SHANGHAI, Feb 9 (SMM) -

Copper cathode

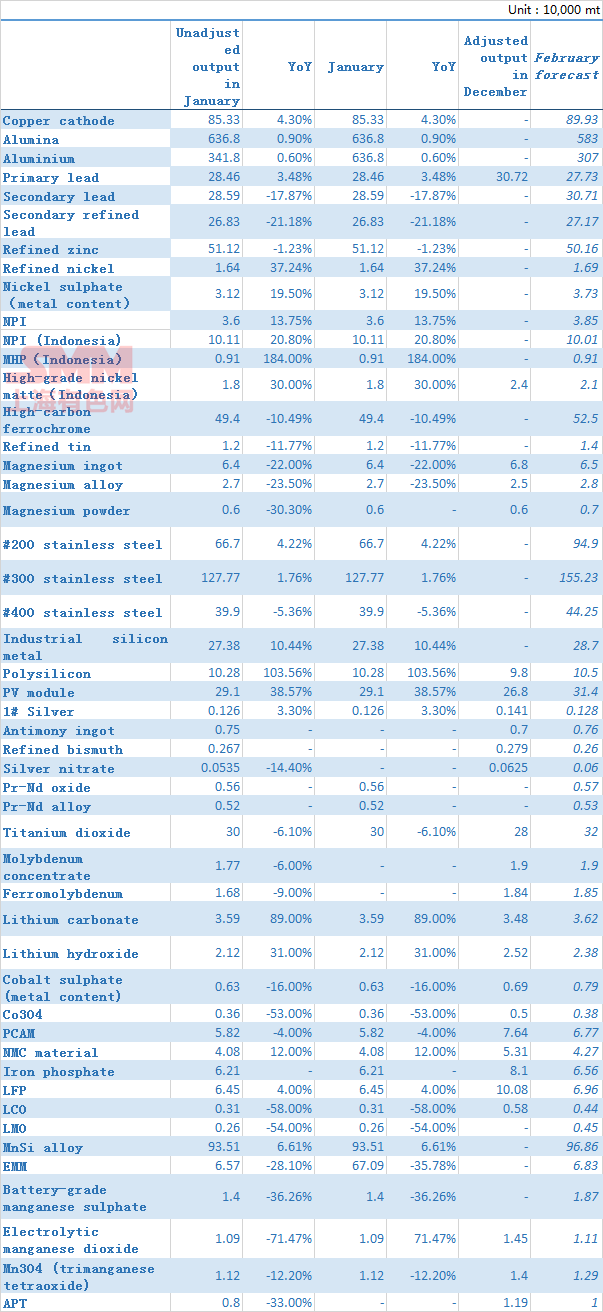

SMM data showed that China’s copper cathode output stood at 853,300 mt in January, down 1.9% from the previous month but up 4.3% from the same period in 2022. The actual output was 41,700 mt lower than the expected 895,000 mt.

The reasons for MoM output drop are as follows: 1. The impact of maintenance carried out by a smelter in east China was greater than expected. 2. The production expansion of new smelters in central and south China was slower than expected. 3. The operating rates declined compared with December 2022 due to the Chinese New Year (CNY) holiday. In addition, the special statistical cycle underestimated the actual output of several smelters.

In February, the two smelters that were overhauled before will resume normal production. SMM estimates that they will contribute an output increase of more than 30,000 mt. As most smelters have resumed normal production after the Chinese New Year holiday, the output in February will increase obviously. However, the less production days in February, the slow release of new capacity and tight raw material supply still affect the output.

To sum up, SMM expects that China’s copper cathode output will stand at 899,300 mt in February, up 46,000 mt or 5.39% month-on-month (MoM) and 7.6% year-on-year (YoY) based on the current production schedules. The output is estimated at 1. 75 million mt in January and February, up 5.97% or 98,800 mt year-on-year.

Aluminium

Domestic aluminium output in January (31 calendar days) declined 0.6% month-on-month but increased 6.7% year-on-year to 3.42 million mt, with the daily output declining 642 mt to 110,300 mt. In light of power shortage in Guizhou province from December 2022 to January 2023, the operating aluminium capacity in January 2023 was 760,000 mt lower than that at the end of November, and 310,000 mt lower than that at the end of December after three round of power curtailment. At the same time, a total of 50,000 mt of capacity was resumed in Sichuan and Guangxi province and 120,000 mt was newly put into production by Gansu Zhongrui, Guizhou Yuanhao and Mongolia Baiyinhua. According to SMM statistics, by the beginning of February, domestic installed aluminium capacity reached 45.26 million mt (including the production capacity that has been installed but has not been put into production). The domestic operating aluminium capacity was 40.3 million mt, and the national operating rate averaged about 89%. In January, the proportion of aluminium liquid fell 7.2 percentage points month-on-month to 59.2% amid seasonal low and Chinese New Year holiday.

Entering February, operating aluminium capacity may decline slightly to 40.1 million mt due to expectations of a 10-20% production cut in Yunnan and the slow production resumption in Guizhou as the hydropower shortage in south-west China extends. The output in February (28 calendar days) is expected to increase 4.1% year-on-year to around 3.07 million mt.

