SHANGHAI, Apr 10 (SMM) -

Copper cathode

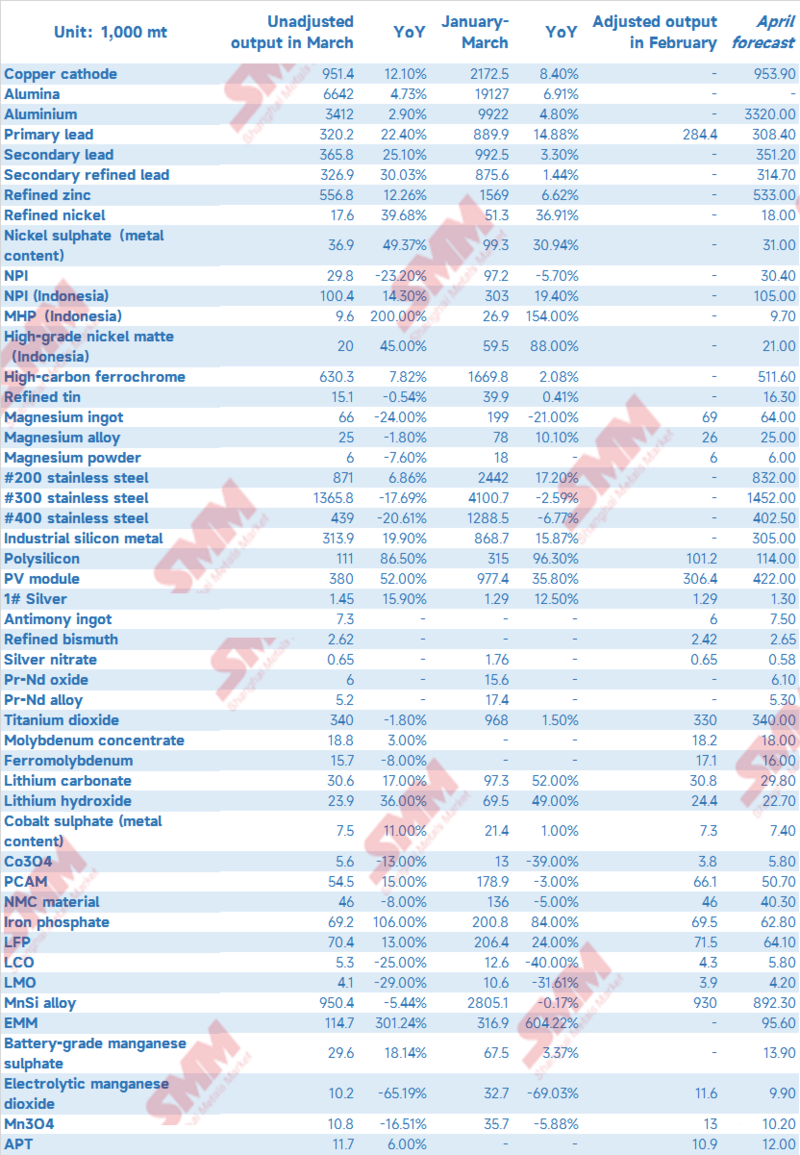

SMM data showed that China' s copper cathode output stood at 951,400 mt in March, up 43,600 mt or 4.8% from the previous month and 12.1% from the same period in 2022. The actual output was 1,900 mt higher than the expected 949,500 mt. The output totalled 2.71 million mt in January-March, an increase of 210,200 mt or 8.4% year on year.

Despite the maintenance of three smelters, the actual output in March did not fall as these smelters have restocked sufficient raw materials. Coupled with the production increase of a smelter in central China, the total output in March increased further. In addition, the sufficient domestic supply of blister copper and anode in China drove up the output of many smelters and the production resumption of a smelter in Jiangxi greatly exceeded expectations. That is why the actual output in March was 19,000 mt higher than the predicted output. The average operating rate of copper cathode industry rose 4 percentage points MoM to 89.62% in March.

According to SMM statistics, six smelters plan to carry out maintenance in April, which will lead to an output cut of 28,600 mt. However, more working days in April are expected to bring about a month-on-month output increase of 23,200 mt. In addition, the rising output of a smelter in central China and the official commissioning of a smelter in Jiangxi that uses hazardous waste as raw materials (with an annual capacity of 100,000 mt) will also lead to additional output increase.

To sum up, China's copper cathode output is estimated at 953,900 mt in April, up 2,500 mt or 0.26% MoM and 15.3% YoY based on the current production schedules. The total output is estimated at 3.67 million mt in January-April, up 10.12% or 336,800 mt year-on-year. However, according to SMM statistics, there will be 7 smelters to be overhauled in May, and thus the output in May is expected to decline.

Aluminium

SMM data shows that China's aluminium output was 3.41 million mt in March (31 days), a year-on-year increase of 2.9%. In March, the daily aluminium output declined 349 mt to 110,000 mt as enterprises in Yunnan still reduced the production and the output increase contributed by the resumption of enterprises in Guizhou and Sichuan was very limited. Aluminium output totalled 9.92 million mt from January to March, up 4.8% year on year. In March, the output of domestic aluminium billet and aluminium alloy increased significantly. According to SMM statistics, the proportion of domestic aluminium liquid increased 8.3 percentage points month-on-month and 8 percentage points year-on-year to around 71% in March.

