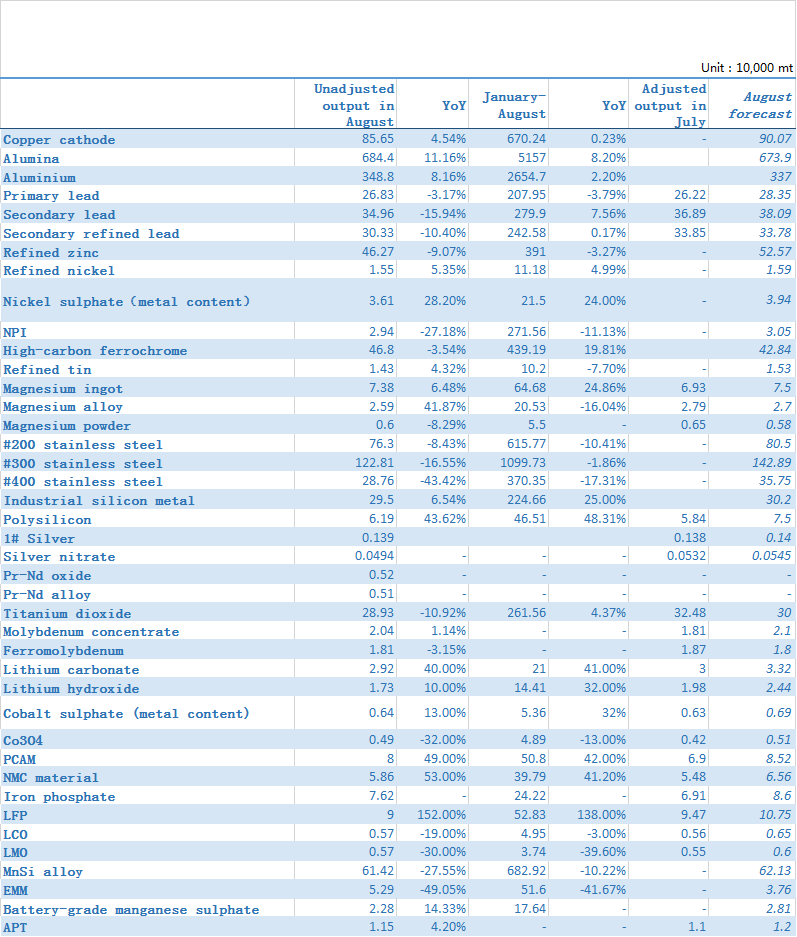

Copper cathode

China's copper cathode output stood at 856,500 mt in August, up 1.97% month-on-month and up 4.54% year-on-year.

The copper cathode output increased in August mainly due to the production resumption of some smelters and the capacity expansion of Fuye headquarters. However, according to production schedules at the beginning of the month, the output in August should have been 892,100 mt. The actual output was lower mainly owing to the impact of the high temperature and power cuts, tight supply of blister copper and the pandemic. Since the end of July, affected by the high temperature and the power rationing, the output in Anhui, Hubei, Jiangsu, Zhejiang and other provinces fell by a combined 21,000 mt. The output of domestic smelters was affected by the tight supply of blister copper and copper scrap. The production ramp-up plans of Jinchuan Co. and Xinjiang Xinjiang Wuxin Copper Industry were hindered. In August, the supply of blister copper continued to be tight. Although the shipment of copper scrap cargo holders increased, the supply of copper scrap was still tight. Therefore, the output of blister copper was limited. Due to the maintenance of LCS, the production disruptions of CCS in Africa, and local transportation limitation, the imported blister copper supply was extremely tight. In this scenario, the copper cathode output of domestic smelters was further affected. What's more, due to the pandemic in Guixi city, Jiangxi province, the output of local smelters declined by about 5,000 mt in August.

According to the production schedules in September, the impact of power cuts has eased, and the maintenance is also less intensive. The output of some smelters in north China that were in maintenance are expected to resume to normal level. The output of Fuye continues to increase as the newly expanded capacity is put into production. Therefore, the copper cathode output is expected to increase in September. However, the actual output may be limited by the pandemic and the tight supply of blister copper. According to the production schedules, China's copper cathode output in September is expected to be 900,700 mt, up 5.16% on the month and 12.18% on the year.

Alumina

Domestic metallurgical-grade alumina output in August (31 calendar days) was 6.844 million mt with an average daily output of 220,800 mt, down 1.4% on the month and up 11.16% on the year. The operating capacity of alumina was 80.583 million mt and the domestic average operating rate stood at 85%. In terms of regions, the total alumina output in Shandong province was 2.17 million mt, up 2.3% on the month. In Shanxi province, the total output stood at 1.698 million mt, a decrease of 5.5% compared with that in July. In Henan province, the total output was 789,000 mt, up 6.9% on the month. The total output in Guangxi province was 1.058 million mt, down 1.1% on the month. In Guizhou province, the total output stood at 461,000 mt, a decrease of 1.3% from July. The total output in Chongqing was 305,000 mt, down 18.2% on the month, and that in Hebei stood at 185,000 mt, a decrease of 5.1% from July. The output in other provinces was basically stable, with an output of 136,000 mt in Yunnan and 42,000 mt in Inner Mongolia.

On the whole, it is estimated that the net imports of alumina in August will be -50,000 mt. There was a slight surplus of 79,000 mt in the month, with a combined surplus of 878,000 mt in the first eight months of 2022. The alumina supply was not in significant surplus in August, alluding tightly balanced supply and demand. The output of alumina in September is expected to be 6.739 million mt, which is slightly lower than that in August. On the one hand, there are only 30 calendar days in September. On the other hand, environmental protection and safety inspections will continue as the 20th National Congress will be held in Beijing soon. Therefore, the operating rates of alumina enterprises in north China may decline.

