SHANGHAI, Jun 8 (SMM) -

Copper cathode

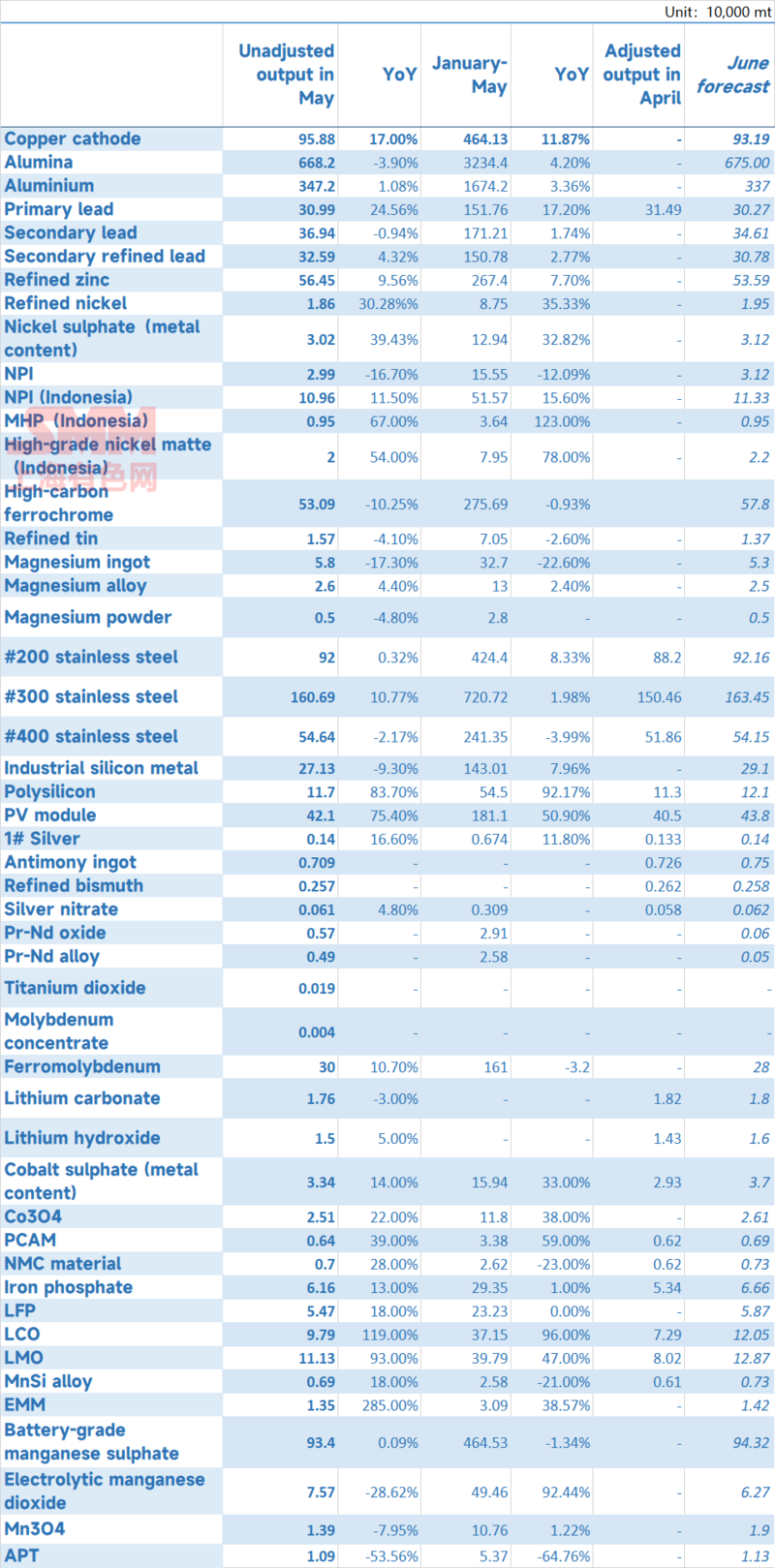

SMM data showed that China's copper cathode output stood at 958,800 mt in May, down 11,200 mt or 1.2% MoM, but a rise of 17% YoY, and the output was 5,300 mt higher than expected. The output totalled 4.64 million mt in January-May, an increase of 492,500 mt or 11.87% year-on-year.

According to SMM, scheduled maintenance from five smelters was responsible for 29,100 mt reduction in May. Notwithstanding low price and supply overhang, there was no smelters selling sulphuric acid for free. Some smelters with tight inventory of sulfuric acid purchased more blister copper and copper anode while reducing use of copper ore. Increased maintenance and purchases lowered RCs of blister copper by 250 yuan/mt MoM to 1,050 yuan/mt as of June 2. The average operating rate of copper cathode industry declined by 3.5 percentage points MoM to 87.90% in May.

According to SMM statistics, there will be scheduled maintenance from eight smelters in June, involving a total output cut of 54,400 mt. Meanwhile, restart of facilities that went down earlier and start-up of new capacity of a new smelter in Shandong will take place in June.

To sum up, China's copper cathode output is estimated at 931,900 mt in June, down 26,900 mt or 2.81% MoM and up 8.7% YoY, which will probably bringing output from January to June up to 5.5732 million mt, an increase of 11.33% year-on-year, or 567,400 mt. There will be only five smelters that shut units for maintenance in July.