Domestic aluminium capacity increased slightly as some enterprises in Guizhou, Sichuan and Guangxi resumed production with a total capacity of 220,000 mt, and the capacity transfer in Guizhou and new capacity of Sichuan Guangyuan Zhongfu also contributed to a capacity increase of 140,000 mt. Major capacity cuts stemmed from the production reduction in Shandong. According to SMM statistics, by the beginning of April, installed aluminium capacity reached 45.25 million mt (including the production capacity that has been built but not put into production). The operating capacity was 40.23 million mt, and the national operating rate of aluminium smelters increased 0.8 percentage point to 88.9%.

In April, a total capacity of 370,000-400,000 mt in Guizhou, Guangxi and Sichuan is expected to be resumed or transferred. But the capacity transfer in Shandong may lead to a slight decline in capacity. At present, the aluminium enterprises in Yunnan produce stably as there is no further production reduction requirement. SMM predicts that the domestic aluminium capacity will be restored to more than 40.6 million mt by the end of April and the output will stand at 3.32 million mt in April (30 days), a year-on-year increase of 0.67%.

On the demand side, given the improving downstream demand, domestic aluminium social inventory fell 180,000 mt in March and is expected to decline further to 880,000 mt in April as the domestic supply is limited. However, considering the sharp output increase of aluminium billet and the weak downstream consumption of construction extrusion, it is recommended to pay attention to the changes in the inventory of aluminium billet.

Alumina

Domestic metallurgical-grade alumina output in March (31 calendar days) increased 8.59% on the month and 4.73% on the year to 6.64 million mt with average daily output dipping 4,200 mt to 214,300 mt. The installed capacity and operating capacity of alumina totalled 100.25 million mt and 78.21million mt respectively. The domestic average operating rate stood at 78%. The net imports of alumina is estimated at around 80,000 mt in March, and the alumina surplus will be 158,000 mt.

The average operating rate of alumina refineries in Henan fell to 61.5% in light of poor profits and shortage of ore and that in Shanxi declined to 67.7% for the same reason. The average operating rate in Guizhou rose to 96.5% after the ore supply recovered. In Hebei, the total installed capacity of Wenfeng alumina plant has reached 4.8 million mt, but the operating rate in the region averaged at 66.2% due to the restriction of natural gas. Even with the new capacity, the average operating rates in Guangxi and Shandong fell slightly to 87.1% and 90.1% respectively as the capacity has not been fully put into operation.

Overall, the supply surplus of alumina extended in March, and the overall surplus was 249,000 mt in the first quarter, which weighed on the alumina prices. As alumina plants in Shanxi and Henan are not willing to resume or increase production, the daily alumina output in April is expected to remain at 218,000 mt, and the total alumina output is estimated at 6.54 million mt.

Primary lead

China produced 320,200 mt of primary lead in March, up 12.61% from February and 22.4% on the year. Cumulative output in January-March surged 14.88% from the same period last year. Production capacities of enterprises involved in SMM survey totalled 5.77 million mt in 2023.

According to research, in March, the output of most smelters increased in light of more working days and only a few enterprises in Hunan, Henan, and Yunnan reduced production due to maintenance or raw material shortage. The ramp-up of new capacity in Henan and the production resumption of medium and large enterprises in Henan, Yunnan and Hunan led to a significant output increase. The output in March increased more than 30,000 mt as expected.

Looking forward, more primary lead smelter will conduct maintenance in April. Thus the output will fall in April. Moreover, even with the production resumption of some enterprises in Hunan and Henan, the maintenance of large-scale enterprises in Henan and Yunnan may also cause the output to decline in April. SMM expects China's primary lead output will shed more than 10,000 mt to 308,000 mt in April.

Secondary lead

China produced 365,800 mt of secondary lead in March, up 15.47% from February, and up 25.01% on the year. Cumulative output in January-March surged 3.3% from the same period last year to 992,500 mt. The secondary refined lead output in March increased 16.58% on the month and 30.3% on the year to 326,900 mt. The combined output in the first three months in 2023 advanced 1.44% on the year to 875,600 mt.

The domestic output of secondary refined lead in March increased significantly compared with February as the production of refined lead smelters in February was affected by the Chinese New Year holiday, the maintenance and fewer working days. Anhui Chaowei, Guangxi Zhenyu, Guangdong Xinyu and Xinjiang Renewable Resources resumed production in the middle and late February. Only Guangdong Xinyu stopped production in mid-March due to losses. Most smelters maintained normal production in March, resulting in an increase in monthly output. In addition, the production increase of Anhui Huabo, Anhui Dahua, Tongliao Taiding, Ningxia Chenhong and Hunan Jinyi also brought additional increase to total output.

