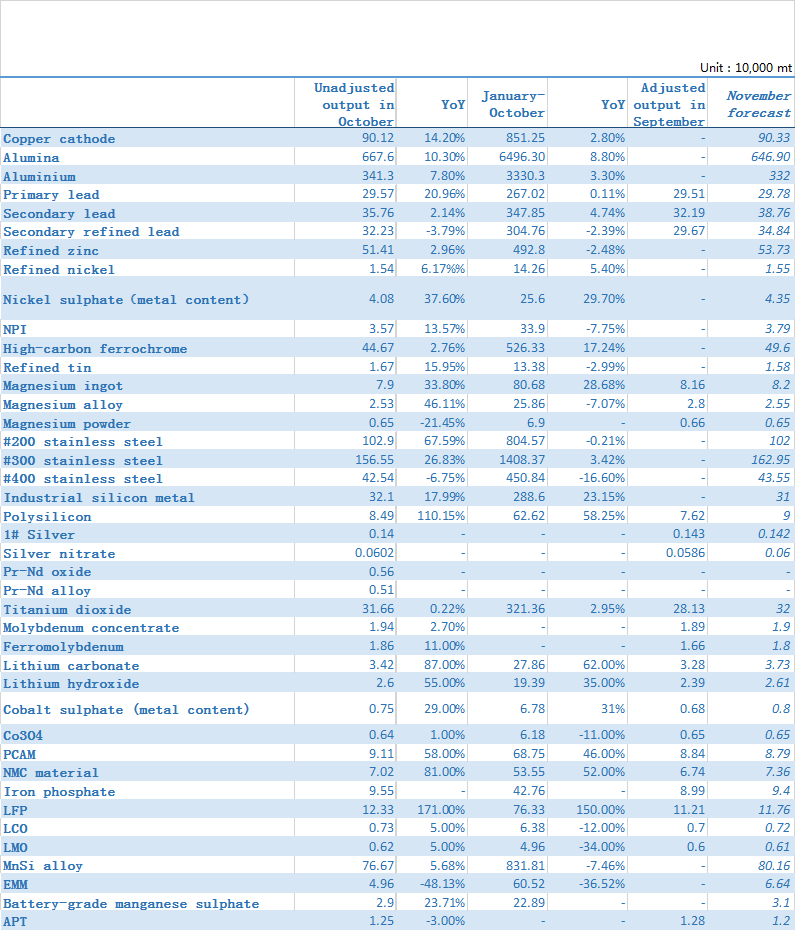

Copper cathode

China’s copper cathode output stood at 901,200 mt in October, down 0.9% month-on-month (MoM) and up 14.2% year-on-year (YoY). The output totalled 8.51 million mt from January to October, an increase of 2.8% or 232,800 mt on the year.

The output growth in October fell MoM and fell short of expectations mainly for the following causes, according to SMM analysis: 1. The output was partly affected by the overhaul of smelters. According to SMM statistics, 3 smelters had overhaul plans in October; 2. The tight supply of blister copper and copper scrap weighed on the production some smelters which fell more than expected; 3. The pandemic and power cuts resulted in more-than-expected output reductions of smelters in south-west China and Inner Mongolia; 4. The newly commissioned smelters in October were slow in yielding output, and several smelters even delayed their commissioning plans.

Currently, five smelters have disclosed maintenance plans in November, more than that in October. In addition, the supply tightness of blister copper and copper scrap is not addressed, which will remain another important factor restricting the increase in production. The expected commissioning of a smelter in central China is unlikely to bring any surprises in November. Nevertheless, most of the smelters have high production enthusiasm recently, stimulated by the fact that sulphuric acid prices and copper concentrate TCs are still rising. China copper cathode output is estimated at 903,300 mt in November, up 0.23% or 2,100 mt MoM and 9.4% YoY based on the current production schedules. The output will then total 9.42 million mt from January to November, an increase of 3.4% or 310,200 mt on the year.

Alumina

According to SMM, China metallurgical-grade alumina output in October (31 calendar days) was 6.68 million mt with a daily output of 215,400 mt, down 0.61% MoM but up 10.3% YoY. The operating capacity of alumina was 78.61 million mt and the domestic operating rates stood at 81.1% on average.

The total output was 2.16 million mt in Shandong, down 2.41% on the month; 1.58 million mt in Shanxi, down 0.62%; 721,000 mt in Henan, down 7.43%; 1.09 million mt in Guangxi, up 4.78%; 465,000 mt in Guizhou, up 7.69%; 320,000 mt in Chongqing, down 3.03%; 165,000 mt in Hebei, down 8.33%. The operating rates in other provinces were basically stable, with a total output of 136,000 mt in Yunnan and 42,000 mt in Inner Mongolia.

On the whole, it is estimated that the net imports of alumina in October will be 100,000 mt. And there will be a surplus of 205,000 mt in the month, and a surplus of about 1.62 million mt during January-October. At present, the supply surplus of alumina has expanded. Luyu Bochuang and Lubei Chemical each expanded their production by 1 million mt at the end of September, and are expected to contribute to the output increase in the fourth quarter. At the same time, due to the production reduction and slow resumption of production of aluminium in Yunnan, the demand for alumina is declining. Affected by the continuous increase in raw material prices and the weak domestic alumina prices, the profits of domestic alumina plants declined further in the first half of 2022. By the end of October, the average profit of Chinese alumina plants was less than 50 yuan/mt.

