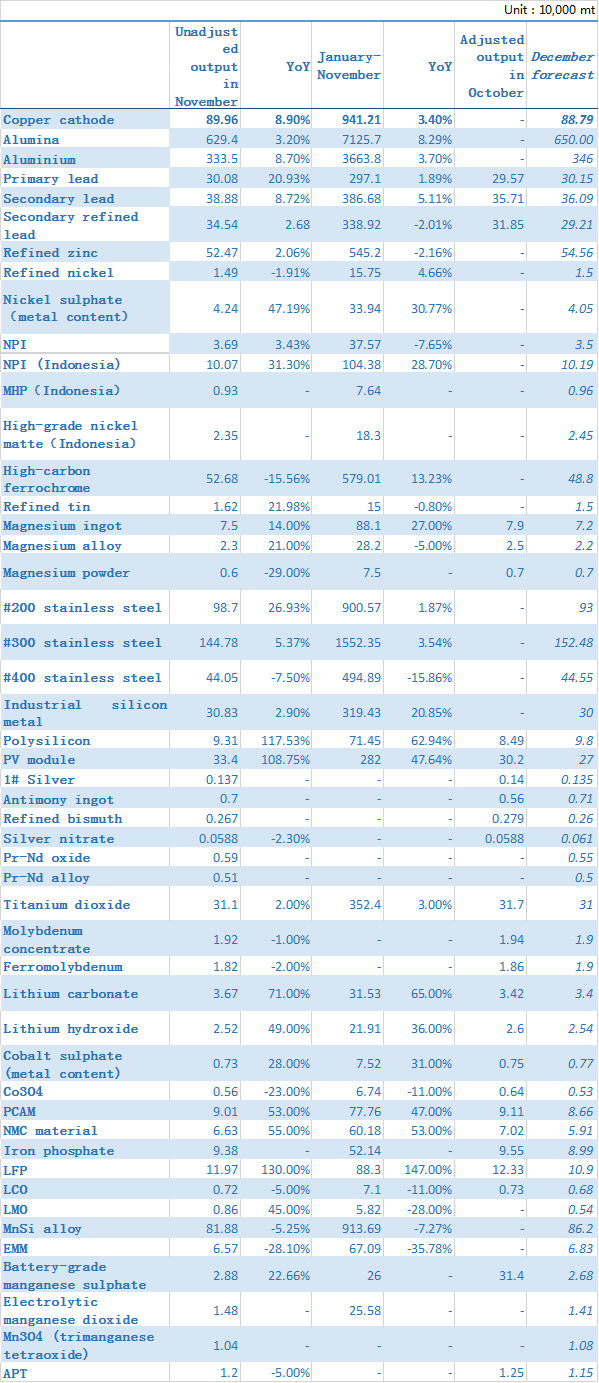

Copper cathode

China produced 899,600 mt of copper cathode in November, down 0.2% MoM but up 8.9% YoY. The output was 3,700 mt lower than the expectation of 903,300 mt. The output totalled 9.41 million mt from January to November, up 3.37% or 306,500 mt year-on-year.

1. A smelter in east China undertook maintenance ahead of time due to equipment failure and there were six smelters overhauled in November. 2. The shortage of crude copper and blister copper also restricted the increase of output. 3. The new production capacity of two projects in central and south China was released at the end of November, hence the contribution to the output increase was very limited.

In December, although the new production capacity of two smelters projects has been put into production, the output increment is not significant. The total output increase of the two smelters is about 10,000 mt. According to SMM statistics, five smelters will be overhauled in December. Three of which started the maintenance at the end of November, but the impact on output is reflected in December. Another smelter will stop the production for a long time due to the relocation, with a total output decline about 40,000 mt. In addition, the tight supply of crude copper and blister copper has not been resolved, which will still restrict the increase of output. Due to the unfavourable news, the smelters does not increase the output at the end of 2022 and the output even continues to decline. China copper cathode output is estimated at 887,900 mt in December, down 11,700 mt or 1.3% MoM but up 2% YoY based on the current production schedules. The output may reach 10.3 million mt from January to December, up 3.2% or 324,100 mt year-on-year.

Alumina

Domestic metallurgical-grade alumina output in November (30 calendar days) was 6.29 million mt with an average daily output of 209,800 mt, down 5.7% or 5,600 mt on the month but up 3.2% on the year. The production capacity of alumina was 76.6 million mt and the domestic operating rates stood at 79%. The output totalled 71.26 million mt from January to November 2022, an increase of 8.29% on the year. On the whole, it is estimated that the net imports of alumina in November will be 150,000 mt. And there will be a slight surplus of 24,000 mt in the month, and the surplus of about 1.74 million mt during January-November. The output in November decreased compared with that in October. On the one hand, the production days in November decreased by one day compared with that in October. On the other hand, the enterprises continued to reduce the production. In the northern region, affected by the pandemic and poor transportation in Shanxi and Henan in the first ten days of November, the operating rates of alumina plants in Shanxi and Henan were low, hence the output did not increase. In late November, Shanxi and Shandong issued a severe pollution weather warning. Therefore, the roasting process of alumina plants in the two provinces was suspended for nearly a week, which also led to the decline in output. In south-west China, a large-sized alumina plant in Guangxi stopped the production for nearly a week due to equipment failure at the end of November, hence the output fell by nearly 40,000 mt. Due to the low alumina prices in November, some enterprises in Guizhou reduced their production due to poor profits. On the whole, although the output in November declined significantly compared with the previous year, the supply surplus is unlikely to improve in 2022. The new production capacity in Shandong will be released intensively in December. It is expected that the output in December (31 calendar days) will increase to about 6.5 million mt, up 3% year on year.

