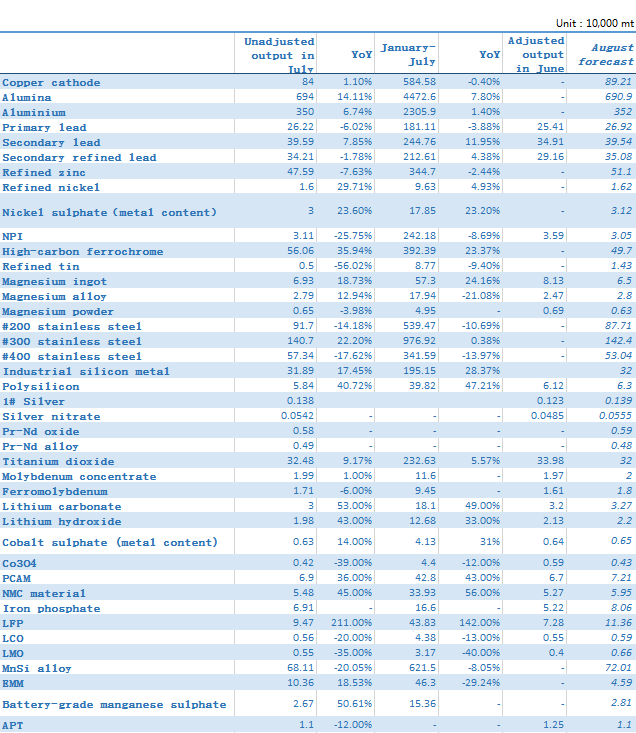

Copper cathode

China produced 840,000 mt of copper cathode in July, down 2.5% on the month and up 1.1% on the year, according to SMM statistics.

Overall, domestic smelters were still under maintenance in July. The output of Jinchuan, Nanguo and Chifeng Jintong Copper was significantly affected by the maintenance. However, the decline in copper cathode output was mainly caused by the individual technical upgrade and the tight supply of blister copper, anode and copper scrap. The supply of copper concentrate was relatively sufficient, and the spot TCs remained at $72/mt-$72/mt. With the increase of copper inventories at some ports, the TCs showed signs of picking up. Due to the rapid decline in overseas sulphur prices, the domestic sulphuric acid prices fell by nearly 50% in July. However, the profits of smelters were still relatively considerable. At the same time, the tight supply of blister copper, anode and copper scrap greatly restricted the production of smelters. The domestic blister copper supply was tight and will remain so in the short term mainly due to the rapid decline in copper prices that resulted in the shortage of copper scrap. In terms of imports, as LCS took a two-month maintenance since early July, the output fell by about 20,000 mt. In addition, the output was further reduced as CCS was overhauled for 10 days due to the leak problem and the production of Kansanshi was unstable.

According to the production schedules in August, except for the short-term extension of the maintenance plan and the technical renovation of a few smelters, most smelters have resumed the production. With the commissioning of the headquarters of Fuye, the output is expected to reach 900,000 mt. However, the market players should pay attention to the impact of tight blister copper supply on copper production. SMM expects that the domestic copper cathode output in August will stand at 892,100 mt, up 6.2% on the month and 8.9% on the year.

Alumina

Domestic metallurgical-grade alumina output in July (31 calendar days) was 6.94 million mt with an average daily output of 223,900 mt, up 2.97% on the month and 14.11% on the year. The operating capacity of alumina was 81.71 million mt and the domestic operating rates stood at 87% on average.

In terms of regions, the total alumina output in Shandong province was 2.12 million mt, flat from June. In Shanxi province, the total output stood at 1.798 million mt, a slight increase of 2% compared with that in June. Due to the tight supply of raw materials and high prices, the profits of alumina plants were squeezed, hence the operating rates rarely increased. In Henan province, the total output was 738,000 mt, up 6% from June. The enterprises in Henan province, like those in Shanxi, mainly produced for the long-term orders, and were less interest in retail sales. The total output in Guangxi province was 1.07 million mt, up 6% on the month. Due to the production resumption of aluminium in Yunnan province, the demand for alumina increased. Therefore, the operating rates of alumina refineries in Guangxi remained at around 95%-100%. Although the enterprises were willing to produce, they mainly focused on the long-term orders. Therefore, there were few sources available in the market. In Guizhou province, the total output stood at 467,000 mt, an increase of 3% from June. Although the local ore supply increased slightly, the enterprises barely maintained normal production. The reliance of raw material supply determines the stability of local production. With the release of new capacity in Chongqing city and Hebei province, the output across these two provinces increased. Among them, the total output in Chongqing was 373,000 mt, up 3% on the month, and that in Hebei stood at 195,000 mt, an increase of 11% from June. The output in other provinces was basically stable, with a total output of 136,000 mt in Yunnan and 42,000 mt in Inner Mongolia.

On the whole, it is estimated that the net imports of alumina in July will be -100,000 mt. There will be a slight supply surplus of 103,000 mt in the month, and a surplus of about 578,000 mt during January-July. At present, the alumina market experiences both production reduction and the release of new capacity. At the same time, it is rumoured that an alumina plant in Shanxi may suspend the production (involving 3 million mt of alumina capacity) in August. In this scenario, the supply is expected to gradually change from huge surplus to a tight balance. The market will gradually restore the balance between supply and demand through the wresting between the supplier and buyer and SMM will continue to pay attention to the production reduction and the release of new capacity.

