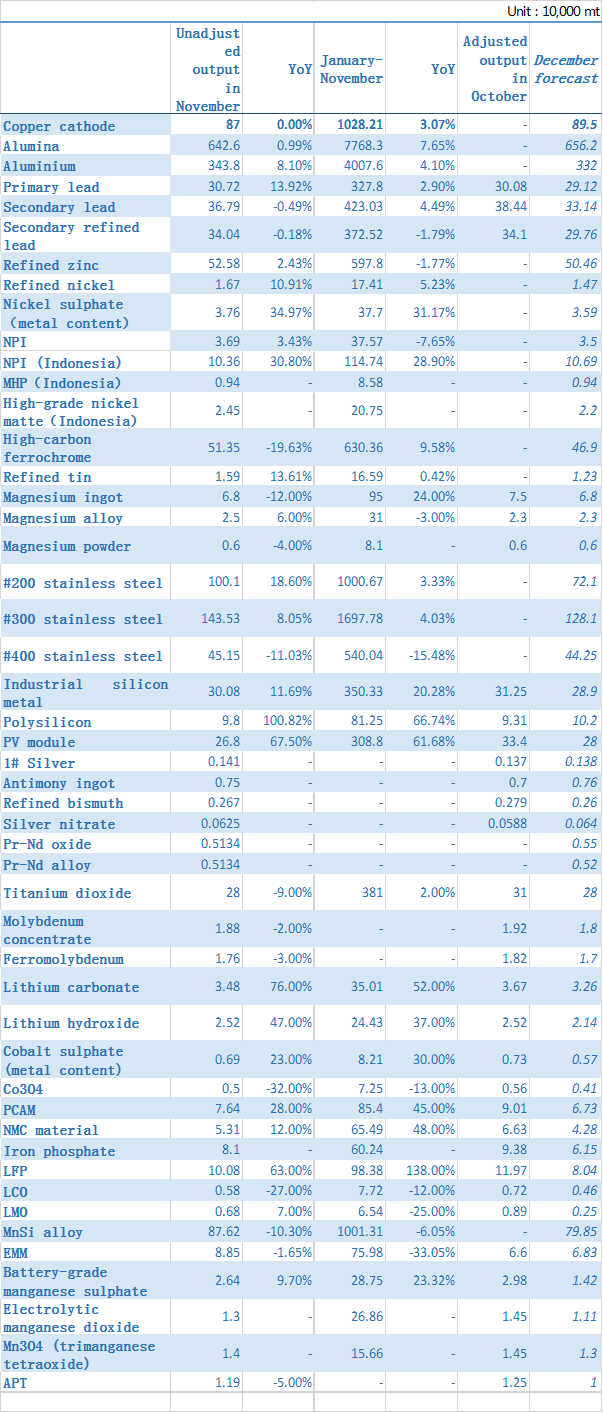

Copper cathode

SMM data showed that China’s copper cathode output stood at 870,000 mt in December 2022, down 3.3% from the previous month and flat from the same period in 2021. The actual output was 17,900 mt lower than the expected 887,900 mt. The output totalled 10.28 million mt in 2022, up 3.07% or 306,200 mt year-on-year.

SMM attribute the unexpected decline in output to the following reasons: 1. Four smelters undertook maintenance in December, which had more significant impact on the production than expected. 2. The output of some smelters was also lower than expected due to the pandemic outbreak. 3. The output increase contributed by the two newly-commissioned smelters was lower than expected. 4. Some smelters controlled the production in December as they have completed the production goal of 2022 ahead of schedule.

Entering 2023, although the operating rates of most smelters will drop slightly compared to December 2022 due to the Chinese New Year holiday, the output will gradually resume to the normal level as the newly-commissioned smelters continue to ramp up and the smelters that undertook maintenance in the previous period gradually resume. China’s copper cathode output is estimated at 895,000 mt in January 2023, up 25,000 mt or 2.87% MoM and 9.7% YoY based on the current production schedules.

Aluminium

According to SMM data, China produced 3.44 million mt of aluminium in December 2022 (31 calendar days), up 8.3% on the year. The daily output dropped 261 mt/day on the month to 110,900 mt. The output totalled 40.08 million mt from January to December 2022, an increase of 4.1% on the year. The domestic operating capacity of aluminium in December declined slightly month-on-month as the aluminium smelters in Guizhou were forced to stop the production twice amid the power shortage in late December, which led to an output cut of 450,000 mt. However, considering the equipment shutdown process and collection of aluminium liquid, the impact of production cuts in Guizhou was limited. Meanwhile, an aluminium smelters in Shandong planned to transfer part of its production capacity, hence its output declined about 60,000 mt. Meanwhile, the aluminium smelters in Sichuan continued to resume the production in December 2022 and 340,000 mt of capacity was resumed. The commissioning progress of the new project of Inner Mongolia Baiyinhua and Gansu Zhongrui was slow, hence the output increased only slightly. According to SMM statistics, by the beginning of January 2023, domestic installed aluminium capacity reached 45.26 million mt (including the production capacity that has been installed but has not been put into production). The domestic operating aluminium capacity was 40.43 million mt, and the national operating rate averaged about 89.3%. In December 2022, the proportion of aluminium liquid fell 2.74 percentage points month-on-month to 66.38% as the operating rates of downstream users like aluminium billet and aluminium alloy enterprises declined.

Entering January 2023, there is no expectation of large-scale production ramp-up as the power shortage in south-west China is unlikely to alleviate in the short term. The aluminium enterprises in Guizhou will continue to significantly reduce the production in January with an estimated output cut of 400,000-500,000 mt. Meanwhile, the resumption of production in Sichuan and Guangxi has slowed down due to the power shortage and low profits. According to the capacity changes, the domestic operating capacity of aluminium may decline to around 40 million mt at the end of January and the output in January (31 days) is expected to increase 3.7% YoY to 3.32 million mt.