Aluminium

China produced around 3.34 million mt aluminium in November, up 8.7% YoY. The daily output rose 1,055 mt MoM to 111,200 mt. The output totalled 36.64 million mt from January to November, an increase of 3.7% on the year. In November, the aluminium output saw both increase and decrease, but the output increase was more significant as the operating capacity continued to increase amid the production resumption of aluminium plants in Guangxi and Sichuan. 230,000 mt of capacity was resumed in Guangxi. And the capacity in Sichuan increased 140,000 mt MoM to 500,000 mt. The output of the two provinces increased steadily. In addition, the new production capacity of Inner Mongolia Baiyinhua was slow released in November, and its operating capacity increased to 150,000 mt in November. Other production capacity was still in production. Phase II of Gansu Zhongrui’s project was put into production by the end of November, and there was no output within the month. However, due to the heating season, some enterprises in Henan and Shanxi reduced the production slightly, with a total output decline of about 120,000 mt. Smelters in other regions produced normally. According to SMM statistics, by the beginning of December, domestic aluminium production capacity reached 45.26 million mt (including the production capacity that has been built but not put into production). The domestic aluminium operating capacity was 40.59 million mt, and the national aluminium operating rates were about 89.7%. In November, the shipment of aluminium rods and other primary processed products was sluggish. Meanwhile, the processing costs declined, hence some aluminium processing enterprises reduced the production. The proportion of aluminium liquid fell 0.59% month on month to 69.16%.

In December, some enterprises in Sichuan and Guangxi resumed the production. However, due to the power shortage in Sichuan and the high costs in Guangxi, SMM estimates that the production resumption in these regions would slow down in December. In addition, the new production capacity of Inner Mongolia Baiyinhua, Phase II of Zhongrui’s project in Gansu and Guizhou is released slightly, hence the domestic aluminium operating capacity will continue to increase in December. According to the capacity changes, the domestic operating capacity of aluminium at the end of December may increase slightly to about 40.89 million mt. Domestic aluminium output is expected to increase 9% YoY to 3.46 million mt in December (31 calendar days). On the demand side, in November, downstream consumption was poor. Central and south China were affected by the pandemic, and the downstream operating rates were lower than expected. Meanwhile, amid the coming winter in north China, the terminal construction demand weakened. As such, the demand for aluminium extruders and aluminium plates weakened. The total inventory of domestic aluminium inventory dropped to the new low in November. Up to now, the total inventory was about 507,000 mt, a decrease of 472,000 mt compared with the same period last year. However, the shipment in November was lower than that in last year. SMM believed that the current domestic low inventory was caused by many reasons, such as the high costs of transportation, high aluminium liquid proportion and the increase of shipment to terminal enterprises. In December, the domestic pandemic prevention policy will be relaxed, and the transportation may continue to improve. In addition, the operating rates of downstream enterprises may decline. Amid the seasonal low of aluminium ingot in December, SMM expects that the social inventory of aluminium ingot will increase to near 600,000 mt in December. But the social inventory will still be low.

Primary lead

China produced 300,800 mt of refined lead in November, up 1.72% MoM, and up 20.93% from YoY. The combined output in January-November increased 1.89% on the year. Production capacities of enterprises involved in the survey totalled 5.71 million mt in 2022.

According to research, the output of refined lead increased as expected in November. As the pandemic in Yunnan and Inner Mongolia was eased, local smelters resumed the production. At the same time, the new production lines of Henan Yuguang and Zhongjin Lingnan reached full capacity, which led to some output increase. However, Yunnan Mengzi was still in maintenance. And some enterprises did not increase the production and the output declined slightly from the previous month as they have completed the annual production and sales target. Therefore, the overall output of refined lead only increased slightly.

In December, the domestic pandemic prevention and control policy will be further optimised, but some smelters in Hunan still slightly reduce the production due to the pandemic. In addition, amid the end of the year, most companies will not increase the production in December as they have completed their annual production and sales targets. Therefore, the output will continue to decline slightly. On the other hand, Yunnan Mengzi will complete the maintenance and the output will gradually resume to normal. On the whole, SMM predicts that the domestic output of refined lead will remain at 300,000 mt in December.

Secondary lead

SMM data showed that China produced 388,800 mt of secondary lead in November, up 8.88% MoM and 8.72% YoY. For January-November, the combined output surged 5.11% from the same period last year to 3.87 million mt. China produced 345,400 mt of secondary refined lead in November, up 8.45% MoM and 2.68% YoY. For January-November, the combined output fell 2.01% from the same period last year to 3.39 million mt.

In November, both domestic secondary lead and secondary refined lead output increased sharply month-on-month. Due to the increase in domestic lead prices in November, the secondary lead smelters were active in production amid the high profits. AS such, the output of domestic secondary lead and secondary refined lead increased. The secondary lead smelters in Anhui, Jiangxi and Jiangsu contributed most of the output increase in November. Among them, Anhui Dahua resumed the production at the end of October after maintenance. The enterprise reached full production in the first ten days of November and produced stably. Jiangxi Jinyang also resumed the production in November. Jiangsu Shuangdeng Tianpeng increased the production in November, which also brought about an increase in the output. The secondary refined lead output of these three enterprises increased about 33,000 mt in November. At the same time, many other smelters increased the production due to the rise in lead prices in November.

The purchasing prices of battery scrap offered by domestic secondary lead smelters also gradually increased amid the increasing demand. In December, domestic battery scrap prices rise sharply, and many secondary lead smelters indicate that their costs increase and the profits narrow. Some secondary lead smelters in Inner Mongolia gradually reduce the production due to the difficulty in purchasing battery scrap and the delay in transportation. Meanwhile, due to the routine maintenance of the Zhejiang Tianneng, the enterprise stopped the production since December 4. Some secondary lead smelters in Yichun and Jiangxi also stopped the production due to the abnormal proportion of thallium in the drinking water source of the main stream of the Jinjiang River. It is estimated that the domestic output of secondary lead in December will decrease to 360,900 mt, and the output of secondary refined lead will decrease to 292,100 mt.

Refined zinc

China's refined zinc output stood at 524,700 mt in November, up 10,600 mt or 2.06% MoM and 5,200 mt or 0.99% YoY. The output of some neterprises exceeded the expectations. From January to November 2022, the combined refined zinc output stood at 5.45 million mt, a decrease of 2.16% year-on-year.

The domestic refined zinc output in November was higher than that in October as the output of some smelters exceeded the expectations. The output of smelters in Yunnan, Inner Mongolia, Hunan and Xinjiang exceeded the expectations after resumed the production. A large-sized smelter in Guangdpng resumed its production after maintenance, hence its output increased. A smelter in Shaanxi raised its production and the output increased slightly. However, the output of smelters in Sichuan declined significantly in November due to the impact of environmental protection. Meanwhile, affected by the pandemic in Qinghai, smelters stopped the production.