The alumina prices in November are unlikely to rebound and more domestic alumina refineries have suffered losses. Nearly 80% of the refineries are struggling at the break-even point, especially those in Shanxi, Henan and Guizhou. Amid the heavy operating pressure and the high costs, the refineries may reduce or stop the production. Up to now, 2.8 million mt of alumina capacity has been eliminated in 2022, but there is also 10.5 million mt of new capacity. However, some alumina refineries with higher costs may stop the production in the follow-up period.

Aluminium

According to SMM data, China produced 3.41 million mt of aluminium in October (31 calendar days), up 7.8% YoY. The daily output stood at 110,100 mt, down 1,204 mt on the month. The output totalled 33.3 million mt from January to October, up 3.3% YoY. In October, the domestic operating aluminium capacity rose slightly and the output in Sichuan and Inner Mongolia increased more significantly. The operating aluminium capacity in Sichuan ramped up to about 360,000 mt, an increase of 160,000 mt MoM. But the operating capacity in Sichuan may be unable to reach full production by the year end due to the electricity shortage during the dry season. The resumed capacity in Guangxi and the new capacity in Guizhou and Inner Mongolia was still less than expected. Meanwhile, the aluminium output in Yunnan dropped significantly in October as some smelters stopped the production as planned. As of now, the total operating capacity in Yunnan was about 4.04 million mt, and the combined production cuts amounted to 1.17 million mt in September and October.

According to SMM, as of the beginning of November, Chinese installed capacity of aluminium reached 45.16 million mt, and the operating capacity was 40.34 million mt, equalling to a national average operating rate of 89.4%. In October, the transportation was limited by the pandemic and aluminium smelters directly shipped the aluminium liquid to local downstream enterprises without casting for energy saving purpose. Therefore, the proportion of aluminium liquid in October increased 1.36% on the month to 69.75%.

In November, the domestic aluminium supply has experienced both ups and downs. High-cost aluminium smelters in Shandong and Henan are expected to reduce the production. The decline in output may exceed 100,000 mt. Meanwhile, amid the heating season in north China, some aluminium smelters in Shanxi may reduce the production slightly. The resumption of production in Sichuan and the new capacity of Inner Mongolia Baiyinhua may contribute to the output increase in November. In addition, according to SMM research, the commissioning of new capacity in Guizhou may be delayed until December. Combined with future production capacity changes, SMM predicts that the domestic operating aluminium capacity may be lifted to around 40.51 million mt at the end of November, and the output in November (30 calendar days) is expected to be around 3.32 million mt, a year-on-year increase of 8.1%. On the demand side, the downstream consumption was still weak in October. The operating rates and orders of mainstream sectors such as aluminium plate/sheet, strip and foil and aluminium extrusion declined due to the pandemic. However, due to the poor transportation, the domestic aluminium inventory in October was low. Taking the future arrivals and the resumption of downstream enterprises into account, the social inventory of aluminium ingot will remain at 500,000-600,000 mt in November. Coupled with the slow commissioning of new capacity, aluminium prices may be supported.

Primary lead

China produced 295,700 mt of primary lead in October, up 0.21% MoM and 20.96% YoY. The total output in January-October increased 0.11% after falling for 8 months. Production capacities of enterprises involved in the survey totalled 5.71 million mt in 2022.

According to the survey, the primary lead smelters went over maintenance and production resumption, while the output in October increased. In October, Power Supply Bureau of Yunnan Honghe Prefecture issued a notice on energy efficiency management for this winter and next spring, proposing power cuts in the dry season. Some lead smelters were included in the list of production control. At the same time, smelters in Inner Mongolia and Yunnan either stopped or reduced the production in the short term due to the intensifying pandemic. However, in the fourth quarter, large-sized enterprises ramped up the production actively at the end of the year. For example, smelters in Henan and Inner Mongolia continued to increase the production. Meanwhile, with the lift of power rationing, smelters in Hunan resumed the production to some extent in October. Therefore, the output of primary lead increased slightly.

In November, the impact of the pandemic in the main producing areas has eased. Lead smelters in Inner Mongolia, Yunnan and other places, such as Yunnan Mengzi, Xing'an Silver & Lead and Yunnan Zhenxing, have gradually resumed the production. The production of other smelters remains relatively stable. Overall, the output of primary lead will continue to increase in November. SMM expects Chinese primary lead output will rise slightly to 298,000 mt in November.

Secondary lead

China's secondary lead output stood at 357,600 mt in October, up 11.09% on the month and 2.14% on the year. Output from January to October totalled 3.48 million mt, a year-on-year increase of 4.74%. China's secondary refined lead output stood at 322,300 mt in October, up 8.63% on the month but down 3.79% on the year. Output from January to October was 3.05 million mt, a year-on-year decrease of 2.39%.

In October, domestic output of secondary lead and secondary refined lead increased significantly on the month as the smelters in Anhui, Henan and Hebei increased the production. In the Jieshou and Taihe areas of Anhui, the production of the secondary lead smelters was limited by the power rationing in September. From the end of September to the first ten days of October, the smelters in the two areas were successively affected by the local pandemic and poor transportation. Therefore, the output did not increase significantly. After the impact of the pandemic was lifted in mid-October, smelters gradually increased the production in light of the improved profits and the undelivered long-term orders. At present, most smelters reached full production and the output of some smelters still had upside potential. Among them, Anhui Huabo reduced the production significantly in September due to equipment failures, but resumed to normal production in October, bringing significant output increases. Anhui Chaowei, Anhui Camel, and Anhui Tianchang also ramp up their production in October compared with the previous month. Henan Yongxuan reduced its output in September due to equipment failures and resumed the production slightly in October. However, the equipment failed again, which led to a sharp reduction in its production. It is expected that its output will decrease in November. The new production line of Hebei Songhe also brought a substantial increase in output in October. However, Anhui Dahua undertook maintenance from late September to late October, hence its output declined significantly in October. Jiangxi Jinyang also carried out maintenance in October, which greatly reduced its output.