Aluminium

According to SMM statistics, the output of aluminum in China was 3.472 million mt in May with 31 days, a year-on-year increase of 1.08%, bringing output from January to May up to 16.742 million mt, a year-on-year increase of 3.36%. In May, the growth rate of aluminum production capacity slowed down amid a few restart in Guizhou and stable operating rate in other regions. The daily output of aluminum increased by 404 mt from the previous month to around 112,000 mt. In May, with new capacity coming on-stream in the Northwest and South-west regions, share of molten aluminum output at domestic smelters registered a record high in May, hiking by 2.3 percentage points to 75.5%.

Capacity changes: In May, operations of aluminium smelters remained unaltered, except for that in Guizhou. Enterprises fully resumed production in Zunyi and Liupanshui, and slowed down the pace of production in Guzhou. July will probably see full production. In May, the resumption of production capacity in Guizhou was about 180,000 mt, and production capacity that was taken down involved around 50,000 mt in in Anshun. According to SMM statistics, as of now, installed capacity reached 45.29 million mt (including the production capacity that was not putted into production), and operating production capacity increased to 40.923 million mt. Operating rate was about 90.4% in China, a month-on-month increase of 0.4 percentage point.

Production forecast: As of now, there are 200,000 mt of pending production capacity in Guizhou and Sichuan to be resumed. In June, a possible restart will be monitored in late June on increased rainfalls in Yunnan, but is expected be slowed down by the short rainy season. The capacity of nearly 2 million mt will fail to fully resume production in the short term, and there is estimated 100,000 mt of capacity reduction in Shandong. SMM predicted that operating aluminum production capacity in China may increase to around 41.15 million mt by the end of June, and aluminum output in China in June with 30 days may be around 3.37 million mt, a year-on-year increase of 0.28%.

On the demand side, downstream sectors showed a mixed performance in May, with operating rate inching lower in aluminium plate/sheet, strip and foil and aluminium extrusion, and standing stable in the industrial aluminium extrusion. However, more new production capacity of aluminium billet was putted into production, and the proportion of molten aluminum output in the industry continueed to be high. Aluminum ingots stocks shrank to 232,000 mt in May. Only about 6,000 mt of aluminium billet inventory was depleted in May on supply increment and moderate downstream demand. In June, share of molten aluminum output may edge down, and the destocking of aluminum ingots may slow down slightly. SMM predicted that social inventory of aluminum ingots at the end of June may be around 500,000 mt.

Alumina

According to SMM data, in May (31 days), the output of metallurgical grade alumina in China was 6.682 million mt, with the average daily output decreasing by 2,500 mt/day to 216,000 mt/day, owing to slow-down of new capacity growth and concentrated maintenances. The number of production days in May increased by one day compared with April, so the total output increased by 2.2% month-on-month. Alumina production in May fell by 3.9% YoY in May, citing shut-down of some alumina facilities triggered by high-cost alumina in Shanxi, Henan, Inner Mongolia and other regions, and the operating rate remained low. As of the end of May, China's installed alumina production capacity was 100.25 million mt, the operating production capacity was 79.1 million mt, and the national operating rate was 78.9%.

In Shanxi, notwithstanding finished alumina price erosion, operating rate trended up by 3.6 percentage point MoM to 73% amid soft prices of caustic soda and coal. In Henan, The operating rate remained low at 64.6%. In Guizhou, operating rate dipped by 18.1 percentage point MoM to 75%, mainly due to a few scheduled maintenance, will improve this month. In Hebei, with start-up of new capacity, the operating rate hiked from 76% in April to 90.6% in May. Operating capacity in May rose to 4.35 million mt per year, and is expected increase to reach full production in a short run. The operating rate rose from 87% to 90.6% in Guangxi in May, and dropped 3.1 percentage point MoM to 88.2% in Shandong on a few planned overhauls and a consecutive fall in alumina prices.

Forecast for June: In June new capacity in Shandong, Guangxi and Hebei will come on-stream, and capacity in Guizhou and Chongqing will resume normal production. SMM expected the average daily output in June to be 225,000 mt/day and the total output to be about 6.75 million mt.

Primary lead

The output of refined lead was 309,900 mt in May, down 1.59% month-on-month and up 24.56% year-on-year, and hiked by 17.2% year-on-year from January to May. In 2023, the total production capacity of the surveyed enterprises was 5.8357 million mt.

According to SMM research, refined lead production decreased after an initial increase in May, due to restart of capacity in Hunan, and Qinghai in early month and scheduled turnaround in Henan, Shandong, Inner Mongolia, Guangdong and Liaoning in mid-to-late May.

In addition, with start-up of new capacity in Henan in H1 2023 and shut-down of lead smelters in Hunan Yongxing in May 2022 caused by safety accident, the output in May was higher than the same period of last year.

Refined lead production will drop in June on maintenance. From the perspective of raw materials, since the end of May, lead prices continued to fall, while lead concentrate supply tightened, especially the TCs of silver-rich lead concentrates moved up. Under this circumstance, smelters reached the cost line. In addition, falling prices and inventory overhang forced enterprises to cut production. On the whole, SMM expected that the output of refined lead in June will continue to inch lower to 303,000 mt.

Secondary lead

For secondary lead, the output was 369,400 mt in May, a rise of 5.48% MoM and a decrease of 0.94% YoY, and output from January to May was 1.7121 million mt. For secondary refined lead, the output was 325,900 mt in May, and 1.5078 million mt from January to May.