On the demand side, the downstream consumption was poor in December 2022 amid the traditional off-season, the labour shortage and halted transportation caused by the domestic pandemic outbreak. Coupled with the weak terminal demand, the new orders of aluminium processing plants were sluggish and the operating rates declined accordingly. Meanwhile, due to the poor logistics efficiency, the arrivals of aluminium ingot and aluminium billet were few in December 2022 and thus the aluminium inventory remained low. However, the inventory increased in light of the weak demand at the end of December. As for now, the social inventory stood at 576,000 mt, a decrease of 200,000 mt compared with the same period last year. The downstream consumption has declined significantly in January amid the approaching Chinese New Year. Coupled with the increasing aluminium ingot output, the domestic aluminium social inventory may accumulate further in January. SMM predicts that the domestic aluminium ingot social inventory may increase to 850,000 mt by the end of January and reach 1 million mt in mid-February.

Alumina

China’s metallurgical-grade alumina output in December (31 calendar days) was 6.43 million mt, up 2.1% MoM and 0.99% YoY, according to SMM statistics. The average daily output increased 2,500 mt to 207,300 mt. The output totalled 77.68 million mt in 2022, an increase of 7.65% on the year.

As of the end of December 2022, the domestic installed alumina capacity stood at 96.75 million mt, while the operating capacity was 75.44 million mt, implying an average domestic operating rate of 79%. On the whole, it is estimated that the net imports of alumina in December 2022 will be 150,000 mt. And there existed a slight shortage of 44,000 mt in the month, and a surplus of about 1.66 million mt during January-December 2022. The total output in December increased compared with November despite the lower operating rates and daily output as the working days in December increased by one day. In north China, the alumina refineries were less willing to resume or increase the production in December due to the pandemic outbreak, the heating season, high costs, declining transportation efficiency, and the difficulty in ore procurement. In addition, the second phase of Lubei Chemical and Luyu Bochuang’ project failed to yield output intensively in December. Therefore, the overall alumina output in north China did not increase. In south-west China, 1.2 million mt alumina capacity was reduced and the output declined about 110,000 mt in December due to the power restrictions as the supply of electricity was still tight in Guizhou.

On the whole, the total installed production capacity increased 9.2% from 88.6 million mt in 2021 to 96.75 million mt in 2022 with the commissioning of 10.3 million mt of new capacity and the annual alumina output increase 7.65%, which exacerbated the oversupply. In January 2023, the new production capacity of Lubei Chemical and Luyu Bochuang will start to yield output. It is estimated that the output in January (31 days) will be around 6.56 million mt, a year-on-year increase of 3.1%.

Primary lead

China produced 307,200 mt of refined lead in December, up 2.14% MoM and 13.92% from YoY. The total output in 2022 increased 2.9% from the same period of 2021. Production capacities of enterprises involved in the survey totalled 5.71 million mt in 2022.

According to SMM research, most refined lead smelters produced stably in December. Only a few enterprises appropriately lowered their production as they have achieved their annual production goals while some enterprises continued to ramp up the production in order to complete the annual output plan. In addition, Yunnan Mengzi and Western Mining resumed the production from maintenance. Therefore, the output in December continued to increase slightly compared with the previous month.

In January 2023, some small and medium-sized enterprises in Henan and Hunan plans to take holidays for 7-15 days for CNY while most other refined lead smelters will continue to produce in shifts. As such, the output will not decline significantly. However, enterprises such as Yunnan Zhenxing and Hunan Shuikoushan plan to carry out maintenance in January, which will bring a certain reduction in the output. On the whole, the refined lead output in January will stop increasing and decline amid the Chinese New Year, routine maintenance, and the completion of production targets. SMM predicts that the domestic output will drop more than 10,000 mt to around 290,000 mt.

Secondary lead

China produced 367,900 mt of secondary lead in December 2022, down 4.29% MoM and 0.49% YoY. For January-December 2022, the combined output surged 4.49% YoY to 4.23 million mt. China produced 340,400 mt of secondary refined lead in December 2022, down 0.18% MoM but up 1.76% YoY. For January-December, the combined output fell 1.79% YoY to 3.73 million mt.

In December 2022, the output of domestic secondary lead and secondary refined lead both fell month-on-month as some smelters in Jiangxi either stopped or reduced their production to varying degrees in answer to the environmental protection requirements. Meanwhile, the secondary lead smelter of Zhejiang Tianneng stopped the production for maintenance in early December, and will gradually resume the production after the Chinese New Year. In addition, some secondary lead smelters reduced the production in the short term as many workers were infected with covid after the domestic pandemic prevention and control policy was relaxed. However, some enterprises resumed the production since late November and increased the production in December due to the strong performance of SHFE lead contract. Among them, Hubei Jinyang, Xinjiang Camel and Henan Yongxu resumed the production in mid and late-November. Anhui Huabo increased the production more significantly in December and many other companies also ramped up the production slightly. As a result, domestic secondary refined lead output did not decrease significantly in December.

In January 2023, most domestic secondary lead smelters have completed the pre-holiday restocking of battery scrap, and about 40% of secondary lead smelters will take holidays for CNY holiday starting from mid-January and the production will be suspended for 7-15 days. In addition, some secondary lead smelters that have not stockpiled in large amount for the time being will reduce the production during the Chinese New Year. It is estimated that the domestic secondary lead output in January will be 331,400 mt, and the output of secondary refined lead will be 297,600 mt.

Refined zinc

China's refined zinc output was 525,800 mt in December 2022, a month-on-month increase of 1,100 mt or 0.21%, and a year-on-year growth of 12,500 mt or 2.43%, SMM data showed. Output in 2022 totalled 5.98 million mt, down 1.77% from 2021.

According to SMM survey, domestic refined zinc output in December increased compared with November, but was slightly lower than market expectations as a large-sized smelter in north-west China reduced its output in December after completing its annual production plan ahead of schedule. In addition, a smelter in north China cut the output due to equipment failure. The increase in output was mainly driven by the smelters in Shaanxi operating at full capacity and the smelters in Sichuan resuming the production in December.