In November, the production of Anhui Dahua has gradually returned to normal level since October 26. Jiangxi Jinyang is resuming the production recently. As such, the output in November may increase significantly. The production of other smelters also climbs slightly. The secondary lead output may add up to 387,600 mt and the output of secondary refined lead may increase to 348,400 mt in November.

Refined zinc

SMM data showed that the China refined zinc output in October fell slightly short of expectation and stood at 514,100 mt, up 2.02% or 10,200 mt MoM and up 14,800 mt or 2.96% YoY. From January to October 2022, the combined refined zinc output stood at 4.93 million mt, a decrease of 2.48% year-on-year.

SMM survey showed that China refined zinc output in October gained palpably on a monthly basis, but it was still slightly less than expected. Reasons for the increase in output vary. Large smelters in Hunan ramped up the production, and some small smelters in Hunan and Guangxi resumed normal production; the overall output in Yunnan climbed thanks to the production uplift in some large smelters in spite of power rationing; a large smelter in Inner Mongolia ramped up the output after digesting the excessive zinc sheet arising from previous production reduction; a smelter in Xinjiang resumed the production from maintenance, thought it did not reach full capacity due to the impact of the pandemic. Nevertheless, there still existed factors resulting in the reduction in output. Some smelters in Guangdong and Yunnan entered routine maintenance; some smelters in Inner Mongolia did not resume normal production due to equipment problems.

SMM estimates that China refined zinc output in November will add 23,200 mt from the previous month to 537,300 mt, up 17,800 mt or 3.43% on the year. The total refined zinc output in January-November 2022 is estimated to be 5.47 million mt, a decrease of 1.93% year-on-year. Reasons for possible increase in output are as follows. Some smelters in Yunnan and Guangdong will resume normal production after the overhaul; some smelters in Hunan, Guangxi, Xinjiang, and Qinghai will ramp up the capacity in November in the wake of production recovery in October. The production is also likely to experience some reductions in some places. The smelter in Inner Mongolia who has overproduced in October for a lack of zinc sheet, will return to normal production in November; a smelter in Sichuan will see a slight decline in output due to equipment problems.

SMM estimates that China refined zinc output in December will gain 9,800 mt from the previous month to 547,200 mt, up 33,900 mt or 6.6% on the year. The refined zinc output in 2022 is estimated to total 6.01 million mt, down 1.21% year-on-year. It is expected that previously affected smelters will all resume normal production in December.

Refined tin

Domestic refined tin output was 16,746 mt in October, up 10.92% MoM and 15.98% YoY, and the combined output from January to October fell 2.99% YoY, according to SMM research. The refined tin output in October exceeded the expectation.

The output increased significantly mainly as some smelters increased the production. In terms of regions: 1. The output of smelters in Yunnan remained stable. The output of some large-sized smelters dropped slightly while some smelters ramped up the production. According to SMM research, as the conversion margin of tin concentrate fell, the profits of enterprises decreased. In this scenario, smelters increased the production to allocate the costs. 2. The output in Guangxi increased more than expected. Those smelters that were previously affected by tight raw material supply now produced normally. The substantial output increase in October may be related to the staged policy support, while the production is expected to drop significantly in November. 3. The output of smelters in Jiangxi increased on the month. The mainstream smelters in Jiangxi produced normally, and some large-sized smelters purchased raw materials to alleviate the previous tight supply, but the output forecast in November is still limited by the tight raw material supply. 4. The total output of smelters in other regions increased steadily in October. In general, the smelters among SMM’s survey sample produced normally, and the actual output in October was basically in line with the expectation. According to SMM research, the smelters are likely to see little disturbances in November, and the output will remain stable.

In November, domestic mainstream smelters will remain normal production, but the shortage of recycled raw materials may bring certain challenges to some enterprises. Although the conversion margin of tin concentrate has contained the profits, mainstream smelters still produce actively. To sum up, SMM expects the domestic refined tin output will fall to 15,790 mt in November.

Refined nickel

China produced 15,400 mt of refined nickel in October, up 0.06% on the month and 6.17% on the year. In October, domestic refined nickel output changed little compared to September. Although the pandemic in north-west China was more severe, the production of refined nickel smelters was not affected. The pandemic had only some impact on the transportation. The spot refined nickel was shipped normally, but the transportation time extended slightly.

The output of refined nickel in November is expected to increase 0.58% MoM and 1.83% YoY to 15,500 mt. The output of refined nickel in November increased slightly is mainly as the resumed capacity and new capacity has achieved normal production. Coupled with the stable production of other refined nickel smelters, the domestic refined nickel output in November will remain stable.

NPI

China’s NPI output in October stood at 35,700 mt in Ni content, up 14.2% MoM and 14.6% YoY. The spot prices of stainless steel rose sharply in October, and the orders received by stainless steel plants also increased compared with that in September. Therefore, under the condition of improved profits, stainless steel plants elevated the production significantly. The demand for NPI also picked up. In October, the prices of high-grade NPI rose due to the strong demand, and the output of NPI increased significantly. The output of high-grade NPI stood at 28,100 mt (Ni content), up 14.6% on the month. And the output of low-grade NPI was 7,500 mt (Ni content), up 7.78% on the month. In October, as the 200 series stainless steel was profitable and the downstream orders improved, the output of low-grade NPI of integrated enterprises boomed accordingly.