Production of secondary refined lead in May in China increased compared with April, citing facilities from some large smelters, such as Anhui Huabo, Shandong and Zhongqing operating at full capacity. The operating rate of large refineries in May increased by 8.28% compared with April, the operating rate of medium-sized refineries in May decreased by 4.09% compared with April, and the operating rate of small refineries in May decreased by 5.41% compared with April. Sluggish lead price and raw material shortage and high costs led most secondary lead smelters to have meager profits even losses in May. June will witness expected normal operation in Jiangxi Fengri ovens, higher output from May in Hubei Jinyang and Kangdeli after maintenance, and maintenance in Anhui Huaxin, Chifeng Jinfan and other enterprises. To sum up, it is expected that the output of secondary refined lead will decrease by about 18,000 mt in June, and the operating rate will be about 54.97%.

Refined zinc

According to SMM survey, Chinese refined zinc output stood at 564,500 mt in May, an increase of 24,500 mt or 4.54% MoM and 9.56% YoY, slightly exceeding expectations. From January to May, output reached 2.674 million mt, an increase of 7.7% year-on-year. Among them, the domestic die-casting zinc alloy production in May was 85,940 mt, a decrease of 245 mt from a month before.

In May, the production of domestic zinc smelters was relatively stable, and the medium and large smelters of domestic mineral zinc almost maintained full-capacity production. Only some smelters in Shaanxi were routinely overhauled. Due to the low price of sulfuric acid, some smelters were routinely overhauled at the end of the month. Despite secondary zinc smelters had little profits, most smelters maintain normal production.

SMM predicted that domestic refined zinc production in June 2023 will decrease by 28,700 mt MoM and an increase of 9.7% YoY to 535,900 mt. The output from January to June will reach 3.21 million mt, an increase of 8.03% year-on-year. The operating rate will largely stand stable in June. As most smelters in the north will carry out maintenance, it is expected that the overall refined zinc output will further decrease in July.

Refined tin

Chinese refined tin output was 15,660 mt in May, up 4.72% on the month but down 4.1% on the year. The total output from January to May fell 2.6% YoY. A smelter in Jiangxi had previously signed a new scrap supplier, which further pushed up its output. In addition, a smelter in Anhui greatly ramped up its production during the month. Most of the remaining smelters in the SMM survey said that their production was stable, and the output of some enterprises increased only slightly.

In the second half of May, most smelters indicated that the supply of raw materials such as tin ore and scrap was low, which limited their output growth. Most smelters in Yunnan maintained low operating rates and will not cut their production on a large scale unless the supply of tin ore is particularly low. In south-west China and Guangdong, two smelters carried out maintenance, which results in a sharp decline in tin ingot output in June. In Jiangxi, Anhui and Zhejiang, most of the smelting companies are tin scrap recycling and smelting enterprises, and most of them said that as the scrap supply is low, their output may fall slightly in the near term.

Refined nickel

Chinese refined nickel output totalled 18,600 mt in May, up 5.67% MoM and 30.28% YoY. The output increase was in line with expectations. Although the sharp decline in nickel prices in May has narrowed the profit margin of electrowinning nickel, the new electrowinning nickel companies maintained normal production during the month, and some manufacturers in north and South China even increased their output.

The output in June will be 19,500 mt, up 4.40% MoM and 25.08% YoY, because a smelter in north-west China that carried out overhauls is expected to resume production in late June. In addition, the new electrowinning nickel production lines in south China will be put into production. Refined nickel output in June will grow as some companies are ramping up their electrowinning nickel production during the year.

NPI

Chinese NPI output stood at 745,000 mt in physical content in May, up 9.06% MoM but down 16.68% year-on-year. The total Ni content was 29,900 mt. Profits of NPI plants increased somewhat amid stable NPI prices and low nickel ore and coke prices. In addition, stainless steel mills increased their production significantly during the month, which further promoted the NPI factories to resume their production. In detail, the output of high-grade NPI was about 22,600 mt in Ni content, up 3.31% MoM, and that of low-grade NPI added 11.96% on the month to 7,300 mt in Ni content as some profit-making low-grade NPI companies integrated with stainless steel capacity ramped up their production.

It is estimated that the Chinese NPI output in June will gain 7% from May to around 31,900 mt in Ni content. Although some high-grade NPI plants will undertake maintenance, the overall Chinese NPI output will still rise thanks to the production resumption of some factories which carried out overhauls earlier, the considerable profits, and the higher cost efficiency of domestic NPI than Indonesia NPI.

Indonesia NPI

Indonesia NPI output stood at 109,900 mt in Ni content in May, up 1.13% month-on-month and 11.9% year-on-year. Output from January to May totalled 516,100 mt in Ni content, up 15.6% year-on-year. Some companies ramped up the production as power supply in some regions resumed. Besides, stainless steel mills maintained high operating rates during the month. In terms of costs, nickel ore prices dropped following the nickel prices. Coke prices also slumped. NPI plants thus gained considerable profits and thus increased their production. However, some factories reduced output due to maintenance or some other reasons. Therefore, the increase in supply was actually lower than expected. In May, due to the recovery of demand from the new energy sector, the companies were more active in producing high-grade nickel matte than NPI. SMM believes that some NPI enterprises may switch their NPI production lines to high-grade nickel matte. In June, with the rapid commissioning pace, the Indonesia NPI output will reach 113,300 mt in Ni content, an increase of about 3.37% month-on-month and a year-on-year rise of 13.3%.