In 2023, the domestic benchmark TCs of zinc concentrate (Zn 50%) stand at 5,500-6,000 yuan/mt in metal content, ensuring high profit at smelters. According to SMM survey, most of the domestic medium and large-scale primary zinc smelters will maintain relatively high operating rates during Chinese New Year holidays. In addition, Western Mining will complete maintenance and Sichuan Sihuan Electrolytic Zinc Company will beef up the production. Jinli Gold & Lead plans to yield zinc ingots in the first half of January, with a planned output of 150-200 mt/day. In terms of production reduction, it is mainly concentrated in secondary zinc smelters in Sichuan, Hunan and Jiangxi, due mainly to the closure for CNY holidays.

As such, the refined zinc output is expected to fall 21,100 mt month-on-month to 504,600 mt in January 2023, a year-on-year drop of 12,900 mt or 2.5%. SMM mainly surveyed the domestic smelters in the northern regions as the inventory in other regions was low.

Refined tin

Domestic refined tin output was 15,905 mt in December 2022, down 1.82% MoM but up 13.61% YoY, and the combined output from January to December 2022 increased 0.42% YoY, according to SMM research. The actual output in December was slightly better than expected.

The slight drop in the output of refined tin in December was mainly caused by the pandemic outbreak. In terms of regions, 1. the output of smelters in Yunnan decreased slightly from the previous month. Some smelters either reduced or stopped the production due to the shortage of raw materials and the low TCs. However, the impact was limited and the actual output changed little as the large-sized enterprises produced stably. 2. The output of smelters in Guangxi increased on the month. The actual influence of tight raw material supply was limited and enterprises maintained stable production and were active in delivery. Therefore, the actual output was slightly higher than expected. 3. The output of smelters in Jiangxi stabilised. The mainstream smelters in Jiangxi maintained normal production, and only a few smelters slightly reduced the production due to the raw material shortage and the New Year's Day holiday. However, the inventory of smelters in Jiangxi declined obviously as some of them delivered intensively in December. 4. The total output of smelters in other regions decreased month-on-month in December. In general, some smelters in central China were significantly affected by the pandemic outbreak and reduced the production greatly while the others produced stably.

In January 2023, the profits of smelters are still suppressed by the tight raw material supply and the declining TCs. Meanwhile, downstream enterprises are still less willing to purchase amid the high tin prices. Therefore, the pre-holiday restocking is not as active as in previous years. Some smelters have lowered their output expectations due to the production suspension during the CNY holiday. In summary, SMM expects that the domestic refined tin output in January will fall significantly to 12,290 mt.

Refined nickel

China produced 16,700 mt of refined nickel in December, up 11.52% on the month and 10.91% on the year. The refined nickel output increased significantly in December, which is in line with expectations as most smelters produced normally to complete their production tasks in 2022. The domestic refined nickel output in January 2023 is expected to drop 12.01% on the month and increase 22.59% on the year to 14,700 mt.

The refined nickel output will increase significantly on the month in January as the smelters in north-west China have completed the maintenance and reached normal production. In addition, the electrodeposited nickel project owned by Tsingshan and outsourced to a new energy company in Hubei has started to yield output. The preliminary designed output is 1,500 mt/month, and some output will be released in January 2023.

NPI

In December 2022, NPI output in China was 35,200 mt in Ni content, down 4.74% from the previous month but up 6.20% from the previous year. At the end of November, the NPI inventory accumulated slightly. Coupled with the declining futures prices of stainless steel, the NPI prices fell. Some NPI plants reduced the production and conducted maintenance in advance under the sluggish market environment. In December, as the futures prices of stainless steel increased driven by engagement of investors, steel mills were active in making inquiries amid the pre-holiday restocking period. As such, the transactions were active and the NPI inventory declined sharply, which led to the price hike. The output of high-grade NPI in December declined 5.21% on the month to 28,100 mt in metal content as some large-sized NPI plants slightly reduced the production amid the weaker-than-expected market performance. The output of low-grade NPI plummeted 2.84% to 7,100 mt in metal content due to the oversupply as the output of 200 series stainless steel declined in November.

It is estimated that the domestic NPI output in January 2023 will decline 2.74% from the previous month to around 34,200 mt in Ni content. Most NPI plants plan to reduce the production and undertake maintenance during the CNY holiday while some large-sized NPI plants hold a bullish outlook on the market in February and plan to increase the production. In summary, the NPI output in January will show a downward trend as a whole.

Indonesia NPI

Indonesia NPI output in December 2022 stood at 103,600 mt in Ni content, up 2.8% MoM and 30.8% YoY statistics. The output totalled 1.15 million mt throughout 2022, a year-on-year increase of 28.9%. In December, the output of Huadi Industrial Park increased after the maintenance ended. At the same time, the production capacity of the new production lines in Tsingshan Indonesia Weda Bay Industrial Park, Wanxiang Nickel Indonesia and Lygend HJF projects ramped up, and thus the output increased significantly. Although the output of NPI was reduced due to the weak stainless steel market, the output of Indonesia NPI still increased as the impact of output cuts was limited. Meanwhile, the high-grade nickel matte output in December did not increase significantly. In January 2023, the maintenance of the production lines in PT.GNI industrial park will have a certain effect on the NPI output. However, some production lines will be transferred to produce NPI (for stainless steel) amid the weak market demand for high-grade nickel matte and the higher profits of the direct NPI sales. As such, the Indonesia NPI output may continue to increase in January 2023.

Nickel sulphate

China’s nickel sulphate output in December 2022 stood at 37,600 mt in metal content and 170,800 mt in physical content, down 11.39% on the month but up 34.97% on the year. The demand for ternary batteries from new energy vehicle manufactures has diminished as they basically completed battery installation in late November. Some ternary battery plants integrated with nickel sulphate capacity cut the output of salt as a result of significantly lower output of ternary batteries. The use of high-grade nickel matte accounted for 33% in December, and that of MHP accounted for 45%. The use of nickel briquette and nickel powder accounted for only 1% due to the lack of cost efficiency. Scrap accounted for 13% of the use of raw materials. In January 2023, demand for nickel sulphate from ternary manufacturers will weaken further. Some plants have maintenance plans in mid-January, and some enterprises are expected to curtail their production due to poor orders. Output of nickel sulphate in January is expected to decrease 4.5% from December to 35,900 mt in Ni content.