Aluminium

According to SMM data, China produced 3.488 million mt of aluminium in August (31 calendar days), up 8.16% on the year. Although the output in Sichuan fell sharply in August, enterprises still produced some goods. Therefore, the daily output fell less significant by 112,500 mt. The output totalled 26.547 million mt from January to August 2022, an increase of 2.2% on the year. Companies like Gansu Liancheng, Guangxi Jili Baikuang, Guangxi Investment Group Yinhai resumed the production steadily. Among them, 380,000 mt of capacity owned by Gansu Liancheng was resumed and the new capacity of Gansu Zhongrui were put into operation. In August, the power shortage in Sichuan continued to intensify. Aluminium smelters in Sichuan were completely shut down, and the output fell about 920,000 mt. At the end of August, there was only 30,000 mt of capacity running in Sichuan. At present, the power shortage in Sichuan eased and the smelters started to resume the production, but it will take 2-3 months to resume to the level before the shutdown. In August, the capacity replacement of Guizhou Xingren Denggao was completed and Guizhou Yuanhao awaited commissioning. Therefore, SMM has raised the domestic installed aluminium capacity to 44.661 million mt. As of now, the domestic operating aluminium capacity was 40.828 million mt. The domestic operating rates stood at about 91.4% on average. According to SMM, the proportion of aluminium liquid in total production added 1.38 percentage points on the month to 68.02% in August.

In September, the supply of aluminium is uncertain. Guangxi Jili Baikuang, Guangxi Investment Group Yinhai, etc. may continue to resume the production. The new capacity of Guizhou Yuanhao and Inner Mongolia Baiyinhua may also ramp up. However, due to the insufficient water storage in Yunan, the power supply may be tight. Therefore, the output of aluminium smelters in Yunnan may decline. According to the capacity changes, SMM estimates that the domestic operating capacity of aluminium at the end of September may be 40.95 million mt. However, as the impact of production resumption is limited, the average daily output of aluminium in September will be lower than that in August. It is expected that the output in September may be around 3.37 million mt, an increase of 8.3% on the year. On the demand side, the domestic downstream enterprises was affected by the pandemic and power rationing in August. Therefore, the operating rates were low. According to SMM research, downstream orders have improved in September and the power rationing has also ended. In this scenario, the demand for aluminium may increase in September. It is expected that the domestic aluminium ingot inventory may decline slightly. SMM predicts that the domestic aluminium inventory may be around 650,000 mt by the end of September.

Primary lead

According to SMM research, China produced 268,300 mt of refined lead in August, up 2.34% on the month and down 3.17% on the year. The combined output in January-August declined 3.79% from a year ago. Production capacities of enterprises involved in the survey totalled 5.711 million mt in 2022.

Refined lead output increased slightly in August as expected. Due to the high temperature in the month, many places limited the industrial power use in favour of the civilian sector. Lead smelters in Hunan, Henan and other regions were asked to adopt the staggered production scheme or were provided with a fixed amount of power. Therefore, lead output fell. Meanwhile, there were still smelters resuming the production in August. For example, Chifeng Shanjin, Anhui Tongguan, and Yunnan Lead Oxide finished the maintenance and the output of Henan Wanyang increased after technical transformation. Therefore, the output of refined lead in August increased as a whole.

In September, smelters in Hunan and other places have resumed the production amid the cooling weather and the end of power rationing at the end of August. At the same time, the output of Xing'an Silver Lead, Hongqian Nonferrous and other enterprises continues to pick up following the maintenance. Therefore, the refined lead output is expected to increase in September. It is worth noting that since mid to late August, the SHFE/LME lead price ratio has risen, which is favourable to the import of lead concentrate. In this scenario, the tight supply of domestic lead concentrate will ease. In addition, the TCs of lead concentrate have finally stopped falling and rebounded. Among them, the TCs in Yunnan are quoted at 1,000-1,300 yuan/mt in metal content, and some at 1,400 yuan/mt in metal content. The increase in TCs of lead concentrate has provided support for the output increase of refined lead in September. According to SMM, domestic primary lead output in September is expected to increase by more than 10,000 mt to 283,500 mt.

Secondary lead

China produced 303,300 mt of secondary lead in August, down 10.4% from July, and down 21.2% on the year. The combined output in January-August rose 0.17% on the year. In August, the output of secondary refined lead decreased significantly on the month, mainly because the output of smelters in Anhui and Jiangsu declined by about 23,000 mt amid the power rationing. Meanwhile, the output loss due to equipment failure added up to nearly 16,000 mt in August. Some smelters in Anhui and Inner Mongolia resumed the production in July and produced normally in August, which brought some additional output. A smelter in Jiangsu gradually resumed to normal production in August, which also contributed part of the increase.

The domestic lead prices remained low since May. However, the battery scrap supply was tight, hence the prices of battery scrap remained high. Therefore, domestic secondary refined lead smelters generally suffered losses. In September, some smelters have reduced the production due to the huge losses. In addition, a smelter is currently undergoing technological transformation and upgrading and another smelter has reduced the production due to equipment failure. Some smelters will carry out maintenance around the Mid-Autumn Festival. According to research, some smelters in Anhui, Henan, Jiangxi, Jiangsu, Inner Mongolia, Shanxi and other regions are reducing the production. The output is estimated to decline about 2,400 mt per day firstly. After the Mid-Autumn Festival, some smelters will resume the production. Therefore, the output is expected to decline 1,400 mt per day by then.