Nickel sulphate

Chinese nickel sulphate output stood at 148,800 mt in physical content or 32,700 mt in metal content in May, up 8.54% on the month and 36.11% on the year, driven by the expanding demand. Ternary precursor companies ramped up their nickel sulphate purchases amid the growing downstream demand, enabling the nickel salt enterprises to resume production. Nickel sulphate output will rise further to 34,100 mt in metal content in June boosted by low in-plant stocks held by the producers and the increasing downstream demand.

Battery-grade manganese sulphate

China produced 13,900 mt of high-purity manganese sulphate in May, up 93.59% MoM, because manganese salt companies integrated with precursor capacity increased their production amid the small growth of demand from the power battery sector. On the supply side, many high-purity manganese sulphate enterprises maintained a low operating rate, and only a few companies increased output due to optimism about the market outlook or the production ramp-up at the end of the quarter. In terms of demand, ternary precursor enterprises only consumed their in-plant raw material inventories.

Entering June, production of ternary battery cells is low, which fails to boost the operating rates of ternary precursor companies. The output of manganese sulphate solution at manganese salt enterprises integrated with precursor capacity will increase slightly in June, and some high-purity manganese sulphate enterprises with less inventory pressure will also begin to resume their work. The output will be 19,000 mt in physical content in June, up 36.69% MoM.

EMD

Chinese electrolytic manganese dioxide (EMD) output was 10,900 mt (including 1,500 mt for LMO battery, 5,700 mt for alkaline manganese battery, and 3,600 mt for zinc-carbon battery) in May, up 7.59% MoM but down 53.56% YoY. EMD output in the first five months of 2023 stood at about 53,700 mt, down 64.76% on the year. The output of EMD (for alkaline manganese battery) decreased somewhat from the previous month, but that of EMD (for LMO battery) rose significantly driven by the better demand.

In June, as the demand for EMD (for LMO battery) is relatively high, the EMD companies will increase the production of EMD (for LMO battery), which will push the overall EMD output up to around 11,300 mt.

Mn3O4

SMM data showed that in May 2023, Chinese Mn3O4 output was 10,600 mt (including 4,500 mt of electronics-grade Mn3O4 and 6,100 mt of battery-grade Mn3O4), up 12.73% MoM but down 5.93% YoY. The output in the first five months of the year totalled about 55,700 mt, down 6.81% on the year. As lithium carbonate prices soared during the month, LMO battery plants restocked more Mn3O4, further boosting the Mn3O4 production.

In June, the operating rates of LMO battery companies will still be high, and the Mn3O4 producers will ramp up their production accordingly. The Mn3O4 output will be around 11,200 mt.

High-carbon ferrochrome

The output of high-carbon ferrochrome dropped 25,300 mt or 4.55% MoM and 60,600 mt or 10.25% YoY to 530,900 mt in May. The output in Inner Mongolia was 333,900 mt, down 9,300 mt or 2.71% MoM, while that in Sichuan stood at 30,200 mt, up 67.78% on the month. High-carbon ferrochrome bid price for May disclosed by major stainless steel mills were flat from the previous month. But the chrome ore prices stood high. Therefore, ferrochrome companies in areas with high electricity prices such as Guizhou and Hunan had to cease production. In north China, the profit-making big factories maintained normal production. In Sichuan, many ferrochrome producers resumed work amid dropping electricity prices during the rainy season, and the output at these plants was stable.

The output of high-carbon ferrochrome is expected to rise slightly to 578,000 mt in June. Stainless steel mills have raised the high-carbon ferrochrome bid price for June by 200 yuan/mt (Cr 50%), and the stainless steel production rises further, which will promote the ferrochrome plants to produce finished products in spite of the bearish sentiment. In addition, profits of some ferrochrome plants in the south will grow amid the falling electricity prices during the rainy season and the declining coke prices.

Stainless steel

According to SMM survey, Chinese stainless steel output totalled 3.07 million mt in May, up 5.79% MoM and 5.03% YoY. In detail, the output of 200-series stainless steel added 4.31% on the month to 920,000 mt, that of the 300-series gained 6.80% to 1.61 million mt, and that of the 400-series stood at about 546,400 mt, up 5.36% MoM.

The overall crude stainless steel output climbed to a high level in May. During the month, amid the NPI supply surplus and falling prices, the profits of 300-series stainless steel were good, and new production projects were also carried out as scheduled. 200-series output also rose on the month spurred by the rapidly growing profit margins. The output of 400-series stainless steel increased slightly during the month.

In June, the prices of stainless steel may weaken in the traditional off-season. The profit margin of the 300-series is gradually narrowing, and the stocks held by the stainless steel mills grow somewhat due to the shipment controls earlier. The mills thus are more cautious about the 300-series stainless steel production. 200-series output may not change much from the previous month, and the mills will gain some profits. The overall 400-series stainless steel output may decrease slightly in June because of the mills’ losses. Therefore, the crude stainless steel output will rise slightly MoM in June.

EMM

SMM data showed that Chinese EMM output stood at 75,700 mt in May, down 35% on the month and 28.62% on the year, which was caused by the slack market trades and the production cuts or suspension carried by small plants with huge inventory pressure. The output in the first five months of 2023 totalled around 494,600 mt, up 92.44% year-on-year. On the demand side, the stainless mills with low profit margins restocked EMM only on rigid demand.