China refined zinc output is expected to be 545,600 mt in December, up 20,900 mt on the month and 6.29% or 32,300 mt on the year. From January to December 2022, the combined refined zinc output is estimated to be 5.998 million mt, a decrease of 1.45% year on year. As the smelters in Sichuan have resumed normal production, the output may increase. Meanwhile, some smelters in Shaanxi and Xinjiang further increase the production. Some smelters in Jiangxi have plans to increase the production at the end of the year. As the impact of the pandemic gradually eases, some smelters in Qinghai will resume normal production. However, some smelters in Yunnan reduce their production slightly due to the pandemic, and may resume the production in the middle of December.

According to SMM research, most smelters will maintain normal production during the Chinese New Year in January, and only some secondary zinc smelter plan to take the holiday and stop the production.

Refined tin

Domestic refined tin output was 16,200 mt in November, down 3.26% MoM and up 21.98% YoY, and the combined output from January to November fell by 0.8% YoY, according to SMM research. The actual domestic refined tin output in November was slightly better than expected.

The slight drop in the output of refined tin in November was mainly caused by the shortage of raw materials. In terms of regions, the output of smelters in Yunnan decreased slightly from the previous month. The tight raw material supply and low TCs squeezed the profits of smelters. The actual production of smelters in Yunnan was different, and the output of smelters with higher production capacity declined more significant. The production of other refineries was stable. Although some smelters slightly increased the production, the gap of production reduction was not filled. The output of smelters in Guangxi fell on the month. Due to the shortage of raw materials and the elimination of periodic favourable policy, the smelters in Guangxi reduced the production. In December, the raw material shortage extends, and the regional output may fall further. 3. The output of smelters in Jiangxi stabilised. The mainstream smelters in the region produced normally. According to SMM research, due to the poor shipment, the inventory of smelters increased. The equipment maintenance also affects the production forecast in Jiangxi in December. The total output of smelters in other regions continued to increase in November. Some smelters in south China stopped the production for maintenance while other smelters produced stably. A few smelters produced intensively, which made up for the impact of maintenance.

In December, the tight raw material supply and the drop in TCs may further squeeze the profits of smelters. On the other hand, amid the continued rise in tin prices, downstream enterprises are in fear of further price increase. Therefore, the market demand is suppressed, and the spot market weakens. Some domestic smelters have lowered their expected output. In summary, SMM expects that the domestic refined tin output will fall significantly in December to 15,040 mt.

Refined nickel

China produced 14,900 mt of refined nickel in November, down 3.11% on the month and 1.91% on the year. During November, the domestic pandemic eased and the transportation of various smelters returned to normal. However, according to SMM research, a domestic refined nickel plant in north-west China stopped the production due to the maintenance, and is expected to resume normal production in 15-30 days. The output may fall by about 500-1,000 mt. The affected output accounts for 3.23%-6.45% of China's total refined nickel output, hence this overhaul has little impact on the supply of domestic refined nickel.

It is expected that the domestic refined nickel output will stand at 15,000 mt in December, up 0.47% on the month but down 0.08% on the year. The output of refined nickel in December will change little from that in November, mainly because the smelters in north-west China is expected to produce normally in mid-December.

NPI

In November 2022, NPI output in China was 37,000 mt in Ni content, up 3.43% from the previous month and 14.64% from the same period last year. In November, the prices of NPI remained firm amid the support of high ore prices. At the same time, the spot prices of stainless steel fell sharply in November, and the orders of stainless steel also declined compared with October. Coupled with the high NPI prices, steel mills suffered losses. In the first ten days of November, the supply and demand sides were in stalemate for a long time. However, as the hidden inventory flew into the market, the supply was in surplus. The output of high-grade NPI in November was about 29,600 mt in Ni content, a month-on-month increase of 5.21%. As the production of Indonesia NPI of an integrated enterprises decreased significantly, their domestic NPI output increased accordingly. Another integrated enterprise increased their NPI output for its stainless steel production. Due to the poor downstream demand, the rest of the NPI plants undertook maintenance and reduced the production to varying degrees. The output of low-grade NPI was 7,300 mt in Ni content, a month-on-month decrease of 3.21%. As the profits of 200-series stainless steel in October were slightly higher than that of 300-series, the steel mills were more active in the production of 200-series stainless steel. As such, the output of low-grade NPI in October increased amid the strong demand. In November, the inventory of 200-series stainless steel gradually increased, hence the output of low-grade NPI fell slightly.

It is estimated that the domestic NPI output in December will decline 5.64% from October to around 35,100 mt in Ni content. In December, due to the sluggish terminal demand, the NPI output may decline. Meanwhile, stainless steel plants are expected to reduce the production. Amid the slight surplus of NPI and the strong ore prices, NPI plants are in losses. Therefore, some NPI plants choose to reduce the production and undertake maintenance in advance.

Indonesia NPI

Indonesia NPI output stood at 100,700 mt in nickel content in November, a month-on-month decrease of 4.7% and year-on-year increase of 31.3%. Indonesia high-grade NPI output totalled 1.04 million mt in Ni content in January to November. In October, there were two new production lines were built in Qingshan Small K Industrial Park and there were no newly-added production line in other plants. At the same time, due to the poor stainless steel market, stainless steel production lines in Indonesia also reduced the production, which affected the output of NPI to a certain extent. Coupled with the overhaul of some production lines in Indonesian NPI factories, the overall output of Indonesia NPI in November fell. The high-grade nickel matte output release of Huake project in Indonesia gradually will affect the supply of NPI in the future. Indonesia NPI output is expected to recover in December, but the increase will be limited. The poor stainless steel market may still restrict the production of NPI factories. At the same time, the production of high-grade nickel matte will occupy the NPI production lines.

Nickel sulphate

China nickel sulphate output in November stood at 42,400 mt in metal content and 192,700 mt in physical content, up 3.83% on the month and 47.19% on the year. In November, China's nickel sulphate output rose slightly as the production lines of some nickel salt plants increased the production as expectation and a large-sized integrated manufacturers resumed the production form maintenance. In November, the consumption of high-grade nickel matte accounted for 27%, MHP accounted for 45%, nickel briquette and nickel powder only accounted for 7% due to poor cost efficiency, and the nickel scrap and crude nickel accounted for 21%. In December, as the demand for nickel sulphate from ternary manufacturers declines and the nickel salt manufacturers have no new production lines, some nickel sulphate companies may reduce the production due to poor orders. The nickel sulphate output in December will fall 4.53% month-on-month to 40,500 mt in metal content.