Refined zinc

China's refined zinc output stood at 462,700 mt in August, down 13,200 mt or 2.77% on the month and 46,200 mt or 9.07% on the year. From January to August 2022, the combined refined zinc output stood at 3.91 million mt, a decrease of 3.27% on the year.

SMM survey showed that the domestic refined zinc output contracted in August and was far less than expected. The output increment was mainly brought about by some smelters in Gansu, Qinghai and Henan, which resumed the production. The output growth in Inner Mongolia was lower than expected due to the equipment failure. Hunan Haoyu started to produce in August, contributing part of the output increase. The capacity of Hunan Haoyu is now 60,000 mt/year and will gradually reach full production. The decline in output was mainly caused by the power cuts. Smelters in Sichuan and Hunan controlled or suspended the production for this cause. Some smelters in Guangxi reduced the production slightly due to maintenance.

China's refined zinc output is expected to rise 62,900 mt to 525,700 mt in September, up 13,800 mt and 2.69% on the year. From January to September 2022, the combined refined zinc output is estimated to be 4.435 million mt, a decrease of 2.6% year on year. The output is expected to increases as smelters in Sichuan and Hunan have resumed the production after the power rationing ended. Some smelters in Gansu, Guangxi and Inner Mongolia produce normally after the maintenance. Hunan Haoyu will release the output starting from September and October after put into production. The smelter will gradually reach full production and the highest monthly output will be 5,000 mt. The decrease in output is mainly caused by the overhaul of a large-sized smelter in Xinjiang.

Refined tin

Domestic refined tin output was 14,250 mt in August, up 186.14% on the month and 4.32% on the year. The combined output from January to August fell 7.70% on the year. In August, the domestic refined tin output increased significantly as expected due to the output release after the maintenance ended and suspended production of smelters was resumed.

By region: 1. The output of smelters in Yunnan increased sharply on the month. The mainstream smelters in Yunnan produced normally. Although the production of some smelters in September may be disturbed by the tight supply of raw materials, the current production has recovered to the level before the maintenance. 2. The output of smelters in Guangxi further increased on the month. Although the output recovery of some smelters in Guangxi was less than expected due to the tight supply of raw materials, the output increased stably. 3. The output of smelters in Jiangxi increased significantly on the month. The mainstream smelters in the region resumed the production and some finished products entered the market. Among them, some large-sized smelters produced smoothly, and were not affected by the tight supply of raw materials. Although some smelters have reported the problem of tight raw material supply, the impact is expected to be limited. 4. The total output of smelters in other regions increased significantly on the month in August. Overall, except for some smelters which resumed the production slowly due to the high temperature, others have basically resumed to the level before the maintenance.

In September, except for some smelters which resume the production slowly, other mainstream smelters in China now produce stably. At present, domestic tin prices are stable as a whole. Although the production of smelters is disturbed by the tight raw material supply, the smelters are still willing to produce amid the high conversion margins. To sum up, SMM expects the domestic refined tin output to increase further to 15,270 mt in September.

Refined nickel

China produced 15,500 mt of refined nickel in August, down 3.13% on the month but up 5.35% on the year. The pure nickel output declined slightly in August as expected. Due to the high nickel prices in August, the spot transactions weakened significantly, hence the social inventory rose 29% on the month. In addition, the demand for pure nickel from the nickel-based alloys sector lost 4.29% on the month in August. The demand for refined nickel from the stainless steel sector fell by 6.82% on the month as the output of 300-series stainless steel dropped 6.82%.

It is expected that the domestic refined nickel output will stand at 15,900 mt in September, up 2.58% on the month and 11.17% on the year. The output of refined nickel is expected to increase slightly in September, mainly because the output of 300-series stainless steel is expected to climb 9.76% on the month. In addition, due to the release of Indonesia NPI output, nickel prices are expected to fall in the long run. Therefore, the consumption of pure nickel in the alloy sector is expected to grow 1.89% on the month in September.

NPI

The domestic NPI output in August stood at 29,400 mt in Ni content, down 5.68% on the month and 27.18% on the year. Due to the off-season in August, the stainless steel market was sluggish, and the demand for raw materials was weak. In addition, due to the inflow of Indonesia NPI, the market supply was in huge surplus. The output of high-grade NPI stood at 22,500 mt (Ni content), down 9.91% on the month in August. The output of low-grade NPI was 6,800 mt (Ni content), up 11.63% on the month. Due to the overall supply surplus of NPI, the NPI prices fell in August, hence domestic NPI plants chose to suspend or reduce the production to reduce the risks amid the high costs and power rationing. In addition, the inventory of 200-series stainless steel declined obviously in August. As the profits recovered, the output of stainless steel increased, hence steel mills had more demand for low-grade NPI. Therefore, the output of low-grade NPI increased.

The output of NPI in China is expected to be 30,500 mt (Ni content) in September, slightly higher than that in August. On the demand side, the prices of stainless steel may rise slightly amid the bullish outlook. In this scenario, steel mills will have more demand for NPI compared with August, and the operating rates of domestic NPI plants will increase on the month. However, as the Indonesia NPI production lines have been put into operation continuously, the supply is still in surplus. Therefore, the increase of NPI prices will be limited in the short term under the supply pressure.

Nickel sulphate

China’s output of nickel sulphate was 36,000 mt in metal content in August, or 164,000 mt in physical content, up 20.6% on the month and up 28.2% on the year. In August, the output of battery-grade nickel sulphate increased significantly, mainly due to the rapid output growth of integrated large-sized factories. Amidst the good profit of MHP-based production lines in the early stage, some enterprises turned to use MHP as the raw material. The palpable output increase of high-grade nickel matte-based production lines also led to the increase in nickel sulphate output in August. In terms of raw materials, the proportion of nickel sulphate produced with high-grade nickel matte was about 28%, the proportion of hydrometallurgy intermediate products stood at 45%, and the proportion of nickel briquette was about 9%. The rest was produced by scrap and crude nickel. The output of battery-grade nickel sulphate increased significantly in August mainly due to the output increase of integrated plants. Therefore, the goods available in the market thinned and the prices of nickel salts rose in August. As the profits expanded, salt factories were more willing to produce.