In June, production of stainless steel mills will grow slightly boosted by the acceptable profits of 200-series. The small and medium-sized EMM plants will suspend production, while the big ones may maintain normal operation. The overall EMM output is expected to be around 62,700 mt in June.

Industrial silicon

According to SMM statistics, China's industrial silicon output in May was 271,000 mt, a decrease of 20,000 mt or 6.8% from the previous month, and a year-on-year decrease of 28,000 mt or 9.3%. From January to May 2023, the cumulative industrial silicon output was 1.43 million mt, an increase of 8% year on year.

In May, the output of industrial silicon decreased significantly both month-on-month and year-on-year. Industrial silicon prices fell more than expected, and production areas such as Xinjiang, Inner Mongolia, and Guizhou, especially small and medium-sized silicon companies, were less motivated to produce under the pressure of losses. This, combined with lower operating rates at some silicon companies for a long period, resulted in a larger number of producers that cut output or suspended production. At the same time, the suspension of some production capacity in Baoshan, Yunnan and other places for maintenance also reduced the output in May by about 5,000 mt from the previous month.

Sichuan region entered the flat water period in May. Although the progress of silicon enterprises' resumption of production was slow, the output in May increased by nearly 7,000 mt month-on-month.

Entering June, the market remained pessimistic about the industrial silicon market. The delayed arrival of the rainy season in south-west China led to tight supply of hydropower, and the resumption of production of silicon factories in south-west China was slow. In other regions, only a few silicon plants planned to restart production in June, and most of other plants will remain closed. China's industrial silicon output is expected to rise to around 290,000 mt in June.

Polysilicon

The output of polysilicon stood at around 117,000 mt in May, up 2.63% on the month, according to SMM statistics. Domestic polysilicon supply continued to grow. Although the price of polysilicon continued to fall, the profit was still relatively high. Enterprises maintained high operating rates. At the same time, the ramp-up of new production lines at Inner Mongolia Daquan Energy and Ningxia Runyang Silicon Material Technology also increased polysilicon production.

PV module

According to SMM statistics, domestic module production in May was about 42.1 GW, an increase of 2.6% from April. The growth rate from the previous month slowed significantly. In May, the price of the entire upstream photovoltaic market "collapsed", and the confidence of the downstream market was depressed. Terminal enterprises began to slow down the delivery-taking. At the same time, due to the high price of cell enterprises and terminal enterprises pushing for lower prices, the profit of modules was not guaranteed. The second-tier and third-tier enterprises generally cut production. Under the pressure, the production schedule of modules was lower than expected.

SiMn alloy

Chinese SiMn alloy output stood at 934,000 mt in May, up 4.26% on the month and 0.09% on the year, SMM data showed. From January to May 2023, the SiMn alloy output in China was 4.65 million mt, a drop of 1.34% year-on-year. Due to the orders from National Food and Strategic Reserves Administration, the operating rates of a large factory in Guizhou increased in May. Although some alloy factories reduced output, the overall output growth exceeded output declines. Restricted by high electricity prices in Guangxi, only some SiMn alloy 6014 plants in the region restarted production. Some alloy enterprises in Ningxia, the main production area in the north, increased production schedules, and their output grew month-on-month. Although plants in Inner Mongolia undertook maintenance, the overall output was relatively stable. On the whole, the SiMn alloy output increased in May.

Entering June, there is strong expectations of resumption of work in the south, but lower price of SiMn alloy may lead to reduction of the supply side. Considering that the current supply pressure, the resistance to a sharp increase in production is relatively strong. The output of SiMn alloy is projected to grow slightly to around 943,200 mt in June.

Magnesium ingot

China's magnesium ingot output stood at 58,000 mt in May, down 17.3% MoM and down 32.7% YoY, according to SMM statistics. The output totalled 327,000 mt in January-May 2023, a year-on-year decrease of 22.6%.

With the implementation of the semi-coke rectification policy in the main magnesium ingot production areas, the supply decreased sharply. In addition, the sluggish downstream demand and the continuous declines in magnesium prices, caused plants to reduce output. The overall supply thus dropped. According to the current production schedule plans of the producers, the output cuts may further expand due to the continued sluggish downstream demand. The output in June is expected to be about 53,000 mt.

Magnesium alloy

According to SMM data, China's magnesium alloy output stood at 25,500 mt in May, down 4.4% month on month and 7.4% on the year. The output totalled 130,000 mt from January to May, a year-on-year increase of 2.4%.

Judging from the current market transaction, the domestic magnesium alloy market demand is relatively stable, but due to the continuous sluggish export orders, magnesium alloy enterprises were more pessimistic. According to customs data, China’s magnesium alloy exports in April fell by 19% year-on-year. It is estimated that the output of magnesium alloy in June will remain low and stabilise at about 25,000 mt.

Magnesium powder

China's magnesium powder output stood at 5,000 mt in May, down 4.8% MoM. The output totalled 28,000 mt in January-May 2023.

The magnesium powder market remained weak in May. Affected by fluctuations in raw material prices, downstream purchases were generally more cautious. A magnesium powder company said that orders fell by 30% compared with the same period last year. With high magnesium prices, stronger advantage of rival products as well as sluggish demand in the near term, the output of magnesium powder is expected to be about 5,000 mt in June.