Alumina

China’s metallurgical-grade alumina output in January (31 calendar days) was 6.37 million mt, down 0.9% MoM but up 1.4% YoY, according to SMM statistics. The average daily output decreased 2,000 mt to 205,000 mt. As of the end of January, the domestic installed alumina capacity stood at 97.75 million mt while the operating capacity was 74.94 million mt, implying an average domestic operating rate of 77%. On the whole, it is estimated that the net imports of alumina in January will be 115,000 mt. And there existed a slight shortage of 97,000 mt in the month.

The output in Guizhou, Henan and Chongqing declined on the month, that in Hebei increased and that in Shanxi, Guangxi, Inner Mongolia and Yunnan remained stable. The high cost, poor transportation efficiency and short ore supply in Henan led to a sharp decline in operating rates, with output dipping 25,000 mt month-on-month and 242,000 mt year-on-year. The monthly output in Guizhou decreased 27,000 mt as some alumina refineries were shut down in December 2022 and January 2023 amid local power cuts. These alumina refineries have resumed the production in early February and the output in Guizhou is expected to pick up in March. In Chongqing, the output decreased 10,000 mt month-on-month as the production was affected by the tight natural gas supply. In Hebei, the output climbed 20,000 mt month-on-month after the third alumina production line (1.2 million mt) of Hebei Wenfeng was put into production at the end of January. It is expected that the output in Hebei will increase further in February.

On the whole, domestic alumina market maintained a tight balance in January. In light of the resumption plans in Guizhou and Shanxi and 1.2 million mt new capacity of Heibei Wenfeng, the total domestic output of metallurgical-grade alumina in February (28 days) is estimated at 5.83 million mt, with daily output increasing to 210,000 mt.

Primary lead

SMM data showed that China produced 284,600 mt of primary lead in January, down 7.36% month-on-month but up 3.48% year-on-year. Production capacities of enterprises involved in the survey totalled 5.76 million mt in 2023.

Most refined lead smelters maintained normal production during the Chinese New Year holiday and only a few smelters took holidays for 1-2 weeks. The expected decline in output was mainly caused by the maintenance carried out by Zhongjin Lingnan, Yunnan Zhenxing, Yunnan Mengzi and Hunan Shuikoushan. However, the new capacity of large-sized smelters in Henan, which started commissioning at the end of 2022 and ramped up the production in early 2023, contributed to the year-on-year output increase in January.

Entering February, refined lead smelters that took holidays or undertook maintenance during Chinese New Year holiday, such as Zhongjin Lingnan, Yunnan Zhenxing and Hunan Shuikoushan, have resumed the production. Coupled with the new production lines of large-sized smelters in Henan, the output in February is expected to increase. Besides, the output of most producers will decrease simultaneously due to less production days in February, hence SMM expects the national refined lead output will fall more than 10,000 mt to 277,000 mt in February.

Secondary lead

China produced 285,900 mt of secondary lead in January, down 22.29% MoM and 17.87% YoY. Output of secondary refined lead was 268,300 mt, down 21.18% MoM and 19.36% YoY.

Both secondary lead and secondary refined lead output in January saw a significant decline due to maintenance and production reduction caused by tight battery scrap supply amid the Chinese New Year holiday. For example, Zhejiang Tianneng carried out maintenance in December 2022 and resumed work after the CNY holiday while Anhui Chaowei, Anhui Huaxin, Tongliao Taiding, Shuangdeng Tianpeng, Jiangxi Fengri, Guangxi Zhenyu and Shandong Zhongqing took holidays for Chinese New Year. At the same time, Anhui Huabo, Dahua and other secondary lead smelters slightly reduced their output.

Entering February, secondary lead smelters have gradually resumed work after the CNY holiday, which will bring an increase in domestic secondary lead output in February. And the recycling amount of battery scrap has further recovered after the Lantern Festival, which supports the resumption of secondary lead smelters. The profits of retail transactions are poor under the current low lead prices, but the profits of long-term orders are able to stand at 200-400 yuan/mt based on the monthly average price of SMM #1 lead ingot. Therefore, secondary lead smelters that mainly ship in the form of long-term orders are still active in production.

Refined zinc

China's refined zinc output stood at 511,200 mt in January, down 14,600 mt or 2.77% MoM and 6,400 mt or 1.23% YoY. The actual output was slightly higher than the expected 504,600 mt.

Most large and medium-sized zinc smelters in China produced at or above full capacity in January in light of high profits while some secondary zinc smelters in Sichuan and Hunan, Yunnan and Inner Mongolia undertook maintenance. The output increase was mainly brought by the resumption of production of smelters in Qinghai, Gansu and Inner Mongolia.

The refined zinc output in February is expected at 501,600 mt, down 9,600 mt on the month and up 9.43% or 44,200 mt YoY. The less production days in February may lead to an output reduction of 34,800 mt. But the operating rates are expected to increase further as most smelters maintain stable production and only some smelters in Hunan carry out maintenance.

In terms of new capacity, the daily output of Henan Jinli currently exceeds 300 mt, and its operating capacity is approaching the designed level. The daily output of Jiangxi Siyuan is low during trial production.