In September, integrated manufactures will continue to release new capacities. Some nickel salt factories are expanding the production capacity, but the output will increase mainly in the fourth quarter this year and the first quarter next year. Therefore, the output in September is expected to add 9.2% on the month and 41.2% on the year due to the considerable profits. However, as the increase in MHP-based and high-grade nickel matte-based production capacity is insufficient, the output increase in September mainly comes from the nickel briquette-based production lines.

Battery-grade manganese sulphate

China's battery-grade manganese sulphate output stood at 22,800 mt in August, down 13.47% on the month. According to SMM research, due to the high inventory of manganese factories in the early stage, the ratio of inventory and sales stood at 1.29. Therefore, the prices of battery-grade manganese sulphate failed to increase. Mainstream manganese factories reduced the output intensively to control the prices. Large-sized manganese factories reduced the production more significantly, while the output of small and medium-sized manganese factories was the same as that in July. Overall, China's battery-grade manganese sulphate output dropped significantly in August.

At present, manganese factories have a strong willingness to hold the prices firm. Amid the restocking of battery enterprise and the increase in the demand for manganese sulphate, mainstream manganese factories will continue to reduce the production and digest the their inventory first in September. The output in September is expected to be about 21,300 mt.

High-carbon ferrochrome

SMM data showed that China's high-carbon ferrochrome output fell 92,600 mt on the month and 17,200 mt or 3.5% on the year to 468,000 mt in August. The output in Inner Mongolia was 292,700 mt, down 14,900 mt or 4.8% on the month. The output in Sichuan was 18,100 mt, down 53.6% on the month. In August, the output of stainless steel fell further, and some steel mills reduced their purchasing volume and even suspended the procurement of high-carbon ferrochrome. Therefore, the demand for ferrochrome further declined. In mid-August, due to the high temperature and insufficient rainfall in Sichuan, the civil power consumption surged while the power supply was in shortage. In this scenario, ferrochrome plants in Sichuan were asked to suspend the production to in favour of the civilian sector. Although the power rationing eased in late August, some ferrochrome plants did not resume the production due to the high costs. The prices of ferrochrome continued to fall in August, hence the ferrochrome plants reduced the production, and only produced for the long-term orders. As such, the supply of ferrochrome fell significantly.

The output of high-carbon ferrochrome in September is expected to stand at 428,400 mt, lower than that in August. The mainstream steel mills lower their purchasing prices of high-carbon ferrochrome in September, driving the retail prices to fall simultaneously. Meanwhile, the prices of chrome ore are stable due to the low port inventory, scarce sources, and the high spot costs. Therefore, the raw material costs of ferrochrome plants are very high. The large-sized ferrochrome plants in north China also suffer huge losses. In this scenario, Xin Ganglian plans to reduce the production, and many other ferrochrome plants plan to further reduce the production for maintenance. Therefore, the supply of ferrochrome will further decline. However, as the output of stainless steel has recovered in September, hence the surplus of ferrochrome may ease.

Stainless steel

According to SMM survey, the domestic stainless steel output in August totalled about 2.2787 million mt, down 3.87% on the month and 13.69% on the year. The output of 200-series stainless steel stood at 763,000 mt, down 16.65% YoY; 300-series 1.3199 million mt, down 14.29% YoY; 400-series 287,600 mt, down 43.42% YoY.

In August, the output of 200-series increased slightly and the output of 300 and 400-series further declined. In August, steel mills actively reduced the production and digested the inventory. Therefore, the inventory declined significantly and the supply and demand was balanced. The market experienced a short-term supply shortage at the end of August. In September, the output of 200, 300, and 400-series stainless steel will increase compared with August amid the production resumption. The profits of the three series will recover. The significant increase of 300-series output is mainly contributed by some large-sized steel mills. The production schedules of small and medium-sized steel mills are conservative. On the demand side, the consumption is expected to recover in September as the market sentiment has improved amid the peak season. But attention should be paid to the transmission. Among them, the output of 200-series in September will rise 5.5% on the month while the output of 300-series is expected to jump 16.35%. The output of 400-series is expected to add 24.3% on the month. Therefore, on the whole, the overall supply and demand of stainless steel will both increase slightly. SMM expects that the prices of stainless steel will increase in September amid cost support.

EMM

Domestic EMM output stood at 52,900 mt in August, down 48.91% on the month and 49.05% on the year, according to SMM statistics. The combined output in January-August totalled 516,000 mt, down 41.67% on the year. According to SMM research, at the end of July, the manganese industry alliance held a meeting to call on the EMM factories to maintain a 40% operating rate from August to December. EMM factories reduced the production due to the poor shipment and high inventory. In addition, in light of the weak terminal demand and the slow demand release of downstream stainless steel sector, the high-priced EMM was less preferred. Meanwhile, as the EMM prices rebounded, stainless steel plants mainly used other manganese alloys. As such, the demand for EMM declined. Overall, although the supply of EMM declined in August, the market was still in surplus. Therefore, the spot prices continued to decline, and the output of EMM dropped significantly.

In September, the EMM prices have exceeded 16,000 yuan/mt. However, due to the weak demand and sufficient supply, the prices are unlikely to remain high. Therefore, the market mainly purchases as needed and the demand is still weak. In addition, although some EMM plants will reduce the production for a lasting period of time in September, they are expected to resume the production in the middle of the month. However, a large-sized EMM plant is upgrading the equipment for environmental protection purpose. In this case, the EMM output in September is expected to be about 37,600 mt.