PrNd oxide

Domestic output of PrNd oxide in May 2023 stood at 5,741 mt, down 3.6% MoM. Among them, the output in Guangxi, Shandong and Sichuan was significantly reduced, and the output in other regions remained basically the same as in April.

According to SMM survey, at present, the spot supply of rare earth oxides is insufficient, and the sellers were more reluctant to sell. Quotations were relatively firm. Although downstream PrNd alloy factories were reluctant to accept high-priced spot goods due to losses, sellers refused to lower prices and it was still difficult to purchase low-priced goods. Due to the shrinking profits of rare earth ore, the sellers held back goods. Some separation plants also slightly reduced production due to the tightening of raw materials. The production of PrNd oxide in Sichuan decreased 16% MoM, and 14% in Shandong. PrNd oxide output in Guangxi dropped 9% MoM.

PrNd alloy

China's output of PrNd alloy in May 2023 stood at 4,948 mt, down 5% MoM. Output in Jiangxi, Inner Mongolia, Shandong and Sichuan fell to varying degrees, while production in other regions changed little compared with April.

Most of the PrNd alloy factories produced based on sales. In May, the orders of rare earth downstream magnetic material enterprises continued to be poor. Under this circumstance, the purchase volume and inquiries of rare earth metal remained at a low level. The output of PrNd alloy factories thus decreased. Among them, the output in Shandong decreased by 16.7% month-on-month, and the output in Jiangxi decreased by 13% month-on-month; the output in Sichuan and Inner Mongolia fell 7% and 2% respectively.

Dysprosium oxide

Domestic output of dysprosium oxide in May 2023 stood at 188 mt, up 4% month-on-month. Most of the output growth was contributed by Jiangxi.

According to SMM, although Southeast Asia has entered the rainy season, the import volume of ion ores from the region has not been greatly reduced. A large inflow of imported ion ores resulted in an increase in the production of dysprosium oxide. The output of dysprosium oxide in Jiangxi grew 40% compared to April. The output in Guangxi decreased by 33% month-on-month due to equipment problems.

Terbium oxide

Domestic output of terbium oxide in May 2023 stood at 39.5 mt, up 8% MoM. The output in Jiangsu and Jiangxi increased significantly.

According to SMM statistics, from January to April, the amount of rare earth imported from Southeast Asia increased by about 6 times year-on-year. With sufficient supply of terbium oxide and weaker-than-expected downstream demand, its prices failed to rise significantly. With large imports of ion ore, the output of terbium oxide has also increased. The output of terbium oxide in Jiangxi increased by 22% month-on-month, and that in Jiangsu increased by 19% month-on-month.

Molybdenum concentrate

SMM data shows that in May 2023, the domestic molybdenum concentrate output was 17,600 mt, a drop of 3% from the previous month. The decrease in the output of molybdenum concentrate is mainly due to two reasons: 1. With the recent tightening of environmental protection control, the output of some private mines in central China has been restricted for as long as half a month or even longer. 2. As the grade of some molybdenum mines associating with other metals fell, total output declined despite stable mining capacity. Supported by the lucrative profits of molybdenum concentrates, most molybdenum mining companies maintained relatively high operating rates. As a result, the monthly output of molybdenum concentrates did not drop significantly from April.

Entering June, molybdenum mining enterprises in central and north China said that the molybdenum mining and delivery were stable, and they had no maintenance plan; some private mines in the south said that they will undertake maintenance/stop production for a month due to environmental protection renovation plan in June. SMM expects that the output of molybdenum concentrate will be stable in June compared to May.

Ferromolybdenum

SMM data shows that in May 2023, the domestic ferromolybdenum output was 15,000 mt, a growth of 5% from the previous month. In May, the bid volume of ferromolybdenum by mainstream steel mills was about 12,000 mt, an increase of nearly 2,000 mt compared with April. The demand was strong. In addition, the price of molybdenum stopped falling and rebounded, and the profits of ferromolybdenum smelters picked up. Therefore, the enthusiasm for production improved and the smelters arranged production for over a month.

In June, steel mills have no plan to reduce production of molybdenum-containing steel, and the inventory of ferromolybdenum is not at a high level. The spot supply of ferromolybdenum from smelters is also tight. SMM thus expects ferromolybdenum production to increase slightly in June.

Silver

According to SMM survey, domestic #1 silver output in May stood at 1,399.707 mt (including 1,050.707 mt of silver produced with ore), an increase of 4.9% month-on-month and 16.6% year-on-year. The month-on-month increase in output is due to two factors: 1. The silver content in the raw material ores changed. 2.Smelters purchased raw materials as the price of silver fell in the second half of May. Output at some plants fell due to closures for maintenance. Overall, the number of companies whose output increased in May and the output growth both exceeded the number of companies whose output decreased and the output declines. SMM understood that, at the end of May, smelters tended to export silver ingots. At the same time, due to the change in the price difference between spot silver and the most active SHFE silver contract, purchases in the market improved, and spot quotes rose. As silver prices still hovered at high levels in June, SMM predicts that silver production may remain flat in June from May.