Refined tin

Domestic refined tin output in January was 11,990 mt, down 24.61% MoM and 11.77% YoY, according to SMM research. The actual output was slightly lower than expected.

The year-on-year decrease was caused by the earlier CNY holiday while the month-on-month decrease caused by the obvious decline in operating rates amid the CNY holiday. 1. In Yunnan, the output decreased significantly month-on-month as expected due to the CNY holiday. 2. The impact of CNY holiday on the output in Guangxi was insignificant, but the tight raw material supply aroused expectations of sharp output cut in February. 3. The output in Jiangxi declined slightly as mainstream smelters maintained normal production during the CNY holiday. The output in February is expected to remain stable. 4. The total output of smelters in other regions decreased MoM in January as most smelters produced stably while some smelters reduced the production amid raw material shortage.

In February, the profits of smelters are still suppressed by tight raw material supply and declining TCs. However, with the sharp drop in tin prices, the downstream enterprises have been more willing to purchase and their operating rates rebounded significantly. As such, the demand for refined tin will recover in February. In summary, SMM expects that the domestic refined tin output in February will increase significantly MoM to 14,035 mt.

Battery-grade manganese sulphate

In January, China’s high purity manganese sulphate output stood at 14,000 mt, down 46.97% on the month. Some demand was released in advance due to the Chinese New Year holiday and the expiry of national NEV subsidies. Meanwhile, ternary precursor companies stopped or reduced the production intensively. Therefore, the demand for high-purity manganese sulphate remained weak. According to SMM research, most high purity manganese sulphate enterprises stopped the production for maintenance for about 15-20 days before the CNY holiday. The overall output of high purity manganese sulphate fell sharply in January.

In February, the recovery of demand is still limited. According to SMM research, the new energy car companies and battery cell factories have been less active in resuming the production, and are expected to return to normal production in mid-February. As such, the demand for high purity manganese sulphate stays weak. Considering the declining inventory, high-purity manganese sulphate enterprises have plans to build finished products inventory in February. It is estimated that the output in February will be about 18,700 mt in physical content, an increase of 33.57% from the previous month.

Stainless steel

According to SMM survey, the stainless steel output was 2.34 million mt in January, down 18.48% MoM but up 1.59% YoY. The output of 200-series stainless steel fell 17% MoM to 667,000 mt, 300-series dropped 4.5% MoM to 1.28 million mt, and 400-series declined 8% MoM to 399,000 mt.

The sharp output cut was related to the annual large-scale maintenance carried out by many stainless steel mills. Due to the weak pre-holiday demand and fewer production days in January, the orders received by stainless steel mills were poor. As such, the output of 200-series stainless steel declined sharply and that of 300-series also fell slightly. At the same time, the high ferrochrome prices in December also led to output cut of 400-series stainless steel.

In February, the total output of stainless steel may increase to a certain extent as most stainless steel mills plan to resume the production amid positive market outlook on demand. Some large-sized stainless steel mills may schedule the production cautiously due to tight raw material supply. It is still necessary to pay attention to the digestion of high inventory and the material recovery of terminal demand.

To sum up, SMM believes that the prices of stainless steel may fall slightly in February.

EMM

China produced 101,400 mt of EMM in January, up 16.56% MoM and 680% YoY, according to SMM statistics. Despite the vacations taken by small-sized enterprises amid weak downstream demand, the overall output increased as large-sized enterprises produced actively to ensure the delivery of orders as they stopped the production for a long time in the early stage.

In February 2023, the demand from downstream stainless steel mills is expected to improve and small-sized ones have resumed the production after February 5. But the large-sized enterprises are unlikely to ramp up the production further. Coupled with the less production days in February, the output in February may decline on the month.

Refined nickel

The domestic refined nickel output in January dropped 1.5% on the month and increased 37.24% on the year to 16,400 mt. According to SMM research, mainstream refined nickel enterprises worked in shift during the CNY holiday to ensure normal production. Therefore, the output did not drop sharply in January. In addition, some refined nickel enterprises have increased the production to make sure that downstream rigid demand is fully fulfilled in 2023. Coupled with high premiums of refined nickel against nickel sulphate, some new electrodeposited nickel production lines based on nickel sulphate have been scheduled for production in early January.

The domestic refined nickel output in February is expected to increase 3.05% on the month and 30.8% on the year to 16,900 mt. The capacity of new electrodeposited nickel production lines maintained low operating rates in January and will be fully put into production in February.

NPI

China produced 36,000 mt (Ni content) of NPI in January 2023, an increase of 2.47% month-on-month and 13.75% year-on-year. Affected by the Chinese New Year holiday in January, stainless steel mills carried out large-scale annual maintenance, so the demand for NPI was muted. This forced a small number of NPI plants to cut the output and undertake maintenance to varying degrees. The month-on-month increase is attributable to the output from new capacity at large-scale stainless steel mills integrated with NPI facilities. In detail, the output of high-grade NPI in January was about 30,800 mt in Ni content, an increase of 9.59% from the previous month. The stainless steel mills integrated with NPI facilities which had stainless steel capacity in commissioning accounted for the growth of high-grade NPI output. The output of low-grade NPI stood at 5,300 mt in Ni content in January, a drop of 25.74% on the month. Stainless steel mills that had low-grade NPI facilities conducted large-scale production cuts and maintenance at the end of the year, causing the output to fall precipitously.