Industrial silicon metal

The domestic silicon metal output stood at 295,000 mt in August, down 7.5% on the month and up 6.5% on the year, according to SMM statistics. China’s industrial silicon metal output totalled 2.2466 million mt in January to August, a year-on-year increase of 25%. Xinjiang and Sichuan, two of the major supplying regions of industrial silicon metal in China, were affected by the pandemic and power rationing in August, the output of the two provinces declined by around 35,000 mt in August. Meanwhile, the output in Yunnan, Guizhou, Henan and other places increased slightly in August. Nonetheless, with the ease of the pandemic in Xinjiang and the recovery of the production in Sichuan, the supply of industrial silicon metal is expected to resume in September. However, due to the power shortage in Yunnan, the production of silicon factories may be affected amid the expected power rationing. Therefore, the output in September is uncertain. It is expected that the output of industrial silicon metal may stand at around 300,000 mt in September.

Polysilicon

SMM statistics show that the domestic output of polysilicon stood at 61,900 mt in August, up 5.99% on the month and marking the first positive growth after falling for two months. The main reason for the increase was that the output increase contributed by newly commissioned enterprises or enterprises that resumed the production was larger than the output loss caused by power rationing in Sichuan. Specifically, the output of the three polysilicon plants in Sichuan, namely Leshan GCL, Sichuan Yongxiong and Yongxiang New Energy, was far below expectations, with output loss of about 5,000 mt. On the contrary, the production resumption of manufacturers like Xinjiang Daqo New Energy, GCL and Inner Mongolia Xinte, as well as the capacity ramp-up in Inner Mongolia Tongwei and Qinghai Lihao brought more increase in output. SMM expects that the output of polysilicon will reach about 75,000 mt in September with the end of power rationing and the following release of production capacity.

Silicon-manganese alloy

SMM data shows that China produced 614,200 mt of silicon-manganese alloy (SiMn alloy) in August, down 9.82% MoM and 27.55% YoY. The combined output in January-August totalled 6.8292 million mt, down 10.22% from the previous year. According to SMM survey, there are two reasons behind the MoM drop in SiMn alloy output. First, the second round of coke price hike pushed up the costs of SiMn alloy, but the spots mainly traded at low prices. Therefore, the huge losses of manufactures led to lower operating rates. Second, the production resumption of steel mills was slower than expected due to power rationing and rising steel scrap prices. The market traders were cautious about purchasing, and the demand for SiMn alloy remained sluggish. On the whole, despite the weak supply and demand, the relatively huge stocks of SiMn alloy spots still led to an oversupply in August. Meanwhile, the SiMn alloy output dipped on a monthly basis under the pressure of poor sales.

In September, the raw material prices are less firm, indicating a further decline in SiMn alloy costs. If so, the profits of manufacturers might be repaired. Moreover, the increase in downstream pig iron output might lift the demand for SiMn alloy, thus the output of SiMn alloy is estimated to increase to 621,300 mt in September.

Magnesium ingot

China's magnesium ingot output stood at 73,800 mt in August, up 6.48% MoM and 30.57% YoY, according to SMM statistics. The output totalled 646,800 mt from January to August 2022, a year-on-year increase of 24.86%.

According to SMM survey, as magnesium plants in the main producing areas successively completed the maintenance, the market supply has increased. While at the same time, some plants have cut the production due to the recent downturn in magnesium prices. According to the current production schedules, the magnesium market is expected to pick up with the prospect of a traditional peak season. It is estimated that the production of magnesium ingots will rebound continuously to 75,000 mt in September.

Magnesium alloy

China's magnesium alloy output stood at 25,900 mt in August, down 7.26% MoM and up 41.87% YoY, according to SMM statistics. The accumulative output from January to August was 205,300 mt, down 16.04% from the previous year.

The average operating rate of magnesium alloy industry stood at 45.62% in August, down 7.26% on the month and up 35.21% on the year. In August, the downstream orders for magnesium alloys were relatively weak, leading to a slide in the operating rates of magnesium alloy plants. A salesperson of a large magnesium alloy plant said that the recent overseas orders were poor because inquiries from the European downstream enterprises were rarely heard due to the energy crisis. Therefore, despite the traditional peak season in September, the recovery of the magnesium alloy market will be relatively limited. It is estimated that the output of magnesium alloys in September will add slightly to 27,000 mt in total.

Magnesium powder

China's magnesium powder output stood at 6,000 mt in August, down 8.29% MoM, and the output totalled 55,000 mt in January-August 2022.

The domestic magnesium powder production maintained a downward trend in August as some magnesium powder factories saw sharp decline in orders due to the weak demand of domestic and overseas steel mills. The person in charge of a large magnesium powder factory commented that the downstream steel market remained sluggish and the demand for magnesium powder dropped steeply. As a result, some magnesium powder plants halted the production, weighing hefty on the average operating rate. Considering that the demand is unlikely to recover in the short term, it is expected that the magnesium powder market will remain sluggish in September with an estimated output of 5,800 mt.