Antimony ingot

According to SMM survey, China’s antimony ingot output (including antimony ingot, converted crude antimony, antimony cathode, etc.) in May fell by 2.37% MoM to 7,085.8 mt. Customs data shows that from January to April this year, the import volume of other antimony ores and their concentrates reached 14,923.21 mt, almost double the 7,544.69 mt in the same period last year. Many market players said that the supply of antimony raw material resources may be gradually loosened in the future. With the continuous inflows of imported ore into the market, the supply of domestic ore may also increase significantly. This is also reflected in the recent stable output of antimony products in the market.

In May, many manufacturers increased production, returned to normal production or resumed production. There were also some manufacturers that cut output. Therefore, the output of antimony ingot in May decreased slightly. Among the 33 respondents in SMM survey, 8 manufacturers suspended the production, 5 fewer than the previous month; 16 reduced their production, 7 more than in April; and 9 maintained normal production, 2 fewer than in April. SMM predicts that the domestic antimony ingot output in June is likely to grow as some plants resumed or increased production.

Notes: SMM starts to disclose the output of antimony ingots (including antimony ingots, converted crude antimony, cathode antimony, etc.) since May 2022. Thanks to high coverage of the antimony industry, SMM has successfully investigated a total of 33 antimony ingot manufacturers, which are located in 8 provinces across the country, with a total capacity of nearly 20,000 mt and a total capacity coverage rate of over 99%.

Refined bismuth

According to SMM survey, the output of refined bismuth in China was 2,569.494 mt in May, down 1.95% MoM. The shortage of bismuth raw materials eased slightly. The recovery of primary lead production this year and slightly easing supply crunch of bismuth concentrates ensured raw material supply to refined bismuth producers. Some producers remained closed, while a few resumed production in May. Many producers saw output fluctuations. Downstream demand did not change much. The short-term supply/demand dynamics of domestic refined bismuth market will barely change.

SMM surveyed 24 refined bismuth producers in May, four of whom were closed, compared with five in April; four producers reported higher output; one producer resumed production, and the product it yielded was crude bismuth for the time being; five producers saw their output drop slightly. SMM predicts that the domestic refined bismuth production will probably stabilise in June, but a slight increase is also likely.

Notes SMM has released Chinese refined bismuth output data since October 2022. Thanks to high coverage of the bismuth industry, SMM has successfully investigated a total of 24 refined bismuth manufacturers, who are located in eight provinces across the country, with a total capacity of more than 50,000 mt and a total capacity coverage rate of over 99%.

Silver nitrate

The domestic silver nitrate plants with sales qualification together produced 582 mt of silver nitrate in May, up 5.6% MoM. The total output of silver nitrate nationwide stood at 612 mt, up 4.8% YoY. Silver nitrate plants restocked after silver prices fell in mid-to-late May, but remained cautious about purchasing and producing as silver prices remained high at above 5,000 yuan/kg. Rapidly growing silver powder demand in the domestic photovoltaic industry boosted demand for silver nitrate and silver. If China realises the entire localisation of TOPCON silver powder this year, the demand for silver nitrate will rise further.

Titanium dioxide

SMM data showed that China's titanium dioxide output stood at 300,000 mt in May, down 10.7% MoM and 10.7% YoY. From January to May, the output totalled 1.61 million mt, a drop of 3.2% YoY.

End-use demand shrank sharply in May due to high temperature, weighing down titanium dioxide prices and eroding producers’ profits. Some titanium dioxide producers cut output so as to alleviate their inventory pressure.

According to the current production schedules, China's titanium dioxide output is estimated to drop further to 280,000 mt in June.

Ammonium paratungstate (APT)

According to SMM survey, the domestic APT output stood at 11,500 mt in May, up 3% MoM. In May, the domestic end-use demand was weak, but did not worsen. Smelters maintained stable production to deliver long-term APT orders. Smelters did not cut output in May as they were optimistic about demand.

Tungsten raw material prices rose in early June, but downstream demand failed to keep up, which could put APT smelters at risk of losses. As such, APT output may drop slightly this month.

Lithium carbonate

China’s lithium carbonate output stood at 33,382 mt in May, up 14% MoM and 14% YoY. Despite maintenance by some smelters, growing spodumene supply enabled the total output of spodumene-based battery-grade lithium carbonate smelters to increase. Some lepidolite-based smelters returned to profit-making territory and lepidolite production increased, significantly driving up the output of lepidolite-based lithium carbonate smelters. In addition, salt lake -based smelters saw significant growth in their output, whereas scrap-based smelters reported only mild production growth.

Driven by brisk lithium ore purchases and optimistic market expectations, SMM estimates that China’s lithium carbonate output will climb 11% MoM and 17% YoY to 36,982 mt in June.

Lithium hydroxide

China’ lithium hydroxide output stood at 25,108 mt in May, up 7.4% MoM and 22% YoY. The production of some lithium hydroxide smelters recovered remarkably after being hindered by ore shortages, which more than offset output loss caused by maintenance at others. While rising industrial-grade lithium carbonate prices weakened the cost performance of causticisation process, the increase in outsourcing orders allowed the total output of causticisation-based lithium hydroxide to grow.

Market is betting on recovery of demand for high-nickel ternary materials this month. SMM estimates that China’ lithium hydroxide output will be 26,090 mt in June, up 3.9% MoM and 22% YoY.

Cobalt sulphate

China’s cobalt sulphate output stood at 6,449 mt in metal content in May, up 3% MoM and 39% YoY. The output amounted to 33,799 mt in metal content in the first five months of this year, up 59% YoY.