It is estimated that the domestic NPI output in February will increase 6.69% from January to around 38,500 mt in Ni content. In February, some NPI factories are expected to resume normal production, in turn lifting the output remarkably. But at the same time, profit margins have shrunk due to the tight supply and the consequent high cost of nickel ore. This has prompted a small number of NPI plants to consider maintenance in February. Still, the output in February will climb.

Indonesian NPI

Indonesian NPI output stood at 101,100 mt in nickel content in January, a month-on-month decrease of 2.41% but a year-on-year increase of 20.8%. In January, Qingdao Zhongzi Zhongcheng and Lygend’s PT Halmahera Jaya Feronikel (HJF) both yielded NPI through their new production lines. The scale of Indonesia's NPI industry has continued to expand as new production lines continued to be put into production, growing the output. Besides, as the poor demand for nickel matte from nickel sulphate has diminished the profitability of the former, the producers’ interest in shifting to produce nickel matte has waned. They turned back to the production of NPI quickly, thus the output of NPI increased. Yet, the production of NPI in Indonesia remained on the decline. The main reason is that one steel mill in Indonesia has significantly whittled down its stainless steel output and undertook partial maintenance of RKEF production lines. That affected the supply of NPI. The production of NPI in Indonesia should continue to shrink in February 2023. Although the output of some manufacturers is expected to recover, the switch of production from NPI to nickel matte will limit the NPI output growth.

Nickel sulphate

China produced 31,200 mt of nickel sulphate with Ni content in January 2023. The output stood at 141,800 mt in physical content, down 16.99% month-on-month but up 19.5% year-on-year. The output cuts of nickel sulphate across China were even more substantial in January than in December, which almost returned to the level of July last year. Significant output cuts at precursor plants in January led to high nickel sulphate inventories, dampening the demand for nickel sulphate. This hampered shipments from nickel sulphate producers. Meanwhile, the raging Covid infections across China on top of China changing its pandemic control policy has taken a toll on all enterprises in the industrial chain. For some enterprises, even more than half of their labour force was infected with Covid-19. The production of nickel sulphate was affected significantly, especially for small enterprises. The lack of personnel has become a major issue. In this scenario, some plants were closed in advance for CNY holidays in January and undertook maintenance. The operating rates then declined, thereby causing the overall production to fall in January. In February, the demand for nickel sulphate proliferated as the large price spread between nickel sulphate and nickel galvanised some plants to purchase nickel sulphate used in refined nickel production. The demand from ternary plants also picked up gradually. Output of nickel sulphate in February is expected to grow 19.7% from January to 37,300 mt in Ni content.

Electrolytic manganese dioxide

SMM data showed that in January 2023, China's electrolytic manganese dioxide output was 10,900 mt (including 500 mt used in LMO battery, 7,000 mt used in alkaline manganese battery, and 3,300 mt for zinc-carbon battery), a month-on-month decline of 16.15%. The decline of electrolytic manganese dioxide output which can be used in LMO battery is the most significant in January partly because the demand for LMO battery was poor. And the price spread between trimanganese tetroxide and manganese dioxide narrowed, which also weakened the electrolytic manganese dioxide demand. This, together with some Chinese manganese plants undertaking maintenance during CNY holiday, reduced the output in January. The output is expected to increase slightly in February to some 11,100 mt as the market players have gradually resumed the production after CNY holidays.

Trimanganese tetroxide

SMM data showed in January 2023, China's Mn3O4 output was 11,200 mt (including 8,200 mt of electronics-grade Mn3O4 and 3,000 mt of battery-grade Mn3O4), a month-on-month drop of 20.36%. The weak demand for lithium manganese oxide prompted some factories to be shut down for CNY holidays, lowering the output of Mn3O4. Factories gradually resumed the production after the Lantern Festival on February 5. But spot prices did not fall sharply even as the downstream demand remained weak. Given the high profit at plants, the output is set to increase slightly MoM to about 12,900 mt.

High-carbon ferrochrome

According to SMM statistics, the output of high-carbon ferrochrome in January stood at 494,000 mt, down 19,500 mt or 3.8% from the previous month and down 57,900 mt or 10.49% on the year. The output in Inner Mongolia was 310,500 mt, down 16,300 mt or 4.99% MoM, and that in Guizhou stood at 16,500 mt, down 43.88% MoM. Many stainless steel mills were overhauled and reduced the production during the slow season at the beginning of 2023. Meanwhile, higher power costs and power rationing during the dry season in south China caused ferrochrome manufacturers in the south to lower their operating rates. But the commissioning of new capacity in north China which had cost advantages ensured some profits, keeping the output in north China stable.

The output of high-carbon ferrochrome in February is expected to be 525,000 mt, which is higher than that in January. Although the peak season has not yet arrived, the remarkably higher production schedules of stainless steel in February will boost the demand for ferrochrome. Bid prices by steel mills in February also beat market expectations. The high ferrochrome prices encouraged the producers to step up or restart production. However, due to the low inventory and low arrivals at ports, the chrome ore prices have gained ground. This in turn eroded the profits of ferrochrome production. In the meantime, the consumption of stainless steel has not really improved. As such, the ferrochrome producers will stand on the sidelines before deciding to resume the production.