In April, the maintenance of Anhui Huabo and technical renovation of Jiangxi Xinya may have a great impact on output. But the production resumption of Anhui Tianchang, Shandong Zhongqing and Inner Mongolia Senrun will bring some increases. In April, the overall output of secondary refined lead may decrease 3.73% month-on-month (MoM) to 314,700 mt.

Refined zinc

SMM data showed that the domestic refined zinc output increased 55,300 mt or 11.03% MoM and 12.26% YoY to 556,800 mt in March as expected. The alloy output registered 82,610 mt, up 16,900 mt on the month. The output totalled 1.57 million mt from January to March, up 6.62% year-on-year.

Although the TCs for domestic zinc ore dropped to 5,100 yuan/mt in metal content in March, the high profits still encouraged domestic zinc smelters maintained high operating rates in March. The production cuts in Yunnan caused by power rationing contributed to most of the decline in output. Meanwhile, the Henan Jinli Zinc Smelter successfully reached full capacity in March, bringing additional growth. Maintenance is mainly concentrated in smelters in Yunnan, Liaoning and Inner Mongolia, but the actual output reduction is relatively limited. In terms of secondary zinc, the enterprises in Hunan maintained low operating rates amid poor profits. However, since most secondary zinc enterprises resumed work late in February, their production brought additional output growth in March.

SMM predicts that domestic refined zinc output in April 2023 will decrease 23,800 mt to 533,000 mt, an increase of 7.55% year-on-year; the cumulative output from January to April will reach 2.10 million mt, an increase of 6.86% year-on-year. The routine maintenance of some smelters in Hunan and Shaanxi will lead to major output cut.

Refined tin

Domestic refined tin output was 15,114 mt in March, up 18.15% MoM and down 0.54% YoY, and the combined output from January to March rose 0.41% YoY, according to SMM research.

The actual domestic refined tin output in March was higher than expected in contrast to the extremely low output in February due to the Chinese New Year holiday, the production suspension and fewer working days. Most tin smelters produced stably in March. Only a few smelters reduced production due to the raw material shortage and the low conversion margin. Smelters in Guangxi resumed normal production after maintenance in late March, which will bring significant output increments in April. Two smelters in Yunnan have slightly reduced production due to the shortage of tin ore and lower conversion margin, and some smelters in Jiangxi have slightly increased the production after the supply of tin scrap resumed. Most other smelters will still maintain stable production.

Refined nickel

Chinese refined nickel output totalled 17,600 mt in March, up 1.73% MoM and 39.68% YoY. The output increase was in line with expectations. Some electrowinning nickel companies postponed the production schedules in the month on the shrinking profit margins of producing finished products with MHP or nickel sulphate.

The output in April will be 18,000 mt, up 2.27% MoM and 39.21% YoY. Profits gained by electrowinning nickel producers that produce with MHP have risen somewhat, but a small number of Chinese enterprises still produce electrowinning nickel with scrap to gain a relatively stable profit margin and they intend to increase the production. In addition, a company in north-west China has experienced a decline in pure nickel production due to a technological upgrade.

NPI

Chinese NPI output stood at 29,800 mt in Ni content in March 2023, down 9.1% month-on-month and 23.2% year-on-year. Stainless steel mills cut production intensively in the month, sending NPI prices into a nosedive, which forced the NPI plants to reduce the production. In detail, high-grade NPI output was about 23,500 mt in Ni content, down 9.82% MoM. 300-series stainless steel output fell greatly, and the NPI factories were less willing to ship amid the high nickel ore prices, driving up the NPI stocks held by the NPI factories. Therefore, NPI plants generally cut their output. Low-grade NPI output stood at 6,400 mt in Ni content, down 6.31% MoM. Profits of enterprises with integrated capacity of low-grade NPI and stainless steel were poor, and 200-series stainless steel mills with NPI facilities increased the output in March. Some NPI plants slightly cut the production on equipment failure.

It is estimated the Chinese NPI output in April will increase 0.02% from March to around 30,400 mt in Ni content. Some high-grade NPI plants will still cut their output. The plants’ profit margins will hardly grow sharply in April despite the price decline of nickel ore. Prices of high-grade NPI will also fall following the costs. Most of the NPI factories that cut production due to losses will still carry out output cuts in April. Some that reduced output due to factors such as short-term equipment failures may resume the operation in a certain scale.

Indonesia NPI

Indonesia NPI output stood at 100,400 mt in Ni content in March, down 1.4% month-on-month and up 24.5% year-on-year. Output from January to March totalled 303,000 mt in Ni content, up 19.4% year-on-year. The overall Indonesia NPI output rose despite the poor demand from stainless steel sector and the reduced construction of power equipment in some factories. The high-grade NPI prices plunged into a free fall in March, once approaching the break-even points of Indonesia NPI plants and weighing greatly on NPI factories. With the drop in nickel prices in April, the nickel ore prices in China fell as well, slightly pushing up the profit margins of NPI plants. In April, Chinese 300-series stainless steel output will only increase slightly from the previous month. Accordingly, the Indonesia NPI output is expected to grow about 4.8% MoM to 105,000 mt in Ni content, an increase of 11.8% year-on-year.