China's NPI output in November is expected to be 37,900 mt (Ni content), up 6.12% MoM. The NPI output growth in November is mainly contributed by the new capacity of integrated enterprises that has been put into production. Coupled with the slight production increase of stainless steel in November, the total NPI output of integrated enterprises is expected to go up slightly while the output of other plants will remain stable.

Nickel sulphate

Chinese nickel sulphate output in October stood at 40,800 mt in Ni content or 186,000 mt in physical content, down 1.7% on the month but up 37.6% on the year. Chinese nickel sulphate output in October was basically the same as in September, and the expected increase did not appear. The output of some large-sized factories declined due to problems of production lines. The release of new capacity is expected to be delayed until November and the end of the year. In terms of raw materials, the nickel sulphate produced with high-grade nickel matte accounted for 29% of the total production, MHP 45%, and nickel briquette and nickel powder 7%. In November, due to the release of new capacity and resumption of existing capacity, the supply of nickel sulphate will increase slightly. Chinese nickel sulphate output in November is expected to rise 6.6% MoM to 43,500 mt in Ni content.

Battery-grade manganese sulphate

China's battery-grade manganese sulphate output stood at 29,000 mt in October, an increase of 21.85% MoM. According to SMM research, the long-term orders of mainstream manganese salt factories increased in October compared with September. As the new energy enterprises rushed to produce approaching the end of the year, the output of precursors increased. At the same time, the sales of new models improved, which increased the proportion of 5-series and 6-series precursors. Therefore, the demand for manganese picked up. In this scenario, the operating rates of many manganese sulphate factories gradually rose, and the overall inventory continued to decline.

In November, as the traditional car companies are transferring to new energy vehicle companies, the production of precursors still has upside momentum. At the same time, the monocrystal high-voltage 6-series precursors are as good as the high-nickel precursors. Coupled with better cost efficiency, the output growth of 6-series precursor exceeds that of the 8-series precursor. As such, manganese salt factories are bullish about the manganese demand in the future. It is expected that the output of manganese sulphate in November will climb slightly to about 31,000 mt in physical content.

High-carbon ferrochrome

According to SMM, China's high-carbon ferrochrome output in October added 22,000 mt or 5.1% on the month and 12,000 mt or 2.8% on the year to 446,000 mt. The output in Inner Mongolia was 275,700 mt, up 3,000 mt or 1.1% month-on-month; and the output in Sichuan was 28,000 mt, up 22.8% month-on-month. The demand for ferrochrome picked up as the stainless steel output increased amid the traditional peak in September and October. However, the ferrochrome plants were less willing to resume the production due to the losses as the purchase prices of ferrochrome grew limitedly and the prices of chrome ore remained high under the influence of the strike in South Africa.

The output of high-carbon ferrochrome in November is expected to be 496,000 mt, which is higher than that in October. The output of stainless steel in November is expected to remain high. The purchase prices of high-carbon ferrochrome offered by mainstream steel mills such as Tsingshan and Taiyuan Iron & Steel edged up 800 yuan/mt (Cr 50%) on the month as the demand for ferrochrome increased. The smelting costs in north China were relatively low, hence the operating rates were basically flat. In south China, ferrochrome plants that purchased low-priced chrome ore in the early stage were able to make profits, hence they resumed the production. However, ferrochrome plants in south China were more sensitive to costs. Therefore, the output in south China is unlikely to boom as the electricity prices may further increase in November amid the dry season. In November, low-priced chrome ore will arrive at ports intensively. Coupled with the improving demand for ferrochrome from stainless steel mills, the output of ferrochrome is expected to increase.

Stainless steel

According to SMM survey, the domestic stainless steel output in October totalled about 3.02 million mt, up 9.44% MoM and 31.04% YoY. The output of 200-series stainless steel stood at 1.03 million mt, up 19.79% MoM; 300-series 1.57 million mt, up 2.93%; 400-series 425,400 mt, up 12.09%.

In addition to the sharp output increase in September, the output of most domestic stainless steel mills still managed a small gain in October. The output of 200 and 400-series increased slightly while that of 300-series remained stable. The output of 200-series rose as stainless steel mills switched from 300-series to 200-series amid the improved orders.

The total output of stainless steel may increase slightly in November amid the ramping up of the new capacity. Other steel mills still maintain conservative production scheduling. The NPI prices have remained high, but steel mills are unwilling to purchase high-prices goods. As such, the prices of nickel raw materials are uncertain amid the tug-of-war between upstream and downstream players. In addition, due to the weak demand and poor transmission, the inventories of some steel mills, traders, and some terminal enterprises have been too high. Therefore, enterprises will give top priority to the digestion of inventory. Overall, amid the off-season in November, the supply and demand of stainless steel is weak. But the prices of stainless steel in November will fall slightly amid the strong cost support.

EMM

China produced 49,600 mt of EMM in October, up 18.52% MoM and down 48.13% YoY, according to SMM statistics. The combined output in January-October totalled 605,200 mt, down 36.52% YoY. According to SMM research, although the large-sized manganese plants were still under maintenance, manganese plants in Guangxi resumed the production due to the insufficient spot inventory, hence the output increased slightly month-on-month. In November, the medium and large-sized manganese plants that stopped the production due to the pandemic and maintenance in the early stage have resumed the production, hence the market supply is likely to boom. The estimated output in November is about 66,400 mt.

Industrial silicon metal

The domestic silicon metal output stood at 321,000 mt in October, down 0.7% on the month and up 18% on the year, according to SMM statistics. China’s industrial silicon metal output totalled 2.89 million mt in January to October, a year-on-year increase of 23%.