Industrial silicon

SMM data showed that China’s industrial silicon output stood at 273,800 mt in January 2022, down 8.97% month-on-month, but up 10.44% year-on-year.

In January 2023, prices of above-standard #553 silicon fell to 17,300 yuan/mt in east China, with the ex-works price of some plants falling below 16,500 yuan/mt. Affected by the sluggish consumption of downstream aluminium alloys and silicone as well as the gloomy export market, silicon plants saw poor shipments and orders. The average electricity price in Xinjiang was 0.32 yuan/kWh, and that in north-China was generally above 0.5 yuan/kwh. For silicon plants in south China, the full cost was mostly above 17,500 yuan/mt. The losses and market pessimism forced the plants to cut or halt the production. The output declined the most sharply in Yunnan and Sichuan with a drop of 10,000-12,000 mt, followed by Hunan and Guizhou where the output fell by some 4,000 mt. New capacity accounted for the output growth in Xinjiang, and the output in Inner Mongolia and Gansu grew only marginally due to maintenance and gradual commissioning of new capacity.

In February, the operating rates during the dry season in Yunnan and Sichuan, the main producing areas, will change little compared to January. The overall output in Xinjiang, Inner Mongolia and Gansu will continue to increase thanks to the commissioning of new capacity. The silicon supply in north-west China will outperform that in south-west China. Driven by the new capacity, industrial silicon output in February is likely to exceed 280,000 mt.

Polysilicon

SMM data shows that in January, the domestic polysilicon output stood at 102,800 mt, up 4.58% on the month. The supply of polysilicon continued to grow and due to the relatively slow growth of downstream demand, polysilicon inventory has continued to accumulate.

According to SMM, the domestic average monthly price of polysilicon in January was 163 yuan/kg (taking dense polysilicon as an example). Based on the industry cost of 60 yuan/kg, polysilicon companies still had a profit of roughly 100 yuan/kg. As such, the polysilicon companies, especially second and third-tier ones, still maintained high production enthusiasm and ramped up the production of some new production lines. In addition, polysilicon prices rebounded in mid-to-late January, which further fuelled the production enthusiasm. Some enterprises in north-west China carried out routine maintenance, which suppressed the growth of polysilicon supply to a certain extent.

Photovoltaic module

According to SMM statistics, the domestic photovoltaic module output in January was about 29.1 GW, an increase of 8.58% from December. Bid solicitation for some end-user projects was initiated in January, lifting module demand to a certain extent. The rebound in upstream products prices bolstered market confidence. This, combined with the recovery of labour force from pandemic, incentivised photovoltaic module plants to beef up production, thus growing the output.

Silicon-manganese alloy

China produced 935,100 mt of silico-manganese alloy (SiMn alloy) in January, up 6.72% MoM and 6.61% YoY, according to SMM statistics. The increase in SiMn alloy output was enabled by aggressive pre-CNY stockpiling by steel mills, ensuring brisk orders and shipments. On the other hand, operating rates in south-China slid as the high costs and power rationing in some regions forced some small plants to cease production during CNY holiday. Most of the producers in north China maintained normal production, and the output increased month-on-month.

Entering February, the market gradually recovered after the CNY holiday. Steel mills will be restarting their production, hence boosting the demand for SiMn alloy. In addition, most of the plants in north China maintained normal production, and the producers in south-China that were shut down for holiday resumed the production. The overall operating rates have increased. The output of SiMn alloy is projected to grow to around 968,600 mt in February.

Magnesium ingot

China's magnesium ingot output stood at 64,000 mt in January, down 2.8% MoM and down 22% YoY, according to SMM statistics. The YTD output in January totalled 64,000 mt, a YoY decrease of 22%.

Affected by migrant workers returning to their hometowns for CNY holiday in January, the number of workers on duty decreased. At the same time, magnesium prices were running at a low level. The shrinking profit also depressed the enthusiasm for production. At present, the workers have gradually returned to work. The magnesium prices lack upward momentum recently, and the prices of raw materials such as ferrosilicon and coal have dipped. It is estimated that the output of magnesium factories will remain low in February at about 65,000 mt collectively. SMM will continue to keep an eye on the output changes in the main producing areas.

Magnesium alloy

China's magnesium alloy output stood at 27,000 mt in January, up 8.7% MoM and 23.5% YoY, according to SMM statistics.

According to some domestic magnesium alloy factories, due to the losses of magnesium ingot in January, some magnesium alloy factories switched to produce magnesium alloys from magnesium ingots, which drove the growth of magnesium alloy production. Based on the current orders, the recovery of magnesium alloy downstream industries has been barely satisfactory, which is still weaker than the same period last year. As the recent upward trend of magnesium prices has been hindered, the magnesium plants in Shanxi are facing great cost pressure and weaker-than-expected orders. As such, the output of magnesium alloy will remain stable at about 27,500 mt in February.

Magnesium powder

China's magnesium powder output stood at 6,000 mt in January, down 2% MoM.