Aluminium

According to SMM data, China produced 3.5 million mt of aluminium in July (31 calendar days), up 6.74% on the year. The daily output stood at 112,900 mt, up 862 on the month and 7,113 mt on the year. The output totalled 23.059 million mt from January to July 2022, an increase of 1.4% on the year. In July, the total domestic operating capacity of aluminium continued to increase. The resumption of production and the release of new capacity in Gansu province and Yunnan was stable, while the production resumption in Guangxi slowed down. Due to the power shortage and other problems, the combined output in Sichuan and Shandong province declined about 70,000 mt. As of early August, the domestic operating aluminium capacity has reached 41.405 million mt, with the installed capacity at 44.475 million mt, hence the average operating rate stood at 93.1%. The proportion of aluminium liquid in the production protfofio of domestic aluminium smelters was stable. Some smelters adjusted the proportion according to the market dynamics. According to SMM, the proportion of aluminium liquid increased merely 0.2 percentage point on the month to 66.64% in July.

In August, Gansu Liancheng, Jili Baikuang, Guangxi Investment Group Yinhai, etc. will continue to resume the production. In addition, the new projects led by Gansu Zhongrui and Guangyuan Zhongfu will reach full production and the capacity replacement project in Yunnan also proceeds steadily. But due to the production reduction in Sichuan and Shandong in July and the overhaul of a smelter in Henan, SMM expects that the domestic aluminium operating capacity will reach 41.59 million mt by the end of August, and the aluminium output in August is expected to be around 3.52 million mt, a year-on-year increase of 9%.

On the demand side, according to SMM research, the new orders of domestic aluminium sheet/plate and strip and aluminium extrusion, especially construction extrusions, declined in August. Therefore, the operating rates are unlikely to pick up significantly, but the aluminium supply will still increase. As the inventory of domestic aluminium ingots and aluminium rod may continue to increase in August, SMM expects that domestic aluminium inventory may stand at 750,000 mt by the end of August.

Primary lead

China produced 262,200 mt of refined lead in July, up 3.18% MoM and down 6.02% YoY. The combined output in January-July declined by 3.88% on the year. Production capacities of enterprises involved in the survey totalled 5.711 million mt in 2022.

According to the survey, the output in July increased as expected after most smelters finished the maintenance. Chifeng Shanjin, Anhui Tongguan, Yunnan Mengzi and other enterprises resumed the production from maintenance, and Yongning Gold Lead resumed after technical transformation. Therefore, the overall lead output increased. However, it is worth noting that the actual increase in output in July was less than expected, mainly due to the tight supply of lead concentrates. In addition, as the lead prices fell below $1,800/mt in July, the TCs fell and some miners even quoted $5/dmt. Meanwhile, the supply of ores in Yunnan was tighter, as some enterprises reduced the production.

Refined lead output is expected to increase slightly in August. The lead smelters, such as Chifeng Shanjin, Anhui Tongguan, and Yunnan Lead Oxide have finished the maintenance, which contributes to the major increase in output. In addition, the output of Henan Wanyang will also rise after its technical transformation. Therefore, the output of refined lead in August is expected to climb by more than 10,000 mt. But Xing'an Silver Lead will start routine maintenance. Overall, SMM expects that the domestic refined lead output will grow to 269,000 mt in August.

Secondary lead

China produced 342,100 mt of secondary refined lead and alloy in July, up 7.99% on the month and 1.78% on the year. The combined output in January-July increased by 4.38% on the year. Anhui Tianchang officially resumed the production after the overhaul in July, contributing to the major increase in output. In addition, many enterprises slightly increased the production to prepare for the approaching peak season. However, the domestic supply of battery scrap was still tight. Many enterprises increased the inventory of reduced lead and restocked raw materials. Therefore, the raw material inventory of secondary lead smelters addded 33,200 mt in July. Meanwhile, due to the power rationing in some areas of Anhui in July, the normal production of some smelters was affected. Owing to the longer duration of power rationing in some areas, the production of smelters in these areas has declined by about 20-40%, which may become the main factor disrupting the normal production of smelters in August.

Refined zinc

China's refined zinc output stood at 475,900 mt in July, down 12,600 mt or 2.57% on the month and 39,300 mt or 7.63% on the year. From January to July 2022, the combined refined zinc output is estimated to be 3.447 million mt, a decrease of 2.44% year on year.

SMM survey showed that the output of domestic refined zinc decreased in July and was less than expected. Yet the output still saw some increments. Some smelters in Henan and Qinghai resumed the production in July. The output of some smelters in Yunnan increased due to the supplement of zinc concentrate. The decline in output was mainly caused by the production control of some smelters in Shaanxi and the maintenance of smelters in Gansu. In addition, the output in Inner Mongolia fell amid the maintenance. Some smelters in Hunan were under routine maintenance and some small-sized smelters in Guangxi reduced the production due to the overhaul of mines.

China's refined zinc output is expected to increase by 35,100 mt to 511,000 mt in August, an increase of 2,100 mt or 0.42% on the year. From January to August 2022, the combined refined zinc output is estimated to be 3.958 million mt, a decrease of 2.08% year on year. The output is expected to increases as some smelters in Henan, Shaanxi, Inner Mongolia and Qinghai resume the production after maintenance. In addition, the output in Sichuan will increase as a smelter uses zinc hypoxide to produce. The output in Gansu is expected to increase significantly as a smelter gradually finishes the overhaul. The decrease in output is caused by the routine maintenance of a smelter in Anhui. Overall, the refined zinc output in August is expected to increase sharply mainly because the of the production resumption after maintenance. In addition, with the concentrated arrivals of imported zinc concentrate, the short-term supply problem is alleviated.

Refined tin

Domestic refined tin output was 4,980 mt in July, down 51.91% on the month and 56.02% on the year, and the combined output from January to July fell by 9.40% on the year, according to SMM research. In July, the domestic refined tin output decreased significantly as expected.