The industrial silicon metal output fell about 11,000 mt from the previous month as the output in Yunnan fell significantly. The output in Hunan, Inner Mongolia and other regions grew as local plants resumed the production while those in Sichuan ramped up the output.

In November, the top two silicon plants in Xinjiang are affected by the pandemic to varying degrees and have reduced the production. It is not clear when they will resume the production. Amid the dry season in Sichuan, some silicon plants are less active in production due to the poor production conditions. If electricity prices increase further, local silicon plants may reduce the production by the end of November. Yunnan has entered dry season on November 1, and plants in Nujiang are expected to reduce the production in mid-to-late November while those in other areas will produce stably.

Silicon plants in Sichuan and Yunnan are expected to reduce the production intensively in late November. And the production in Xinjiang is not certain. It is expected that the industrial silicon metal output in November will drop to about 310,000 mt.

Polysilicon

The output of polysilicon stood at around 84,900 mt in October, up 11.4% on the month, according to SMM statistics. But it should be pointed out that the growth rate in October was significantly lower than that in September. The major increase in the polysilicon output was contributed by the companies including GCL, Tongwei and Asia Silicon, who put new capacity into production and ramped up the output. As for the slowdown in the growth rate, it is because the output in September enjoyed multiple driving forces such as the end of the earthquake and power rationing, while the output in October was merely facilitated by the ramp-up of new capacity.

SiMn alloy

China produced 766,700 mt of silicon-manganese alloy (SiMn alloy) in October, up 6.07% MoM and 5.68% YoY, according to SMM statistics. The combined EMM output in China from January to October stood at 8.32 million mt, a decrease of 7.46% year-on-year. According to SMM research, thanks to the decline in the prices of raw materials such as manganese ore and coke, the cost of SiMn alloy was reduced. The recovering profits lifted the operating rates of SiMn alloy producers in north China. However, the increase in the output was insignificant in south China as the costs still remained high. In November, although the bid price of mainstream steel mills has dropped month-on-month, it is close to the spot price. In this scenario, the market has no expectations for output cuts. Instead, with raw material prices falling and the profits of alloy factories restored, the output in November is expected to increase to 801,600 mt.

Magnesium ingot

SMM data shows that China magnesium ingot output stood at 79,000 mt in October, down 3.75% MoM and up 33.8% YoY. The output totalled 806,800 mt in the first ten months of 2022, a year-on-year increase of 28.68%. It is learned that due to the less-than-expected recovery of the downstream consumption in the high season, the magnesium inventory in magnesium plants stood high in addition to the high prices of raw materials such as coal and ferrosilicon. As a result, the profits of magnesium plants were squeezed so severely that some of them had no choice but to cut the production under the pressure of high inventory. In the meantime, the orders for magnesium alloy were lower compared with the previous month, which also affected the output of magnesium. Based on the current production plans of major magnesium plants, most plants prefer to maintain low operating rates under the influence of weak magnesium prices. It is estimated that the output of magnesium ingots in November will be 82,000 mt.

Magnesium alloy

China magnesium alloy output stood at 25,300 mt in October, down 9.44% MoM and up 46.11% YoY, according to SMM statistics. The accumulative output from January to October was 258,600 mt, down 7.07% from the previous year. The average operating rate of magnesium alloy producers stood at 44.67% in October, down 4.66 percentage points month-on-month and up 16.2 percentage points year-on-year. It is learned from domestic magnesium alloy enterprises that the weak downstream demand for magnesium alloy in October was the main reason for the MoM decline in output. The sluggish demand in the domestic market also led to weak expectations for the recovery of export orders. It is expected that under the influence of poor downstream consumption, the output of magnesium alloy in November will remain low at about 25,500 mt.

Magnesium powder

According to SMM data, China magnesium powder output stood at 6,500 mt in October, down 1.61% MoM, and the output totalled 69,000 mt in January-October. In October, the domestic magnesium powder production remained weak. Some magnesium powder enterprises revealed that the downstream market remained weaker in comparison with the same period of previous years due to the high prices of raw materials. In addition, the fourth quarter is a traditional off-season, when the operating rates of enterprises usually stay low. Therefore, it is expected that the domestic output of magnesium powder will remain unchanged at 6,500 mt in November.

PrNd oxide

Domestic output of PrNd oxide in October 2022 stood at 5,622 mt, down 0.78% on a monthly basis. The decline in output mainly came from Sichuan and Shandong provinces, with little change in other regions. The PrNd alloy was still in short supply in the spot market in October, but due to the resurging pandemic, the terminal demand was more sluggish, thus the PrNd oxide prices continued falling. In Sichuan, the PrNd oxide output was down about 1.24% MoM as plants carried out equipment maintenance and suffered losses caused by high raw materials costs. In Shandong, the severe pandemic precipitated 5.0% MoM drop in the PrNd oxide output. It is predicted that PrNd oxide output in November will be basically flat from October.

PrNd alloy

Domestic output of PrNd alloy in October 2022 stood at 5,149 mt, down 0.71% month-on-month. The main decrease in output resulted from Shandong province, while the output of other regions was flat from the previous month. In October, as the downstream demand was poor, the orders of leading magnetic material companies saw no palpable increase and the sales of metal factories dropped. The rare earth supply in the spot market was still tight, and the prices remained weak and stable. At the same time, the upstream and downstream enterprises all suffered losses, and some enterprises in Shandong and Sichuan began to reduce the production by a small amount. Although the Inner Mongolia was hit by the resurging pandemic, the local factories still maintained normal production. That is why the PrNd alloy output in October was basically the same as that in September. It is predicted that PrNd alloy output in November will continue to be flat from October.

