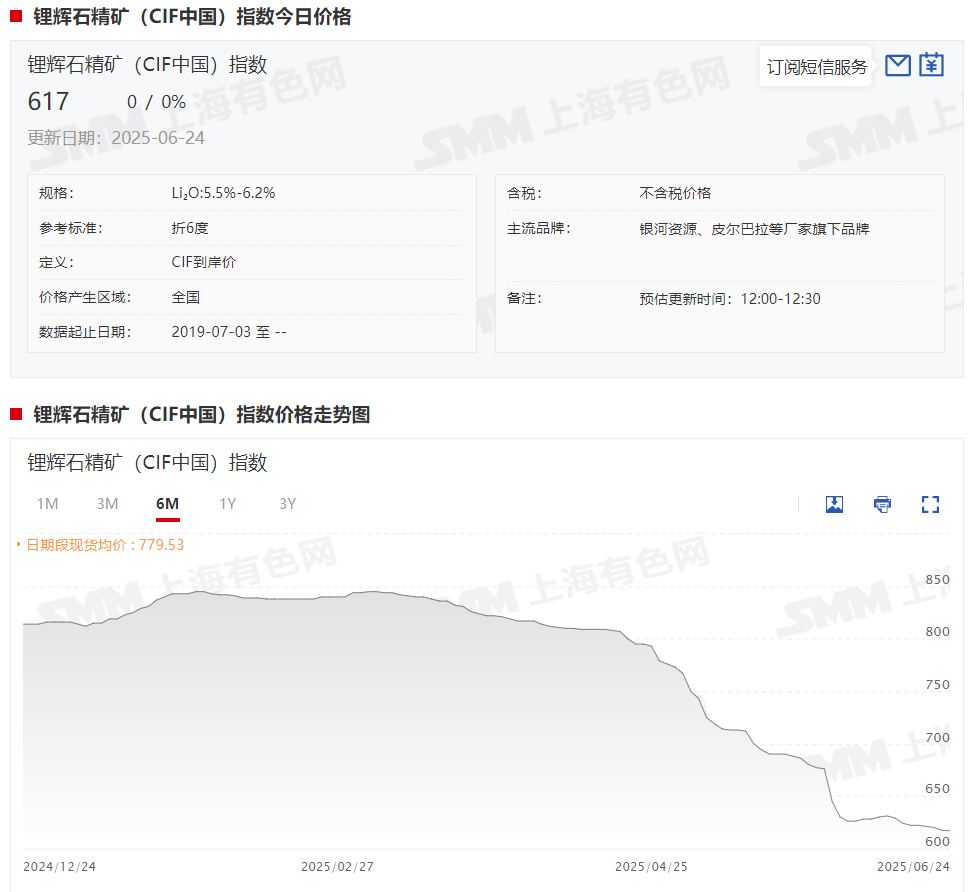

Returning to the current lithium ore market, on the spodumene side, SMM learned thatearly this week, lithium carbonate prices fell noticeably faster, while ore quotations remained basically flat MoM. Downstream lithium chemical plants and purchasing traders showed weak purchase willingness for lithium ore priced at $620/mt and above due to pessimistic expectations about future lithium chemical prices.Overall lithium ore transaction prices still ranged between $600-620/mt, with ore prices expected to fluctuate in sync with lithium carbonate prices later.

As of June 24, the spot price index for spodumene concentrates (CIF China) stood at around $617/mt, down $59/mt or 8.73% from $676/mt at May-end.

Click to View SMM New Energy Products Spot Prices

Lithium Carbonate

Customs data showed:China's total lithium carbonate imports in May 2025 reached approximately 21,146 mt, down 25%MoM and 14% YoY. The average import price was approximately $9,392/mt, down 1.7% MoM from the average price in April.

Among them, imports of lithium carbonate from Chile were approximately 13,393 mt, a 34% decrease MoM, accounting for about 63% of the total imports this time. Imports of lithium carbonate from Argentina were approximately 6,626 mt, a 3% decrease MoM, accounting for about 31% of the total imports this time. Chile and Argentina remain the main sources of China's lithium carbonate imports.

In April, China's lithium carbonate imports saw a significant increase, mainly due to the impact of shipping cycles leading to a concentrated arrival of goods at ports. In May, although imports pulled back from the highs in April, they still remained at a relatively high level of over 20,000 mt. According to the latest export data from Chilean customs, the quantity of lithium carbonate shipped to China in May was approximately 9,700 mt, a 38% decrease MoM. In response, overseas lithium chemical producers stated that this was a normal fluctuation in shipments, influenced also by differences in statistical methods. It is expected that China's total lithium carbonate imports will continue to fluctuate at highs.