The output declined mainly due to the intensive maintenance and suspension of smelters. In terms of regions: 1. The output of smelters in Yunnan declined sharply on the month. Some large-sized smelters in Yunnan suspended the production for one month, which led to the huge decline in the output. Meanwhile, the finished products produced by smelters that resumed earlier contributed to the major output. 2. The output of smelters in Guangxi fell on the month because some smelters reduced the production due to the tight raw material supply. It is expected that production may recover in August. 3. The output of smelters in Jiangxi changed little. The output of large-sized smelters was stable. Although some small-sized smelters had no finished product output in July, but the impact on the overall output was limited. 4. The total output of smelters in other regions decreased slightly month on month in July. In general, most smelters had no output in July, and the resumption time of a few smelters had indefinite timeline as of when to resume production.

In August, domestic mainstream smelters gradually resume the production after the maintenance and a small amount of finished products have flowed out. According to SMM research, it is expected that the output will increase significantly in mid-August after smelters resume the production. Recently, due to the tight raw material supply, the TCs fall obviously. Some smelters plan to produce less due to the expected decline in profits and the impact of tight raw materials. To sum up, SMM expects the domestic refined tin output will increase significantly to 14,250 mt in August.

Refined nickel

China produced 16,000 mt of refined nickel in May, up 2.89% MoM and 29.71% YoY. The slight increase in the output in July was basically in line with expectations. The main reason was that orders placed by the alloy military sector increased and the demand for pure nickel increased amid the low SHFE nickel prices. However, as the overall shipment of steel mills was not smooth, the demand for pure nickel further decreased. Therefore, some salt factories suspended the production of refined nickel, but the impact was limited and the output still increased in July.

The output of refined nickel is expected to stand at 16,200 mt in August 2022, up 1.25% on the month and 10.11% on the year. It is expected that the output of refined nickel will still increase slightly in July, mainly because the refined nickel production lines of some salt plants are still being commissioned. Therefore, it is expected that the output will further increase in the future.。

NPI

China produced 31,100 mt of NPI in Ni content in July, down 8.82% MoM and 25.75% YoY. As the stainless steel market was weak amid the off-season, the demand for NPI declined. In addition, due to the inflow of Indonesia NPI, the market supply was in huge surplus. The output of high-grade NPI stood at 25,000 mt (Ni content), down 7.15% MoM in July. And the output of low-grade NPI was 6,100 mt (Ni content), down 15.11% on the month. Due to the overall supply surplus of NPI, the NPI prices fell sharply in July. Therefore, domestic NPI plants chose to suspend or reduce the production to contain the risks amid the high cost pressure. In addition, the output of 200-series stainless steel in the integrated steel mills decreased. Therefore, the operating rates and output of low-grade NPI both declined.

It is estimated that the NPI output in August will stand at around 30,500 mt in Ni content, and the market holds a cautious attitude towards the follow-up stainless steel market. In addition, with the increase in the Indonesia NPI output, the supply surplus may be more severe. In this scenario, the domestic NPI plants will lower the operating rates to slow down the increase in output. In the future, the market should pay attention to the recovery of terminal demand for stainless steel, which may underpin NPI prices. However, the increase in Indonesia NPI will still put greater pressure to the domestic market in the long term.

Nickel sulphate

China’s output of nickel sulphate was 30,000 mt in metal content in July, or 136,200 mt in physical content, up 10.8% on the month and up 23.7% on the year. In July, the output of battery-grade nickel sulphate increased significantly. As the profits of nickel sulphate produced with MHP was good, some enterprises favoured MHP on top of scrap and some cobalt sulphate enterprises indicated that they may transfer to produce nickel sulphate with MHP in the future. In terms of raw materials, the proportion of nickel sulphate produced with high-grade nickel matte was about 20%, the proportion of hydrometallurgy intermediate products stood at 51%, and the proportion of nickel briquette was about 2%. The rest was produced by scrap and crude nickel. In July, the inventory of battery-grade nickel sulphate further declined, and the supply for retail transactions tightened. Therefore, the prices rebounded slightly and profits expanded. In this scenario, salt factories were more willing to produce.

In August, integrated manufactures will continue to release the new capacity and the operating rates of some companies that reduced or suspended the production will increase. Therefore, the output in August is expected to rise 4.1% on the month and 10.7% on the year in light of lucrative profits. However, as the current MHP-based nickel sulphate capacity is unlikely to increase significantly, the output growth in August may be mainly contributed by high-grade nickel matte-based production line.

Battery-grade manganese sulphate

China produced 26,700 mt in physical content or 8,528 mt in metal content of battery-grade manganese sulphate in July, up 29.21% MoM and 50.61% YoY. The increase was mainly brought about by the production resumption of major enterprises in Guangxi and Guizhou. The orders and inquiries of precursor plants increased in July and August compared with May and June, but the prices of battery-grade manganese sulphate were still under pressure due to the high inventories.

In August, with the gradual increase in the output and sales of new energy vehicles, the demand for precursors will boom. Therefore, it is expected that the output in August will increase slightly by 5.25% on the month and 40.66% on the year to 8,976 in metal content.

High-carbon ferrochrome

SMM data showed that China's high-carbon ferrochrome output fell by 19,900 mt on the month and up 148,200 mt or 35.94% on the year to 560,600 mt in July. The output in Inner Mongolia was 307,600 mt, up 20,400 mt or 7.1% on the month. The output in Sichuan was 39,000 mt, down 7.8% on the month. In July, the purchasing prices disclosed by mainstream steel mills fell by 650 yuan/mt (Cr 50%). In addition, the output of stainless steel further declined. Therefore, the demand for high-carbon ferrochrome declined. Although the output of ferrochrome declined, the supply was still in surplus amid the weak demand, hence the ferrochrome prices fell. At the end of the month, due to the high costs, the operating rates of ferrochrome plants dropped significantly. However, the operating rates of most medium and large-sized ferrochrome plants in the north were still high because of the high-priced orders received in the early stage and the cost advantage. Therefore, the domestic high-carbon ferrochrome output dropped only slightly.