Battery-grade manganese sulphate

In December 2022, China’s high purity manganese sulphate output stood at 26,400 mt, down 11.41% on the month. According to SMM research, the delivery of long-term orders of mainstream manganese salt factories was lower than that in November. As the terminal demand in the new energy sector extended the weakness, most battery factories and ternary cathode material companies reduced the production to lower their inventory, hence the demand for precursor declined significantly. Among them, the output of 5 and 6-series ternary precursor declined the most significantly, and thus the demand for manganese sulphate was suppressed greatly. Therefore, most manganese sulphate plants maintained low operating rates to control the inventory level and the prices. Coupled with the production cuts of manganese sulphate by integrated precursor enterprises, the overall output of high purity manganese sulphate fell sharply in December.

In January 2023, the demand for high purity manganese sulphate will remain weak as the precursor enterprises will continue to reduce the output during the CNY holiday. Therefore, manganese salt plants will suspend the production for maintenance since January and the duration diverges. And the maintenance is expected to end in early February. The output in January will be about 14,200 mt in physical content.

Electrolytic manganese dioxide (EMD)

In December 2022, China's electrolytic manganese dioxide (EMD) output was 13,000 mt (including 1,200 mt for LMO battery, 8,400 mt for alkaline manganese battery, and 3,400 mt for alkaline zinc battery), a month-on-month decline of 10.34%. The total output in 2022 was around 268,500 mt. The output in December declined as the overseas demand was released in the previous stage and the traditional off-season arrived. Coupled with the further decline in the prices of trimanganese tetraoxide and the sluggish LMO market, the market demand was weak and the operating rates declined.

It is estimated that in January 2023, due to the CNY holiday and the traditional off-season, the output may decline further to about 11,100 mt.

Mn3O4 (trimanganese tetraoxide)

In December 2022, China's Mn3O4 output was 14,000 mt (including 8,300 mt of electronics-grade Mn3O4 and 5,700 mt of battery-grade Mn3O4), a month-on-month decrease of 3.45%. Although the delivery activities in the spot market were active, the new orders declined amid the declining downstream demand. Coupled with the pandemic outbreak, the operating rates declined and the output dropped amid the labour shortage.

In January 2023, the market transactions are thin amid the traditional off-season. And some factories will suspend the production for CNY holiday. As such, the expected output is about 13,000 mt.

High-carbon ferrochrome

According to statistics, the output of high-carbon ferrochrome stood at 513,500 mt in December, down 13,300 mt or 2.52% from the previous month and 125,400 mt or 19.63% on the year. The output in Inner Mongolia was 326,800 mt, up 21,100 mt or 6.9% MoM, and that in Shanxi stood at 44,000 mt, up 27.54% MoM. In December, the bid prices offered by steel mills were still higher than market expectations. The ferrochrome plants in north China were active in production amid the restocking demand of steel mills and the recovered production profits. During the dry season in south China, the electricity prices increased and Guizhou announced to conduct power rationing. As such, more ferrochrome plants in south China either reduced or stopped the production, and thus the overall output decreased slightly on the month.

In January 2023, the output of high-carbon ferrochrome is expected to be 469,000 mt, which is lower than that in the previous month. At the beginning of 2023, the steel mills are not in a rush to produde and many steel mills plan to reduce the production and conduct overhaul. As such, the stainless steel output is expected to decline greatly and the demand for ferrochrome weakens accordingly. Due to the impact of the pandemic and the approaching Chinese New Year, some ferrochrome factories have experienced a labour shortage, hence the supply of high-carbon ferrochrome scrap was tight. In addition, the factories in Guizhou extends and Ulan Qab and Bayannaoer in Inner Mongolia also experience power shortage. Therefore, the supply of high-carbon ferrochrome is likely to drop.

Stainless steel

According to SMM survey, the stainless steel output was 2.89 million mt in December 2022, down 0.29% MoM but up 7.76% YoY. The output of 200-series stainless steel increased 1.42% MoM to 1 million mt, 300-series stainless steel dropped 2.28% MoM to 1.44 million mt, and 400-series stainless steel increased 2.50% MoM to 451,500 mt.

The total output in December remained stable, of which the output of 200-series stainless steel increased slightly, the 300-series stainless steel decreased slightly, and the 400-series stainless steel remained flat. In the first half of December, the transactions of 200-series CRC (cold-rolled coil) picked up slightly and the profit margin of 200-series stainless steel expanded. As such, stainless steel mills slightly increased the production of 200-series stainless steel. Some stainless steel mills reduced the production and conducted maintenance from the second half of November to December due to the high raw material costs and high social inventory as the downstream enterprises were less willing to restock. Therefore, the total output of the 300-series stainless steel decreased slightly from the previous month.

In January 2023, the total output of stainless steel will decline obviously month-on-month as the output of 200-series stainless steel declines amid the high raw material prices and the poor profits. As the demand continues to weaken amid the approaching Chinese New Year, the market is cold and stainless steel mills plan to conduct annual large-scale maintenance in January.

EMM

China produced 88,500 mt of EMM in December 2022, up 34.07% MoM but down 1.65% YoY, according to SMM statistics. The EMM output totalled 759,800 mt in 2022, a decrease of 33.05% year-on-year. The output increased in December as some manganese plants that had a backlog of orders due to the production suspension in the early stage were active in production. Although some small-sized factories remained halted, the operating rates of large-sized factories were relatively stable. Therefore, the overall output increased month-on-month.

In January 2023, the downstream demand is relatively weak despite the restocking period, hence many small-sized factories stop the production and take holidays in advance. Coupled with the power shortage in Guizhou, the market output will decline. However, since the operating rates of large-sized factories remain stable, the output is expected to be about 92,300 mt in January.