Molybdenum concentrate

SMM data shows that in October 2022, the domestic molybdenum concentrate output increased 3% MoM to 19,400 mt. Although the CPC 20th Congress was convened in October in addition to environmental protection-related control and management, the ROM output of molybdenum was under limited impact, which ensured the stable output of molybdenum concentrates. At the same time, the molybdenum prices surged high in the first ten days of October, which lifted the operating rates of ferromolybdenum enterprises. This, in turn, provided the demand support for the production of molybdenum mines. The mining of molybdenum in some areas were restricted due to COVID-19 resurgence, but it had limited impact on the overall output since the capacity in these areas only took up a small market share. In conclusion, the output of molybdenum concentrate in October increased steadily. In November, despite that some companies have plans to overhaul, the output of molybdenum concentrate is likely to remain flat thanks to the restocking demand at the end of the year.

Ferromolybdenum

The domestic ferromolybdenum output in October was 18,600 mt, a substantial increase of 11% from the previous month, according to SMM statistics. In October, most ferromolybdenum enterprises maintained high operating rates throughout the month thanks to strong demand from steel mills, which was the major reason for the significant increase in ferromolybdenum output. Apart from that, owning to the high molybdenum prices in October, some smelting enterprises only accepted limited orders considering the costs, so their operating rates was constrained. At the same time, a small number of smelting enterprises in Shaanxi also reduced the operating rates for the pandemic, transportation disruption and other issues. Generally, the number of ferromolybdenum enterprises producing at full capacity was more than those cutting the production, hence the total domestic output of ferromolybdenum showed an upward trend. In November, since the stainless steel plants are likely to reduce the production, the orders of ferromolybdenum plants are not saturated. The output of ferromolybdenum is thus expected to decrease.

Silver

According to SMM survey, domestic silver output stood at 1,397.32 mt (including 1,194.32 mt of mineral silver) in October 2022, down 2.57% from the previous month. Manufacturers with increased silver production in October includes Henan Jinli Gold and Lead, Hunan Shuikoushan, Hechi Nanfang, Jiangxi Longtianyong, Chifeng Yuntong, and Inner Mongolia Xing'an Silver Lead. Some of them suspended the production in September and then resumed in October, while some enjoyed slightly higher sliver content in raw materials. However, more manufacturers cut their output in comparison, including Yunnan Copper, Tongling Nonferrous Metals, Shandong Zhaojin, Jinye Precious Metals, Mengzi Mining and Metallurgy, Zijin Mining, Guiyan Platinum, Shandong Fangyuan Nonferrous Metals, Jinlong Copper, etc. Altogether, the overall output was in a downward trend. SMM anticipates that silver production may increase slightly in November. On the macro front, the US Federal Reserve announced a 75 basis-point interest rate hike on November 3, which was in line with market expectation. Afterwards, Powell made a relatively hawkish speech, which slightly suppressed silver prices. On November 5, the US non-farm payroll data was released. The unemployment rate in October was 3.7%, higher than the previous reading and market estimate. After seasonal adjustment, US employers added 261,000 payrolls in October, lower than the previous reading but higher than estimate. Then silver prices rebounded after US Fed officials delivered a dovish speech.

Notes: SMM has released Chinese silver output since February 2021. The silver is usually produced along with copper, lead and zinc. Thanks to its high coverage of the base metals industry, SMM has successfully investigated a total of 45 silver production enterprises, which are located in 17 provinces across the country, with a total capacity of 24,000 mt and a total capacity coverage rate of over 99%.

Antimony ingot

According to SMM survey, China antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in October 2022 fell sharply MoM by 24.34% to 5,567 mt. In fact, the production of antimony has experienced ups and downs in recent months, which is attributed to the on-and-off production of many manufacturers. The high prices of antimony and its shortage still weighed on the market, but the impact seemed to be diminishing. Recently, the domestic demand for antimony oxide has been sluggish, which is reflected in the falling orders. The export orders of were poor as well. According to customs statistics, the export volume of antimony oxide as of September dropped significantly compared with the same period last year. The difficulty in selling antimony oxide in turn affected the consumption of refined antimony by antimony oxide manufacturers, so the prices of refined antimony prices also trended lower significantly. In particular, on the imminent CNY holiday, many manufacturers may begin to sell off to increase cash flow, which will exert more downside pressure on antimony ingot prices. Judging from the production situation of manufacturers in October, those who cut or suspended the output have increased. Among the 33 survey respondents in SMM research, 16 manufacturers stopped the production in October, up by 4 from the previous month; 13 reduced their production, up by 1 MoM; and 4 maintained normal production, 5 fewer than that in September. SMM predicts that the supply and demand of the domestic antimony market in October will remain basically unchanged under the current economic situation, and especially the sluggish demand is more than likely to extend. Yet, since many manufactures who have cut or suspended the production said that they plan to resume the production in November, it is expected that the domestic antimony ingot output in November may increase slightly.

Notes: SMM starts to disclose the output of antimony ingots (including antimony ingots, converted crude antimony, cathode antimony, etc.) since May 2022. Thanks to high coverage of the antimony industry, SMM has successfully investigated a total of 33 antimony ingot manufacturers, which are located in 8 provinces across the country, with a total capacity of nearly 20,000 mt and a total capacity coverage rate of over 99%.