The output of high-carbon ferrochrome in August is expected to stand at 497,000 mt, lower than that in July. In the end of July, due to the weak demand and the supply surplus, Tsingshan Group is the first to lower the purchasing prices by 1,000 yuan/mt (Cr 50%) in August. Meanwhile, some steel mills reduce the purchase amount or even suspend the long-term orders. Therefore, the demand for ferrochrome further declines. As steel mills reduce the purchase volume, it is more difficult for ferrochrome plants to ship amid abundant supply for retail sales. In addition, the prices of chrome ore and coke have continued to fall, hence the ferrochrome prices decline further with weak cost support. Due to the low prices, ferrochrome plants mainly focuse on the orders received in the early stage. It is expected that the output will further decline after mid-August. However, the prices may continue to fall due to the weak demand and low costs.

Stainless steel

According to SMM survey, the domestic stainless steel output in July totalled about 2.3705 million mt, down 273,800 mt or 10.35% MoM and 18.76% YoY. The output of 200-series stainless steel stood at 651,000 mt, down 25.68% YoY; 300-series 1.3199 million mt, down 14.29% YoY; 400-series 399,600 mt, down 20.4% YoY.

In July, the output of series 200, 300 and 400-series stainless steel all decreased compared with June. The output of 200 and 400-series stainless steel dropped more significantly as steel mills tended to produce 300-series due to the poor profits of 200 and 400-series. Although steel mills chose to digest the inventory as early as in June, the overall decline of inventory was less than expected. In the first half of July, the steel prices further declined and the losses expanded. Therefore, many steel mills had to reduce the production to control the losses. In August, the output of 300-series stainless steel is expected to pick up. However, the output of 200 and 400-series is unlikely to resume significantly due to weak consumption. Moreover, as the decline in inventory is less than expected, steel mills will further reduce the production.

In terms of demand, although the consumption is expected to resume in august, it may not be able to recover significantly. The operating rates and restocking pace of downstream enterprises will be affected by the high temperature, but the overall demand will still be better than in July. Among them, the output of 200-series in August is expected to fall by 1.84% on the month while the output of 300-series is likely to increase by 7%. The output of 400-seriesmay fall by 11.39% on the month. Therefore, on the whole, the overall supply and demand of stainless steel will both increase slightly. SMM expects that the prices of stainless steel will decline slightly in August amid cost support.

SMM national stainless steel output statistical samples includes 35 steel mills, namely Dingxin Industry, Tsingtuo Nickel Industry, Qingtuo Industrial, Tsingshan Group, Guangqing, Beibu Gulf New Materials(Beihai Chengde), TISCO Stainless Steel, Zhangjiagang Pohang, Ansteel, Jiugang and Taishan Steel Group, Jiangsu Delong (including Danan project + Xiangshui phase II), Eastern Special Steel, Xinjinhui Stainless Steel Industry, Baosteel Desheng, Fujian Wuhang Stainless Steel Products, Fuxin Special Steel, Jiangsu Delong, Inner Mongolia Shangtai Industry, Yantai Walsin Lihwa, Huale Alloy, Yongxing Materials, Shandong Shengyang, Guangxi Jinhai, Liuzhou Steel Zhongjin, Guangxi Yongda Steel, Guangxi Xinfeng, Wolaidi Metal Material, Shenyuan Special Steel, Friendship Special Steel, Taizhou Huadi, Ningbo Dongmeng, Jiangxi Shengda and Ningbo Yiyue.

EMM

China produced 103,600 mt of EMM in July, up 5.82% on the month and 18.53% on the year, according to SMM statistics. The combined output in January-July totalled 463,000 mt, down 29.24% on the year. According to SMM research, the main output growth in July came from Hunan Province. The prices of EMM continued to fall in July. Meanwhile, downstream stainless steel mills reduced the production, hence the shipments of EMM were not smooth and transactions were few. Therefore, most EMM factories chose to reduce the production to control the losses. However, the output in Hunan Province increased obviously as the operating rates in June were relatively low due to the stricter environmental inspections and mine problems.

In August, amid the on-going manganese alliance meeting, the continuous decline in the transaction prices of EMM and the weak demand from stainless steel mills, the shipments of EMM are expected to remain poor. Therefore, the inventory accumulates and EMM factories hold a bearish outlook. In this scenario, EMM factories further reduce the production to control the losses. It is estimated that the output of EMM in August will stand at 45,900 mt.

Industrial silicon

China’s output of industrial silicon stood at 318,900 mt in July, an increase of 3.6% on the month and 17.5% on the year. The output totalled 1.9515 million mt in January to July, a year-on-year increase of 28.4%.

In July, the output in Yunnan rose significantly due to the release of new capacity of the silicon metal factories in Dehongzhou, Yunnan province. In addition, the output of the plants in Nujiang increased. Therefore, the output in Yunnan increased by about 19,000 mt. The production in Sichuan resumed earlier than in Yunan, but the output fell slightly by 5% on the month due to the tight hydropower supply and the environment problem. The operating rates in Xinjiang were high and the output rose slightly by 3%. The output in Fujian, Inner Mongolia, Shaanxi and other places decreased as the silicon factories reduced the operating rates amid the sluggish market and routine maintenance.