In January, the domestic magnesium powder market remained relatively stable. Due to the impact of the CNY holiday, the output of some magnesium powder companies declined. It is understood from the producers that the relatively high prices of magnesium have diminished the demand from downstream steel mills. The market orders failed to pick up noticeably post CNY holiday. But considering the weather will get warmer and downstream players will resume the production gradually, magnesium powder market is expected to pick up down the road. In February, the output is estimated at roughly 7,000 mt.

PrNd oxide

Domestic output of PrNd oxide in January 2023 stood at 5,622 mt, up 9.5% MoM. Output increased across Fujian, Guangdong, Guangxi, Jiangxi, Jiangsu and Shandong to varying degrees.

In December, the separation plants and recycling companies cut or suspended the production due to year-end maintenance, losses and testing of new equipment. This exacerbated the shortages of spot supply in the rare earth market, thus pushing up the price of PrNd oxide. But most enterprises resumed normal production in January. The output in Guangdong and Guangxi increased noticeably, with a MoM growth of 50% and 150% respectively. The production in Jiangsu also basically recovered, and its output grew about 97% MoM. The production of a small number of enterprises was curtailed during CNY holiday, and will resume in February. SMM expects that the output of PrNd oxide will increase slightly in February.

PrNd alloy

Domestic output of PrNd alloy in January 2023 stood at 5,223 mt, up 1.7% MoM. Fujian and Inner Mongolia accounted for most of the output growth, and the output in other regions changed little compared with December 2022.

In January, the price of PrNd alloy continued to rise. Due to the output cuts and shutdown of separation plants and recycling companies in December, the spot supply of PrNd alloy tightened greatly, and the quotations were raised frequently. PrNd alloy plants hardly had access to raw materials. Meanwhile, downstream magnetic material companies stocked up for CNY holiday, and made inquiries actively. In this scenario, the prices of PrNd alloy climbed. During the CNY holiday, most PrNd alloy plants maintained normal production. Some of the plants that completed maintenance in December also reported small output growth. The output in Inner Mongolia rose about 2% from the previous month, and the output in Fujian increased by a remarkable 50%.

Molybdenum concentrate

In January 2023, China’s molybdenum concentrate output was 17,700 mt, a drop of 6% MoM.

Firstly, healthy profitability of molybdenum concentrate in 2022 has led to a large number of mines in south China closing for holiday in January. This reduced the output of molybdenum concentrate. Secondly, during the CNY holiday in January, some mining enterprises stopped the production for maintenance, thereby reducing the output of molybdenum concentrate. Thirdly, because the downstream demand is relatively stable and the demand has not been fully met, most mining companies maintained stable mining activities. As mining companies fully resume their production after the Lantern Festival, SMM expects that molybdenum concentrate production will rally and exceed 19,000 mt in February.

Ferro-molybdenum

In January 2023, China’s ferro-molybdenum output was 16,800 mt, a drop of 9% MoM.

Two factors have led to the decrease in ferro-molybdenum output in January. First, workers returning to their hometowns for CNY holiday resulted in a shortage of manpower at ferro-molybdenum smelters, so they were forced to lower their operating rates, thereby reducing the output. Second, limited molybdenum concentrate resources available in the market prevented some private smelters from restocking sufficient raw materials in a timely manner, so the output of ferro-molybdenum decreased.

In February, the increase of available molybdenum concentrate resources, combined with the purchases of steel mills, will boost the production enthusiasm of ferro-molybdenum smelters. The output of ferro-molybdenum is expected to rebound to 18,500 mt.

Silver

According to SMM survey, domestic silver output stood at 1,261.515 mt (including 1,145.515 mt of mineral silver) in January 2023, down 10.8% on the month.

Production growth was observed in the market. Some enterprises ramped up the production along with the increase in the raw material supply, while some resumed normal production after they cut the output on completing the production target in December. The reasons for the decrease in output include the CNY holiday and maintenance. In general, the decrease in output outweighed the increase, so the silver output dropped.

SMM expects that the silver output will pick up slightly in February with the production resumption and completion of maintenance.

On the macro front, the US Fed raised the interest rate by 25 basis points on February 2, and the non-farm payroll data released the day after showed that the US unemployment rate in January was 3.4%, lower than the previous print of 3.5% and the forecast of 3.6%. After seasonal adjustment, US non-farm payroll added 517,000 in January, higher than the previous print of 223,000 and the estimate of 185,000. The rate hikes and outstanding non-farm payroll data triggered bearish sentiment in the market, thus the silver prices face downward pressure recently.

Antimony ingot

According to SMM survey, China’s antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in January fell sharply by 15.83% MoM to 6,304 mt.

On the one hand, the surging infections after the relaxed covid-19 control measures at the end of last year caused many workers to take a rest, taking toll on the operating rates of producers in early January. On the other hand, many manufacturers had to cut or halt the production due to raw material shortages and low operating rates. The delayed production was complicated by the Chinese New Year break. Therefore, the overall production of antimony ingots in China recorded a steep fall in January.

So far, the tight supply of antimony ore still persists. It seems that both domestic and overseas supply of antimony ore will not advance in the foreseeable future, which will provide a solid support for a steady increase in antimony prices.