PrNd oxide

Domestic output of PrNd oxide in August amounted to 5,160 mt, down 10% month-on-month. In terms of the final output, the outputs in Jiangxi, Inner Mongolia, Sichuan, Guangdong and Guangxi fell by 390 mt, 110 mt, 100 mt, 78 mt and 56 mt respectively. In terms of the amount of decline, the outputs in Guangxi, Guangdong, Jiangxi and Sichuan were down 56%, 52%, 20% and 14% respectively from the previous month. The domestic supply of PrNd oxide in August was modest, while the downstream demand decreased significantly. The separation plants remained bearish towards the PrNd oxide prices. Many small and medium-sized PrNd oxide producers, whose products were mainly sold in the spot market, slashed the output or even suspended the production, while some producers who sold products under long-term orders generally maintained stable production. But plenty of PrNd oxide enterprises in Jiangxi were greatly affected by the market volatility. The power rationing in Sichuan and Jiangsu had limited impacts on local PrNd oxide enterprises, whose production has resumed gradually after one or two weeks of suspension. Although the prices of both rare earth ores and PrNd oxide retreated, separation plants still suffered losses and reduced the purchase of raw materials. The imports of raw ore from Myanmar already recovered from the closed customs in August, contributing to a stable supply of rare earth ores domestically.

PrNd alloy

Domestic output of PrNd alloy in August stood at 5,118 mt, up 4.55% month-on-month. The increase mainly came from the production growth in Inner Mongolia, while the output in Sichuan was down from a month ago. In August, major magnetic materials factories received slightly shrinking orders, but the average operating rate and sales were stable. Small and medium-sized enterprises saw a slight year-on-year decline in order, while downstream magnetic material enterprises were less willing to purchase PrNd alloy amid falling rare earth prices. Altogether, the orders of metal factories saw a decline. As some enterprises in Inner Mongolia ramped up the output in August, the overall PrNd alloy output there gained 16.24% on the month. In contrast, some metal factories in Sichuan halted the production due to power rationing, covid-19 pandemic outbreak and poor orders, and the PrNd alloy output in Sichuan contracted 19.23% month-on-month. The Pr-Nd alloy output in September is expected to inch slightly higher.

Molybdenum concentrate

SMM data shows that the domestic molybdenum concentrate output in August stood at 20,390 mt, an increase of 1.14% from the previous month. It is learned that most mines maintained stable operation in August with booming enthusiasm thanks to the robust downstream demand for ferromolybdenum. Some small private mines halted the mining activities for environmental protection checks, but the output losses were offset by the produciton of mainstream mines who was running at full capacity. Thus, the overall Molybdenum concentrate output climbed steadily.

Ferromolybdenum

The domestic ferromolybdenum output in August was 18,140 mt, a drop of 3.15% from the previous month, according to SMM statistics. In August, more steel mills resumed the operation while the stocks of ferromolybdenum, one of the important raw materials, were not sufficient, thus there was robust demand for ferromolybdenum from steel mills, which facilitated its table production. The nearly 3% month-on-month decline in output was attributed to two reasons. First, some smelters were still under maintenance with no output. Second, some smelters were unable to maintain normal production due to inadequate raw materials, thus the growth in output was rather limited. Generally, the ferromolybdenum output was fairly stable under the support of strong terminal demand.

Silver

According to SMM survey, the domestic silver output stood at 1,386.33 mt (including 1175.33 mt of mineral silver) in August, up 0.49% from the previous month. The output varied in different plants, but the overall output rose slightly on the month. On the macro level, the US private payrolls grew by 132,000 in August, lower than the expectation of 300,000. The US unemployment rate rose to 3.7% in August of 2022, above market expectations of 3.5%, while the previous print was 3.5%. This marked the first time in the past five months that the unemployment rate in US has increased. After seasonal adjustment, U.S. employers added 315,000 payrolls in August, slightly above expectations of a gain of 300,000 jobs. The figure in the previous month was 528,000. In fact, the seasonally-adjusted non-farm payrolls in the United States saw the slightest increase in this August since April 2021. At the 2022 FOMC meeting, Cleveland Fed President Loretta Mester delivered a speech on the U.S. economic outlook, and once again stressed the Fed’s determination to raise interest rates. Instead of expecting interest rate cuts next year, she was in favour of raising interest rate to above 4% before the early 2023. In terms of the production of domestic silver manufacturers, a few manufactures, such as Henan Jinli Gold and Lead, Hunan Yuteng, Hunan Shuikoushan, Shandong Zhaojin and Hechi Nanfang, reported slight increase in August. Basically few manufacturers cut their production significantly. In terms of enterprises with increased output, such as Chifengshan Gold, Silver and Lead, Hongqian Non-ferrous, Chifeng Yunnan Copper, Guiyan Platinum, Zijin Mining, and Henan Yuguang Gold Lead, etc., their increase was not large as well. Therefore, the overall output of domestic silver output was basically stable in August with a slight increse. It is expected that the domestic silver production will continue to grow at a low speed in Septebmer.

Antimony ingot

According to SMM survey, China’s antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in August 2022 fell significantly by 30.89% month-on-month to 5,098 mt. On the whole, the high antimony prices and enduring tight supply of raw material remained the major reasons behind the production suspension or reduction of domestic refined antimony smelters. In recent months, the domestic demand for antimony products, especially the antimony oxide, has been sluggish, and the export orders have also shrunk significantly. As a result, antimony oxide manufacturers held back from purchasing refined antimony, which dampened the enthusiasm of antimony ingot manufacturers and some of them have reduced the production. Judging from the production situation in August, basically all the manufacturers that SMM had investigated either cut or suspended the production. The number of operating manufacturers fell month-on-month. Among the 33 survey respondents, the manufacturers who suspended the production in August lost one to 13 compared with July; 15 diminished their production, a month-on-month increase of two, and 5 maintained normal production. For example, Flash Star Antimony, one of the largest antimony producers in China, stopped its antimony production again on July 25, 2022, with all its blast furnaces and antimony white furnaces shut down. The output of the enterprise in August was zero, and the resumption time has not yet been determined. At the same time, more than half of the manufacturers under SMM investigation saw decline in August compared with the previous month, which was why the overall output in August slumped 30.98% on the month. SMM predicts that the supply and demand of the domestic antimony product market in September will remain basically unchanged under the current economic situation, especially, the weak demand will extend. Given that the operating rates of plants already stand at a fairly low point, the domestic antimony ingot production in September will be flat from August, but the potential of further decline still exists.