In August, the operating rates in Yunnan are stable. In Sichuan, silicon factories continue to reduce the production due to the lack of electricity supply caused by the drought. The new capacity of large-sized factories in the north will continue to be released. If the power supply in Sichuan remains stable, the output of industrial silicon in August is expected to increase slightly on the month.

Polysilicon

SMM data shows that in July, the domestic polysilicon output was 58,400 mt, down 4.58% on the month. The monthly supply of domestic polysilicon declined continuously in June and July. According to SMM research, domestic polysilicon enterprises basically maintained full production in the early stage due to the robust demand. In July, in order to ensure equipment and production safety, many major polysilicon enterprises successively carried out routine maintenance, including GCL and Daqo. In addition, two production lines of East Hope Group were suspended for the whole month due to an unexpected accident at the end of June. Therefore, the supply of polysilicon decreased immediately in July.

Silicon-manganese alloy

China produced 681,100 mt of silicon-manganese alloy in July, down 17.49% MoM and 20.05% YoY, according to SMM statistics. The combined output in January-July totalled 6.215 million mt, down 8.05% on the year. According to SMM research, on the one hand, although the prices of raw materials dropped sharply, most factories used high-priced raw materials purchased in the early stage, hence the factories were less willing to ship. On the other hand, due to the high temperature, the progress of real estate, infrastructure and other projects was slow, hence the traders and steel mills were less willing to purchase amid the weak terminal demand. Therefore, the spot inventory of silicon-manganese alloy was high and the supply exceeded the demand. In this scenario, factories reduced or suspended the production to prevent further losses, hence the output of silicon-manganese alloy declined in July.

In August, as the prices of raw materials are low and are unlikely to increase in the future, the profits of factories will recover amid the low costs. In addition, amid the recovery of terminal demand, steel mills plan to resume the production. In this scenario, the output of silicon-manganese alloy in August is expected to increase to 720,100 mt amid the improved profits.

Magnesium Ingot

According to SMM research, domestic magnesium ingot output dropped to 69,000 mt in July 2022, down 15% from the previous month. The output totalled 570,000 mt from January to July, up 24.16% year-on-year.

Domestic magnesium plants have begun their summer overhaul, and the output in China fell somewhat. Some factories still plan to overhaul in August, and the overall output of magnesium ingots is expected to decline further in the future. The sales staff of a large magnesium factory said that due to the weak demand in the magnesium ingot market, the prices remained low, putting severe cost pressure on the factories. Meanwhile, the hot weather cooled down the production enthusiasm, and the equipment was waiting to be overhauled urgently, so the production cut and overhaul started in early July. The resumption of normal production depends on the future market trend.

Although the prices of magnesium are in a slow downward trend, the falling trend will be curbed somewhat by the further drop in output. In August, domestic magnesium ingot output is expected to maintain a downward trend, which is about 65,000 mt, amid the weak demand.

Magnesium alloy

China's magnesium alloy output stood at 27,900 mt in July, up 12.94% MoM and down 8.91% YoY, according to SMM statistics. The output totalled 179,400 mt from January to July, a year-on-year decrease of 21.08%.

The average operating rate of magnesium alloy industry stood at 49.20% in July, up 12.94% MoM and down 13.19% YoY. As the prices of magnesium ingots trended lower in July, the market quotation of magnesium alloys was lowered accordingly. Therefore, the price acceptance of end-consumers increased, and some downstream enterprises of magnesium alloys chose to build the stock. The trading volume of magnesium alloys increased, and the operating rate of magnesium alloy plants also climbed. A salesperson from a large magnesium alloy plant revealed that recently the domestic and overseas orders for magnesium alloys were sufficient in that the low prices of magnesium had boots the downstream purchasing. Thus the magnesium alloy output in August is expected to be flat from July at 28,000 mt amid strong demand.

Magnesium powder

China's titanium dioxide output stood at 6,500 mt in July, down 5.13% MoM, and the output totalled 49,000 mt from January to July.

The domestic magnesium powder production maintained a downward trend in July, and the sluggish demand of domestic and overseas steel mills led to a sharp decline in the orders some magnesium powder factories received. The person in charge of a magnesium powder factory commented that the dropping average operating rate of magnesium powder factories was justified amid the traditional off-season and the losses of the steel mills, which reduced the operating rates of downstream enterprises and weighed on the overall demand for magnesium powder further. Considering that the supply is less likely to recover in the short term, it is expected that the magnesium powder market will remain sluggish in August with an estimated output of 6,300 mt.

Pr-Nd oxide

Domestic output of PrNd oxide in July amounted to 5,750 mt, down 3% month-on-month. The decline mainly resulted from the reduced production in Jiangxi, Jiangsu, Fujian, Shandong and other provinces.

The domestic supply in July was modest, while the demand was relatively weak. The ion ore supply was still relatively insufficient. In July, the output of raw ore in Myanmar gradually increased, while the domestic output was small expect for the output in Hunan. Therefore, Chinese enterprises were still highly dependent on the ion ores imported from Myanmar. The production of Pr-Nd oxide in Jiangsu fell 6% month-on-month. Some raw ore separation enterprises suspended the production of Pr-Nd oxide in July due to the short supply of raw ore, and the production is expected to resume in August.

In Jiangxi, the output of Pr-Nd oxide dropped 6% on the month. Some raw ore separation enterprises maintained stable production, and some scrap separation enterprises slightly cut the production.

The outputs of Pr-Nd oxide in Shandong and Fujian declined 5% and 9% respectively. Due to weak demand and insufficient scrap supply as well as the enduring losses, metal plants were less willing to purchase, and some even reduced the production by a small amount. The Pr-Nd oxide output in August is forecast to rise slightly.