Industrial silicon metal

The domestic silicon metal output stood at 300,800 mt in December, down 3.47% MoM but up 11.69% YoY, according to SMM statistics. The output totalled 3.50 million mt in 2022, a year-on-year increase of 20.28%. The operating rates varied across different regions. The reduction in the output in December was mainly attributed to the manufacturers in Sichuan, Yunnan, Guangxi and Hunan. The production costs of silicon enterprises in Sichuan were about 1,000 yuan/mt higher than that in Yunnan due to the higher electricity prices. As the spot prices of industrial silicon metal continued to fall, silicon companies in Sichuan suffered losses and the operating rates dropped rapidly to about 30%. Silicon enterprises in Dehong, Yunnan gradually reduced the production in late December amid the dry season, but the overall reduction pace was slower than that in Sichuan. The output in Yunnan and Sichuan decreased more than 30,000 mt in December from the previous month. In Xinjiang, the output increased mainly due to the resumption of production of the large-sized factories and the release of new production capacity. In January 2023, the output of silicon enterprises in Sichuan and Yunnan is expected to continue to decrease and the operating rates may stand around 20%. The operating rates in Yunnan may be around 40-50% as the silicon enterprises in Nujiang resume the production. The output of silicon enterprises in the Sichuan and Yunnan will decline further in January. At the same time, the production capacity in Xinjiang, another major production area, continues to increase and output increases further. Overall, the domestic industrial silicon metal output will continue to decrease in January 2023.

Polysilicon

The output of polysilicon stood at around 98,300 mt in December, up 5.59% on the month, according to SMM statistics. The continuous increase in the polysilicon output exacerbated the oversupply. According to SMM, the polysilicon enterprises were still active in production as the first-tier enterprises still managed a profit of 90 yuan/kg when the sales price stood at 150 yuan/kg. Coupled with the commissioning of new production lines, the polysilicon output continued to increase. However, due to the aggravation of the domestic pandemic in December, the production of some enterprises in Xinjiang and Inner Mongolia was suspended or reduced amid labour shortage.

PV module

According to SMM statistics, the output of domestic photovoltaic (PV) module in December 2022 was about 26.8 GW, a significant decline of 19.76% from November. The PV market was cold and the terminal demand plummeted due to the stagnated terminal projects, declining raw material prices and domestic pandemic outbreak. As such, the module companies lowered their operating rates and the output declined accordingly. In January 2023, leading module companies have raised their operating rates after the New Year’s Day holiday as the silicon wafer prices remain stable and the terminal demand is expected to increase. The PV module output is expected to increase to 28 GW amid the improving market confidence.

SiMn alloy

China produced 876,200 mt of silicon-manganese alloy (SiMn alloy) in December, up 7.02% MoM and down 10.30% YoY, according to SMM statistics. The combined SiMn alloy output in China throughout 2022 stood at 10.01 million mt, a decrease of 6.05% year-on-year. According to SMM research, the MoM increase in SiMn alloy output in December was driven by two factors. On the one hand, the pandemic had previously disrupted the transportation, resulting in low inventory of SiMn alloy at steel mills. With the gradual lift of pandemic control in December, steel mills started to restock and SiMn alloy producers received abundant orders. On the other hand, steel mills still engaged in winter stockpiling towards the year-end, hence the demand for SiMn alloy was moderate. In conclusion, the production enthusiasm of SiMn alloy manufacturers pushed up the SiMn alloy output month-on-month.

In January 2023, the terminal sector has entered the traditional low season. In addition, most steel mills have cut or suspended the production on upcoming Chinese New Year, with some already off for holiday. The general transactions were thin. Altogether, SiMn alloy output is expected to decline to 798,500 mt in January.

Magnesium ingot

According to SMM data, China's magnesium ingot output stood at 66,000 mt in December, down 12% on the month and 4% on the year. The output totalled 950,000 mt from January to December, a year-on-year increase of 24%.

The transactions in the domestic market shrank sharply in December compared with the same period last year due to lower-than-expected downstream demand. At the same time, the falling magnesium prices squeezed the profits of factories, some of whom were reluctant to produce on high losses. Moreover, the widespread pandemic also weighed on the operating rates of magnesium plants. Altogether, the total output of magnesium ingots in December posted a substantial decrease. As for the forecast, the impact of the first wave of intensive covid-19 outbreak on the production of magnesium factories has subsided, but the sluggish demand will continue to subdue the production enthusiasm. Therefore, it is expected that the domestic output of magnesium ingots will remain low at about 68,000 mt in January.

Magnesium alloy

China's magnesium alloy output stood at 25,000 mt in December, up 6% MoM and 22% YoY, according to SMM statistics. The total output in 2022 declined 3% year-on-year to 310,000 mt.

According to the feedback from domestic magnesium alloy factories, the downstream market continued to be weak in December, and some terminal enterprises took holidays half a month earlier than usual. As a result, the new orders for magnesium alloys dropped, and some large plants mainly produced to deliver previous orders. At present, the economic environments at home and abroad still remain weak, and downstream buyers are not interested in making inquiries. As such, it is estimated that the output of magnesium alloys in January will dip to about 23,000 mt.

Magnesium powder

China's magnesium powder output in December, 2022 was down 4% MoM to 6,000 mt, and the combined output in 2022 totalled 81,000 mt.

Generally, the domestic output of magnesium powder in December was slightly lower than that of the previous month. According to the feedback from factories, the operating rates were depressed amid widespread covid-19, while the sluggish downstream demand, featuring fewer-than-expected export orders during the Christmas holiday, also dampened the production willingness. Currently, the downstream enterprises mostly stand on the sidelines, and the bids from steel mills have missed the expectations. It is thus anticipated that the magnesium powder output in January will continue to stay low at 6,000 mt.

PrNd oxide

Domestic output of PrNd oxide in December was 5,134 mt, down 11% month-on-month. Output declines were seen in Fujian, Guangdong, Guangxi, Jiangxi, Jiangsu and Guangdong.

In December, as many separation plants and scrape recyclers reduced or halted the production, the shortage of PrNd oxide in the rare earth market festered. Goods holders quoted high while low-priced resources were rare. As a result, the PrNd oxide prices continue to go up. Towards the end of the year, the enterprises across the country started to overtake overhauls or shakedown tests. As a result, the output in Jiangxi and Jiangsu shrank sharply in December by 14% and 56% respectively from the previous month. Yet, most enterprises have resumed their production to date, and plan to maintain normal production during the CNY holiday. It is expected that the output of PrNd oxide will rise in January 2023.