The prices of cobalt sulphate was at a historically low level in early May, and the overall operating rates of precursor plants picked up, driving non-integrated precursor plants to restock. As cobalt chloride supply tightened due to strong demand, downstream refined cobalt and Co3O4 producers purchased cheaper cobalt sulphate instead as raw materials. Some cobalt salt factories resumed production, but they mainly focused on cobalt chloride products. Shortages of battery scrap inhibited the output increase of cobalt sulphate producers who use scrap as raw materials.

Downstream demand is expected to continue to improve in June. Cobalt salt enterprises are relatively optimistic over market outlook in H2. SMM sees China’s cobalt sulphate output at 6,886 mt in metal content in June, up 7% MoM and 8% YoY.

Tricobalt tetraoxide (Co3O4)

The output of Co3O4 in China stood at 7,046 mt in May, up 13% MoM and 28% YoY. The operating rates of Co3O4 enterprises were around 70-80% in late May. Downstream restocking was monitored after the Labour Day holiday. Demand softened after stocking for upcoming electronics product shopping festival (June 18) passed.

At present, some LCO plants still take outsourcing orders from other producers. LCO plants mostly take a wait-and-see approach amid rising raw material prices. The domestic Co3O4 output is estimated at 7,342 mt in June, up 4% MoM and 31% YoY.

Ternary cathode precursor

China’s ternary cathode precursor output was 61,624 mt in May, up 15% month-on-month and 13% year-on-year. The output amounted to 293,471 mt in January-May, up 0.5% YoY.

Domestic demand gradually recovered, especially from consumer electronics and e-bike sectors. Ternary cathode material producers restocked after a prolonged period of destocking. Top-tier precursor enterprises reported stable production and little increase in exports. One precursor enterprise resumed production. The overall production growth was mainly contributed by low and medium-nickel precursor. Precursor enterprises ramped up production in order to prepare for potential downstream stocking.

Driven by recovering demand and mid-year targets, China’s ternary cathode precursor output is estimated to rise 8% MoM to 66,602 mt in June, albeit down 0.5% YoY.

Ternary cathode materials

The domestic ternary cathode material output was 54,675 mt in May, up 22% MoM and 18% YoY. Overseas demand was stable. In the domestic market, growing automobile production and sales, together with stocking up for electronics shopping festival on June 18, boosted demand for ternary cathode materials. In addition, depleted inventories on hand and rising lithium prices also drove battery cell makers to stock up. Driven by growing demand, ternary cathode material enterprises beefed up production significantly. The 5-series ternary cathode materials saw the most significant output increase amid strong domestic demand, while output of the 6 and 8-series rose only slightly.

Demand from NEV market is expected to rise slightly in June, while demand from the e-bike and digital electronics sectors may stabilise. SMM estimates China’s ternary cathode material output at 58,727 mt in June, up 7% MoM and 11% YoY.

Iron phosphate

China produced 97,857 mt of iron phosphate in May, up 34.3% month-on-month and 119% year-on-year. The monthly output hit a new record high. The cumulative output surged 96% YoY in January-May. The production and sales of iron phosphate both rose in May. Sharply increasing LFP production boosted iron phosphate demand, which drove medium-sized and large iron phosphate producers to beef up production. In terms of cost, the phosphorus chemical market weakened, thereby reducing iron phosphate cost. Despite thin profits and severe overcapacity, medium-sized and large iron phosphate enterprises raised production and locked in orders by leveraging their advantages in technology and sales channels.

The current raw material costs are relatively low. With the ramp-up of new capacity and improving market expectations, iron phosphate production is expected to grow 23.1% MoM and 130.9% YoY to 120,510 mt in June.

LFP

China produced 111,357 mt of LFP in May, up 38% month-on-month and 93% year-on-year. The cumulative output surged 47% YoY in January-May. After destocking in April, LFP production recovered in May with the rebound of lithium carbonate prices. The production growth was mainly contributed by large enterprises. Medium-sized enterprises maintained stable production, while some small enterprises cut production a little. In end-use sectors, NEV market recovered slightly, while energy storage market boomed, driven by PV connection to power grid towards mid-year and widening difference between peak and valley power tariffs.

Optimistic market expectations have incentivised LFP enterprises to raise production schedules this month. SMM predicts that the domestic LFP output will stand at 128,744 mt in June, up 15% MoM and 74% YoY.

LCO

China’s LCO output stood at 6,918 mt in May, up 13% MoM ad 18% YoY. Large LCO enterprises raised production, while the rest reported only slight or little increase in production. Orders from battery cell makers have returned to normal after stocking up for upcoming electronics products shopping festival on June 18 has come to an end.

LCO enterprises currently schedule production based on orders and hold limited finished product inventories. The LCO market is slightly oversupplied. SMM forecasts that the domestic LCO output will be 7,296 mt in June, up 5% MoM and 33% YoY.

LMO

China’s LMO output stood at 13,515 mt in May, up 99% MoM and 285% YoY. Lithium carbonate prices bottomed out in late April and early May, which triggered panic stocking by LMO battery cell factories. Hence, LMO enterprises ramped up production in May. Large LMO enterprises’ new capacity was released, while the rest maintained high operating rates.

Trading activity in LMO market cooled down in early June. However, the long delivery cycle of orders received in early May will enable LMO enterprises to sustain production through June. Considering the release of new capacity, LMO output is expected at 14,206 mt in June, an increase of 5% MoM and 256% YoY.