Battery-grade manganese sulphate

In November, China’s high purity manganese sulphate output stood at 28,800 mt, down 8.28% on the month. According to SMM research, the delivery of long-term orders of mainstream manganese salt factories in the second half of November was lower than expected. Due to the poor demand of new energy vehicles, battery factories and ternary cathode material companies generally held a bearish outlook towards the market. Therefore, the output of precursor factories declined slightly in the November. In addition, as the downstream enterprises already finished the stockpiling of raw materials in October, the demand for manganese sulphate from precursor factories was suppressed. The operating rates of many manganese sulphate plants were about 50%, and the inventory continued to decline.

In December, the battery and ternary cathode material factories will clear out the finished product inventory at the end of the year, hence the production will decline further. According to SMM, the precursor factories will also reduce the production accordingly. Among them, the output of 5 and 6-series will decline significantly while that of 8-series will remain stable due to the strong overseas demand. On the whole, the demand for manganese sulphate will weaken further in December, and the manganese salt plants are pessimistic about the market outlook. It is expected that the actual output in December will be 26,800 mt in physical content.

Electrolytic manganese dioxide

In November 2022, China's electrolytic manganese dioxide output was 14,800 mt (including 1,500 mt for LMO battery, 9,500 mt for alkaline manganese battery, and 3,700 mt for alkaline zinc battery), a month-on-month increase of 5.71%. The output of the electrolytic manganese dioxide for alkaline manganese battery increased more significantly as the overseas demand increased amid the Thanksgiving. As such, the operating rates increased, and the output increased month-on-month. In addition, electrolytic manganese dioxide (for LMO battery) was less cost-effective than trimanganese tetraoxide, hence the market of electrolytic manganese dioxide was further squeezed. The demand for electrolytic manganese dioxide was weak, and the output decreased slightly from the previous month.

In December, the downstream demand for LMO battery is weak and the operating rates decline, hence the demand for electrolytic manganese dioxide (for LMO battery) further weakens. The enterprises mainly deliver in the form of long-term orders and the output is unlikely to increase. At the same time, the demand of electrolytic manganese dioxide (for alkaline manganese battery) will also return to rationality As such, the total output is expected to decline slightly to about 14,100 mt.

Mn3O4 (trimanganese tetraoxide)

In November 2022, China's Mn3O4 output was 10,400 mt (including 4,300 mt of electronics-grade Mn3O4 and 6,100 mt of battery-grade Mn3O4), a month-on-month increase of 0.97%. In November, the output of Mn3O4 increased slightly. On the one hand, the battery-grade Mn3O4 further squeezed the market of manganese dioxide during the month. On the other hand, as the battery-grade Mn3O4 was more cost-effective than manganese dioxide, the demand for Mn3O4 from sodium battery and lithium iron manganese phosphate enterprises was stronger. At the same time, the current production capacity of Mn3O4 was limited, and the manganese plants basically reached full capacity at this stage, hence the output increase was limited.

In December, the demand from LMO enterprises declines and the demand for battery-grade Mn3O4 may weaken. However, due to the orders in the next year, the insufficient market supply and the release of new capacity of some manganese plants in December, the output may still increase slightly to 10,800 mt in December.

High-carbon ferrochrome

According to statistics, the output of high-carbon ferrochrome stood at 526,800 mt in November, up 80,100 mt or 17.93% from the previous month but down 97,100 mt or 15.56% on the year. The output in Inner Mongolia was 305,700 mt, up 30,000 mt or 10.88% MoM, and that in Guizhou stood at 47,600 mt, up 53.55% MoM. In November, the purchasing prices offered by the mainstream steel mills rose sharply. As ferrochrome plants suspended the production due to the losses in the early stage, they still had enough raw material inventory. In addition, as the low-priced chrome ore arrived at ports in November, the costs declined and the profits of ferrochrome plants were restored. As such, the ferrochrome plants resumed the production actively.

In December, the output of high-carbon ferrochrome is expected to fall slightly MoM to 488,000 mt. In December, the bid prices of high-carbon ferrochrome offered by the mainstream stainless steel mills were higher than the previous market expectations. Under the guidance of bid prices, the prices of ferrochrome have stopped falling and stabilised, and the chrome ore prices also increase accordingly. The ferrochrome plants in north China are still profitable and produce normally as they still have low-priced raw materials. However, at the end of November, amid the dry season in Sichuan, hydropower supply decreased, and electricity prices rose. Therefore, the costs of ferrochrome smelting increased and more ferrochrome plants stopped the production. The overall supply of ferrochrome is expected to decline slightly in December. Recently, many stainless steel mills reduce the production. Meanwhile, the pandemic in many places affects the transportation, hence the freight costs increase and the delivery situation is more uncertain. In addition, the demand for winter storage at the end of the year is gradually released, hence the recent demand for ferrochrome is acceptable. Under the weak overseas demand, the domestic ferrochrome output is relatively low, but the supply is still sufficient and the accumulated inventory in the early stage is slowly consumed. As such, the decline in the output has little impact on the prices of ferrochrome. It is expected that the ferrochrome market may remain stable at the end of the year.

Stainless steel

According to SMM survey, the stainless steel output was 2.88 million mt in November, up 6.67% MoM and 9.42% YoY. The output of 200-series stainless steel fell 4.08% MoM to 987,000 mt, 300-series dropped 7.52% MoM to 1.45 million mt, and 400-series increased 3.55% MoM to 440,500 mt.

In November, the output of domestic stainless steel mills increased to a certain extent compared with October. Among them, the 200 and 300-series stainless steel declined significantly while the 400-series still increased slightly. The transactions of 200-series stainless steel were in November. At the same time, the in-plant inventory of steel mills and the social inventory in the spot market accumulated. Therefore, many steel mills carried out maintenance and reduced the production in advance. Although the production capacity of newly commissioned steel mills increased, many steel mills reduced the production in the second half of November due to the high costs of various raw materials and the weak downstream demand. Therefore, the total output of the 300-series stainless steel still decreased month-on-month.

In December, the total output of stainless steel mills across the country may increase slightly from the previous month. Due to the recovering profits and the good spot transactions, the production of 300-series stainless steel may resume. In addition, the pandemic prevention and control policies are gradually eased in various places. As such, terminal enterprises in some areas may purchase in advance and the construction of some large-sized infrastructure projects gradually starts. The transmission of demand to terminals is relatively smooth. On the whole, the supply of stainless steel may increase in December. Amid the improving demand and the decline in costs, SMM believes that the prices of stainless steel will stabilise in December.