PrNd alloy

Domestic output of PrNd alloy in December 2022 stood at 5,134 mt, up 0.1% month-on-month. The increase in output mainly came from Sichuan, with little change in other regions.

The PrNd alloy prices slightly rose in December, but the growth of orders from magnetic material enterprises slowed down with the upcoming year-end. Therefore, the trades of PrNd alloy were muted. The metal factories also suffered huge losses in addition to a lack of raw material supply. The PrNd alloy production in Fujian was cut for this reason. In Sichuan, the high PrNd alloy prices promoted local metal plants to ramp up the production by about 10% on the month, since it was still lucrative to produce using raw material stocks.

Molybdenum concentrate

SMM data shows that molybdenum concentrate output in December 2022 was 18,800 mt, a drop of 1.7% from November.

There are two main reasons for the slight decrease. First, some areas were racked by the aggravating covid-19 pandemic, where the operating rates were slightly down due to a growing number of sick workers, thus restricting the output of molybdenum concentrate. Second, a small number of private enterprises in south China carried out maintenance ahead of schedule with their annual production targets completed. But, thankfully, their small proportion of the total output did not led to a significant decline in the molybdenum concentrate supply in the market.

In January, some mines have decided to lower their operating rates for annual maintenance. SMM thus predicts that the output of molybdenum concentrate in January may continue to decrease.

Ferromolybdenum

The domestic ferromolybdenum output in December was 17,600 mt, a decline of 3.2% from the previous month, according to SMM statistics.

To explain the decline in ferromolybdenum output, there are some aspects for reference. First, the relaxation of covid-19 control measures resulted in a surge in infected workers, which weighed on the operating rates of ferromolybdenum plants and limited the output. Second, the domestic molybdenum mines, who were bullish on molybdenum prices, held back from selling, and traders were also reluctant to sell. Therefore, the molybdenum supply in the market was limited, which failed to meet the demand from ferromolybdenum producers. Third, ferromolybdenum enterprises refrained from purchasing imported raw materials when the molybdenum prices overseas soared. Under these circumstances, ferromolybdenum output edged down.

In January, the demand for ferromolybdenum from steel mills has increased steadily, but steel mills were still discouraged by the high molybdenum prices with further upward potential. Therefore, they mainly purchased on rigid need. On the other hand, the tight supply of raw materials also continued to pressure the production of ferromolybdenum. As such, the output of ferromolybdenum may continue to decline in January.

Silver

According to SMM survey, domestic silver output stood at 1,414.82 mt (including 1,191.82 mt of mineral silver) in the final month of 2022, up 3.2% on the month. In fact, the silver output rose following the increase in copper and lead output. Apart from this, the high silver prices in December also motivated the silver smelters to produce, and some plants were still in a rush to meet their production targets at the end of the year. Some silver smelters saw decrease in their output for reasons like maintenance and sluggish production willingness on completion of annual production targets. In general, the increase in output outweighed the decline, so the silver output showed an upward trend in December. It is expected that some silver smelters will have a holiday for the upcoming Chinese New Year, thus SMM estimates that silver production will shrink slightly in January.

On the macro front: The Federal Reserve released its meeting minutes that tilted towards the hawkish side. The ADP employment data in the United States added 235,000 in December, higher than the previous print of 127,000 and the estimate of 150,000. Silver prices were thus suppressed. The initial jobless claims in the United States during the week ended December 31 stood at 204,000, which was lower than the previous print and the forecast of 225,000, and thus negative for silver prices. The weak economic data economic and hawkish minutes of the Federal Reserve meeting subdued the upside room for silver prices, and the prices went down as a result.

Antimony ingot

According to SMM survey, China’s antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in December 2022 was 7,489.5 mt, up 7.28% month-on-month. The output in December maintained an upward trend but with a slowdown in the growth rate compared with the significant increase of 27.92% in November output. On the one hand, it has something to with the fact that many manufacturers had to reduce their production on a shortage of raw materials and more workers on the break at the end of the year. On the other hand, some producers were resuming their production but at a slow pace. Taken together, the overall production of antimony ingots in China continued to advance in December but with an obvious slowdown in growth. At present, the shortage of antimony has extend, and market participants said that that persisting influence of tight raw materials was having less impacts on the market sentiment. That also explained why antimony prices did not see wild swings in 2022. However, it seems that both domestic and overseas supply of antimony ore will not advance in the foreseeable future, which will provide a solid support for a steady increase in antimony prices.

Among the 32 respondents in SMM survey in December, 10 manufacturers stopped the production, down by 4 from the previous month; 16 reduced their production, up by 5; and 6 maintained normal production, one fewer than in November. These figures tell that the production has been increasingly concentrated. SMM predicts that the supply-demand structure of the domestic antimony market in January 2023 will not be overturned under the current economic situation. Although the sluggish demand is more than likely to extend, the tight supply will also continue. The national antimony ingot output in January is anticipated to increase slightly on a monthly basis.

Refined bismuth

According to SMM survey, the domestic output of refined bismuth in December, 2022 fell 1.83% month-on-month to 2,621.66 mt. On the whole, only a small number of refined bismuth manufacturers were shut down while a considerable cut their production. The production cuts were in part owed to the covid-19 pandemic, but generally speaking, the impact of the covid-19 on refined bismuth output was insignificant. Among the 23 survey respondents, three manufacturers halted the production in December, and five slashed their output on a monthly basis. However, four manufacturers increased their output in December significantly compared with that in November. Therefore, the total output reduction of refined bismuth nationwide was small. SMM predicts that the supply and demand of the domestic refined bismuth will not change much in January, 2023. On the bright side, the relaxation of covid-19 control measure is expected to greatly stimulate the recovery of the consumer market, and the thin trades caused by weak demand will be improved. At the same time, as the Chinese New Year approaches, many manufacturers will step up the production, thus the refined bismuth output in January will not be cut too much due to the holiday break. When the supply is still large, it is unlikely for refined bismuth prices to pivot and rise. However, there is also little downward room for the prices with upbeat sentiment on the recovery of future demand, In addition, it is also difficult to say for sure that the manufacturers that have suspended or cut the production will resume normal production in January. In conclusion, SMM expects that the national production of refined bismuth in January is inclined to continue falling slightly, though the change will be little.