Pr-Nd alloy

The domestic output of Pr-Nd metals in July stood at 4,895 mt, down 5% on a monthly basis. The output reduction was mainly attributed to the falling production in Inner Mongolia, Jiangxi and Guangxi.

In July, the magnetic material enterprises were less willing to purchase Pr-Nd metals as they received fewer new orders and the rare earth market was sluggish. Metal factories received relatively small orders, and the high temperature in summer increased the cost of electricity. The production of Pr-Nd metals in Inner Mongolia diminished by 8% month-on-month, some metal factories in Baotou reduced the production, and the production of rare earth processing enterprises in north China was stable.

The metal factories in Jiangxi, Guangxi and Chengdu all received flat orders, and the output of Pr-Nd metals in the above three provinces declined by 10%, 8%, and 43% respectively from June. The Pr-Nd metals output in August is expected to inch lower.

Molybdenum concentrate

SMM data shows that the domestic molybdenum concentrate output was about 19,900 mt in July, up 200 mt or 1% from the previous month.

In July, the domestic molybdenum prices fell continuously, but the bid volume from steel mills increased steadily, which, according to incomplete statistics, had exceeded 10,000 mt. With a slight recovery in demand, the operating rate of domestic molybdenum mines rebounded slightly. The overall supply also increased slightly, but had not returned to high levels yet.

Ferromolybdenum

SMM data shows that the domestic ferromolybdenum output amounted to about 17,100 mt in July, up 1,000 mt or 6% on the month.

The main reason for the increase was that the domestic bid volume from steel mills in July was over 10,000 mt, an increase of about 2,000 mt compared with that in June. Motivated by the steadily increasing demand of the steel mills, the smelters were willing to produce and the productivity of ferromolybdenum picked up slightly.

Silver

According to SMM survey, the domestic silver output stood at 1,379.6 mt (including 1,179.6 mt of mineral silver) in July, up 11.51% from the previous month. The output varied in different plants, but the production of most plants rose, which contributed to the significant increase of the total output. On the macro front, on July 27, the US Federal Reserve announced a 75 basis-point interest rate hike, raising the target range of the federal funds rate to between 2.25% and 2.5%. This was the fourth time the Fed had raised interest rates this year and the raise of 75 basis points was also the second time in a row. The US Federal Open Market Committee issued a statement on July 27 after the conclusion of its two-day monetary policy meeting that the lingering high inflation was induced due to a supply and demand imbalance, rising energy prices and broader price pressures caused by Covid-19 pandemic. In addition, the conflict between Russia and Ukraine and related events also weighed on the inflation. The committee said it would “pay close attention to the risks of inflation" and continue to significantly reduce the size of its balance sheet. Fed Chairman Powell said at a news conference after the monetary policy meeting that the Fed planned to look for "compelling" evidence of easing inflation in the next few months and raise interest rates further. He also claimed that it might be appropriate to propose an "extraordinarily sharp rate hike" in the the September meeting. In terms of the silver production, the companies that cut the production radically in July were limited, which included Yunnan Copper, Jinlong Copper, Hongqian Nonferrous Chemicals, Baiyin Nonferrous, and Zijin Mining. At the same time, the companies that increased the production were obviously growing, such as Henan Jinli Gold Lead, Hunan Yuteng, Hunan Shuikoushan, Yanggu Xiangguang Copper, Zhejiang Hongda, Jiangxi Longtianyong, Guiyang Yinxing, and Huludao Nonferrous Metals. In addition, the increase in output was also substantially greater than the decrease, hence China’s overall production of silver in July still increased steeply. It is expected that the domestic silver production will continue to grow in August.

Notes: SMM has released Chinese silver output since February 2021. The silver is usually produced along with copper, lead and zinc. Thanks to its high coverage of the base metals industry, SMM has successfully investigated a total of 45 silver production enterprises, which are located in 17 provinces across the country, with a total capacity of 24,000 mt and a total capacity coverage rate of over 95%.

Silver nitrate

Despite of the off-season, the output of silver nitrate increase by 12% on the month due to the domestic production of silver powder. According to SMM, the output of silver nitrate in July was 542 mt, up 12% on the month.

The output in central China rose 16% on the month mainly due to the increase in the demand of silver powder. In addition, as the prices of silver nitrate fell and stabilised in mid-July, downstream enterprises purchased on dips. The output in east China and south China remained stable as enterprises remained normal production. The output in the north-west region increased by 11% on the month, mainly because the some manufacturers increased the production lines.

The downstream enterprises increased the use of domestic silver powder to control the costs. Therefore, the demand for silver powder and silver nitrate increased, and SMM expects that the output of silver nitrate will increase slightly in August.

Titanium dioxide

According to SMM, China's titanium dioxide output stood at 324,800 mt in July, 2022, down 4.41% MoM and up 9.17% YoY. The output totalled 2.3263 million mt from January to July, a year-on-year increase of 5.57%.

SMM survey shows that the titanium dioxide market remained sluggish in July, and most orders were placed out of rigid demand. As a result, the titanium dioxide factories were facing greater pressure amid high inventory, and the quotations of small and medium-sized factories were falling. The average operating rate also decreased. The person in charge of a large titanium dioxide plant in southwest China revealed that due to poorer trades, the plant lowered its output by 15% in July. As for when the production will return to a normal level, it depends on the follow-up market orientation. Affected by the traditional off-season, the prices of titanium dioxide also dropped considerably. The downstream demand was limited, and traders were more cautious in taking orders. The terminal consumers preferred to wait and see, and thus mainly placed orders on rigid orders. It is expected that the titanium dioxide market will remain weak in August with an estimated domestic output of about 320,000 mt.

APT

SMM data shows that China’s output of APT in July dropped 12% from June to 110,000 mt.