In terms of exports, China exported 287 mt of lithium carbonate in May, a 156% decrease MoM and a 35% increase YoY, mainly to Japan and India.

》[SMM Analysis] China's domestic lithium carbonate imports for May 2025 released

Regarding lithium carbonate prices, according to SMM spot quotes, as of June 24, the spot quotes for battery-grade lithium carbonate fell to 59,300-60,500 yuan/mt, with an average price of 59,900 yuan/mt. The average price of lithium carbonate has officially fallen below the 60,000 yuan/mt threshold.

》Click to view SMM's spot quotes for new energy products

Reviewing the lithium carbonate market in May, according to SMM, affected by the continuous and significant decline in lithium carbonate prices, some non-integrated lithium chemical plants were unable to withstand the cost pressure and reduced or halted production, leading to a decrease in domestic lithium carbonate output. Downstream demand was driven by the rush to export of ESS battery cell enterprises and the increase in power demand in the first half of the month, resulting in a considerable increase in demand throughout the month. The marginal improvement in the supply-demand pattern shifted the apparent demand from oversupply to a tight balance. However, the phased rebound in futures prices provided lithium chemical plants with opportunities for hedging profits, stimulating expectations of a restorative increase in supply in June.

Looking at the current situation, according to SMM surveys, the lithium carbonate market still maintains a basic pattern of oversupply. In terms of supply, there is an abundant supply of goods circulating in the market. In terms of demand, downstream material enterprises have low purchase willingness and mainly focus on restocking for rigid demand. Due to the uncertainty in production schedules for July, there are currently no signs of concentrated stockpiling. From a price performance perspective, the market is showing a divergent trend: leading lithium chemical enterprises, with a relatively high proportion of long-term contracts and limited spot order supply, are maintaining relatively firm quotes. However, some small and medium-sized lithium chemical plants, affected by inventory and financial pressures, have seen some relaxation in their quotes. Nevertheless, downstream buyers are generally adopting a wait-and-see attitude, resulting in sluggish overall market transactions. Overall, against the backdrop of no significant recovery in end-use demand and high inventory levels across the industry chain, it is expected that lithium carbonate prices will likely continue to fluctuate at lows in the short term.