EMM

China produced 65,700 mt of EMM in November, up 32.40% MoM but down 28.10% YoY, according to SMM statistics. From January to November 2022, the EMM output in China was 670,900 mt, a decrease of 35.78% year-on-year. According to SMM research, on the one hand, a large-sized domestic manganese plant completed its maintenance and its output increased. On the other hand, as the production was suspended for a long time in the early stage, the spot goods were digested and the market supply and demand relationship eased. As such, the manganese plant resumed the production significantly and the domestic output increased month-on-month.

In December, although the demand is still relatively weak, the spot supply is tight. Coupled with the production suspension of some manganese plants in the early stage, the enterprises are willing to produce amid the backlog of orders. Therefore, the output is expected to be about 68,300 mt.

Industrial silicon metal

SMM data showed that China’s industrial silicon metal output stood at 308,300 mt in November, down 4% month-on-month, but up 3% year-on-year. The output totalled 3.19 million mt from January to November, an increase of 21% on the year.

In November, the three main producing areas, namely Xinjiang, Yunnan, and Sichuan, all saw a decline of about 1,000 mt in the output. In detail, the total supply in Xinjiang diminished due to the production reduction at large factories. Fortunately, the operating rates of local silicon metal plants recovered at the end of November when the pandemic was under control, and meanwhile the new capacity kept ramping up. As such, it is expected that the silicon metal output in Xinjiang in December will increase significantly month-on-month. As for Sichuan and Yunnan, the operating rates of local silicon metal plants both dipped as the dry season started. In Sichuan, the average operating rate of silicon metal companies declined five percentage points month-on-month to 66% in November. Amid falling silicon metal prices and rising costs of silicon metal companies, it is estimated their operating rates will slip at an even faster speed in December to below 50%. The production cuts in Yunnan in November mainly occurred in Nujiang. In December, the power supply shortage in Baoshan and Dehong has eased, but the poor production efficiency of furnaces in some silicon metal producers has affected the output. In this case, it is expected that silicon metal producers in Yunnan will slash the output at the end of December.

Additionally, the month-on-month changes in the output in other producing areas in November were insignificant. Generally, it is expected that the supply of industrial silicon metal will not fall sharply in December. The total output of industrial silicon metal in 2022 will be around 3.5 million mt, an increase of 590,000 mt or 20% year-on-year.

Polysilicon

The domestic output of polysilicon continued to increase by 9.66% on the month to around 93,100 mt in November, according to SMM statistics.

According to SMM survey, polysilicon producers still acquired high profits in November thanks to the high profitability of polysilicon. Generally, the enthusiasm for production was high. The operating rates of top-tier companies basically remained above 90%, such as Tongwei, Xinjiang TBEA, and Daqo Group. In addition, many enterprises maintained 100% operating rates or even produced at more than full capacity. The production ramp-up of newly-commissioned production lines in Qinghai Lihao and Leshan GCL contributed to most of the growth in the output, while the maintenance of Tongwei’s production lines in Inner Mongolia caused a loss of about 3,000 mt in total output.

PV module

According to SMM statistics, the output of domestic module output in November was about 33.4 GW, a further increase of about 10.5% from October. In the fourth quarter, downstream enterprises’ stockpiling has triggered a vast increase in module demand. While with the end of the restocking, the production of modules in December is expected to drop sharply. The output in December is estimated at only 27 GW. In October, a number of terminal projects at home and abroad rushed to install the capacity. At the same time, the Chinese government called on "all power grid companies to ensure the safety and stability of the power grid as well as the stable supply of power before connecting as many grids as possible, and as early as possible”. The power grid companies were also advised to take effective measures to ensure the timely grid connection of wind power and photovoltaic power generation projects. Terminal enterprises already locked in a large number of orders in advance during October and early November. The improvement in demand kept the operating rates of module companies at a high level. According to SMM statistics, the individual module output of many leading companies such as LONGi, Jinko Solar and JA Solar in November all stayed above 3 GW.

SiMn alloy

China produced 818,800 mt of silicon-manganese alloy (SiMn alloy) in November, up 6.79% MoM and down 5.25% YoY, according to SMM statistics. The combined SiMn alloy output in China from January to November stood at 9.14 million mt, a decrease of 7.27% year-on-year. According to SMM survey, the frequent positive news from the terminal sectors in November boosted the market confidence and the operating rates of steel mills. Therefore, the higher demand for SiMn alloy fuelled the operating rates of SiMn alloy producers, which contributed to the higher output compared with the prior month.

In December, the bid prices of mainstream steel mills have increased month-on-month. At the same time, the pandemic control policies are eased, and the market has strong expectations for favourable policies. As such, the enthusiasm of enterprises for production has been high. On the other hand, as the end of the year approaches, downstream steel mills are inclined to stock up, which will also improve the demand for SiMn alloy. Altogether, the SiMn alloy output is expected to rise to 862,000 mt in December.

Magnesium ingot

According to SMM, China’s magnesium ingot output stood at 75,000 mt in November, down 5% MoM and up 14% YoY. The output totalled 881,000 mt in January-November, up 27% from the comparable months last year.

The trades in the magnesium market were thin as downstream demand in November failed the expectation. As such, magnesium prices showed a downward trend. According to SMM statistics, the prices of Mg90% magnesium ingots in Fugu county, Shaanxi province, generally fell by more than 2,200 yuan/mt in November alone. The exceedingly low profits dampened the enthusiasm for production among magnesium factories, which led the domestic magnesium ingot output to post a second straight Month month of decrease. It is learned from some people in charge of the magnesium factories that the constant falling magnesium prices already caused market transaction prices to drop below the costs of some producers, and most magnesium factories generally operated under financial pressure. What was worse, employees of several plants were under lockdowns for testing positive for COVID-19. As a result, the operating rates of magnesium plants were dragged down. It is expected that the output of magnesium ingots will remain low as the outlook for pandemic control is pessimistic. To be specific, the domestic magnesium ingot output in December is predicted to be 72,000 mt.

Magnesium alloy

China magnesium alloy output stood at 23,000 mt in November, down 8% MoM and up 21% YoY, according to SMM statistics. The accumulative output from January to November was 282,000 mt, down 5% from the previous year.