It is learned from some APT smelters that the limited terminal demand for alloys along with the declining operating rates of powder companies and the difficulty of purchasing raw materials on dips put smelters under dual pressure. On the one hand, the APT prices were hovering around the cost line; on the other hand, the demand of the European market was relatively weak amid the summer break, leading to diminishing orders. Amid a sluggish market, most private enterprises reduced the operating rates in order to contain losses and only maintained the delivery of long orders; a small number of smelters chose to suspend the production for maintenance with the purpose of reducing costs and increasing efficiency.

The domestic smelters were still scheduling their maintenance plans, and APT production is expected to remain stable in August.

Antimony ingot

According to SMM survey, China’s antimony ingot (including antimony ingot, converted crude antimony, cathode antimony, etc.) output in July 2022 fell 6.55% month-on-month to 7,377 mt. On the whole, the enduring tight supply of antimony raw materials still inhibited the growth of domestic refined antimony production. In recent months, the domestic demand for antimony products, especially the antimony oxide, has been sluggish. The consumption dropped dramatically in July, and the export orders also shrunk significantly. Many suppliers of antimony oxide even reported that the export orders had halved since the beginning of the summer. The poor sales of antimony oxide also affected the purchase or production of refined antimony by antimony oxide manufacturers, which dampened the willingness of antimony ingot manufacturers to produce. Judging from the production situation in July, basically all the manufacturers that SMM had investigated had cut their production, and a large number of manufacturers had suspended the production. Among the 32 survey respondents, the manufacturers who suspended the production in July added one to 14 compared with June; 13 reduced their production, flat from the number in June, and 6 maintained normal production. For example, Flash Star Antimony, one of the largest antimony producers in China, stopped its antimony production again on July 25, 2022, with all its blast furnaces and antimony white furnaces shut down. It is expected that the enterprise’s output in August will also be affected by the suspension. The resumption time has not yet been determined. SMM predicts that the supply and demand of the domestic antimony products market in August will remain basically unchanged under the current economic situation, especially with the continuous weak demand. It is expected that the domestic antimony ingot production in August may be flat from July.

Notes: SMM starts to disclose the output of antimony ingots (including antimony ingots, converted crude antimony, cathode antimony, etc.) since May 2022. Thanks to high coverage of the antimony industry, SMM has successfully investigated a total of 33 antimony ingot manufacturers, which are located in 8 provinces across the country, with a total capacity of nearly 20,000 mt and a total capacity coverage rate of over 99%.

Lithium carbonate

China’s lithium carbonate output stood at 30,319 mt in July, down 4% MoM and up 53% YoY. As some manufacturers started the overhaul in July, the operating rate of production lines trended lower. In addition, some manufacturers reduced the production due to the shortage of ore materials, and the overall supply was tighter. Although newly commissioned capacities in some smelters ramped up the production, and the output of the salt lake was at its peak, the overall supply still dropped slightly. With some manufacturers completing the maintenance in August, the output is expected to gradually recover. This, coupled with the ramp-up in new capacity, will motivate the overall supply to rise month-on-month. China lithium carbonate output in August is estimated at 32,691 mt, up 8% MoM and up 57% YoY. Due to the rapid changes in the industry dynamics, and in order to ensure the accuracy and reliance of SMM data, SMM has added 1 lithium hydroxide sample company since July 2022.

Lithium hydroxide

China’s lithium hydroxide output stood at 19,847 mt in July, a MoM increase of 7% and a YoY growth of 43%. As some manufacturers started maintenance one after another in July, and the tight ore supply of some manufacturers weighed on the production and operation, the lithium hydroxide output dropped significantly. Some causticising producers still maintained a sufficient supply to gain the profits, but the overall supply inched lower. It is expected that some large smelters will complete the maintenance in late August, which, coupled with the output of causticising plants stabilising at a high level, is likely to stimulate the overall supply of lithium hydroxide to trend higher. China’s lithium hydroxide output is estimated at 21,990 mt in August, up 11% MoM and 40% YoY.

Cobalt sulphate

China’s cobalt sulphate output was 6,292 mt in July, a month-on-month decrease of 2% and a year-on-year increase of 14%. On the supply side, the prices of cobalt sulphate fell sharply in July, resulting in enduring losses, so most intermediate-based cobalt salt plants maintained or cut the production. In July, due to the rising popularity of lithium recycling, smelters that use recycled materials stockpiled a large number of raw materials to expand market share, leading to an increase in the production of recycled cobalt salts. Most large precursor manufacturers increased the production, and the some with cobalt salt smelting capacity continued to relied more on their in-house production of raw materials, driving the production of cobalt salts to exceed the demand. The demand for cobalt salt slightly improved in July, and the manufacturers mainly consumed in-house cobalt salt, thought the purchase demand improved slightly compared with the previous month. The small and medium-sized precursor manufacturers mainly purchased on rigid demand. It is expected that the lithium recycling sector will continue to increase in August, and the leading precursor plants are likely to increase self-produced products. The cobalt sulphate output is forecast to be 6,547 mt in metal content in August, a month-on-month increase of 4% and a year-on-year growth of 15%.

Tricobalt tetraoxide (Co3O4)

The output of domestic Co3O4 stood at 4,219 mt in July, down 29% MoM and 39% YoY. July marked the beginning of the third quarter. On the supply side, due to a large backlog of finished product inventories in the tricobalt tetraoxide enterprises, the production in July did not return to a normal level. The tricobalt tetraoxide enterprises still maintained low production or suspended the production, which caused a extended supply-demand imbalance in the digital electronics market. On the demand side, at the beginning of the third quarter, the weak demand of digital electronics showed no signs of improvement. The tricobalt tetraoxide enterprises that received modest orders purchased about once a week, and the downstream consumers still purchased based on the orders at hand. In the short term, the inactive Co3O4 market will hardly improve, and the low production of the tricobalt tetraoxide enterprises is expected to extend to August. The output of Co3O4 is estimated at 4,301 mt in August, down 2% MoM and 41% YoY.