Lithium Hydroxide

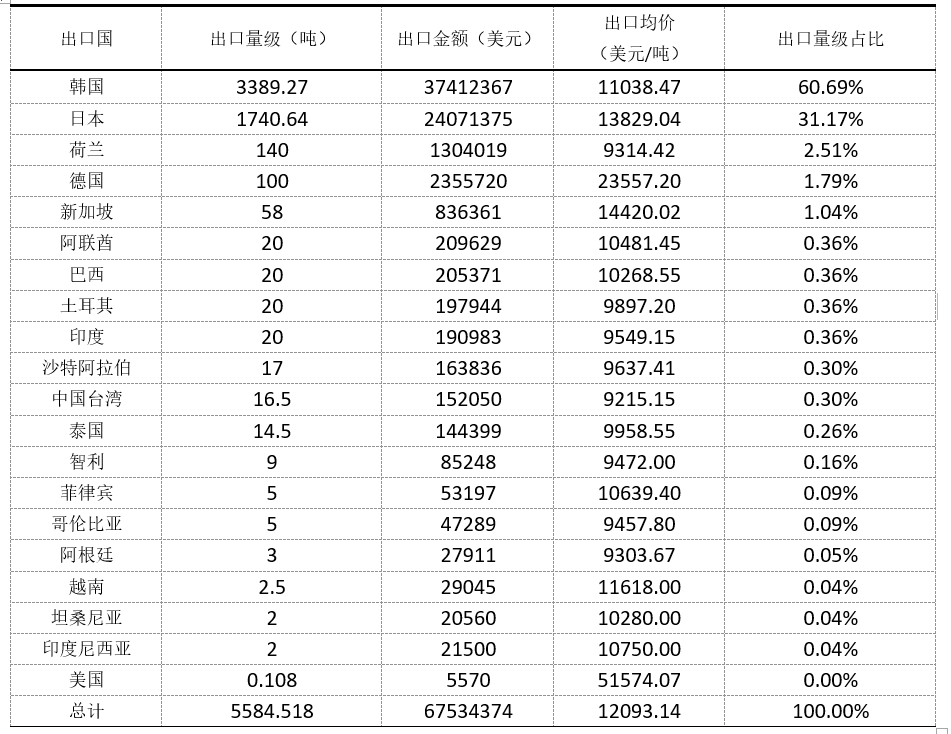

According to customs data, China's lithium hydroxide exports reached 5,585 mt in May, up 32.3% MoM. Exports to South Korea amounted to 3,389 mt, accounting for 61% of China's total exports, up 65.5% MoM. Exports to Japan reached 1,740 mt, accounting for 31.2% of China's total exports, with the volume basically flat MoM. The average export price of lithium hydroxide from China in May was $12,093/mt, down 15% MoM.

Additionally, China's lithium hydroxide imports amounted to 842 mt in May, down 34% MoM.

Data source: General Administration of Customs, compiled by SMM

》[SMM Analysis] China's lithium hydroxide exports increased to 5,585 mt in May

Battery Materials

Ternary Cathode

May Imports

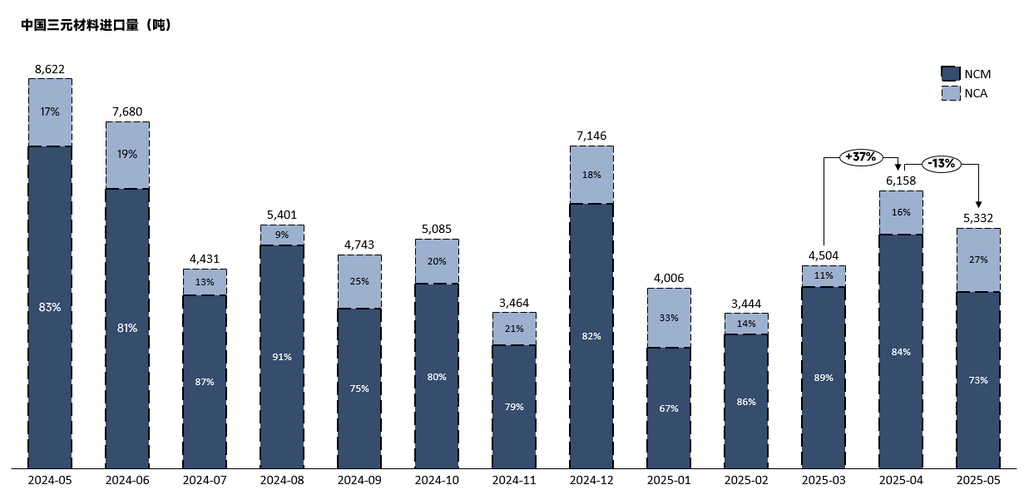

In May 2025, China's imports of ternary cathode materials (combined NCM+NCA values) reached 5,332 mt, down 13% MoM and 38% YoY. Among them, NCM imports were 3,901 mt, down 25% MoM and 45% YoY. NCA imports were 1,431 mt, up 45% MoM and down 4% YoY.

May Exports

In May 2025, China's exports of ternary cathode materials (combined NCM+NCA values) reached 9,021 mt, down 4% MoM and up 31% YoY. Among them, cumulative NCM exports were 8,775 mt, down 3% MoM and up 31% YoY. Countries with sustained recovery in overseas demand mainly include Japan, Germany, Malaysia, and India. NCM exports to Japan reached 1,108 mt in May, increasing slightly by 92 mt. Exports to Germany reached 425 mt, up 412% MoM. Exports to Malaysia and India were 273 mt and 34 mt, respectively.