Notes: SMM has released Chinese refined bismuth output since October 2022. Thanks to its high coverage of the refined bismuth industry, SMM has successfully investigated a total of 23 refined bismuth manufacturers, which are located in 8 provinces across the country, with a total capacity over 50,000 mt and a total capacity coverage rate over 99%.

Silver nitrate

The domestic silver nitrate plants with sales qualification certificates together produced 625 mt of silver nitrate in December, up 6.3% from a month earlier. The total output of silver nitrate nationwide reached 658 mt in the final month of 2022. Reasons for the increase include the growing restocking demand among downstream enterprises before the holiday and the new orders from new consumers, while the decrease in the output is largely attributed to the overhauls. Generally, the increase in output outnumbered the decrease.

As the downstream companies still plan to maintain production during the upcoming Chinese New Year holiday, the stocking demand has been still high. At the same time, some companies who decide to take early holidays also need to stock up in advance. Therefore, SMM expects that the demand for silver nitrate will still increase in January.

Titanium dioxide

SMM data shows that China's titanium dioxide output stood at 280,000 mt in December 2022, down 9% from the previous month and 8% from the previous year. The combined output in 2022 increased 2% year-on-year to 3.81 million mt.

According to SMM research, most titanium dioxide enterprises faced huge pressure in December amid the end market downturn and the rampant covid-19. Some enterprises in south China and south-west China had to cut their production, and the average operating rate of titanium dioxide producers fell. Since the operating rates of the terminal construction sector will remain low in the midst of weak economic environment both at home and abroad, the titanium dioxide producers will continue to face mounting pressure brought by accumulating inventories. In this context, the production expansion will be unlikely, and the titanium dioxide output in January is expected to remain low at 280,000 mt.

APT

The domestic APT output in December was 11,900 mt, a decline of 5% on a monthly basis, according to SMM statistics.

The reduction in APT output was mainly affected by the following factors. First, the spread of the covid-19 slightly dragged down the operating rates of APT smelters, hence the APT output was cut. Second, downstream enterprises mainly stocked as needed due to the sluggish end demand in the recent quarter. The weak demand and strong supply promoted some smelters to be closed for maintenance in December, which was also the main reason for the decrease in the total output of APT. Thirdly, as mines and goods holders held their prices firm whiling holding back from selling, the available tungsten concentrates in the spot market was limited. The low-priced goods were scarce while high-priced cargoes would bring about losses. In this scenario, APT smelters resorted to production cuts, and mainly focused on the delivery of long-term orders. Altogether, the output of APT decreased in December.

In January, the production at smelters has still been upset by the tight supply of raw materials and lower profits. Moreover, the unwillingness of downstream enterprises to stock in the year-end seems to further weigh on the operating rates of smelters. SMM thus expects that APT production will continue to move down in January.

Lithium carbonate

China’s lithium carbonate output was 34,813 mt in December, a month-on-month decrease of 5% but a year-on-year increase of 76%. In December, some enterprises resumed their production from the impacts of covid-19 and the production capacity of some large factories climbed up. This, coupled with the increase in recycling, contributed to an increase in lithium carbonate production. However, the output from salt lake was on the decline during cold winter, and some lepidolite-based smelters in Jiangxi either reduced the production or carried out overhauls in accordance with the environmental protection-related requirements. As a whole, the total supply in December diminished. In January, the enterprises affected by environmental protection-related production restriction has gradually recovered the production, but most spodumene-based smelters intend to slash the output with maintenance plans. As such, the lithium carbonate output is estimated to drop 6% MoM and gain 71% YoY to 32,587 mt in January.

Lithium hydroxide

China’s lithium hydroxide output was 25,246 mt in December, a year-on-year increase of 47%. On the one hand, some smelters ramped up the production thanks to the eased shortage of ore and the weakened impacts of covid-19. On the other hand, causticising plants cut the production when faced with falling downstream demand. Therefore, the total supply ended up with a slightly MoM increase in December. In January, some new factories began to increase their output, while some other plants carried out maintenance. However, causticising plants continued to reduce the output sharply amid softer demand. In this case, China's lithium hydroxide production in January is estimated to be 21,385 mt, a decrease of 15% month-on-month and an increase of 32% year-on-year.

Cobalt sulphate

China’s cobalt sulphate output was 6,908 mt in metal content in December, down 6% from a month earlier but up 23% from the prior year. On the cost side, the falling prices of cobalt-based raw materials overseas in December lowered the cost of cobalt intermediate products. At the same time, the trades of scraps were subdued by the decline in salt prices, which prompted its prices to restore rationality accompanied with lower costs. On the supply side, a sharp decrease in the output of domestic battery factories affected the orders for cobalt salts and precursors. In response, large integrated precursor plants and leading cobalt salt smelters lowered their production, leading to reduced supply. On the demand side, the demand for ternary batteries slumped with the removal of domestic new energy vehicle subsidies. The 5 and 6-series batteries, the majority of ternary batteries in China, had high demand for cobalt as raw materials for their precursor production. Therefore, the reduction in ternary batteries finally translated into lower demand for cobalt. The demand for high-grade nickel precursor maintained upward momentum with growing export orders, but gave limited boost to cobalt salt demand. In January, the demand for cobalt sulphate has been sluggish with upcoming holiday, and cobalt salt companies have displayed low production willingness while gearing up for the holiday. Therefore, SMM predicts that China’s cobalt sulphate output will contract 17% MoM and 24% YoY to 5,735 mt in mental content in January.