Nickel sulphate

Chinese nickel sulphate output stood at 167,800 mt in physical content or 36,900 mt in metal content, up 18.30% on the month and 49.37% on the year. Driven by the demand for nickel sulphate from electrowinning nickel companies, Chinese ternary precursor companies were worried about its future supply and made frequent inquiries. The booming demand boosted the nickel sulphate output, and nickel salt plants accelerated production. Some nickel sulphate enterprises that have signed long-term orders sped up production in the month amid the surging nickel sulphate prices. In April, the supply surplus of nickel sulphate can hardly ease in the short term since the demand from the ternary precursor companies is expected to fall. SMM believes that the nickel sulphate output will lose 15.93% MoM in April to 31,000 mt in metal content.

Battery-grade manganese sulphate

China produced 29,600 mt of high-purity manganese sulphate in March, up 23.85% MoM. On the supply side, according to SMM survey, high-purity manganese sulphate companies generally ran at high capacities to reduce costs as the ternary precursor companies undercut discounts of long-term contracts. The power battery demand remained poor, and the high-purity manganese sulphate consumption by the ternary precursor companies was sluggish accordingly. The high-purity manganese sulphate market was in a severe supply surplus.

In April, considering the high inventory of high-purity manganese sulphate and the poor demand from the power battery sector, most high-purity manganese sulphate enterprises will maintain low operating rates, and some even suspended their production. The output in April is expected to be around 13,900 mt in physical content, down 53.04% MoM.

Electrolytic manganese dioxide

SMM data showed that the Chinese electrolytic manganese dioxide (EMD) output was 10,200 mt (including 200 mt for LMO battery, 6,300 mt for alkaline manganese battery, and 3,800 mt for zinc-carbon battery) in March, down 12.07% MoM and 65.19% YoY. EMD output in the first three months of 2023 stood at about 32,700 mt, down 69.03% YoY. This was because the demand from the LMO battery sector remained poor, and prices of trimanganese tetraoxide (Mn3O4) stood lower than the EMD. In addition, the primary battery demand also weakened, reducing the output of EMD for alkaline manganese battery and zinc-carbon battery.

It is expected that in April, the downstream demand will hardly improve, hence the output may decrease further to about 9,900 mt.

Mn3O4

SMM data showed that in March 2023, Chinese Mn3O4 output was 10,800 mt (including 7,600 mt of electronics-grade Mn3O4 and 3,200 mt of battery-grade Mn3O4), down 16.83% MoM and 16.51% YoY. Output in the first three months of the year stood at about 35,700 mt, down 5.88% YoY. LMO battery companies reduced the production on the sharp fall in lithium carbonate prices, hence the manganese salt demand also decreased sharply, which further dragged down the production of Mn3O4 producers.

In April, the downstream demand may remain poor, thus orders received by Mn3O4 enterprises will be slack. The output may fall slightly to 10,200 mt as the companies will not restock raw materials.

High-carbon ferrochrome

Chinese high-carbon ferrochrome output stood at 630,300 mt in March, up 84,800 mt or 15.55% from the previous month and 45,700 mt or 7.82% on the year. The output in Inner Mongolia was 349,400 mt, up 31,000 mt or 9.74% MoM, and that in Guizhou stood at 57,500 mt, up 70.12% MoM. Ferrochrome prices were supported by the high chrome ore prices despite the poor consumption by the stainless steel sector in March. Bid prices of high-carbon ferrochrome at the leading stainless steel mills rose further. The profits of ferrochrome manufacturers increased somewhat in the month, greatly pushing up the output. Moreover, imported ferrochrome also flew into the market. However, the consumption did not improve as fast as expected, resulting in a severe supply surplus of ferrochrome.

The output of high-carbon ferrochrome in April is expected to fall to 511,600 mt. Stainless steel mills plan to cut their production on high social stocks, thus the demand for ferrochrome may decrease. The costs can hardly prop up ferrochrome prices since the plants are running at high capacities. Bid price of ferrochrome in mainstream stainless steel mills will decline sharply in April. Ferrochrome manufacturers in the south suspend their production intensively on huge loss, but the ones in the north maintain normal production with order support. Ferrochrome supply can barely be tight with poor demand and the accumulated inventory in the previous period.

Stainless steel

According to SMM survey, Chinese stainless steel output totalled 2.68 million mt in March, down 5.41% MoM and 11.62% YoY. The output of 200-series stainless steel fell 3.65% MoM to 871,000 mt, 300-series dropped 7.35% MoM to 1.37 million mt, and 400-series declined 2.55% MoM to 439,000 mt.

In March, the high stainless steel social inventory was consumed slowly. Spot prices ran with some declines, gradually suppressing the prices of raw materials. Many stainless steel mills cut production on low profit margins.

In April, the stainless steel output may rise slightly. Production of 200-series and 400-series will be at huge losses, and the in-plant and social inventory will both fall slowly. SMM believes that 200-series and 400-series output will decrease in April. In early April, 300-series stainless steel profits have improved somewhat. Orders received by the state-owned stainless steel mills were acceptable. Some mills even ramped up the production. Therefore, the overall output of 300-series stainless steel in April will grow. In addition to the slack domestic and foreign demand, the weakening cost support is an important reason for the drop in stainless steel prices. It is necessary to pay attention to the inventory consumption amid the declining spot supply and the bottom of raw material prices.