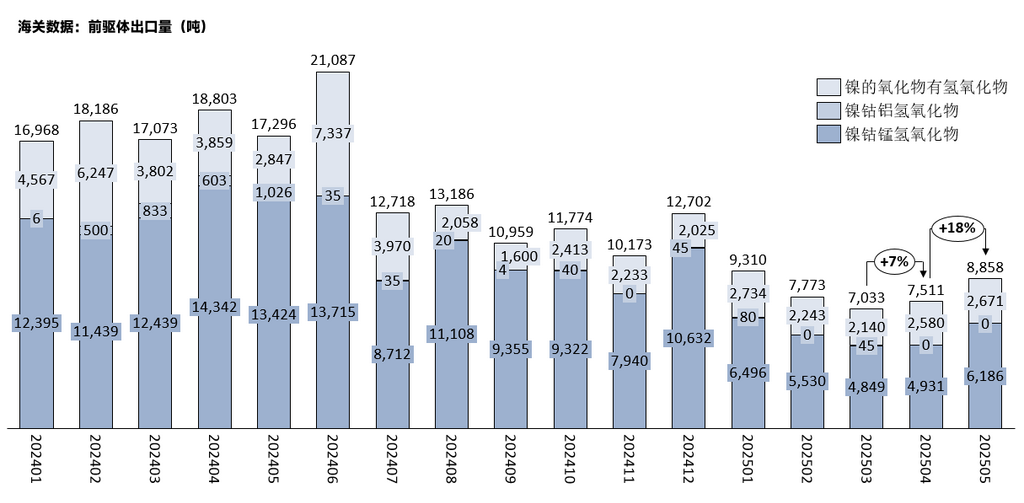

Ternary Cathode Precursor

In May 2025, China's exports of ternary cathode precursors reached 8,858 mt, up 18% MoM and down 49% YoY.

In May, the overall export volume of ternary cathode precursors increased compared to April. Among them, the export volumes of NCM and NC have rebounded. The total export volume of NCM in May was 6,186 mt, up 25% MoM and down 54% YoY. The total export volume of NC in May was 2,671 mt, up 4% MoM and down 6% YoY. There were no exports of NCA in April and May.

By country, South Korea remained the main export destination for China's ternary cathode precursors in May, accounting for 92% of total exports of NC, at 2,461 mt; and 83% of total exports of NCM, at 5,111 mt. Poland and Morocco ranked second and third, with export volumes of 480 mt and 437 mt, respectively.

》【SMM Analysis】Analysis of Ternary Cathode Precursor Exports in May

Artificial Graphite

In May 2025, China's imports of artificial graphite stood at 1,253 mt, up 11% MoM and 52% YoY. In terms of average import price, in May 2025, the average import price of artificial graphite in China was 43,809 yuan/mt, down 34% MoM and 42% YoY.

Data source: SMM, China Customs

In May 2025, China's exports of artificial graphite reached 52,020 mt, down 11% MoM and up 21% YoY. In terms of average export price, in May 2025, the average export price of artificial graphite in China was 8,875 yuan/mt, down 3.4% MoM and 37% YoY.

In May 2025, with the easing of tariff policies, domestic imports of anode materials increased significantly; coupled with the continuous decline in raw material coke prices, domestic supply also rose, leading to an increase in anode material supply in May. The imbalance in the supply-demand pattern intensified, resulting in a decline in the average import price. Meanwhile, affected by fierce market competition in recent years, the average import price saw a YoY decline of 42%.

In May 2025, the sharp fluctuations in coke prices in the earlier period led to the depletion of industry inventory to a low level. As a result, domestic exports of artificial graphite in May 2025 decreased by 11% MoM.

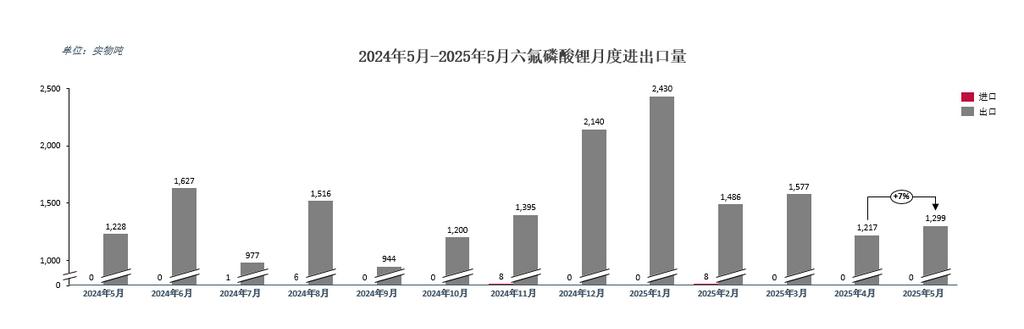

LiPF6

According to China Customs data, in May 2025, China's cumulative exports of LiPF6 stood at 1,299 mt, up about 7% MoM, and cumulative imports of LiPF6 were 0 mt.

In terms of exports, in May 2025, China's exports of LiPF6 reached 1,299 mt, up about 7% MoM and about 6% YoY compared to April. Specifically, 120 mt of LiPF6 was exported to Poland, down about 67.7% MoM; 157.403 mt was exported to Japan, down about 22.7% MoM; 229.684 mt was exported to South Korea, up about 34.2% MoM; and 373.143 mt was exported to the US, up about 250% MoM, showing a significant increase.