Silver nitrate

The domestic silver nitrate plants with qualification certificates together produced 602 mt of silver nitrate in October, up 2.7% on the month. The total output of silver nitrate nationwide reached 633 mt. Among them, the output in central China increased 3.4% MoM, that in north-west China was down 5.9% MoM, that in east China was basically the same as the previous month, and that in south China advanced 15.4% on the month. Generally, the silver nitrate output in October climbed slightly because of the steady increase in the domestic demand for photovoltaic. Although the trading of silver was suspended during the National Day holiday, domestic manufacturers of silver nitrate, silver powder and silver paste all maintained normal production and shipment. In this case, output was affected during the holiday. Moreover, the output was boosted after the holiday as the downstream demand for photovoltaic was still robust. SMM also learned that the supply of some mainstream cells has been in short supply, while the expansion of cell production capacity is relatively slow, so SMM predicts that the demand for silver nitrate will remain stable in November.

Titanium dioxide

According to SMM, China titanium dioxide output stood at 316,600 mt in October, up 12.53% over the month and 0.22% over the year. The output totalled 3.21 million mt from January to October, a year-on-year increase of 2.95%. The increase in October was mainly contributed by large titanium dioxide plants who ramped up the output. In November, except for those large titanium dioxide enterprises who continue to enhance the production, other plants still maintain low operating rates. On the one hand, some factories have raised the quotations of their products, but the downstream buyers were generally reluctant to accept. Therefore, the titanium dioxide prices continued to hover at lows. On the other hand, the fourth quarter is the traditional off-season for the titanium dioxide industry. The consumption of coatings, the terminal application of titanium dioxide, has been curtailed due to the downturn in the real estate industry. As a result, the high inventory amid weak supply and demand weighed heavily on the prices of titanium dioxide. It is expected that titanium dioxide prices will remain weak, and the manufacturers will maintain low operating rates. Under these circumstances, the domestic output of titanium dioxide in November is estimated at about 320,000 mt.

APT

SMM data shows that the domestic output of APT in October dropped 3% on the month to 12,500 mt. In October, the terminal buyers in tungsten market only purchased on rigid demand. As the inventory of APT climbed higher and the bidding became more frequent in trading, the lower profit margin led to less purchasing of upstream raw materials. Consequently, the midstream smelting enterprises lowered their operating rates, who focused on the delivery of long-term orders. Eventually, stockpiling was rare, the spot market was quiet and the APT production was basically stable with a slight decline. In November, overseas demand and domestic stockpiling at the end of the year may become the main support for APT production. In this case, APT output is expected to remain stable. Lithium carbonate China lithium carbonate output in October stood at 34,168 mt, up 4% on a monthly basis and 87% on a yearly basis. Some lithium carbonate enterprises maintained normal operation as they managed to replenish their stocks with imported ore in a timely manner. But the average operating rate was low as the production of some top-tier plants was affected by overhaul. In addition, the low temperature in Qinghai resulted in a slight decline in the output of brine lake, so the overall supply was slightly tight. In November, the output has picked up with the completion of the above-mentioned overhaul. China lithium carbonate output in November is estimated to increase 9% on the month and 99% on the year to 37,294 mt.

Lithium hydroxide

China lithium hydroxide output in October was 26,020 mt, up 9% on a monthly basis and 55% on a yearly basis. The output of some manufacturers dropped slightly as their production lines were under shakedown test. Yet the overall production returned to the normal level as most manufacturers recovered from pandemic restriction. The output of some causticising plants remained high, contributing a slight increase in the overall supply. In November, some major smelters have maintained stable production and ramped up the output, so the overall supply of lithium hydroxide will remain flat from the previous month. It is forecast that China lithium hydroxide output will reach 26,129 mt in November, up 0.4% MoM and 54% YoY.

Cobalt sulphate

China cobalt sulphate output was 7,466 mt in metal content in October, a month-on-month increase of 10% and a year-on-year growth of 29%. Although the standard MB cobalt price was slightly lowered in October, the US dollar exchange rate still stood high due to the Federal Reserve’s raising interest rates. Since the costs of cobalt intermediate products remained high, the cobalt sulphate prices edged a little higher. On the supply side, the operating rates of cobalt salt enterprises were stable, and the production capacity of integrated precursor enterprises continued to climb. Therefore, the output of cobalt sulphate increased steadily. On the demand side, the demand for cobalt sulphate in October was higher than that of cobalt chloride. Thanks to the continued recovery of the demand for ternary precursors, the outsourcing demand of some integrated precursor enterprises increased. However, the growing demand was mostly for ternary precursors using medium and high-grade nickel batteries, which had less demand for cobalt sulphate compared with the 5-series precursors. It is expected that the demand for ternary precursors will rise further in November, and with the increase in the cobalt salt capacity of leading integrated precursor plants, the output of cobalt sulphate in November will be higher. The domestic cobalt sulphate output is anticipated to be 8,043 mt in metal content in November, a month-on-month increase of 8% and a year-on-year growth of 40%.

Tricobalt tetraoxide (Co3O4)

In October, the output of Co3O4 in China stood at 6,408 mt, down 2% MoM and up 1% YoY. Over the month, the prices of cobalt salts increased slightly and then stabilized, so the Co3O4 prices saw limited fluctuations. On the supply side, the explosive growth of Co3O4 production in September led to inventory backlogs in Co3O4 companies, who became cautious about production in October and adjusted the production plans according to actual operation. As a result, the Co3O4 output in October declined. On the demand side, the recovery of market demand for Co3O4 was slow in October, and downstream LCO companies only purchased based on actual orders at hand. As the rising prices of lithium carbonate lifted the cost of LCO, the MB standard refined cobalt prices started to pull back. LCO enterprises remained wait-and-see when it came to purchasing Co3O4. In November, the output of Co3O4 is estimated to recover and stand at 6,515 mt, up 2% MoM and down 10% YoY.