EMM

Chinese EMM output stood at 114,700 mt in March, up 14.33% on the month and 301.24% on the year, SMM data showed. EMM output in the first three months of 2023 stood at around 316,900 mt, up 604.22% year-on-year. To explain the surge in output, there are more working days in March on the one hand. On the other hand, EMM plants were less willing to cut output on high profit margins even though the downstream demand was poor.

Entering April, although the stainless steel mills have ramped up the production, the shipments of EMM plants still bore pressure. Besides, the EMM supply stood high, resulting in a fall in EMM prices. EMM plants will likely cut output by 10% in April and may halve the operating rates, though the specific production plans of each enterprise have not yet been determined. SMM believes that the EMM output will be about 95,600 mt.

Industrial silicon metal

SMM data shows that China's industrial silicon metal output was 313,900 mt in March, an increase of 32,900 mt or 11.7% month on month and 19.9% year on year. From January to March 2023, the cumulative industrial silicon metal output was 868,700 mt, an increase of 15.9% year on year

The noticeable growth in industrial silicon production in March was due to more production days than in February. The production capacity in Xinjiang and Inner Mongolia was the major contributor to the output increase. According to SMM data, the month-on-month increase in Xinjiang was nearly 30,000 mt, and that in Inner Mongolia was 5,000 mt. The resumption of a small amount of production capacity in Hunan in March also contributed to the increase in output. In March, the spot prices of industrial silicon fell at an accelerated pace, and the cost pressure on silicon metal enterprises increased sharply. An increasing number of plants in Sichuan and Yunnan incurred losses and thus cut output in March by some 9,000 mt.

On April 7, the low-end price of above-standard #553 silicon metal in east China was 15,600 yuan/mt. This price level pushed most of the silicon companies in south China into losses. Some producers in the north also ran at losses to varying degrees. Combined with sluggish demand and the lack of market bullishness over silicon metal prices, silicon metal enterprises are expected to further reduce production in April. The enterprises in Shaanxi and Qinghai also reported significant cost pressure and a possibility of output cuts. It is estimated that industrial silicon production in April will decrease to around 305,000 mt.

Polysilicon

According to SMM statistics, the domestic polysilicon supply in March was about 110,000 mt, a significant increase of 8.7% from February, returning to the positive territory after a slide in February.

The main reasons driving up domestic polysilicon supply in March include the ramp-up of new production capacity at Runyang and GCL. The increase in the number of production days in March also led to an increase in the supply of polysilicon. In addition, the completion of maintenance of large factories in Xinjiang and Inner Mongolia also contributed to a certain increase in the operating rates of polysilicon producers in March. At present, although the prices of polysilicon continue to fall, the product is still relatively lucrative given the low industry cost of 50-60 yuan/kg, prompting enterprises to maintain high enthusiasm for production.

PV module

According to SMM statistics, domestic PV module output in March was about 38 W, up 24.02% from February. In March, a number of terminal projects were delivered, and several representative terminal projects will be commenced in April, causing module companies to stock up on cargoes actively. This, combined with the recovery of overseas demand, significantly lifting the output of PV module.

SiMn alloy

China produced 950,400 mt of silico-manganese alloy in March, up 2.19% MoM but down 5.44% YoY, according to SMM statistics. From January to March 2023, the silico-manganese alloy output in China was 2.81 million mt, a drop of 0.17% year-on-year. The main reason for the increase is that large factories in the north and south resumed or increased production slightly. This offset the output cuts and suspension at plants in Guangxi in the second half of March.

In April, the electricity fees in Guangxi were raised, and the pressure on existing enterprises has thus increased. The cost in Ningxia is relatively high, and some enterprises are expected to shut down for maintenance. Therefore, the output is expected to decrease to about 892,300 mt.

Magnesium ingot

China's magnesium alloy output stood at 66,000 mt in March, down 3.8% MoM and down 24% YoY, according to SMM statistics. The output totalled 199,000 mt in January-March 2023, a year-on-year decrease of 21%.

Due to weak demand in the downstream market, domestic magnesium prices continued to drop in March, and the profits of primary magnesium factories were severely eroded. The industry's enthusiasm for production thus continued to decline, and some magnesium factories were forced to reduce production due to losses. According to the current production schedule of factories in the main production areas, some magnesium plants still plan to reduce production in April. Considering that the prices of magnesium have rebounded slightly in April, the wait-and-see mood in the market has eased. It is expected that the output of magnesium ingots will remain low in April at around 64,000 mt.

Magnesium alloy

According to SMM data, China's magnesium alloy output stood at 25,000 mt in March, down 2.0% month on month and 1.8% on the year. The output totalled 78,000 mt from January to March, a year-on-year increase of 10.1%.