Overall, overseas procurement volumes of LiPF6 increased slightly in May.

》【SMM Data】Import and Export Data of LiPF6 in May 2025

Cobalt

Cobalt Hydrometallurgy Intermediate Products

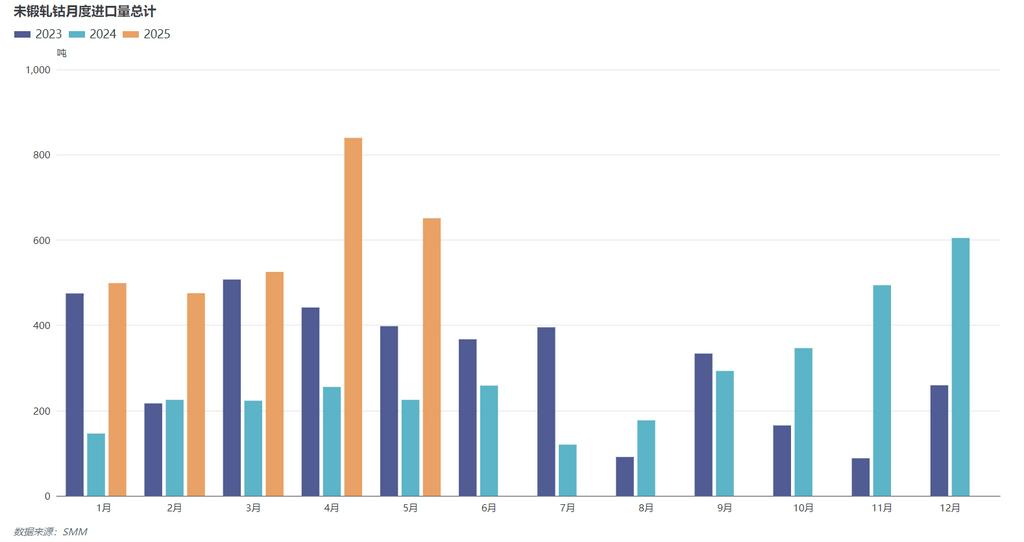

In May 2025, China's imports of cobalt hydrometallurgy intermediate products were approximately 49,487 mt, down 7% MoM and 6% YoY, of which imports from the DRC were approximately 48,493 mt, down 8% MoM and 7% YoY. In May 2025, the average import price of unwrought cobalt in China was $6,749/mt, up 21.89% MoM. From January to May 2025, China's cumulative imports reached 248,287 mt, down 7.09% YoY.

》[SMM Analysis] In May 2025, China's imports of cobalt hydrometallurgy intermediate products dropped back slightly.

Unwrought Cobalt

In May 2025, China's imports of unwrought cobalt were approximately 651 mt (metal content), down 23% MoM and up 189% YoY. Regarding the average import price, in April 2025, the average import price of unwrought cobalt in China was $30,306/mt (metal content), up 12.96% MoM. From January to May 2025, cumulative imports reached 2,990 mt (metal content), up 178.4% YoY.

In terms of exports, in May 2025, China's exports of unwrought cobalt were approximately 2,986 mt (metal content), down 27% MoM and up 433% YoY. Regarding the average export price, in March 2025, the average export price of unwrought cobalt in China was $32,302/mt (metal content), up 3.80% MoM. From January to May 2025, cumulative exports reached 10,383 mt (metal content), up 232.68% YoY.

》[SMM Analysis] In May 2025, China's exports and imports of unwrought cobalt dropped back slightly.

Cobalt Chloride

According to customs data, in May, China exported 3,000 kg of cobalt chloride, down 75% MoM and 3% YoY, all of which was exported to the UK. From January to May, China's cumulative exports of cobalt chloride reached 1,321 tons, up 107% YoY.

Co3O4

According to customs data, in May, China imported 0.1 ton of Co3O4, down 100% MoM and 100% YoY. China exported 334 tons of Co3O4, down 36% MoM and 27% YoY. Among them, 199 tons of Co3O4 were exported to South Korea, accounting for 60% of the total exports. From January to May, China's cumulative exports of Co3O4 reached 1,930 tons, up 6% YoY.

》In May 2025, China imported 0.1 ton of Co3O4 and exported 334 tons of Co3O4 [SMM Data].