According to SMM research, the domestic downstream demand for magnesium alloys continued to weaken in November, which was reflected in the shrinking orders received by magnesium alloy producers. The person in charge of a large domestic magnesium alloy plant said that when the domestic macro environment was weak while the overseas orders were poor, domestic factories generally rushed to lower their prices to compete for orders. As a result, the profits of manufacturers were severely hurt. It is forecast that under the influence of poor demand, the output of magnesium alloys in December will drop further to 22,000 mt.

Magnesium powder

China's magnesium powder output stood at 6,000 mt in November, down 3% MoM, and the combined output in January-August totalled 75,000 mt.

The domestic magnesium powder output moved down in November. According to the feedback from some magnesium powder companies, the domestic magnesium powder orders showed a downward trend due to the impact of the pandemic and weak demand from steel mills. At the same time, most downstream buyers stood wait-and-see owing to previous disruption of shipments caused by the pandemic. Nevertheless, considering that overseas orders are likely to pick up during the Christmas and the latest eased pandemic control policies have boosted the market confidence, the domestic magnesium powder production is anticipated to recover in December to about 7,000 mt.

PrNd oxide

Domestic output of PrNd oxide in November stood at 5,889 mt, up 2% on a monthly basis. The increase in output was mainly contributed by Jiangsu province, while the output in other regions was flat.

In November, the spot goods of PrNd oxide were still in shortage, while inquiries and purchases were frequent in the spot market as the end of the year approached. Generally, the PrNd oxide prices were on the rise. At the same time, some manufacturers ramped up their output to attain their annual production goals. In particular, the output in Jiangsu advanced by about 36% MoM. Since some manufacturers will halt the production for maintenance at year end, it is expected that the output of PrNd oxide may contract slightly in December.

PrNd alloy

Domestic output of PrNd alloy in November 2022 stood at 5,128 mt, down 0.4% month-on-month. The decline in output mainly resulted from the output decrease in Shandong province, with little changes in other regions.

In November, the demand for PrNd alloy remained sluggish. The increase in orders from leading magnetic material companies was limited, thus the transactions of PrNd alloy still fell short of expectations, and metal factories still suffered losses. For this reason, metal factories in Shandong reduced the production by 9% year-on-year. Some manufacturers revealed that they will put a stop to the production in December. As such, it is expected that the output of PrNd alloy will continue to shrink in December.

Molybdenum concentrate

SMM data shows that China’s molybdenum concentrate output in November 2022 was 19,100 mt, a drop of 1% from the previous month.

According to SMM research, the overall ROM at domestic molybdenum mines remained stable in November. It not only enjoyed support from strong actual demand, but was also free from falling temperature and environmental protection-related control. In December, some private mines in south China have plans to end operation in advance, which will lead to a small reduction in the actual output. However, most mines will still maintain stable mining activities because the current supply has failed to satisfy the downstream demand. Therefore, the output of molybdenum concentrate in December is inclined to dip slightly MoM.

Ferromolybdenum

SMM data shows that China’s ferromolybdenum output in November reached 18,200 mt, a drop of 2% from the previous month.

It is reported that the bid volume from domestic steel in November was about 11,000 mt, a proof of lasting peak season for ferromolybdenum. The demand for stainless steel from alloy steel and special steel was relatively stable, so the demand provided strong support for the output of ferromolybdenum. However, the high prices of raw materials and the limited supplies from mines prompted some ferrochrome plants to reduce their operating rates based on cost risk considerations. This explains why there was a slight decline in the total output of ferromolybdenum.

Generally, the delivery of ferromolybdenum plants usually takes place at the end of December or the beginning of the January, and the steel mills' restocking demand at the year-end is still mounting. As such, SMM estimates that the output of ferromolybdenum in December will see a certain growth.

Silver

According to SMM survey, domestic silver output stood at 1,370.75 mt (including 1,134.75 mt of mineral silver) in November 2022, down 1.9% on the month. The silver output of various manufacturers changed differently in November. Some manufacturers increased their output on the support of better quality of raw materials with higher silver content, or in order to attain their annual production goals. Others suspended their production due to maintenance or the Covid-19 pandemic. Generally, the decrease in the output outweighed the increase, which caused the overall output to show a downward trend. As the Spring Festival approaches, most smelters will have to be closed for holidays or maintenance. In this context, SMM expects that the silver output in December will shrink slightly.

Notes: SMM has released Chinese silver output since February 2021. The silver is usually produced along with copper, lead and zinc. Thanks to its high coverage of the base metals industry, SMM has successfully investigated a total of 45 silver production enterprises, which are located in 17 provinces across the country, with a total capacity of 24,000 mt and a total capacity coverage rate of over 99%.

Antimony ingot

According to SMM statistics, China produced 6,981.16 mt antimony ingots (including antimony ingot, converted crude antimony, cathode antimony, etc.) in November, a sharp increase of 27.92% month-on-month. On the whole, the antimony ingot output rose sharply in November thanks to the resumption of production at many manufacturers. Generally, the production cuts or halts were overshadowed by production recovery and output increases, hence the overall antimony ingot output recorded an increase in November. It seemed that the market was constantly in a shortage of antimony ore, but some market participants said that the impact of raw materials had gradually decreased. It is even reported that the shipments of antimony ore (50%-55% grade) have begun to increase before the year 2022 ends, and the prices of antimony ore above 55% grade and above 50% grade once fell to 61,000 yuan/mt and 59,000 yuan/mt respectively. In this case, the domestic antimony ore is likely to increase in December. Nevertheless, some market participants also said that many mines were more inclined to resort to tollers. They would pay processing fees but keep metal in their own inventories, which means that part of the output may not directly enter the market from manufacturers. Judging from the production situation of manufacturers in November, those who cut or suspended the output became fewer. Among the 33 survey respondents, 15 manufacturers halted the production in November, down by 1 from October; 11 curtailed their production, down by 2; and 7 maintained normal production, 3 more than the previous month. These figures tell that the production has been increasingly concentrated. SMM predicts that the supply-demand structure of the domestic antimony market in December will not be overturned under the current economic situation, and the sluggish demand is more than likely to extend. Despite this, the national antimony ingot output in December is anticipated to increase.

Notes: SMM starts to disclose the output of antimony ingots (including antimony ingots, converted crude antimony, cathode antimony, etc.) since May 2022. Thanks to high coverage of the antimony industry, SMM has successfully investigated a total of 32 antimony ingot manufacturers, which are located in 8 provinces across the country, with a total capacity over 20,000 mt and a total capacity coverage rate over 99%.