According to domestic magnesium alloy enterprises, the downstream demand for magnesium alloys continues to be sluggish at present, and the orders for magnesium alloys are weaker than the same period last year. Due to the continuous decline in the prices of primary magnesium, the production of primary magnesium at magnesium alloy enterprises has fallen further. It is expected that the domestic production of magnesium alloys will remain at a low level of 25,000 mt in April.

Magnesium powder

China's magnesium powder output stood at 6,000 mt in March, down 7.6% MoM. YTD output through March totalled 18,000 mt.

In March, the operating rates of the domestic magnesium powder industry continued to decline, and magnesium powder companies generally held a pessimistic attitude towards the market. The person in charge of a large magnesium powder company said that due to the high price of magnesium in the past two years, the domestic terminal demand for magnesium powder applications has shrunk severely. The high price of magnesium powder has increased the competitiveness of alternative products, and the magnesium powder market is likely to shrink across the board. It is expected that the total output of magnesium powder will remain low in April at about 6,000 mt.

PrNd oxide

Domestic output of PrNd oxide in March 2023 stood at 6,011 mt, up 4% MoM. Output increased across Shandong and Jiangsu to varying degrees. Output in Jiangxi fell slightly.

According to SMM survey, due to the large increase in imported rare earth ores and the demand for rare earths having not recovered, the overall price trend of rare earths was under pressure. In the first quarter, the prices of PrNd oxide showed a downward trend as a whole. With stubbornly poor demand, some plants began to reduce production, and their purchasing enthusiasm also declined. Losses at scrap recycling companies remain, and their operating conditions can hardly improve in the short term. However, due to the production plans to be fulfilled and the further recovery of production situation, some separation plants reported a large increase in output. In March, the output of PrNd oxide in Jiangsu increased by 39% month-on-month, and that in Shandong increased by 17% month-on-month.

PrNd alloy

Domestic output of PrNd alloy in March 2023 stood at 5,180 mt, down 1.2% MoM. Sichuan and Guangxi cut output slightly. Output in other regions changed little compared with February.

In March, the prices of PrNd alloy remained on the downswing. In the first quarter, the orders of downstream magnetic material enterprises remained slack. Most of them lowered raw material inventories on purpose, dampening demand for PrNd alloy. Due to the continuous decline in PrNd oxide prices, some PrNd alloy factories that purchased PrNd oxide began to curtail production. The output of PrNd alloy in Guangxi decreased by 13% month-on-month, and that in Sichuan decreased by 8% month-on-month. Manufacturers who used PrNd oxides separated by themselves were less affected by the drop in market prices, and their output has not yet been significantly reduced.

Molybdenum concentrate

SMM data shows that in March 2023, China's molybdenum concentrate output was 18,800 mt, an increase of 3% from the previous month.

Entering March, high sales profits of molybdenum concentrates incentivised mining companies to maintain high operating rates. More working days in March also accounted for higher output, in line with market expectations.

In April, due to the current good profit and further increase in terminal demand, there are few mining companies with maintenance plans. SMM predicts that the output of molybdenum concentrate in April is more likely to be stable.

Ferromolybdenum

SMM data shows that in March 2023, China's ferromolybdenum output was 15,700 mt, a decline of 8% from the previous month.

In March, affected by the high prices of domestic molybdenum, the purchases by steel mills for ferromolybdenum dropped sharply in the first half of the month, limiting new orders of ferromolybdenum smelters. This drove them to lower operating rates to reduce output. In addition, weakened support from demand caused prices of molybdenum to drop rapidly. Some ferromolybdenum smelters that were still working through the molybdenum raw materials purchased previously at a high level suffered losses, dampening their production enthusiasm.

Entering April, due to the further release of terminal demand and the big drop in raw material prices, the profits of ferromolybdenum smelters are gradually recovering. SMM expects that the actual output of ferromolybdenum in April will increase slightly.

Silver

According to SMM survey, domestic #1 silver output stood at 1,454.894 mt (including 1,054.394 mt produced with ore), a jump of 12.5% month-on-month and 15.9% year-on-year. The large increase in output in March is because: 1. The prices of silver in mid-March were low, and enterprises purchased raw materials aggressively. 2. There were more days of normal production in March compared with February; 3. Production plans of silver increased. 4. The overhaul ended. Generally speaking, the number of manufacturers whose output increased were greater than the number of manufacturers whose output declined, and the amount of increase also surpassed the decline, sending silver output to surge. As the prices of raw materials rose with silver prices, SMM predicts that silver production may be slightly lower in April.

On the macro side, ADP said private-sector employment in the United States rose by around 145,000 in March, lower than the previous value of 242,000 and the expected value of 200,000; the EIA crude oil inventory in the US for the week ending March 31 was -3.739 million barrels, higher than the previous value of -7.489 million barrels, and lower than the expected value of -2.320 million barrels; the number of initial jobless claims in the US for the week ending April 1 was 228,000, higher than the previous value of 198,000 and the expected value of 200,000. A string of positive economic data in the US has continuously pushed up silver prices.