Ternary precursor

China ternary precursor output was 91,143 mt in October, a month-on-month increase of 3% and a year-on-year increase of 58%. On the supply side, some leading manufacturers ramped up the capacity, driving the output upward. Among them, the share of 5-series precursor output remained stable, while the share of 6-series rose thanks to its greater cost effectiveness. However, the share of high-grade nickel precursor output slid as the output in some manufacturers was lower than expected under the influence of nickel raw materials. On the demand side, overseas demand was stable. Since the subsidies for NVEs will be cancelled in 2023, the domestic auto makers stepped up the efforts to produce, which pushed up the demand for the 5-series and 6-series precursors. It is estimated that ternary precursor output will drop 4% over the month to 87,934 mt in November, a year-on-year increase of 50%.

Ternary cathode materials

China ternary cathode material output stood at 70,186 mt in October, up 4% MoM and 81% YoY. On the demand side, the electronics and e-bike sectors remained sluggish, while the power battery sector was boosted by the removal of subsidies for NEVs and the fact that no extra license plates were issued to plug-in hybrid vehicles (including extended-range ones). Therefore, the sales of power batteries continued to rise over the month. In October, based on the optimistic expectations that terminal enterprises would be busy stockpiling for production rush in the fourth quarter and on the bullish sentiment towards lithium salt prices, battery cell enterprises placed more orders for ternary materials than in September, which drove the output to increase slightly. On the supply side, ternary material companies basically maintained normal production during the National Day holiday. In addition, the new ternary material production capacity continued to be commissioned, contributing to sufficient supply. Looking ahead, the stockpiling demand has extended into November, so the overall output is expected to continue growing. China is expected to produce 73,577 mt of ternary cathode materials in November, up 5% MoM and 72% YoY.

Iron phosphate

The domestic iron phosphate output stood at 95,510 mt in October, up 8% on a monthly basis. On the supply side, the downstream LFP plants stepped up the production efforts to achieve annual target, which drove the iron phosphate output to increase. Most enterprises ran at full capacity as their orders were saturated, and the capacity of cross-industry enterprises also reached full. In this case, the high operating rates of the industry led to a tight balance in market. The output of iron phosphate once again broke through a new high of 90,000 mt. On the demand side, the downstream LFP plants had high purchasing demand for iron phosphate. However, there is uncertainty in the production scheduling of LFP plants in November as they started to face mounting cost pressure. As a result, they have become cautious in purchasing raw materials, and the tight balance in the market is expected to ease. The output of iron phosphate in November will reach 94,020 mt, down 2% from the previous month.

LFP

China LFP cathode material output was 123,317 mt in Octomber, a month-on-month increase of 10% and a year-on-year increase of 171%. On the supply side, the downstream enterprises were busy producing to meet annual goal. Therefore, to meet the downstream demand the top-tier LFP plants saw rising output, and the second-tier and cross-industry enterprises also put new capacity into operation and ramped up the capacity. On the demand side, it is currently the peak season for the sales of new energy vehicles. Moreover, the imminent removal of subsidies for NEVs and the boom in energy storage markets both at home and abroad all contributed to a sustainable growth in the downstream demand for LFP. However, the continuous tight supply of lithium salts has sent lithium prices skyrocketing. The higher costs of LFP therefore increased the cost pressure of some LFP plants. Considering the long production cycle, the growth rate of demand for LFP batteries from car makers may gradually slow down. It is expected that the LFP output will pivot in November, and it is estimated to reach 117,588 mt, down 5% month-on-month and 126% year-on-year.

LCO

China LCO cathode material output was 7,327 mt in October, up 6% over the month and 5% over the year. Although the release of new digital electronic products in October stimulated some market demand, the momentum of follow-up demand was slightly weak. The prices of new electronic products already dived amid the sluggish electronics market. On the cost side, Co3O4 prices stabilised after a slight increase, while the lithium carbonate prices kept growing due to its shortage, which rattled LCO producers and pushed up the prices of LCO. The production of LCO in leading enterprises increased significantly in October, but downstream LCO battery plants only purchased LCO as needed. In particular, the demand for electronics had not fully recovered, thus the high prices of LCO failed to be transmitted to terminal users. The increase in the LCO output in October might lead to accumulated inventories, and the LCO plants might adjust production arrangement accordingly. Given that the high costs of LCO will suppress the terminal demand, the LCO output in November is expected to decline. Specifically, the output of LCO in November is expected to drop 5% on the month and 1% on the year to 7,224 mt.

LMO

China LMO output stood at 6,186 mt in October, up 3% MoM and 5% YoY. On the supply side, the LMO market was busy stockpiling for the Double Eleven shopping festival. Most companies already received many downstream orders and began to arrange production to deliver. In addition, when the lithium salt prices rose sharply, most small and medium-sized enterprises raised their offers drastically on account of higher costs. As a result, orders were concentrated in top-tier enterprises whose offer remained unchanged thanks to lower costs. On the demand side, Double Eleven shopping festival and year-end restocking demand have boosted the market slightly. At present, the LMO prices are in an upswing but the actual terminal demand is still weak. Some enterprises have reported a slowdown in taking orders based on the expectations for an upsurge in LMO prices. It is expected that LMO output will slip 2% MoM and advance 3% YoY to 6,093 mt in November.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)