Notes: SMM starts to disclose the output of antimony ingots (including antimony ingots, converted crude antimony, cathode antimony, etc.) since May 2022. Thanks to high coverage of the antimony industry, SMM has successfully investigated a total of 33 antimony ingot manufacturers, which are located in 8 provinces across the country, with a total capacity of nearly 20,000 mt and a total capacity coverage rate of over 99%.

Silver nitrate

The silver nitrate sales entered the off-season in August, when the output of domestic silver nitrate producers with qualification certificates fell 7% from July to 494 mt. The decline mainly resulted from its high prices in the first half of the month and limited demand. According to SMM survey, the silver nitrate output in central China and northwest China shrank 13% and 3% respectively, while that in south China added 22% because of concentrated purchase. There are three explanations for the output decline. First, the silver nitrate prices trended higher in the first half month of August, but downstream enterprises had already restocked it aggressively in July, so the inventory barely saw any decline in August. Second, the power rationing in Sichuan suppressed the demand for photovoltaics, inducing a weak demand for upstream raw materials. Meanwhile, some manufacturers were on a summer break. Third, the transportation was hindered due to pandemic lockdown in Sichuan and other regions, thus enterprises stopped purchasing raw materials.

SMM expects that the silver nitrate output in September will improve with pandemic under control and the end of power rationing.

Titanium dioxide

According to SMM, China's titanium dioxide output stood at 289,300 mt in August 2022, down 10.92% from the previous month and 4.33% from the previous year. The output from January to August increased 4.37% year-on-year increase to 2.6156 million mt.

According to SMM survey, the operating rates of domestic dioxide enterprises fell considerably in August due to sluggish demand and power rationing policy. A salesperson of a large titanium dioxide enterprise revealed that with the lift of power rationing, the supply of titanium dioxide is expected to return to normal, but the current downturn in the market and the weak support from the supply side still weigh on the enthusiasm of titanium dioxide enterprises. In this case, the titanium dioxide production in September is expected to rise slightly to 300,000 mt.

APT

The domestic APT output in August was 11,490 mt, up 4% on a monthly basis, according to SMM statistics. The overall APT supply increased in August with the completion of maintenance in some smelters and the growth in ROM supply. However, some production lines were still under shakedown tests after upgrading, hence the output had not returned to a normal level in spite of the production resumption. Moreover, most smelters had unsaturated raw material inventory due to previous losses, which was only enough to deliver long-term orders, hence the APT output just added slightly in August.

Lithium carbonate

China’s lithium carbonate output stood at 29,150 mt in August, down 4% MoM and up 40% YoY. Lithium carbonate manufacturers in Sichuan were affected by power rationing amid high temperatures, and some manufacturers maintained low operating rates owing to tight raw material supply, thus the overall supply of lithium carbonate remained unchanged. Meanwhile, capacity of some companies was not fully released as the production lines were under shakedown test. The production from salt lakes proceeded as usual, though the transportation was hindered under the impact of pandemic. In September, the output gradually picked up with the lift of the power rationing policy. Some manufacturers also increased their new production capacity, contributing to the month-on-month growth in overall lithium carbonate output. China lithium carbonate output in September is estimated at 33,194 mt, up 14% on a monthly basis and up 67% on a yearly basis.

Lithium hydroxide

China’s lithium hydroxide output amounted to 17,316 mt in August, a MoM decrease of 13% and a YoY growth of 10%. As plenty of lithium hydroxide producers are located in Sichuan where the power rationing policy was introduced to fight against soaring temperatures, the output of lithium hydroxide dropped significantly in August. In addition, the operating rates of some manufacturers stayed low amid alternate maintenance of production lines, while both smelters and causticising plants were forced to restrict the production due to power rationing, prompting the overall output to drop further. In September, the overall supply has recovered with the removal of power rationing in Sichuan and the completion of maintenance in some manufacturers, thus lithium hydroxide output is expected to return to its peak. Domestic lithium hydroxide output is estimated to rise 41% MoM and 48% YoY to 24,417 mt in September.

Cobalt sulphate

China cobalt sulphate output was 6,423 mt in metal content in August, a month-on-month increase of 2% and a year-on-year growth of 13%. In terms of raw material costs, as overseas summer break drew to an end in late August, MB prices inched higher continuously, adding to the cost of cobalt intermediate products. Meanwhile, the price coefficient of NMC battery scrap recently jumped boosted by the rising lithium carbonate prices, thus the cost of recycled materials also increased. On the supply side, the output of large-scale cobalt salt manufacturers was restricted due to power rationing amid high temperatures across the country in August; smelters that use recycled materials also curtailed the production due to high costs; integrated precursor enterprises consumed more in-house cobalt salt in August. Therefore, the increase in supply was less than expected. On the demand side, the demand for the ternary precursor continued to recover in August. In addition, there were rumours of government stockpile plan in the early and mid August, which, coupled with the high costs of cobalt intermediate products and recycled materials, prompted the prices of cobalt sulphate to rally. The downstream buyers were more willing to restock cobalt sulphate amid bullish sentiment. Therefore, the demand for cobalt sulphate has increased. It is expected that with the lift of power rationing and the continuous increase in the demand for precursors, the production of cobalt sulphate in September is likely to grow further. The domestic cobalt sulphate output is forecast to be 6,948 mt in metal content in September, a month-on-month increase of 8% and a year-on-year growth of 30%.