PCAM

China’s PCAM (precursor of cathode active materials) output was 69,194 mt in July, up 3% on the month and 36% on the year. On the supply side, the output of major precursor companies recovered in July, with a steady increase in downstream demand. It is learned that a leading precursor company recovered its rationality after stepping up the production, and its inventory dropped slightly in July. In addition, the production recovery of small and medium-sized enterprises was relatively slow, hence the overall market supply grew slightly. On the demand side, the demand of domestic motive power market continued to ramp up, that of some battery companies increased significantly, that of the European motive power market slightly weakened, and that of the digital electronics market was still poor. Generally, the overall demand extended the increase. It is expected that leading precursor companies will release new capacity in August, and the terminal demand for motive power products will sustain growing. The PCAM output is estimated to add 4% on a monthly basis to 72,107 mt.

NMC cathode materials

China’s NMC cathode material output was 54,825 mt in July, a month-on-month increase of 4% and a year-on-year increase of 45%, With a further growth of downstream vehicle sales in the domestic market, the orders for cathode active materials were also lifted, most of which were contributed by the LFP orders. The orders for NMC cathode materials were relatively poor. In terms of the overseas markets, the terminal demand of Europe market was weak, while the demand of the US market grew slightly. Therefore, the overall NMC power battery picked up slightly. At the same time, the demand of the digital electronics market was feeble, so the overall increase of NMC cathode materials demand was limited. In terms of products, the output of the 5 series dropped slightly, while the output of the 6 and 8 series advanced slightly. The fluctuations in the 5- and 6-series output were mainly because that the downstream battery cell factories had switched the battery specification. The 8 series saw a slight increase in output thanks to the recovery of some overseas orders, but the uncertainty remained in terms of the sustainability. In addition, some companies released new production capacity in July, and the capacity will continue to ramp up in August. Considering the continuous recovery of downstream demand, the overall supply is expected to rise further. The NMC cathode material output is forecast to amount to 59,454 mt in August, up 8% MoM, which shall be higher than the monthly growth rate of July.

Iron phosphate

The domestic iron phosphate output stood at 69,122 mt in July, up 27% MoM. On the supply side, the production lines of some crossover enterprises reported good performance in the shakedown test, and the ramp-up of capacity was relatively smooth. It is learned that the production capacity of a start-up had been fully released and the shipments were delivered in batches to the downstream consumers. Other start-ups also released a small amount of production capacity for downstream doping. At the same time, the new production lines of leading enterprises were put into operation immediately, which boost the total supply of iron phosphate. On the demand side, terminal demand continued to improve in recent months, and the demand for upstream LFP and iron phosphate showed a obvious upward trend. The capacity and production of downstream LFP companies also expanded rapidly. Some LFP enterprises that used to rely on self-produced raw materials began to source iron phosphate as the supply gap of iron phosphoric enlarged due to different production expansion cycles between LFP and iron phosphate. As a result, the demand for iron phosphate climbed, boosting the production. The domestic iron phosphate output is estimated to increase 17% MoM to 80,602 mt in August.

LFP

In July, 94,694 mt of LFP was produced in China, an increase of 211% YoY and 28% MoM. On the supply side, new LFP capacity continued to be released in July as many leading enterprises, such as Hunan Yuneng, Shenzhen Dynanonic, Jintang Times, and some crossover enterprises had relatively smooth shakedown tests of production lines and ramp-up of new capacity. Driven by the high terminal demand, the production jumped immediately. Accordingly, the supply increased significantly and the growth rate is expected to remain high in the short term. On the demand side, the demand for motive power and energy storage improve further in July with sharply growing production and sales. The downstream orders for LFP increased steadily, driving the production to surge. It is expected that 113,571 mt of LFP will be produced in Augutst, an increase of 216% YoY and up 20% MoM.

LCO

The domestic LCO material output was 5,582 mt in July, up 2% from the previous month and down 20% from the previoius year. On the cost side, the prices of tricobalt tetraoxide fell, while the prices of lithium carbonate stabilised at a high level. The cost of LCO declined further, which drove the prices of LCO to fall. On the supply side, the scheduled production of LCO companies was relatively low in July, and most companies continued to have high inventories, hence the average operating rate was low. On the demand side, the demand for digital 3C in July did not see palpable increase, and LCO battery factories still purchased LCO materials as needed. The orders of terminal consumers in July sharnk significantly compared with the same period in previous years. Generally speaking, the high penetration rate of mobile phone narrowed the room for its market growth, and the driving force of consumption was gradually declining due to a lack of innovation, leading to falling replacement demand. Consequently, the trades involving the LCO industrial chain were quieter than the previous years. However, the demand is expected to grow in September when there will be launches of new mobile phones. Therefore, the output in August, when most companies will restock for production, is expected to trend higher than July. The output of LCO material in August is expected to rise 7% on the month and drop 14% on the year to 5,949 mt.

LMO

China’s LMO output stood at 5,459 mt in July, down 35% YoY, but up 37% MoM. The terminal demand for LMO picked up recently, and the demand for mobile power supplies, smart wear and electric tools also increased. Moreover, as the high LMO prices still sustained, the downstream enterprises increased their purchases on dips, leading to an increase in LMO output. The output of LMO is expected to fall 19% YoY and 20% MoM to 6,572 mt in August.