Antimony ingot

According to SMM survey, China antimony ingot (including antimony ingot, converted crude antimony, antimony cathode, etc.) output in March 2023 was 7,256 mt, up 20.07% from February. The shortage of antimony raw material resources continues, forcing many manufacturers to cut or suspend production in March. However,many manufacturers have also begun to increase or resume production since March. In detail, the output of four manufacturers increased significantly, and two manufacturers resumed production. Therefore, there will still be a strong support for the future antimony supply.

The number of producers that cut or suspended production changed in March. Among the 33 respondents in SMM survey, 13 manufacturers suspended the production, two fewer than the previous month; 14 reduced their production, unchanged from February; and six maintained normal production, two more than in February. SMM predicts that the supply-demand structure of the domestic antimony market in April 2023 is likely to change slightly. China’s antimony ingot output in April is anticipated to grow from March.

Refined bismuth

According to SMM survey, the output of refined bismuth in China was 2,621 mt in March, up 8.38% MoM, but the growth rate slowed down. Due to persistent raw material shortages, no refined bismuth producer resumed production last month. However, some producers ramped up production, driving up the total output. The future supply-demand dynamics of domestic refined bismuth market will not change much.

Among the 24 refined bismuth producers surveyed by SMM, three of them reported a significant increase in their output in March on a monthly basis, while another one saw a sharp decline in its output. One more producer was shut down last month. It is expected that refined bismuth prices will still have upside room in April. In view of raw material shortfalls, SMM predicts that the domestic refined bismuth production will probably stabilise in April, but a slight increase is also likely.

Notes: SMM has released Chinese refined bismuth output data since October 2022. Thanks to high coverage of the bismuth industry, SMM has successfully investigated a total of 24 refined bismuth manufacturers, who are located in eight provinces across the country, with a total capacity of more than 50,000 mt and a total capacity coverage rate of over 99%.

Silver nitrate

The domestic silver nitrate plants with sales qualification together produced 614 mt of silver nitrate in March, unchanged from February. The total output of silver nitrate nationwide stood at 646 mt. Some producers undertook maintenance or cut their output due to rising silver prices in late March, while others ramped up production on the back of backlog orders or recovered from maintenance, leaving the overall output little changed. However, silver prices have been rising since mid-March, and the prices of silver (T+D) on the Shanghai Gold Exchange approached 5,600 yuan/kg as of April 7. Soaring silver prices cooled downstream enthusiasm for placing orders. Considering the differences in orders and production schedules, the impact of rising silver prices on each silver nitrate producers’ output varies. All in all, SMM expects silver nitrate output to decrease in April.

Titanium dioxide

SMM data shows that China's titanium dioxide output stood at 340,000 mt in March, up 4.1% MoM, but down 1.8% YoY. From January to March, the output totalled 968,000 mt, a drop of 1.5% YoY.

The domestic titanium dioxide market extended its boom into March, with transaction prices going up steadily, encouraging titanium dioxide enterprises to maintain high operating rates. Entering April, new orders have slowed down. Titanium dioxide enterprises are now delivering orders received previously. SMM estimates that the domestic titanium dioxide output will stabilise at around 340,000 mt in April.

APT

According to SMM statistics, the domestic APT output stood at 11,700 mt in March, up 6% on the month.

In March, limited new orders from domestic and overseas customers caused spot tungsten prices to drop. The delivery of long-term orders allowed APT smelters’ output to recover in March.

In early April, tungsten prices inched lower. With thin profits and expectations for demand recovery, APT output may stabilise in April.

Lithium carbonate

China’s lithium carbonate output stood at 30,585 mt in March, down 1% MoM, but up 17% YoY. On the one hand, the output of salt lake-based smelters picked up after the weather warmed up, and some spodumene-based smelters recovered from maintenance. On the other hand, lepidolite-based smelters slashed their production noticeably and battery recycling market was quiet, resulting in a decline in total lithium carbonate output. In April, China’s lithium carbonate output is estimated to drop 3% MoM to 29,756 mt, albeit up 12% YoY. In response to disappointing downstream demand and potential losses arising from continuously plunging lithium carbonate prices, some spodumene and lepidolite-based smelters are likely to cut their output.

Lithium hydroxide

China’s lithium hydroxide output was 23,891 mt in March, down 2% MoM, but up 36% YoY. From the perspective of causticisation, causticisation plants were keen on purchasing lithium carbonate to produce lithium hydroxide due to the big price difference between the two and strong demand. From the perspective of smelting, some large smelters reduced their production further due to lithium ore shortages, while other types of smelters also lowered their output amid pessimistic demand outlook. Sharply falling downstream demand has driven both smelters and causticisation plants to cut their production. As such, SMM estimates that the domestic lithium hydroxide output will decline 5% MoM to 22,712 mt in April, despite a year-on-year rise of 23%.

Cobalt sulphate

China’s cobalt sulphate output stood at 7,472 mt in cobalt content in March, up 5% MoM and 11% YoY. In early March, some cobalt sulphate smelters were running at full capacity as aggressive stocking by traders in February boosted their confidence over future demand. From the demand side, the production schedules of ternary precursor plants were stable. However, the market situation took an abrupt downturn in late March. Precursor plants trimmed or ceased their production while focusing on destocking, thus trades in the cobalt sulphate market almost stagnated. In March, the digital electronics market outperformed than the NEV market. With no signs of recovery in end-user market, cobalt sulphate demand will weaken further. SMM predicts that China’s cobalt sulphate output will slide 1% MoM to 7,408 mt in cobalt content in April, though up 1% YoY.