In terms of production details of individual manufacturers, among the 32 respondents in SMM survey, 14 manufacturers suspended the production, up by four from the previous month; 13 reduced their production, down by five; and five maintained normal production, one fewer than in last December.

These figures tell that the production has been increasingly concentrated with the concentration of raw materials.

SMM predicts that the supply-demand structure of the domestic antimony market in February will not be overturned under the current economic situation and the antimony ingot output is anticipated to decline further on a monthly basis.

Refined bismuth

According to SMM survey, the output of refined bismuth in China was 2087.47 mt in January 2023, a sharp decrease of 20.38% compared with December 2022.

On the one hand, the surging infections after the eased covid-19 control measures at the end of last year caused many workers to get infected, taking toll on the operating rates of producers in early January. On the other hand, many manufacturers had to cut or halt the production due to raw material shortages and low operating rates. The delayed production was further complicated by the Chinese New Year break. As a result, the domestic production of refined bismuth in January posted a significant decline.

However, on the whole, only a small number of refined bismuth manufacturers were shut down while most still operated at reduced capacity. Among the 23 survey respondents in SMM sample, four manufacturers halted the production in January, up by one from the previous month, and six slashed their output on a monthly basis.

It is expected that refined bismuth prices in February will strengthen on the falling output. In conclusion, SMM predicts that domestic production of refined bismuth in February may continue to decline.

Silver nitrate

The domestic silver nitrate plants with sales qualification together produced 535 mt of silver nitrate in January, down 14.4% from a month earlier. The total output of silver nitrate nationwide reached 563 mt.

In general, the output across all silver nitrate producers contracted in January mainly because of the CNY holiday. According to SMM survey, most producers received excessive orders before the holiday thanks to the thriving downstream demand. Therefore, SMM estimates that the silver nitrate output in February will go up.

Titanium dioxide

SMM data shows that China's titanium dioxide output stood at 300,000 mt in January, up 6.7% from the previous month and down 6.1% from the previous year.

SMM survey showed that titanium dioxide producers gradually resumed their production from the year-end maintenance and were passionate about production as the downstream demand picked up on warm weather. In fact, some enterprises were already back to full production. On top of that, the positive macro policies lately also boosted the production enthusiasm.

SMM believes that titanium dioxide output will keep rising and the output in February is estimated at 320,000 mt.

APT

The APT output in China stood at 8,000 mt in January, a decrease of 33% on a monthly basis, which is in line with the market expectation.

There are two reasons for the decline. First, the raw material costs have been rising on elevated tungsten concentrate prices since Q4 last year, while the demand from cemented alloy industry was weakening. As a result, the losses dampened APT smelters’ willingness to produce. Second, many smelters were either closed for maintenance/holiday or cut the production, weighing on the average operating rate and leading to falling APT output.

In February, the APT output has picked up on rising operating rates post the CNY holiday and with end demand recovery. However, the low profit margins will prevent smelters from running at full capacity. SMM forecasts that the APT output in February will be 10,000 mt.

Lithium carbonate

China lithium carbonate output in January stood at 35,925 mt, up 3% on a monthly basis and 89% on a yearly basis.

In January, some spodumene-based smelters were under maintenance and the production from salt lake continued to decline on seasonal factors. This, combined with the falling operating rates of recycling enterprises, caused the output of lithium carbonate to dwindle. While at the same time, the lepidolite-based smelters whose production had been restricted by environmental protection were resuming the production, in addition to a significant increase in new capacity. Altogether, the total output climbed.

In February, the maintenance of some spodumene-based smelters is still ongoing, but the total output will see an increase thanks to the stable production of lepidolite-based smelters and the production ramp-ups of salt lake on warm weather.

China’s lithium carbonate output in February is thus estimated to grow 1% on a monthly basis and 94% on a yearly basis to 36,179 mt.

Lithium hydroxide

China’s lithium hydroxide output was 21,235 mt in January, down 16% MoM and up 31% YoY.

Some new smelters started to ramp up the production, but the output fell as a result of maintenance. Meanwhile, causticising plants cut the production aggressively due to weak downstream demand. In February, the enterprises are recovering from the maintenance, while the new capacity is released along with the increase in the output of causticising plants.

It is forecast that the lithium hydroxide output will reach 23,774 mt in February, up 12% MoM and 87% YoY.

Cobalt sulphate

In January, the cobalt sulphate output stood at 6,315 mt in metal content, down 6% month-on-month and 16% year-on-year.

The sharp decline in the output is primarily attributed to the sluggish cobalt prices that dampened the production enthusiasm of domestic smelters. Additionally, smelters were mostly closed during the CNY holiday. On the other hand, the demand for cobalt sulphate from power battery sector was poor as most precursor plants curtailed their production in the wake of the removal of NEV subsidies. The electronics market remained sluggish, where top-tier electronics manufacturers halved their production and many e-cigarette cell producers took early holiday. In this case, the demand for cobalt sulphate from the electronics sector also recorded a significant decline.

SMM predicts that cobalt sulphate output will rise 25% MoM and 17% YoY to 7,889 mt in metal content in February.