Refined bismuth

According to SMM survey, the domestic output of refined bismuth in November fell 4.29% month-on-month to 2670.59 mt. On the whole, a small number of refined bismuth manufacturers were shut down while a considerable number cut their production. Among the 23 survey respondents, five manufacturers stopped the production in November, and six further curtailed their output on a monthly basis. SMM predicts that the supply and demand of the domestic refined bismuth market in December will not be overturned under the current overall economic situation, and the poor trades in the market are expected to extend. For the downstream enterprises of bismuth, the domestic demand and exports are rather unlikely to see rapid growth in the short term. Although some terminal consumers will stock up for the winter with the upcoming year end, the actual amount of goods will be limited. Thus, the possibility of a reverse in overall consumption is small. But at the same time, the refined bismuth manufacturers across the country are still lowering their output for a tight supply of raw materials. The impact of pandemic on the production in south China will not abate soon regardless of the eased pandemic control measures. Under these circumstances, the consumption of refined bismuth stocks may still be the top priority in the short term. In addition, it is also difficult to say for sure that the manufacturers that have suspended or cut the production will resume the production in December.

Notes: SMM has released Chinese refined bismuth output since October 2022. Thanks to its high coverage of the refined bismuth industry, SMM has successfully investigated a total of 23 refined bismuth manufacturers, which are located in 8 provinces across the country, with a total capacity over 50,000 mt and a total capacity coverage rate over 99%.

Silver nitrate

The domestic silver nitrate plants with qualification certificates together produced 588 mt of silver nitrate in November, down 2.3% on the month. The total output of silver nitrate nationwide reached 619 mt. Among them, the output in central China decreased 8.8% MoM, that in north-west China gained 12.5% MoM, that in east China was basically unchanged, and that in south China advanced 13.3% on the month. Generally speaking, the decrease combined was larger than the total increase. The reasons for the decrease included the surging prices of silver, which caused downstream buyers to purchase only on rigid demand, and slow transportation in some areas affected by the pandemic. The increase in the output was supported by the rigid demand of downstream companies as well as the pre-holiday restocking.

As the Spring Festival approaches, SMM predicts that silver prices may rise before and after the Spring Festival, while the downstream enterprises will continue to restock on rigid demand. Therefore, SMM believes that the demand for silver nitrate will increase in December.

Titanium dioxide

SMM data shows that China's titanium dioxide output stood at 311,000 mt in November 2022, down 2% both from the previous month and the previous year. The output in the first eleven months of 2022 increased 3% year-on-year to 3.52 million mt.

According to SMM research, most titanium dioxide producers were operating under pressure due to the rising prices of raw materials and the persisting low prices of titanium dioxide. Since the mid- and late October, the market sentiment was bullish on the prices of titanium dioxide, and many companies raised the quotes for their product. The downstream orders were thus released, and titanium dioxide companies were successful in destocking. However, the operating rates of terminal construction sector have been low during the ongoing winter, which suggests that the titanium dioxide enterprises will face greater pressure when it comes to restocking. Given that enterprises will be reluctant to expand the production, the titanium dioxide output in December is estimated to remain stable at about 310,000 mt.

APT

According to SMM statistics, China's APT output in November 2022 will be approximately 11,900 mt, a decrease of 5% or 600 mt month-on-month.

On the whole, the actual consumption of tungsten resources was lower as weak terminal demand lasted for a whole quarter and mines reduced the release of resources. Most smelters maintained their operating rates at 70-80%. Few manufacturers produced at full capacity, and some had plans to stop the production. In the meantime, less tungsten ore available in the market also caused the profits of smelters to fall into negative territory in a faster speed. That is to say, the smelters only maintained stable delivery of long-term orders and reduced the retail supply in the spot market under huge cost pressure, thus the output of APT began to decrease in November. In December, the APT output may decline further with limited downstream demand and the implementation of the maintenance plans.

Lithium carbonate

China’s lithium carbonate output in November stood at 36,651 mt, up 7% on a monthly basis and 71% on a yearly basis. In November, some enterprises reduced the production amid the pandemic, and the production from salt lake was down constantly due to seasonal factors. At the end of the month, some lepidolite smelters in Jiangxi also downscaled the production due to environmental protection or road construction, resulting in a certain decline in lithium carbonate output. Nevertheless, some large factories already recovered from the maintenance in November with a sharp increase in their output. This, combined with the ramp-up of capacity in some other enterprises, contributed to a 7% MoM growth in total output. In December, enterprises previously affected by the pandemic have gradually resumed normal production. Yet, the environmental protection-induced production restriction in Jiangxi has still compelled some local enterprises to cut their production, apart from their year-end maintenance plan. As such, the lithium carbonate output is estimated to drop 7% MoM and increase 72% to 33,986 mt in December.

Lithium hydroxide

China’s lithium hydroxide output was 25,210 mt in November, a month-on-month decrease of 4% but a year-on-year increase of 49%. Although some smelters ramped up their capacity, the shortage of mineral materials remained unsolved. This, coupled with the production cuts of some enterprises due to the pandemic, led to a decline in the lithium hydroxide output. At the same time, causticising plants also reduced the output for high costs and a lack of raw materials. Altogether, the supply of lithium hydroxide decreased as a result. In December, the shortage of mineral materials in some smelters has eased, and the impact of the pandemic has also weakened. Therefore, it is predicted that China lithium hydroxide output in December will be 25,351 mt, flat from November and up 48% YoY.

Cobalt sulphate

China’s cobalt sulphate output was 7,347 mt in metal content in July, a month-on-month decrease of 2% and a year-on-year increase of 28%. On the raw material side, the cobalt prices overseas dropped significantly in November, and thus the cost of cobalt intermediate products also decreased. This, coupled with sluggish demand, dragged down the prices of cobalt salts. On the supply side, the output of leading cobalt intermediate product enterprises did not change dramatically, but the output of the smelters using scrap edged lower due to reduced production scheduling. On the demand side, since the new energy subsidies will be removed in 2023, the orders placed by domestic new energy car makers for ternary batteries already slumped, taking a toll on the demand for ternary precursors. In the overseas market, the demand for ternary batteries increased steadily, and the orders for high-nickel precursors thrived. In December, the demand for ternary precursors will continue to shrink, but it is the second-tier manufacturers who will be affected. Instead, the output of cobalt sulphate in integrated precursor companies will continue to increase. SMM predicts that China’s cobalt sulphate output will rise 5% MoM and 37% YoY to 7,744 mt in metal content in December.