Tricobalt tetraoxide (Co3O4)

The output of Co3O4 in China stood at 5,607 mt in March, up 47% MoM, but down 13% YoY. Despite higher output, the operating rates of some producers were still below 50%. A top-tier producer was not running at full capacity in March, and its output in April is expected to be flat from March. On the demand side, most LCO producers adopted a wait-and-see approach. Sluggish digital electronics market and steadily falling lithium carbonate prices discouraged LCO producers from buying Co3O4. The Co3O4 market will hardly improve this month. The domestic Co3O4 output is estimated at 5,781 mt in April, up 3% MoM, but down 19% YoY.

Ternary cathode precursor

China’s ternary cathode precursor output was 54,536 mt in March, down 17% month-on-month and 15% year-on-year. Demand from digital electronics and e-bike sectors was relatively stable. With NEV market showing no signs of recovery and raw material prices in a downward cycle, downstream players in the industry chain tried to clear their inventories, hurting the demand for precursors. Precursor plants maintained low operating rates in response to slack demand and some were even shut down, with no plans to re-open in April. The overseas ternary cathode precursor market is also showing a downward trend. China’s ternary cathode precursor output is estimated at 50,699 mt in April, down 7% month-on-month and 4% year-on-year.

Ternary cathode materials

The domestic ternary cathode material output was 46,042 mt in March, flat month-on-month, but down 8% year-on-year. Some ternary cathode material producers received more orders, driven by rigid demand from the electronics and e-bike sectors. However, market players across the entire industry chain were plagued by high inventories caused by cooling NEV market. Coupled with rapidly falling raw material prices, purchasing activity declined. Orders from overseas power battery market have shown signs of weakening. With the overall demand softening, the operating rates in ternary cathode material industry stopped growing. Entering April, downstream demand continued to decline and pessimistic sentiment is prevailing. Therefore, the domestic ternary cathode material output is estimated to fall 12% MoM to 40,310 mt in April, despite a year-on-year increase of 12%.

Iron phosphate

China produced 69,184 mt of iron phosphate in March, down 0.4% month-on-month, but up 106% year-on-year. The output surged 84% YoY in the first quarter. LFP plants slowed down order pick-up significantly in the second half of March, and some even cancelled their orders. As the operating rates of LFP enterprises kept falling, new orders for iron phosphate shrank, causing iron phosphate producers’ inventories to build up. On the cost side, the prices of phosphoric acid, the main raw material of iron phosphate, continued to fall in March. Under the dual effects of faltering demand and falling costs, iron phosphate prices dropped. With LFP enterprises lowering their production schedules further in April, iron phosphate production will decline accordingly. SMM predicts that the domestic iron phosphate output will stand at 62,755 mt in April, down 9% MoM, but up 78% YoY.

LFP

China produced 70,377 mt of LFP in March, down 1.5% month-on-month, but up 13% year-on-year. The output jumped 24% YoY in the first quarter. Orders from power battery market barely improved. What’s worse, customers from energy storage sector delayed placing orders as LFP prices extended declines. In the second half of March, some buyers either cancelled orders or delayed order pick-up. Following aggressive price cuts by gasoline car manufacturers in early March, the impact had spilled over into the NEV market in the second half of the month. With growing wait-and-see sentiment among consumers, the finished product inventory of LFP plants accumulated, sending its prices down steadily. Falling lithium carbonate and iron phosphate prices brought down the costs of LFP plants. Entering April, LFP plants lowered their production schedules further amid the poor performance of NEV market. SMM predicts that the domestic LFP output will stand at 64,081 mt in April, down 8% MoM, but up 20% YoY.

LCO

China’s LCO output stood at 5,255 mt in March, up 20% MoM, but down 25% YoY. On the supply side, the output of top-tier LCO plants increased in March, but was significantly below that in the same period last year due to poor demand from the digital electronics market. On the demand side, orders from battery cell makers improved only mildly as the electronics market remained sluggish. In terms of input costs, lithium carbonate prices slumped, while CO3O4 prices dropped slightly. Slack demand and lower costs weighed on LCO prices. With the electronics market still lacklustre, LCO production is unlikely to grow significantly this month. SMM forecasts that the domestic LCO output will stand at 5,776 mt in April, up 10% MoM and 2% YoY.

LMO

China’s LMO output stood at 4,103 mt in March, up 7% MoM, but down 29% YoY. With lithium carbonate prices in a downward path, LMO plants restocked in small quantities as needed. Orders from electronics sector were limited, even though this sector outperformed the e-bike market. A large number of small and medium-sized LMO enterprises were shut down due to losses. The overall operating rates of the LMO industry were still at a low level. Entering April, bearish outlook for lithium carbonate prices kept LMO plants restocking as needed. SMM predicts that the domestic LMO output will stand at 4,206 mt in April, up 3% MoM and 29% YoY.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)