Tricobalt tetraoxide (Co3O4)

The output of Co3O4 stood at 3,556 mt in January, down 29% MoM and 53% YoY.

On the supply side, domestic top-tier Co3O4 manufacturers slashed their production while other large producers also trimmed their output on CNY holiday. On the demand side, the leading LCO producers cut their production by two thirds, implying an exceedingly weak demand for Co3O4.

The output of Co3O4 in February is estimated to rise slightly on a monthly basis to 3,838 mt, up 8% MoM and down 48% YoY.

Ternary cathode precursor

The domestic ternary cathode precursor output was 58,219 mt in January, down 24% month-on-month decrease and 4% year-on-year.

The removal of NEV subsidies and the CNY holiday together resulted in a decline in the orders of domestic leading battery plants, which was responsible for a sharp decrease in the output of ternary cathode materials. Since the overseas demand for power battery and energy storage was stable, the top-tier precursor plants having export orders will see a less sharper decline in output.

It is expected that the production of high-grade nickel precursor will continue to take a larger proportion, while the proportion of 5-series precursors will diminish. SMM predicts that the ternary cathode precursor output will rise 16% MoM to 67,658 mt in February, up 14% YoY.

Ternary cathode materials

The domestic ternary cathode material output was 40,804 mt in January, a month-on-month decrease of 23% and a year-on-year decrease of 12%.

The removal of NEV subsidies set off a low season for NEV and electronics markets, in addition to lower demand from overseas market. Moreover,, the end consumption retreated sharply in January compounded by the CNY holiday.

The weak demand finally took toll on the production. The large ternary cathode material plants mostly closed since mid-January for one to two weeks, medium-size plants usually took a two-week holiday, while most small plants were shut down for the whole month. The total output of ternary cathode materials recorded a negative growth compared with the same period last year.

Since February, ternary cathode material enterprises started to resume the production, but still maintained the capacity at low levels. The overseas demand recovery has not be observed yet.

Output of ternary cathode materials in February is expected to rise 5% on the month and drop 2% on the year to 42,665 mt.

Iron phosphate

The domestic iron phosphate output stood at 62,102 mt in January, down 23% on a monthly basis.

On the supply side, the average operating rate of iron phosphate producers were low due to CNY holiday and maintenance, weighing on the output. On the demand side, the LFP enterprises continued to cut the production in January, which led to fewer orders for iron phosphate. The inventories of iron phosphate enterprises have been on the rise. In terms of raw materials, the prices of phosphorus source and iron source fluctuated narrowly, but the upcoming spring ploughing and the ongoing power rationing in Yunnan and Guizhou still pose the risks of rising costs.

Based on relatively stable costs in the short term and potential demand recovery, SMM estimates that the iron phosphate output in February will gain 6% on the month to 65,612 mt.

LFP

China produced 64,457 mt of LFP materials in January, a decrease of 36% month-on-month and an increase of 4% year-on-year.

The LFP enterprises continued to reduce the production considering the CNY break, maintenance and poor demand, and still focused on digesting inventories. On the cost side, the lithium salt prices seem to decline further, while most LFP enterprises had sufficient lithium salt inventories and maintained their operating rates at low levels. The purchasing demand for raw materials was slack. The iron phosphate enterprises also had high inventories, which caused its prices to keep falling. The overall demand was slow in recovery, missing the previous expectations.

The LFP output in China is expected to be 69,571 mt in February if the enterprises fully resume the operation, up 8% month-on-month and 30% from the previous year.

LCO

The LCO output was 3,149 mt in January, a month-on-month decrease of 45% and down 58% on an annual basis.

The weak demand and the CNY break together caused the top-tier LCO producers to slash the production by two thirds, while the second-tier LCO producers also halved their production.

The demand for mobile phone remained sagging, while the demand for laptops slipped drastically. The manufacturers of e-cigarette with high charge and discharge rate were mostly closed in January. Under these circumstances, the LCO output fell aggressively.

It is expected that LCO output will pick up after the post-holiday production resumption, but the increase will be restrained by poor demand. SMM predicts that the LCO output will rise 41% MoM and drop 33% YoY to 4,434 mt this month.

LMO

China's LMO output in January stood at 2,608 mt, down 62% on the month and 54% on the year.

The decline was caused by the Chinese New Year (CNY) break, the falling lithium carbonate prices and poor downstream demand. Specifically, most LMO enterprises cut or suspend the production in January.

At the same time, the trades in the market were quiet with the logistics suspended a week before the holiday, further weighing on the production.

SMM survey showed that the production resumption of LMO enterprises is proceeding smoothly, but the lithium carbonate prices extended the fall. As a result, battery cell makers took a wait-and-see stance and pushed up lower prices strongly. In response, some LMO enterprises delayed the re-opening.

According to the feedback from the market, battery cell makers might face a shortage of LMO stocks after the mid-February, thus lifting the demand for LMO.

It is estimated that LMO output will be boosted to 4,536 mt, up 74% on the month and 10% on the year.

![[SMM Precious Metals Express]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)

![Platinum prices consolidate, while spot market demand remains sluggish [SMM Daily Review]](https://imgqn.smm.cn/usercenter/ipCjz20251217171734.jpeg)