Tricobalt tetraoxide (Co3O4)

The domestic output of Co3O4 in August rose 17% on the month and fell 32% on the year to 4,934 mt. The market sentiment was elevated amid the rumours of government stockpile plan in the early and mid August. On the raw material side, Co3O4 manufacturers raised the offers as the rising cobalt salt prices elevated the cost. In late August, the downstream buyers restocked amid the bearish sentiment, and the market activity increased compared with July. On the supply side, the production of leading enterprises gradually returned to normal levels in August, thus the supply of Co3O4 increased. On the demand side, thanks to the increase in the prices of cobalt salt and Co3O4 in August, LCO companies increased the purchase of Co3O4 in the middle and late August, though the purchase volume was still based on the expectation of the order increase in September. In September, launches of new mobile phones will lead to higher demand for the upstream raw materials, thus Co3O4 manufacturers are expected to schedule more production in September compared with August. The output of Co3O4 is estimated at 5,130 mt in September, down 4% MoM and 18% YoY.

PCAM

The domestic PCAM (precursor of cathode active materials) output was 80,000 mt in August, a month-on-month increase of 16% and a year-on-year increase of 49%. On the supply side, with the production capacity of major precursor plants growing in August, the output of PCAM rose sharply, led by the 5-series and 8-series. On the demand side, domestic leading power battery manufacturers placed more orders for 5-series, which, coupled with the recovery in the demand for digital products, boost the demand for 5-series. Meanwhile, the consumption of 8-series also went up thanks to the growing demand from the American market. It is expected that both domestic and overseas demand will extend the increase in September, thus the output of PCAM is estimated to rise 7% on the month and 61% on the year to 85,200 mt in September.

NMC cathode materials

China’s NMC cathode material output stood at 58,598 mt in August, a month-on-month increase of 6% and a year-on-year increase of 53%. As production of some enterprises located in Sichuan and Jiangsu were affected by the power rationing, the actual output of NMC cathode materials in August was slightly lower than the predicted value in early August. In particular, the share of NMC 5-series and 6-series cathode material output increased while that that NMC 8-series dropped slightly. On the one hand, the normal production resumed in auto manufacturers and battery manufacturers with the end of power rationing, and the demand improved steadily. On the other hand, automobile and battery manufacturers have started to restock for the production in the third and fourth quarters to meet annual targets. Therefore, the demand from motive power market is expected to rise, and that from digital product market is expected to advance slightly, contributing to an upward trajectory in the overall demand for NMC cathode materials. The NMC cathode material output is forecast to reach 65,567 mt in September, up 12% MoM, and the downstream purchase demand is likely to trend higher.

Iron phosphate

The domestic iron phosphate output stood at 76,163 mt in August, up 10.7% MoM. The production capacity of iron phosphate continued to ramp up in August. Some start-ups completed the shakedown tests successfully, and contributed to a significant increase in output of iron phosphate as well as the shipment downstream. Despite the impact of power rationing in Sichuan on the production of LFP, the newly released production capacity of LFP and downstream restocking prompted most traditional LFP manufactures to produce at full capacity, thus the supply was on the rise. The domestic iron phosphate output is estimated to increase 13% MoM to 86,061 mt in September.

LFP

In August, 90,050 mt of LFP was produced in China, up 152% from the previous year and down 2.4% from the previous month. On the supply side, the key production lines in many major LFP enterprises were forced to be suspended due to the enduring power rationing in Sichuan, leading to a slump in the local LFP output. Fortunately, first- and second-tier manufacturers continued to ramp up their capacity to raise the overall production capacity, thus the overall LFP supply only slide slightly. On the demand side, the terminal demand stayed high in August, when the approaching end of the third quarter drove battery and automobile enterprises to restock for the production in the quarter to meet the annual output targets. Generally, the demand for LFP is still in an upward trend. It is expected that LFP output will reach 107,538 mt in September, an increase of 183% YoY and 19% MoM.

LCO

The domestic LCO cathode material output stood at 5,663 mt in August, up 1% from July and down 19% from the previous year. On the cost side, Co3O4 prices rebounded slightly amid the rumours of government stockpile plan, and lithium carbonate prices also rose owing to the power rationing in Sichuan. As a result, LCO prices went up with growing costs. On the supply side, the total output of LCO cathode material in August was flat from July, but the output of leading LCO cathode material enterprises increased slightly, adding to the supply marginally. On the demand side, with upcoming launches of new mobile phones in September, terminal consumers placed more orders in August and September than those in July. In consequence, the LCO battery plants purchased more LCO cathode materials amid bearish sentiment towards cobalt and lithium prices as well as the improving demand. However, the overall supply of cobalt was in a surplus, and the demand from the digital market still failed to return to the level in the same period of last year, thus the imbalance between supply and demand sustained. Given the launches of new mobile phones in September, the market demand is expected to rise, so the output of LCO cathode material is likely to inch higher. Therefore, the output of LCO cathode material is expected to rise 15% on the month and drop 5% on the year to 6,531 mt in September.

LMO

China’s LMO output stood at 5,716 mt in August, down 30% YoY, but up 5% MoM. In terms of supply, LMO prices have risen but the increase was less than that in the raw material costs, therefore the continued losses weighed on the operating rates of many manufacturers. In terms of demand, previously downstream buyers aggressively restocked low-priced LMO, thus the purchase declined in the middle of August. Currently, many manufacturers mainly focus on delivering the previous orders and new orders tend to be concentrated in leading manufacturers with low offers. It is estimated that LMO output in September will amount to 5,995 mt, down 17% YoY and up 5% MoM.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)