Tricobalt tetraoxide (Co3O4)

The domestic output of Co3O4 stood at 5,617 mt in November, down 12% MoM and 23% YoY. On the cost side, the prices of cobalt salts began to pull back in November, and the Co3O4 prices followed the raw material costs to edge lower. On the supply side, the Co3O4 inventory was high due to the output growth in September and October, while the Co3O4 prices were in a downward trend. Therefore, manufactures mainly focused on destocking. In addition, top-tier manufactures reduced the production of Co3O4, when small factories also saw a slip in orders, hence the Co3O4 output decreased in November. On the demand side, the demand for Co3O4 fell sharply in November. The purchase of downstream LCO enterprises contracted, and the trades in the spot market were slack. The LCO plants were not in a rush to stock up raw materials as the demand from the digital electronics sector did not recover as expected. While they resort to risk aversion by reducing the inventory, the poor demand for Co3O4 will hardly improve in the short term. It is expected that the output of Co3O4 will stand at 5,311 mt in December, down 5% MoM and 28% YoY.

Ternary cathode precursor

The domestic ternary cathode precursor output was 90,128 mt in November, a month-on-month decrease of 1% and a year-on-year increase of 53%. The upcoming removal of new energy subsidies in 2023 caused downstream material plants to control the inventory, thus the shrinking orders for precursors led to a MoM decline in domestic precursor output. Nevertheless, the steady growth in overseas orders made up for the decline in domestic orders. As such, the decline in ternary precursor output was limited. It is estimated that the overseas demand will continue to climb steadily while the domestic demand will slip at a faster speed. In this case, the ternary precursor output will drop 4% over the month to 86,555 mt November, a year-on-year increase of 45%. Ternary cathode materials China’s ternary cathode material output stood at 66,294 mt in November, down 6% MoM and up 55% YoY. In terms of demand, the falling demand for ternary cathode materials mainly resulted from the diminishing demand from power battery sector. On the other hand, the demand from digital electronics sector has been small throughout the whole year, and it trended lower in the fourth quarter. In terms of supply, the overall capacity was sufficient as some ternary material companies still ramped up their capacity. But in order to tackle the weaker downstream demand, many companies were forced to reduce the production. The downstream demand has further weakened in December, and most downstream enterprises have finished stockpiling at the end of the year. As such, the output of ternary materials in China is expected to decline further by 11% MoM to 59,052 mt in December, up 25% YoY.

Iron phosphate

The domestic iron phosphate output stood at 93,776 mt in November, down 2% on a monthly basis. On the supply side, the downstream LFP enterprises were firm to bargain down the prices on the support of falling demand, while the costs of raw materials moved up slightly. Under these circumstances, some iron phosphate enterprises had to rearranged their production schedules, and the output thus dropped slightly. On the demand side, the wait-and-see sentiment became stronger among LFP enterprises as the lithium salt prices kept fluctuating while the terminal demand fell short of expectations. The LFP plants were cautious about stocking up iron phosphate due to uncertainty about their following production schedules. Some enterprises even reduced their purchases. Given that the new energy subsidies will be cancelled soon, which will undermine the boost for upstream production, it is expected that the iron phosphate output will decline further by 4% over the month to 89,898 mt in December.

LFP

China produced 119,698 mt of LFP materials in November, a decrease of 3% month-on-month and an increase of 130% year-on-year. As the year end drew near, terminal demand began to weaken amid falling prices of lithium salt. As a result, some plants lowered the production to cope with market uncertainties. As raw material production will lose the support with the upcoming removal of new energy subsidies, there were rumours that some battery cell factories will cut the output of power battery cells. The demand for energy storage was on the rise, but it failed to offer strong support since it only accounted for a small proportion of the total demand. In December, the downstream demand has contracted sharply as the upcoming new energy subsidy removal will undermine the boost for upstream raw material production, and this was compounded by the downward prices of lithium salts. In this context, the production and sales of LFP plants and downstream battery cell companies will be pessimistic. It is expected that the production cuts will expand, so the LFP output is forecast to be 109,045 mt in December, a decrease of 9% month-on-month and an increase of 76% year-on-year.

LCO

Domestic LCO material output was 7,184 mt in November, down 2% on the month and 5% on the year. According to SMM research, the demand for smartphone did not pick up significantly after the fourth quarter started. The prices of some digital products plunged, but still failed to fuel market demand. The mobile phone producers focused on adjusting their capacity utilisation rates along with the upstream enterprises based on the market demand, thus the capacity utilisation rates of LCO plants also dropped. On the cost side, the Co3O4 prices showed a downward trend in November while the prices of lithium carbonate stood high. The elevated costs of LCO caused LCO prices to stabilise after a slight increase. On the supply side, top-tier LCO manufacturers cut their output slightly, leading to supply decrease. On the demand side, the downstream LCO battery cell factories started restocking since the early November, and their raw material stocks may be sufficient enough to support them to the end of 2022. As such, the trades of in the electronics market were lacklustre as the demand remained weak. LCO batteries with high charge and discharge rate are generally applied in e-cigarette manufacturing. As the export orders for domestic e-cigarette were numerous in November, the demand for this kind of LCO rose steadily. However, LCO plants targeting electronics market were still bearish on the demand in the early 2023. Therefore, SMM predicts that China’s LCO output will fall 6% MoM and 14% YoY to 6,770 mt in December.

LMO

China LMO output stood at 8,567 mt in November, up 39% MoM and 45% YoY. The volatile lithium carbonate prices stimulated concerns among LMO enterprises about a decline in the value of the raw materials. As a result, they rushed to make shipments, which induced a spike in the LMO output. In December, the demand slipped again as the boost from Double Eleven shopping festival and year-end stockpiling both abated. Batter cell factories, who were bearish on the prices of lithium carbonate, only accept low quotes of LMO plants, thus the trades in the market were quiet. At the same time, the willingness for production among LMO plants were low at the end of the year. Some of them said that they would take holidays in advance. It is estimated that the LMO output will reach 5,371 mt in December, a decrease of 37% month-on-month and 16% year-on-year.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)