Tricobalt tetraoxide (Co3O4)

The output of domestic Co3O4 stood at 4,985 mt in December, down 11% MoM and 32% YoY. The downward price trend of cobalt intermediate products and cobalt-based raw materials was transmitted to lower costs of Co3O4. However, the orders for Co3O4 remained lacklustre and the production was disturbed by the surging covid-19 infections at the end of the year. Thus, the Co3O4 output in December edged lower. The top-tier Co3O4 factories strived to reduce their production and cleared their inventory by lowering the prices, while small plants mostly produced to deliver orders on hand. Altogether, the output went down. On the other hand, the demand for Co3O4 continued to weaken in December. In detail, the demand from the electronics sector was slack, while e-cigarette producers were already closed for holiday since early December. Therefore, the transactions of Co3O4 were rather muted. In order to avoid the risk of falling prices and orders, LCO cathode material plants were not willing to stock Co3O4. The poor demand for Co3O4 was no longer striking news. It is expected that the output of Co3O4 will further decline in January with manufacturers closed for holiday or cutting the production. The forecast for Co3O4 output in January is 4,117 mt, down 17% MoM and 46% YoY.

Ternary cathode precursor

The domestic ternary cathode precursor output was 76,444 mt in December, a month-on-month decrease of 15% and a year-on-year increase of 28%. The combined output in 2022 advanced 45% from 2021. The removal of NEV subsidies and the end of the rush to install batteries in the year-end resulted in a collapse in the output of domestic leading battery factories. Subsequently, the orders for ternary precursors also dipped sharply. The export orders were stable, but made no difference in production willingness due to its small proportion. The majority of domestic precursors, namely the 5 and 6-series precursors, dropped steeply in terms of proportion in the total output. Overseas orders were dominated by high-grade nickel precursors, and its proportion rose slightly. It is expected that the Chinese New Year holiday in January and the continued weakening of downstream orders will further limit the output of precursors in January. The output in January is expected to be 67,291 mt, a decrease of 12% on a monthly basis and an increase of 10% year-on-year.

Ternary cathode materials

The domestic ternary cathode material output was 53,146 mt in December, a month-on-month decrease of 20% and a year-on-year increase of 12%. The year-end rush of battery installation has come to an end, marking the start of an off-season in the terminal consumption. The demand in electronics and e-bike sectors also weakened, and some battery enterprises had to clear their inventory in the year-end. Under these circumstances, the overall demand for terminal cathode materials retreated significantly. Overseas orders only fell slightly as foreign enterprises stockpiled in advance upon the upcoming holidays for Chinese plants. On the whole, the average operating rate of ternary material producers slid palpably. In January, demand at home and abroad still faces downward pressure. Some small and medium-sized enterprises plan to close and the large ones also decide to halt the production for maintenance. In this scenario, the operating rates are likely to further dip. The domestic ternary cathode material output is anticipated to be 42,794 mt in January, down 19% on the month and down 7% from the previous year.

Iron phosphate

China produced 81,020 mt of iron phosphate in December, down 14% on a monthly basis. The production of most iron phosphate enterprises was cut in view of several adverse factors. First, the demand from downstream enterprises decreased significantly in December, which was reflected in fewer orders and smaller size of purchase. Next, although the prices of phosphorus source, the main raw materials, still stood, multiple battery cell makers and LFP plants forced down the bid prices of iron phosphate. As a result, iron phosphate sellers usually had to lower the prices to promote the sales. At the same time, some enterprises, for a fear of falling demand and stock devaluation, actively reduced their production, resulting in a month-on-month decline in the output. On the demand side, the prices of lithium salt dropped significantly in December. The strong wait-and-see sentiment among LFP enterprises when faced with extremely weak terminal demand will probably precipitate thin trades in January. Since the demand is certain to decline in the short term, some iron phosphate enterprises decide to take holidays in January, hence the output in the future will be lower. It is estimated that the iron phosphate output in January will slide 24% on the month to 61,520 mt.

LFP

China produced 100,804 mt of LFP materials in December, a decrease of 16% month-on-month and an increase of 63% year-on-year. On the supply side, some LFP enterprises cut the production in response to falling demand from battery cell factories and the rapid decline in lithium salt prices. Meanwhile, the downstream demand was on a downward path when auto makers and battery cell producers focused on destocking. However, LFP enterprises generally stood wait-and-see as they held bearish outlook for lithium salt prices and iron phosphate prices. Therefore, the purchases were thin. The weak demand in the market and falling prices of raw materials together suppressed the production willingness of LFP manufacturers. It is reported that some enterprises will be closed for maintenance in January. It is expected that the production cuts will further expand, so the LFP output is forecast to be 80,402 mt in January 2023, a decrease of 20% month-on-month and an increase of 29% year-on-year.

LCO

Domestic LCO cathode material output was 5,750 mt in December, down 20% on the month and 27% on a yearly basis. Following the downward trend of Co3O4 prices, the prices of lithium carbonate in December saw a sharper decline, and thus lowering the costs of LCO. On the supply side, the operating rates of LCO enterprises trended lower amid sluggish demand from digital electronics sector and under the impact of relaxed covid-19 control measures. In general, LCO enterprises cut their production in December and endeavoured to destock by lowering the prices. On the demand side, some LCO battery cell factories focused on consuming the stocks in December, and some small factories already closed for holidays. As a result, the trades of LCO in the spot market were quiet, and weak demand persisted. In January, battery cell factories will stop the production and take the Chinese New Year holidays since the middle of the month. At the same time, the electronics market is expected to remain sluggish in early 2023, and LCO enterprises will not be enthusiastic about production. As such, the LCO output in January is likely to see a considerable decline. SMM predicts that China’s LCO output will fall 20% MoM and 40% YoY to 4,571 mt in January.

LMO

China’s LMO output stood at 6,799 mt in December, 2022, down 24% from the previous month and up 7% on the year. At the end of the year when covid-19 control was lifted, a large number of workers were infected with the disease, which hampered the production and caused the output to slip. In the meantime, the demand from battery cell factories dropped sharply, and the purchases on rigid demand was also scarce. For this reason, most LMO enterprises maintained their operation at low capacity. The prices of lithium carbonate continued to fall, and LMO companies, bearish on its future prices, mainly focused on consuming their inventories in January. According to SMM research, large LMO plants will be shut down for 10-15 days for maintenance, and small and medium-sized enterprises will be closed longer, whose production will not resume until February. The domestic LMO output is forecast at 2,546 mt in January, down 63% MoM and 55% YoY.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)